3 Steps to Avoid Financial Hangover from Year End Shopping Spree

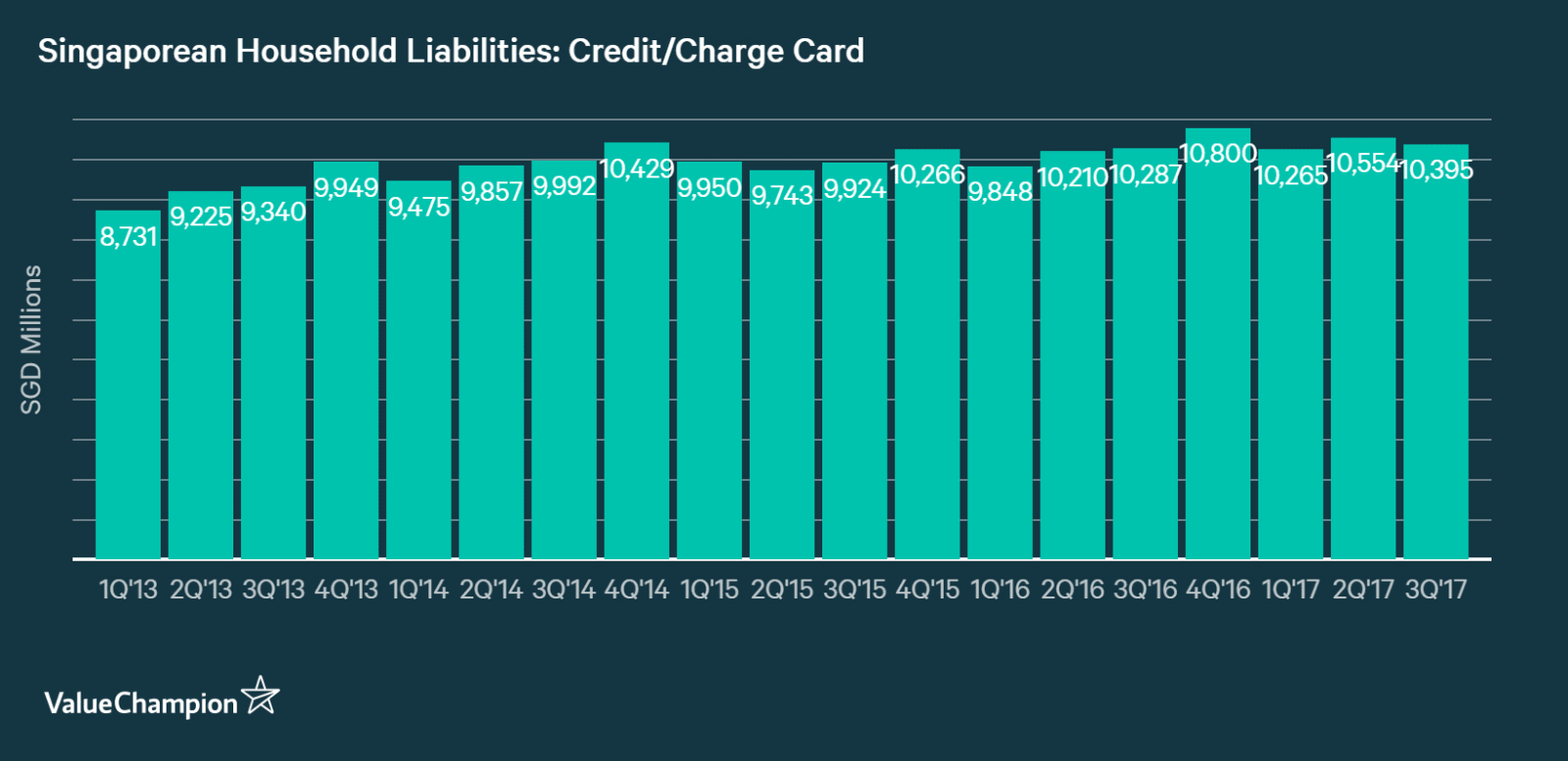

With all the sales events and holidays that take place from November to December, it's easy to end up with a big credit card balance by January. For instance, the year end shopping spree has generally increased the consumer credit card debt in Singapore by 5% from September to December in the past 4 years. At this rate, total card debt in Singapore could reach almost S$11bn in 2017, a record high.

