5 Reasons Why Spotify Is Not the Netflix of Music

Spotify's stock market debut last week has been creating a lot of buzz. Bulls have been bidding up Spotify's stock price to $150, implying a market capitalization of $27bn. People who are bidding Spotify's stock believe that Spotify has potential to be the Netflix of music. Granted, this argument could seem sensible given that 90% of Spotify's revenue comes from subscription instead of advertising. However, we believe this analogy is broken, and that Spotify's valuation is unjustifiable at its current levels. Below, we discuss some crucial differences between Spotify and Netflix's business models, and what ramifications they have on Spotify's value.

Music and Video Are Inherently Different

One of the biggest reasons why the music industry is different from the video industry is that professional quality music is comparatively much cheaper to produce than professional quality video.

Arguably, a talented musician (or a small group of talented musicians) with a guitar, computer, microphone and a keyboard can produce a pretty good song of 3-5 minutes in length. To enhance their work further, they could also rent a studio for $400 to $2,000 per day to create an album. All in all, it's quite possible for a professional quality album to be produced for under $10,000 to $50,000.

On the other hand, TV shows and movies are still incredibly expensive to produce. Producing a blockbuster movies is known to easily cost hundreds of millions of dollars, while TV shows typically cost several million dollars to produce. Even the smallest of microfilms can cost several hundred thousand dollars to million dollars.

Incentive of Producers

This difference in production cost have significant ramifications on what the producers of these works are incentivised to do. For instance, low cost of production makes it very easy for a single musician (or a small group of musicians) to produce music on her own, leading to a comparatively large number of both musicians and songs available in the market. Consequently, large supply of music makes it very difficult for any musicians to stand out from the crowd, which creates a downward pressure on the price that artists are able to charge for their songs (unless you are already a famour musician like Taylor Swift, Jay-Z or Beyonce). Given this, most musicians are incentivised to distribute their music on as many platforms as possible to maximise their chance of being discovered, garnering fans and making money.

In contrast, high production cost requires video producers to find a significant financial support even before they start filming, because they need a large staff of actors, actresses and filming crew on top of all the expensive equipments and filming sets. Therefore, they are incentivized to look for 1 highest bidder that will put up the initial capital to create a show or a movie. Those said sponsors, like Disney, Netflix and HBO, also have to be sizable companies that can invest in several of these content to diversify their risk, since it's still difficult to predict which show or movie will be successful. This dynamic necessitates that both producers and sponsors of professional quality video are relatively few in number compared to producers of music, which grants the content owners the freedom to decide how they monetise the content.

