4 Smart Ways To Spend Your First Paycheck

Getting your first paycheck is something to remember. For most, we cannot forget how the crisp check felt in our hands when we first held it. It doesn't take long for disappointment to set in as we see taxes, CPF retirement deductions, and other expenses carve out what we bring home. For others, you were surprised with how much you've earned and could think of a dozen ways to spend it all in one evening. Whichever the case, let's not dwell on the makings of a nostalgic memory until you are much older. Instead, here are a few prudent and practical things to do with your first paycheck.

Prioritise Debt

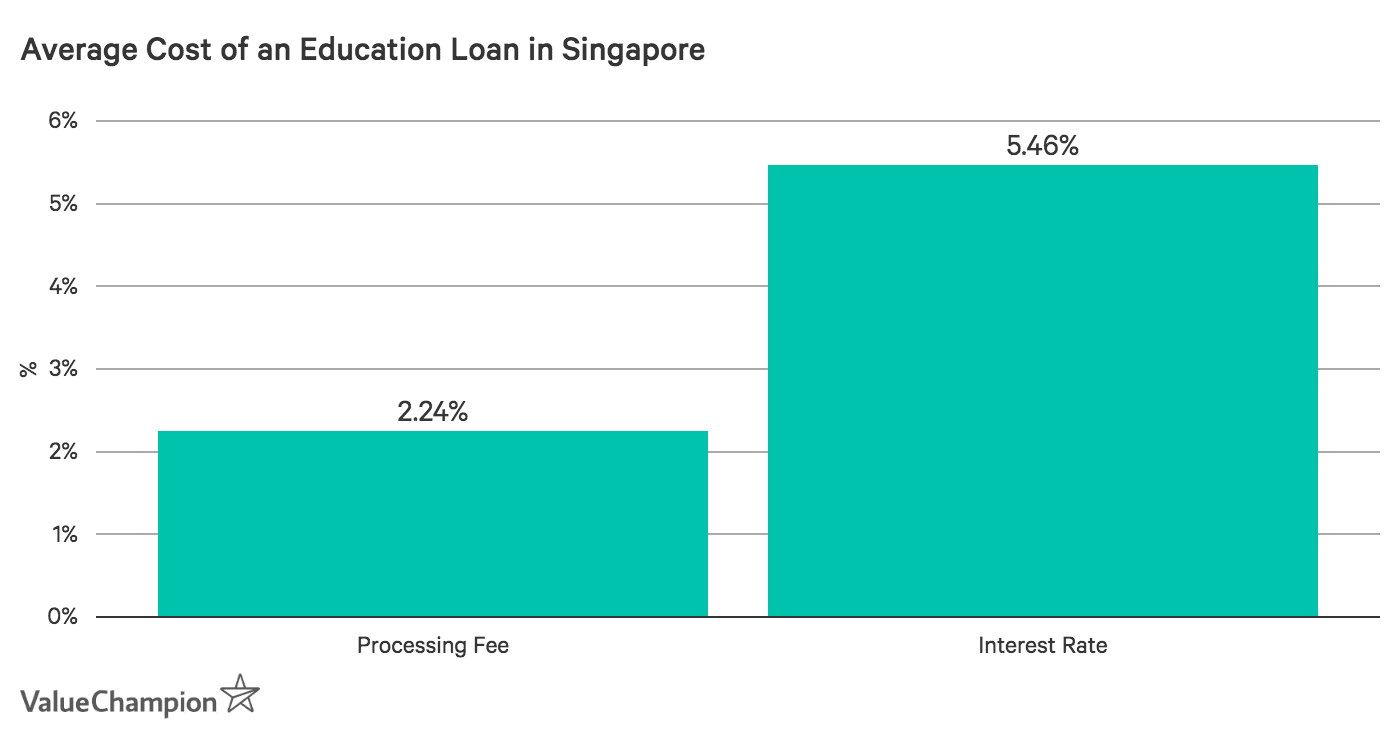

Most Singapore students are working while attending school. The last thing you want to think about is the 4 years of debt you've been incurring—especially if you took on an interest-servicing education loan in Singapore. Unfortunately, what we really ought to hear is often what we don't want to hear. Prioritise your debt first. The reason is simple. The longer you take to pay off debt, the more interest you pay over time.

If you have credit card debt instead, your priority should be to reduce this debt as quickly as possible. Credit card debt usually has higher interest rates for younger individuals building credit. So make it a priority before buying that new mobile phone. Ignoring debt will not only negatively impact your credit rating but will end up being significantly more expensive.

Pro tip: If you have multiple sources of debt (i.e., education loans, personal loans, credit card debt), pay off the debt with the highest interest rate first. Then begin moving down the list with the goal for you and your family to become debt-free.

Budget Out the Essentials

It may seem strange that this isn't at the top of the list. The truth is we often inflate what we deem as essential. So in the interest of prioritizing debt over often unnecessary "essentials" (i.e., the best mobile phone plan, monthly subscription services, etc.), it has been moved slightly down the list.

