5 Things To Do When You Can't Pay Your Home Loan

A recent OCBC study surveying 2,000 Singaporens at random found that 31% of study participants between the ages of 21 and 65 are having difficulties paying off their home loans. This disheartening statistic is unsurprising considering that the COVID-19 pandemic resulted in many Singaporeans losing their jobs or experiencing pay cuts. If you are having difficulties paying off your home loan, you might have thought about your options. So what can you do if you cannot pay back your home loan? We've evaluated some of the actions you can take below.

1. Check With Your Bank To See if You Can Change the Terms of Your Loan

Several measures were put in place earlier in the year to alleviate financial hardship during the pandemic. If you have been more recently been affected, there are still steps you can take. For example, if you have not already received an email from your home loan provider, it may be worth checking to see if they are reducing costs for their customers. Some banks like DBS, OCBC and HSBC are currently charging a reduced monthly rate of 60% your usual loan amount until next year. If you find repayment still difficult, try setting up an appointment to talk to your loan provider. They could extend your loan tenor or show you other options available.

2. Refinance

If interest rates are low, it might be worth refinancing your home loan. Essentially, refinancing is when you replace an existing home loan with a new one with new conditions. Refinancing is a great option for borrowers who might need to reduce their payments and spread it out over a longer period of time. However, there are times when you should and should not refinance.

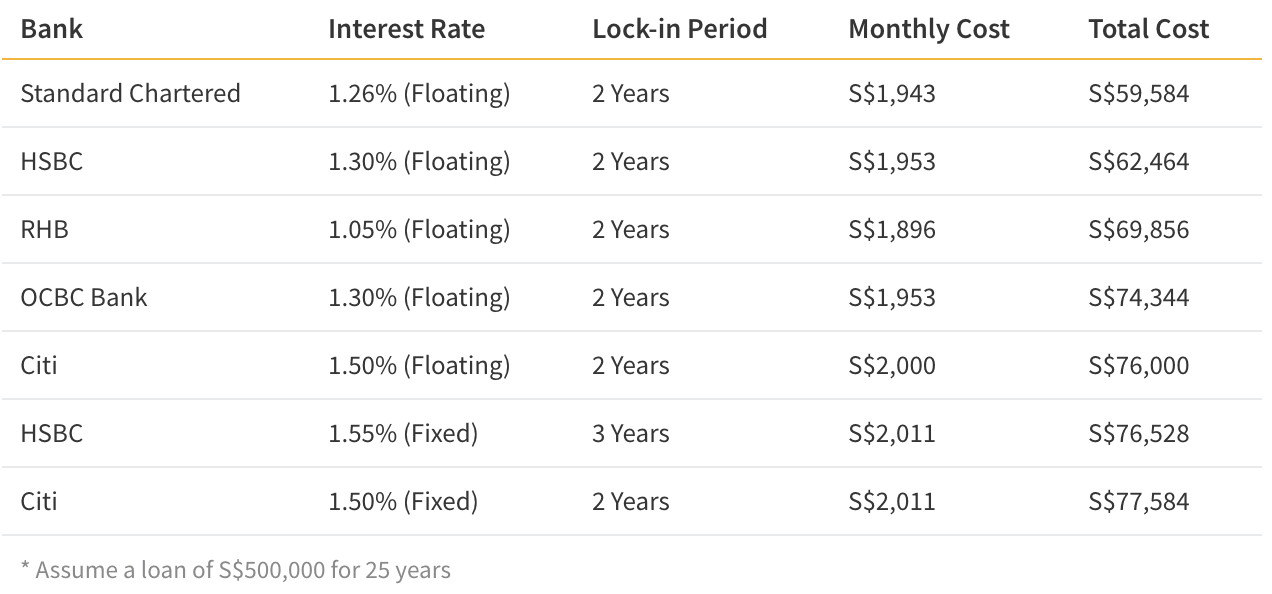

If you can reduce your interest rate by 1%-2% per year, then refinancing could save you a lot on the overall cost of your loan. Before you refinance, however, you should consider whether you are eligible to refinance, the amount of interest you will have to pay, the loan tenor, and the conditions of refinancing. For example, if you originally get a mortgage from HSBC for 25 years at a fixed rate of 1.55% per year, you would pay an extra S$58 per month than if you were to refinance after with Standard Chartered after 3 years. Over the next 22 years, you would even save around S$15,312. Rest assured, there are resources available that can help you get the most out of your home loan.