The Need to Build an Exclusive & Proprietary Content Library

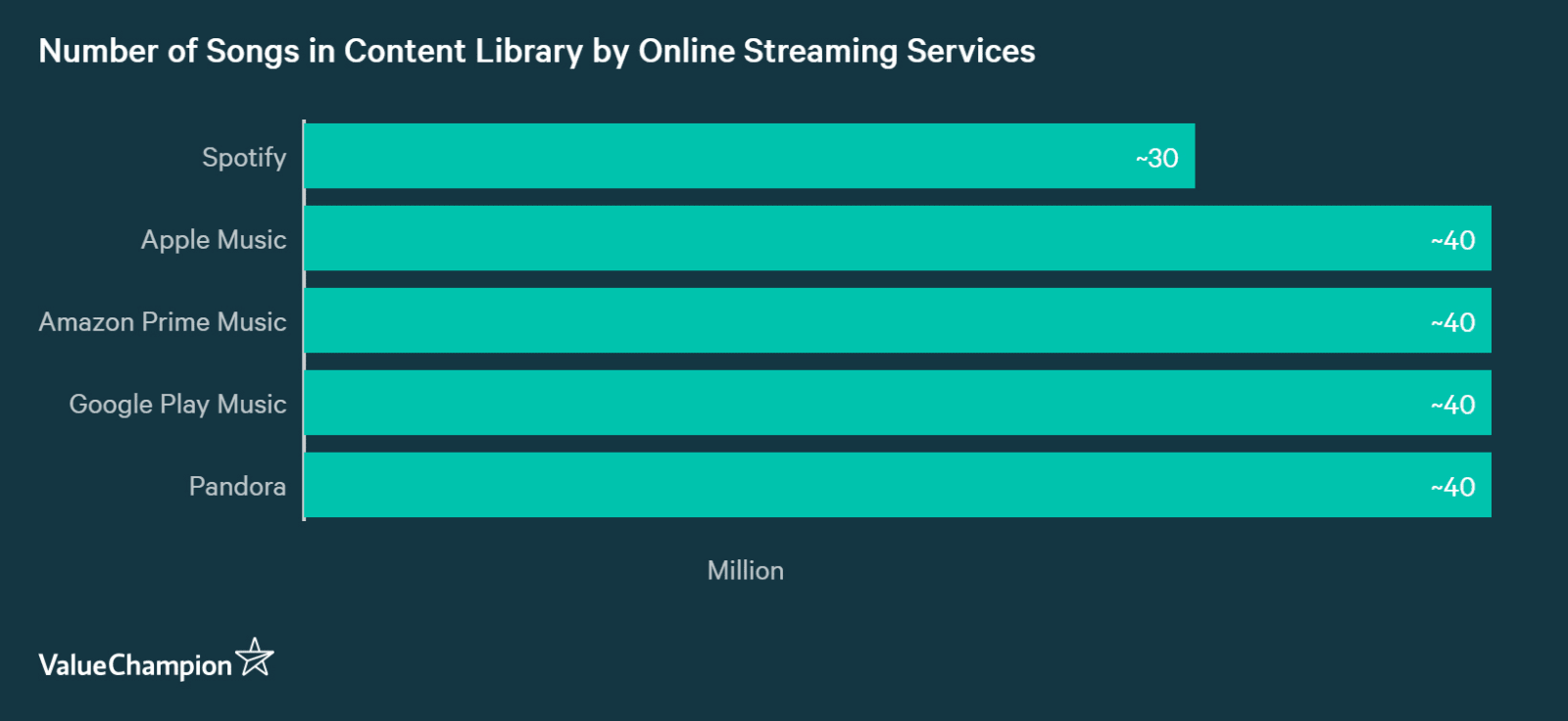

Then, what our discussion above implies is that it is extremely difficult for Spotify to build its own library of original content and set itself apart from its competition, the way Netflix has done in the last several years. Music needs to be available everywhere for its economics to work, while video can be kept proprietary to one platform. In fact, just about every song you can find on Spotify can also be found in Youtube, Apple Music or Amazon Prime Music. In contrast, video streaming sites have all built a very proprietary content library that differentiates each of them from their competitors. While Netflix continues to spend billions of dollars to strengthen this advantage, the only thing Spotify can do is to pay for music rights to get songs that all of its competitors also have.

Therefore, the competitive landscape in video streaming is completely different from what it is in music streaming. In video, each service is complementary: subscribing to Netflix doesn't prevent a consumer from also subscribing to HBO or Amazon Prime Video. For music, however, each service is a substitute: a Spotify subscriber has no incentive to also subscribe to Apple Music, and vice versa.