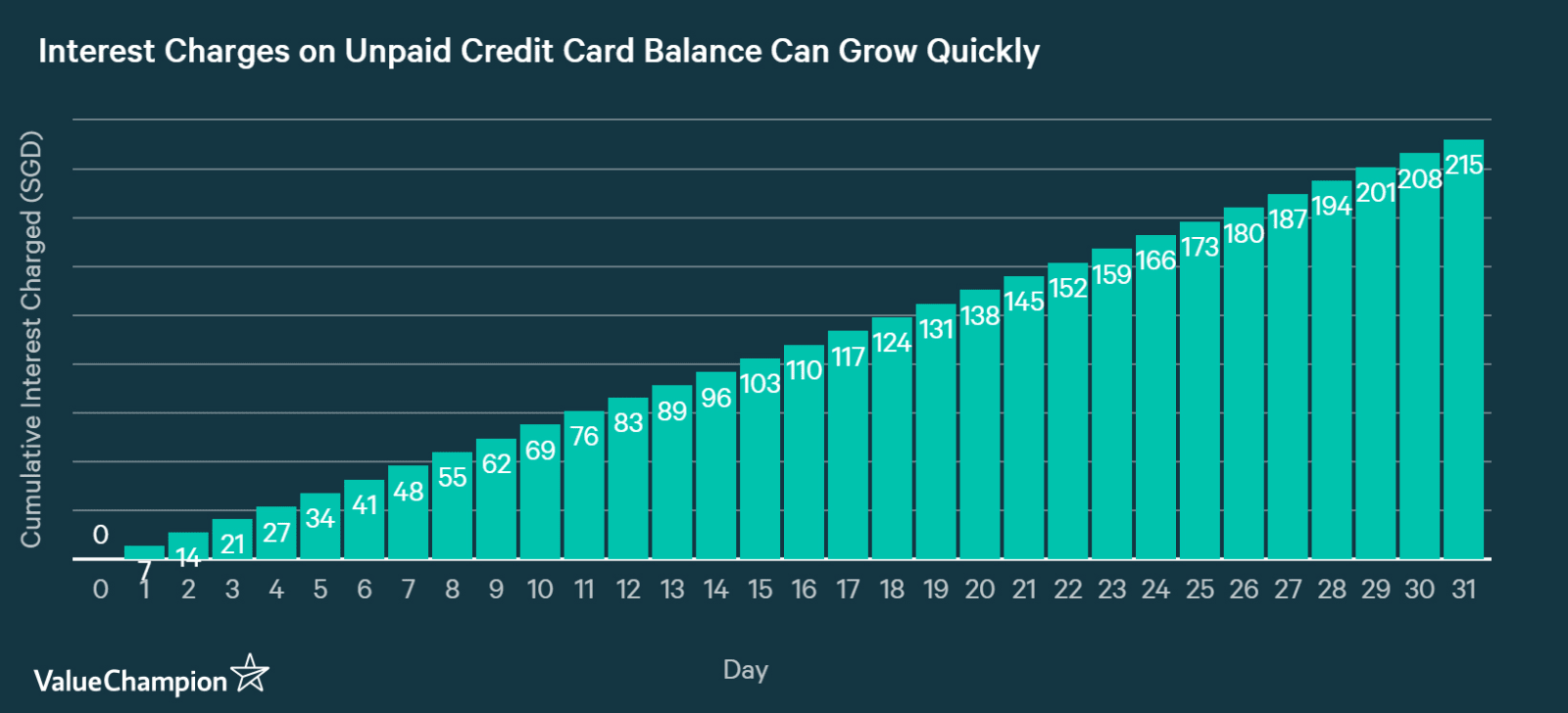

However, this practice of heightened holiday spending can be quite dangerous. Because people tend to spend more than they can typically afford, excessive seasonal spending can often lead to months of interest charges and late payment fees for an overeager spender. Credit cards charge an especially high interest rates that are around 25%-29% that compound your balance daily; if you were to leave an overdue balance of S$10,000 on your card, your balance could grow by more than S$200 in just 1 month. Not only that, this cost is only going to balloon faster as interest rates are expected to increase in 2018. If you find yourself in shock about how much money you owe on your card, it's time for you to start making detailed plans to reduce your balance to zero as soon as possible.

1. Stop all non-essential expenditures & repay as much of card balance as possible

To do so, the first step to take is to immediately stop all non-essential expenditures. Non-essential refers to any discretionary spendings like purchases, entertainment or travel. You should limit your spending to daily necessities like buying groceries, paying rent and utilities, and commuting to and from work. The key concept here is to allocate as much of your money as possible to repaying the loan with the highest interest rate. Typically, credit cards tend to carry the highest cost, with personal loans being the next. However, some loans from money lenders can be even more expensive than either of the two, so you should prioritize them if you have any.

Precaution: No matter what, you have to avoid merely satisfying making the minimum payment requirement on your card. Doing so will exempt you from late payment penalties, but it won't prevent interest charges from accruing.

2. Consider getting a balance transfer or a debt consolidation plan

If you still have a sizable balance left after step 1, you should seriously consider getting a balance transfer or a debt consolidation plan (DCP). These facilities are designed to help debtors manage their loan repayment more easily. For example, balance transfers provide interest-free periods of 3 to 18 months for a small upfront fee, and hence are ideal for repaying a relatively small credit card balance. On the other hand, debt consolidation plans combine all of your personal debt (including card balance) into one that can be managed down over a few years, which work more smoothly for people who have built a sizable balance of tens of thousands of dollars.

3. Stick to a plan

The last step is actually an advice for a permanent behavioral change. Once you've gotten a balance transfer or a DCP, you have to create a disciplined budget for the next few months (or years) so that you can satisfy their repayment schedules on time. Otherwise, you will eventually face more late payment penalty fees and even higher interest rates. Even if you are free of debt, you should always have a plan to save a predetermined amount of money on a regular basis, and to plan your expenditures ahead of time. Instead of making impulsive purchases, for example, you should create a holiday shopping budget for yourself, and save up for it ahead of time. Doing so can even help you save hundreds on your vacation expenditures, as early bookings tend to be much cheaper than last minute ones.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.