Cheapest Home Loans in Singapore as of November 2020

On the other hand, refinancing might not be a viable option. For example, only those who have passed the 1-3 year lock-in period are eligible to refinance. Moreover, if a loan has lower first-year interest rates but costlier interest rates following that, or has the same interest rates after a longer period of time, it might not be a good idea. To see whether this is the case for you, you can use a home loan calculator tool to help you decide. Lastly, you should not refinance your home if the cancellation fees (around 0.75%-1.5% of the amount not yet disbursed) is too expensive.

3. Ask for help from family and friends

This time is particularly stressful for many homeowners. If you have a strong support network, and you are comfortable asking who is in it for some help, borrowing money from your family and/or friends could provide you with quick cash at very low interest rates. Of course, this option might be more difficult to muster up the courage to ask for money. However, if you come prepared with a repayment plan and are happy to negotiate the terms and conditions of the loan, you may be pleasantly surprised with how much the loan could help you.

4. Sell your home

Selling your home might not be the ideal solution, but for some homeowners, it could be the best one. You also may wish to do this preemptively to cut costs in the long-run, as long as you do not foresee your situation improving.

There are several ways to go about selling your home. If you are not in a rush, you can probably put it on the market as you would normally. However, as COVID-19 affected everyone, you may get less than what you initially paid for. Secondly, you could do a short-sale, where you sell your home for less than the balance remaining on your mortgage. This is a good option for those who need cash quickly. You could also transfer the title of your home to your mortgage company. This is known as a "deed in lieu of foreclosure," and could help you move out of your home and avoid foreclosure.

If you're struggling to stay in your current home, you'll need to decide whether you prioritize space or location. If you prioritize location, then you can consider downgrading to a smaller flat. This can be a good option for seniors, singles or couples with no kids. On the other hand, families who need the extra space may have to compromise by moving to a cheaper neighborhood like Bedok or Admiralty. While it may be painful to move from your dream neighborhood or flat, it is worth doing to avoid undue financial stress down the line.

5. Last Resort Option: Declare Bankruptcy

If you owe over S$15,000, then you are able to file for bankruptcy in Singapore. Due to the growing amount of poverty during COVID-19, the Supreme Court of Singapore recently added measures to provide temporary relief. Such measures include an increased time to pay back loans and changes in thresholds.

If you choose to file for bankruptcy, you will have to pay an application fee of S$1,850. Your assets will be collected and sold, and the money earned from that will be used to pay back the money you owe. Although this time is difficult, you will be supported and will eventually surpass this. It is worth emphasizing that bankruptcy should be a last resort option since when you file for bankruptcy, you will likely lose your property, have to declare every asset, cannot travel without telling the courts, your employers and public will know, and your credit score may remain low for up to 7 years after.

What option is the best one for me?

The option that is best for you depends on your unique financial situation. For example, if you have missed or have only partially paid your mortgage for a few months, then you should probably not file for bankruptcy. However, it might be worth renegotiating the terms of your loan or lending money from a family member or trusted friend.

As there is a global pandemic, and several thousands of Singaporeans have lost their jobs, many lending institutions understand that this is a difficult time for people. While finding a home loan can be stressful if you cannot pay it off, there are still options that are available to help you during this difficult time.

Anya is a Research Analyst for ValueChampion who focuses on loans and investments in Singapore. Previously, she assisted global consultancies, hedge funds and private equities with primary research at a high-growth fin-tech based in London. A graduate of the University of Oxford and King's College London, Anya is currently interested in applying quantitative research to help consumers make better financial decisions.