Pricing Power

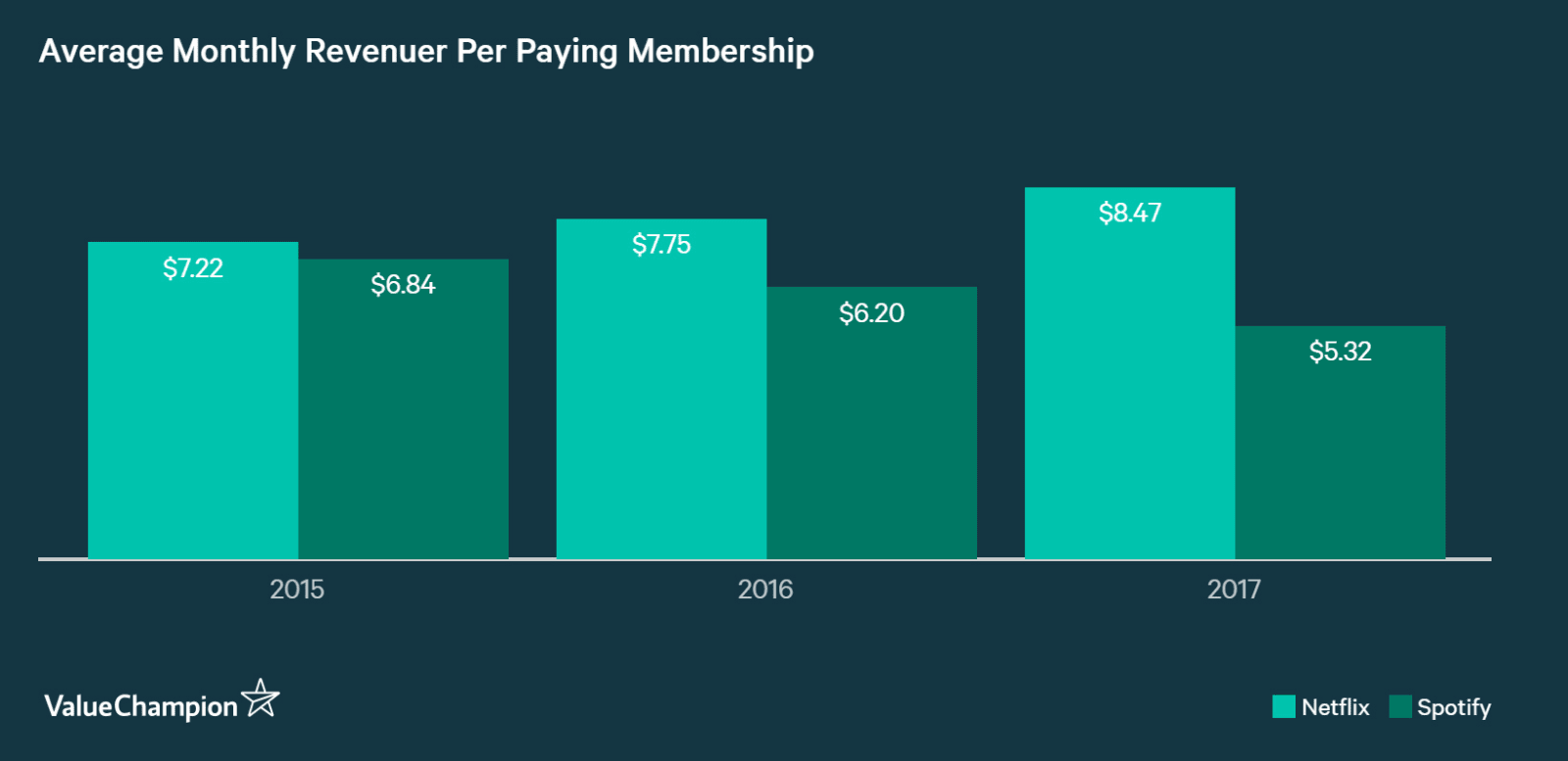

Selling a service that provides the same set of music that people can find elsewhere makes it extremely difficult to make a profit. Essentially, the only effective way of competing in such a situation includes cutting price, branding and providing a better user experience through user interface. Admittedly, Spotify seems to have done well on the last two. However, while Spotify has kept its $9.99/month subscription fee for several years, it has been effectively decreasing its average price by providing cheaper packages for families and students. In contrast, Netflix has been steadily increasing its subscription prices for several years, barring occasional negative impact from adverse foreign currency fluctuations.

