4 Ways To Grow Your Savings Fast

While it's great to have a savings account, it's not news that typical savings account interest rates are quite low, making it tough to make a considerable return by just having your money lie there. Whether you have a lot of savings or not too much, there are several ways you can "put your money to work" to plan for your future. We listed four great ways to grow your savings faster in a little-to-no-risk environment.

Open a Regular Savings Plan Account

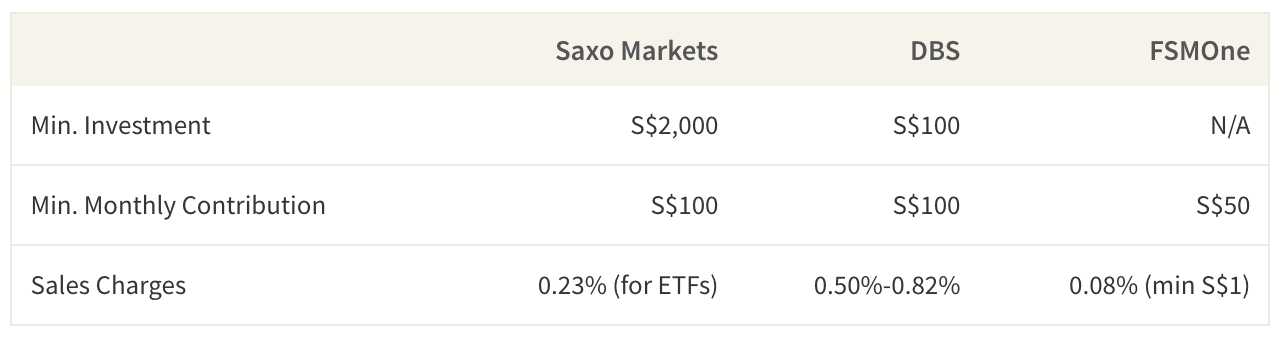

Regular Savings Plans (RSPs) are great for those looking for high returns over a short period of time. This is because the money that you put in monthly is invested into the stock market, so both your account and the interest earned on it grow in tandem. Furthermore, unlike dabbling in the stock market yourself, RSPs (also known as monthly investment plans) use dollar-cost averaging with your monthly contributions, so you can average out the price of the investments you are buying.

Regular Savings Plan Fees for Saxo Markets, DBS, and FSMOne

Some of the more successful accounts can yield around 3-20% per year, which is significantly higher than regular bank's saving account effective interest rates (EIR) of 1.23% per annum. This means that moving some of your money from your regular savings account to an RSP could help you turn your idle money into a high-growing potential cash flow. While the risk of negative returns is possible, the stock market has shown long-term average returns of 8-10% per year. This means that S$10,000 in your savings account that earns only around S$100 of interest per year can end up making 8-10 times more just on interest over the long-term when it's placed in an RSP.

Switch to a High-Yield Savings Account

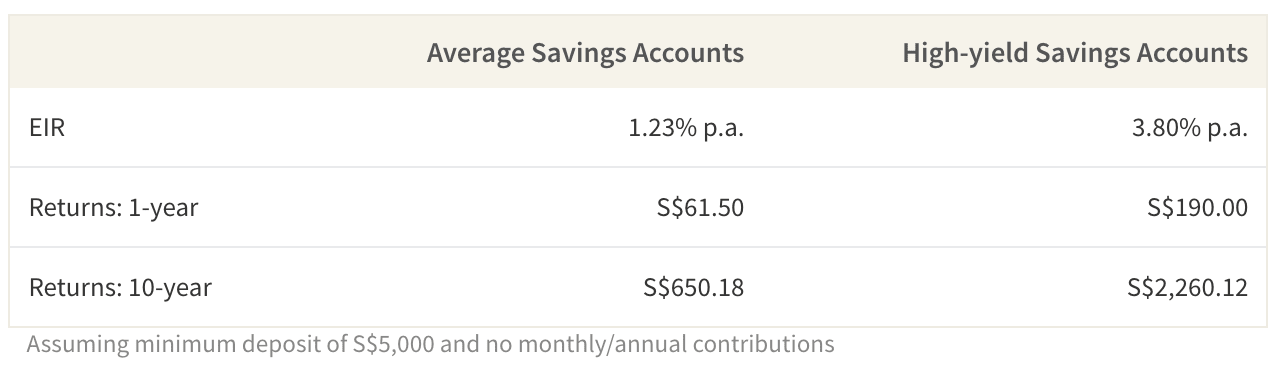

While you may be satisfied with your current savings account, another bank could offer you great promotions, higher EIRs and higher returns than your current bank. Switching your accounts could lead to higher returns in the long-run. For example, in 10 years, you could earn 32% more by moving your funds to a higher-yielding account.