This by no means suggests essentials are not as important as clearing your debt. In fact, when we think of a budget, it usually begins with rent, utilities, and food. Rightfully so. Unfortunately, not everyone makes a budget to start, let alone a prudent one. Make it a habit to be more conservative and cut out the "fat," so to speak. This is your first paycheck, not your last. Create healthy spending habits early and give yourself a fighting chance to build up your wealth.

Pro tip: Monthly subscriptions and expenses add up and are not so obvious to track. Schedule out a few times a year to regularly inspect your bank statement to see what automatic subscription services are draining your wallet. It may be worth it to ask yourself: are subscription services slowly making you poor?.

Save Early and Familiarize Yourself With Compound Interest

The Singapore government automatically allocates earned income into retirement contributions and your Medisave account. Aside from this, you should consider automating additional savings for a rainy day. This is your safety net. No matter how large or small, set up automatic deposits into a savings account for emergencies. The total amount is entirely up to you. However, a good rule of thumb is between three to six months worth of expenses.

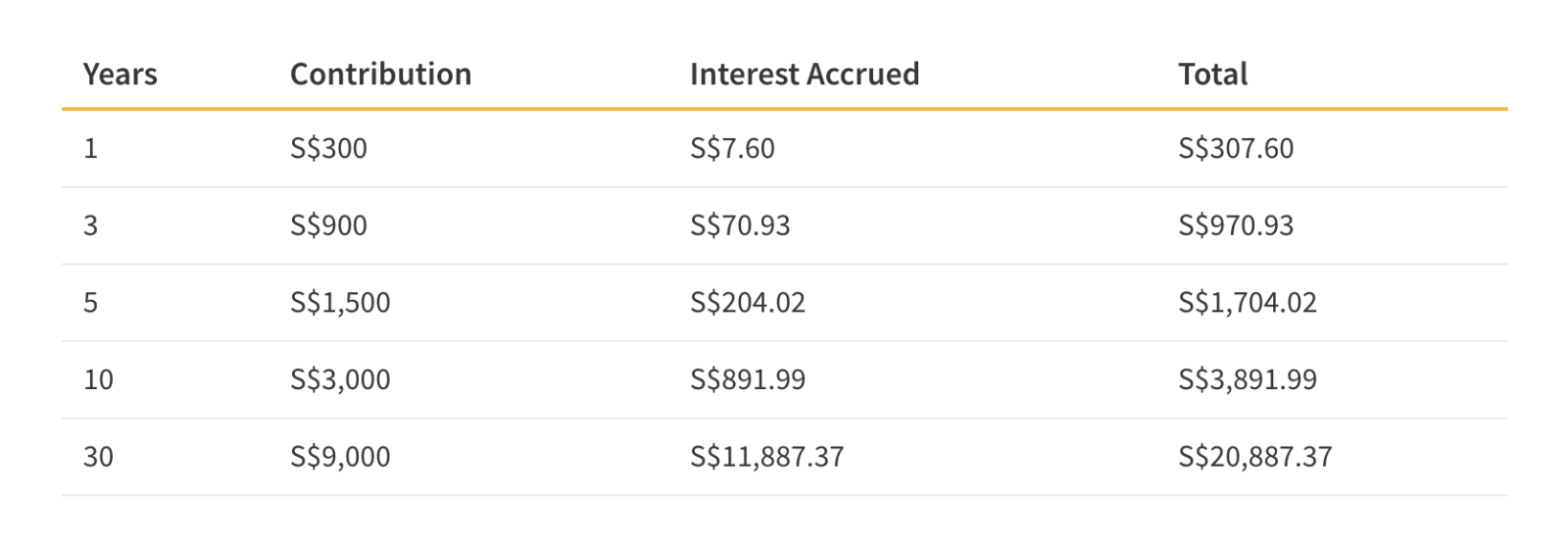

Additionally, educate yourself on compound interest and take advantage of high-interest savings or investment accounts now. Let's see what happens if you manage to put away S$25 per month in a brokerage account for a conservative rate of return of 5% per year.

Even S$25 a month can make a difference in your early 20s. The longer you continue to contribute to a brokerage account, the more you take advantage of this exponential growth. With savvy new applications and trading platforms, Singaporeans can begin investing immediately with as little or as much as they can afford.

Play

If you've made it this far down the list, you've done your due diligence. You are on the road to becoming a personal finance guru, and your first paycheck survived the onslaught of responsible budgeting. It may be laughable to include this—especially after following the first 3 steps—but you deserve some fun. You might not be able to book a private jet off the island, but spend a little on yourself for this special moment. You've earned it. Take yourself out to a special dinner and expand your food budget for the month. Treat yourself to a pedicure or whatever simple pleasure is worth your while. You will have many more paychecks to come.

Stephen Lee is a Senior Research Analyst at ValueChampion, specializing in insurance. He holds a Bachelor of Arts degree in International Studies from the University of Washington, and his prior work experience include risk management and underwriting for professional liability and specialty insurance at Victor Insurance. Additionally, Stephen is a former US Peace Corps Volunteer in Myanmar (serving between 2018-2020), where he continues to provide business development consulting services to HR companies in Asia Pacific.