Cost of Acquiring Users

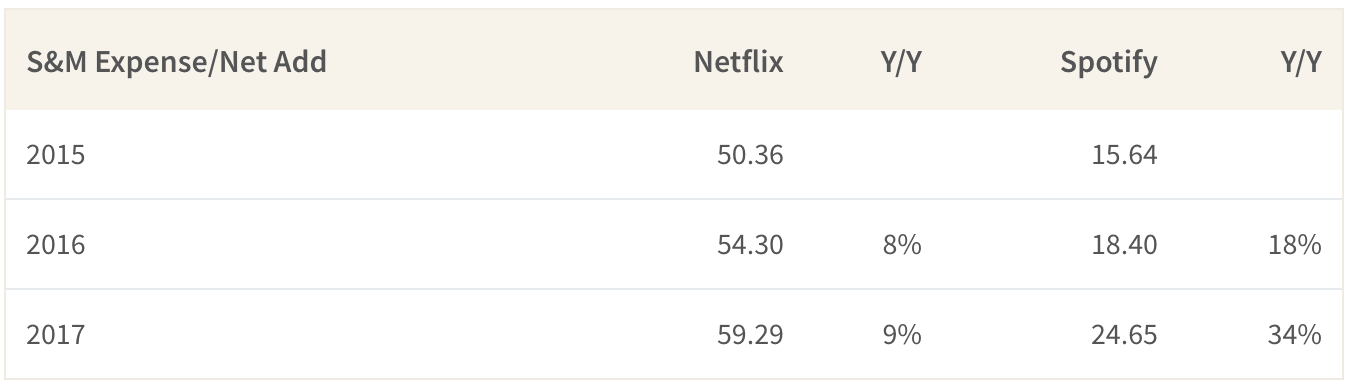

While Spotify has been controlling its content cost reasonably well, it seems to have no control of another major cost item: marketing. By calculating how much money it spent on sales and marketing per each subscriber it gained in a year, we can calculate how much it costs for Spotify to gain and retain a new subscriber. As you can see below, this cost called subcriber acquisition cost ("SAC") has been soaring incredibly quickly for Spotify, growing 34% in 2017. That convincing users to pay for Spotify instead of Apple Music or Amazon Prime Music is becoming increasingly difficult makes sense intuitively because they all seem to offer the exact same service. While SAC has been rising for Netflix as well, the pace of increase has been a lot milder and Netflix also has other benefits that we discussed above that can compensate for this trend (i.e. original contents, pricing power and complementary competition vs substitutory competition). On the other hand, it will be extremely difficult for Spotify to become profitable without being able to control its SAC or raise its prices.

As a side note, we are using subscriber net add figure to estimate SAC because Netflix does not provide enough information to use subscriber gross add in our calculation. Cost of acquiring a new subscriber was closer to $17 for Spotify when using gross add. However, the trend in increasing cost was consistent for both figures.

What Does Today's Valuation Imply?

While the fact that Spotify is receiving a higher valuation than Snapchat, Twitter or Expedia is already somewhat surprising, the juxtaposition of Spotify and Netflix is particularly interesting since both are subscription services for digital entertainment. Clearly, Spotify has built a great product and possibly a brand that has garnered a huge consumer support around the world. However, it doesn't enjoy any of the structural competitive advantage that Netflix possesses. Given this, the stiff valuation discount that Spotify receives compared to Netflix in terms of Enterprise Value to Sales ratio (or even EV/Subscriber ratio) seems more than justified.