Projected Earnings from an Average Savings Account vs High-Yield Saving Account

Higher rates typically accompany higher initial deposits or high daily balances. For example, DBS is currently offering 3.80% interest per year but requires a minimum daily balance of S$3,000. POSB, on the other hand, only requires a minimum daily balance of S$50 and offers high interest rates of 2.25% per annum. To find the best savings account for you, it is worth "shopping around" with your requirements in mind.

Invest in State-Backed Bonds and Bills

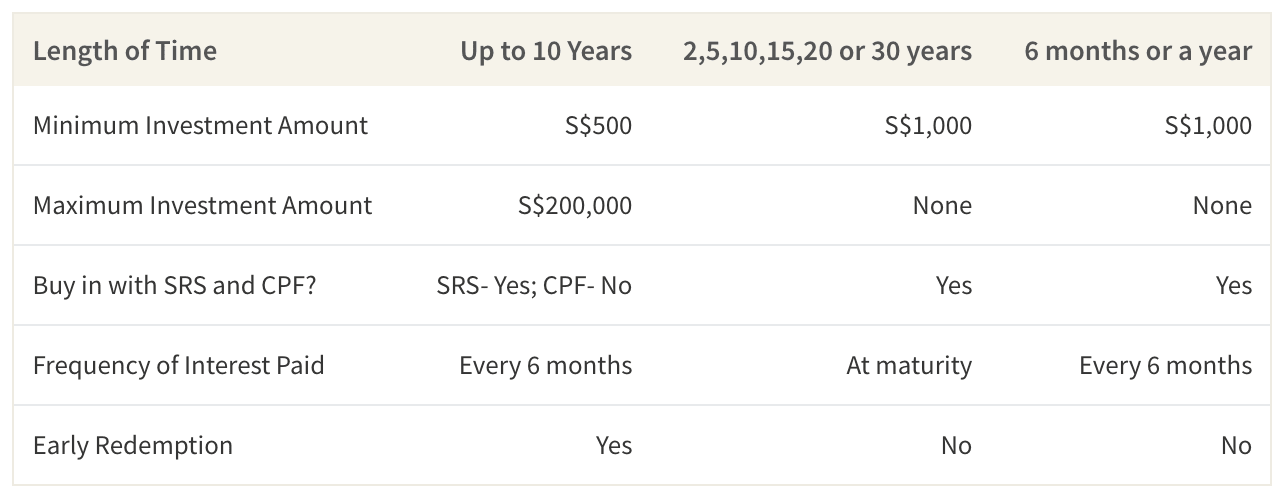

Another way to put your savings to use is to invest in government-backed bonds and bills. Those who want a no-risk option could get a Singapore Savings Bond (SSB), but you should note that the average return over 10 years is currently just 0.90% per annum. Alternatively, you can consider Singapore Government Bonds (SGB), as their coupon rates (yields) can even go up to 3.375% p.a. depending on the maturity date. Lastly, you can also consider treasury bills (T-bills) are securities issued for 6 months or for a year at a time and yield 0.19%-0.27% per annum. Though these interest rates are lower than any of the options here, T-bills are useful if you want a low-risk and secure investment.

Comparison of SSBs, SGS Bonds, and T-Bills

To get an SGS or a T-bill, you have to auction online. One of the pros of SGSs and T-bills as opposed to SSBs is that you will receive payments every six months based on the interest rate. For instance, if you invest S$15,000 in a 30-year SGS bond at 1.87% p.a., you will receive S$140.63 every six months until your bond reaches maturity.

Another thing to keep in mind is that you could reinvest the interest earned or keep it for your own use, making it a great alternative to simply having a savings account. When deciding among the three options, you should consider how long you want to put the money away for, if you would like an early redemption, and how much you wish to tuck away at the moment.