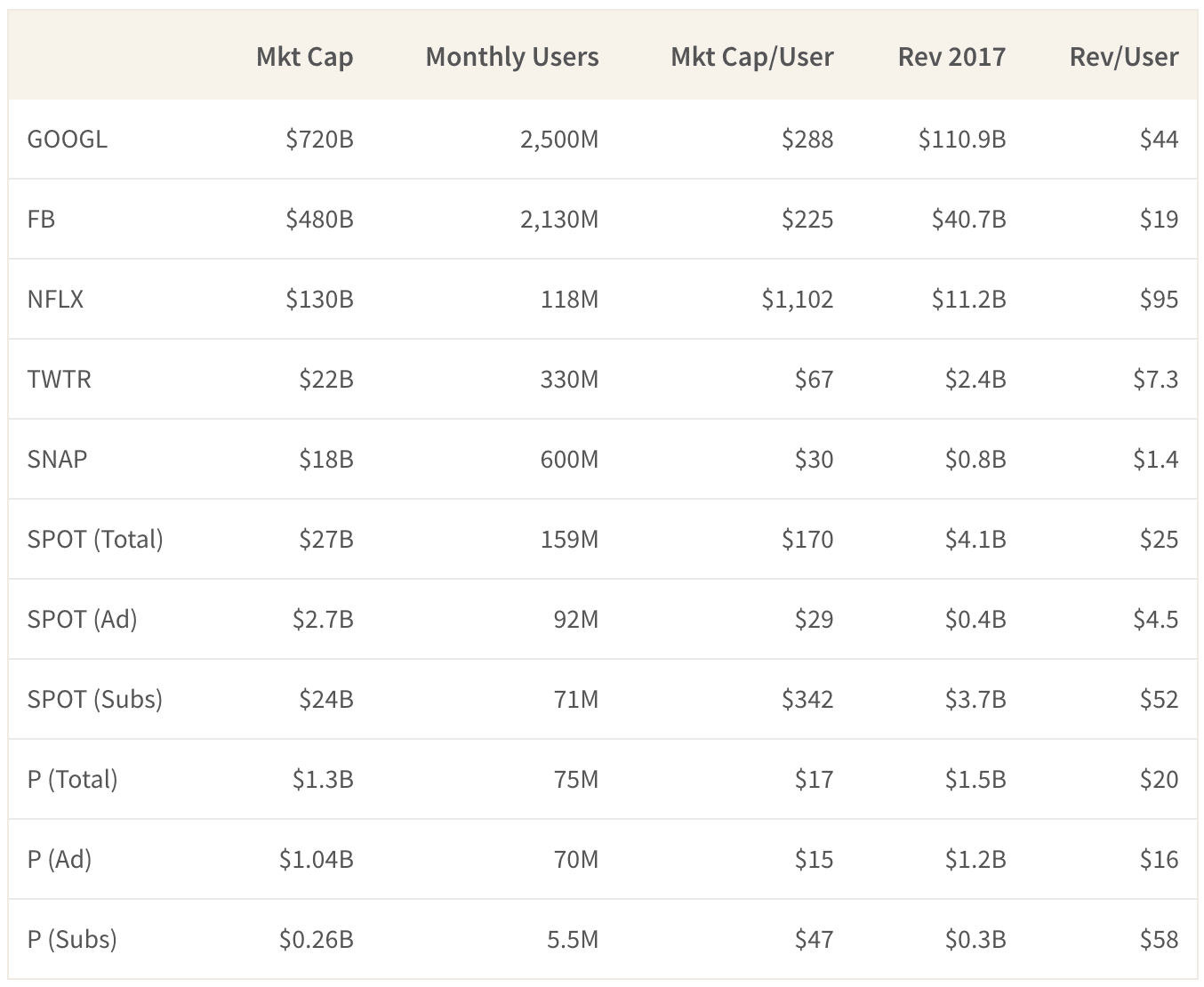

However, although Spotify and Netflix both are online subscription services, Netflix may not be the right point of comparison for Spotify for the reasons we explored above. Instead, other leading internet companies like Google and Facebook provide another interesting insight into Spotify's valuation. Although they are free to use services without paying subscribers, both Facebook and Google have some of the most loyal and sticky user bases in the world. Spotify makes about $50 of revenue per subscriber (or $26 per user) on an annual basis, and receives a valuation of $340 per subscriber (or $170 per user). Google makes $45 per user, and receives a valuation of about $300 per user, while Facebook makes $20 per user with a valuation of $225 per user. Considering the fact that Spotify is highly unprofitable and lacks a truly differentiated product, it is rather shocking that it is able to garner similar valuations as two of the best internet companies that have ever existed. Not only that, Pandora actually monetises its paying subscribers and free users better than Spotify, but receives a valuation that is a fraction of that of Spotify's.

To be worth $27bn, Spotify needs to quadruple its revenue, create a profit margin of at least 10%, and be valued at a healthy multiple of 25x PE ratio sometime in the 3 to 5 years. Giving this company that much credit for growth and profitability, both of which are highly uncertain, seems overly speculative. Not only that, Spotify's listing was not even an IPO. It was a direct listing where the company itself raised zero capital and its founding CEO sold more than half his shares for personal profit. To achieve the remarkable growth it needs to be worth $27bn without any additional capital to backstop its rapid cash burn while competing against gigantic competitors like Apple and Amazon sounds like a gargantuanly difficult task.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.