Top Up Your CPF

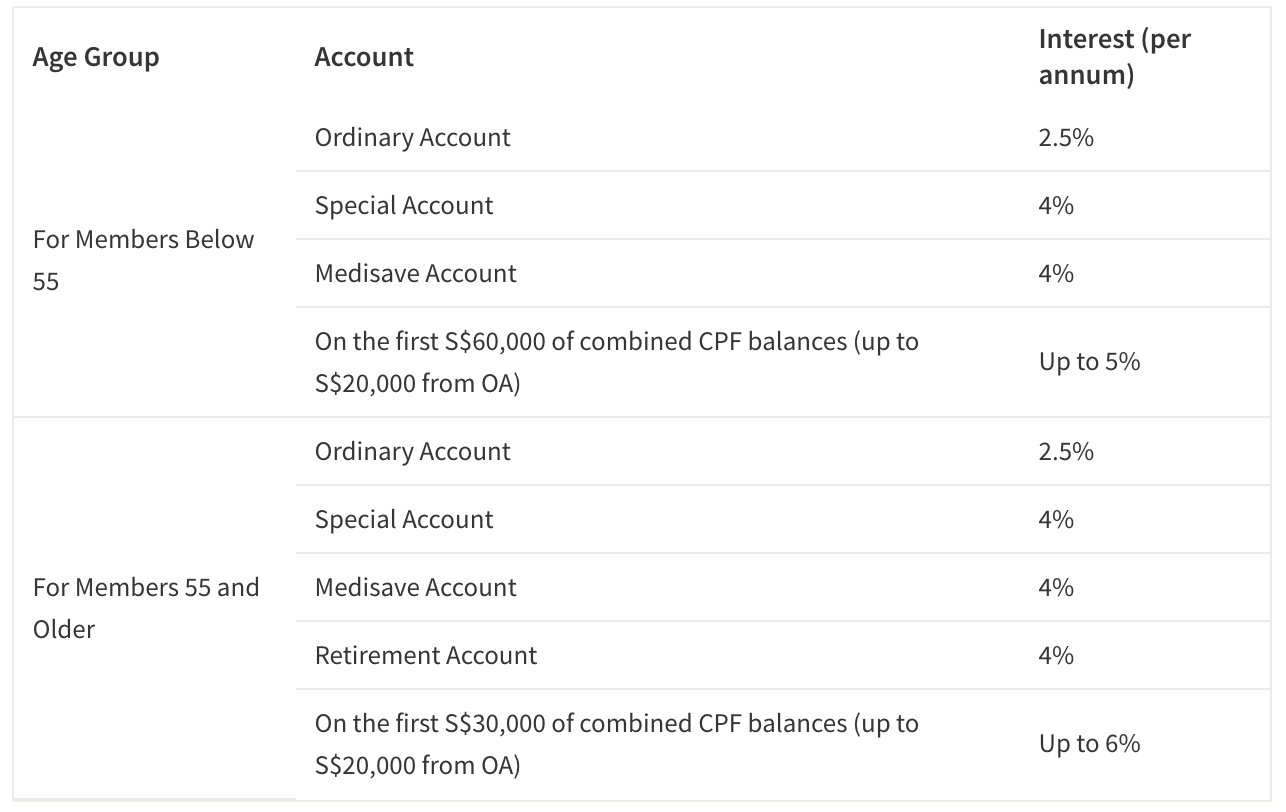

With many Singaporeans worried worried about their ability to fund their retirement, it might be a good idea to funnel some of your savings into your Central Provident Fund (CPF). With the Retirement Sum Topping Up Scheme, higher balances correspond with higher interest that you can earn on each account. For example, a member who is younger than 55 and has a combined balance in their accounts of at least S$60,000 can get up to 5% interest per annum. If a member is 55 or older and has a combined balance of S$30,000 or more, they can earn up to 6% in yearly interest. For both scenarios, the maximum amount counted in your Ordinary Account towards that milestone is S$20,000.

Interest Rates on Different CPF Accounts According To Age Group

Aside from great interest rates, tax relief is another benefit to encourage you to partake in this scheme. You can get tax relief of up to S$14,000—S$7,000 for topping up your own account and an additional S$7,000 for topping up your parents, parents-in-law, grandparents, grandparents-in-law, spouse or siblings accounts. To get tax relief for cash top-ups for your spouse's or sibling's CPF accounts, their salary must not exceed S$4,000 per year or they must be handicapped. Top-ups are irreversible, so it is best for those looking for a locked-in, long-term plan to earn wealth on their savings.

How To Choose Which One is Best for You

In order to choose the best way for you to put your money to use, it's worth thinking about how much you would like to put away and what your risk preferences are. For example, if you already have a set amount aside that you wish to take out at any time, you could switch to a high-yield savings account. If, however, you don't mind locking away your money for a while at a time, you should consider a regular savings plan, investing in no-risk bonds, or topping up your CPF retirement account.

You should also consider the amount you will pay into this fund over time, as regular savings plans require monthly minimums to keep those accounts active. If you would like to take more risks with your savings, you could also consider investing online. Regardless of what you choose to do, making sure you are actively saving, whether small or large amounts, will be crucial in helping you ultimately achieve financial independence.

Anya is a Research Analyst for ValueChampion who focuses on loans and investments in Singapore. Previously, she assisted global consultancies, hedge funds and private equities with primary research at a high-growth fin-tech based in London. A graduate of the University of Oxford and King's College London, Anya is currently interested in applying quantitative research to help consumers make better financial decisions.