Average Cost & Benefits of Direct Purchase Life Insurance 2024

Life insurance is an insurance policy that pays out a lump sum of money upon death, terminal illness or total and permanent disability of the person insured. There are two main types of life insurance: term insurance and whole life insurance. Term insurance insures you for a set period of years, whereas whole life insurance will insure you for your whole life and can provide some cash and bonus benefits. In Singapore, Direct Purchase Life Insurance plans are simple term life and whole life insurance products that were created with affordability in mind and can be bought without going through an intermediary such as a financial advisor. Currently, 15 insurance companies in Singapore offer DPI plans and sell them either online or through a customer service representative.

Average Cost of Direct Purchase Term Life Insurance

There are three types of term life DPI plans available: 5-year renewable plans, 20-year plans and up to age 65 plans. The maximum sum assured is S$400,000. Term life DPI premiums change depending on the age, gender and health of the applicant, as well as the tenure and coverage amount of the plan.

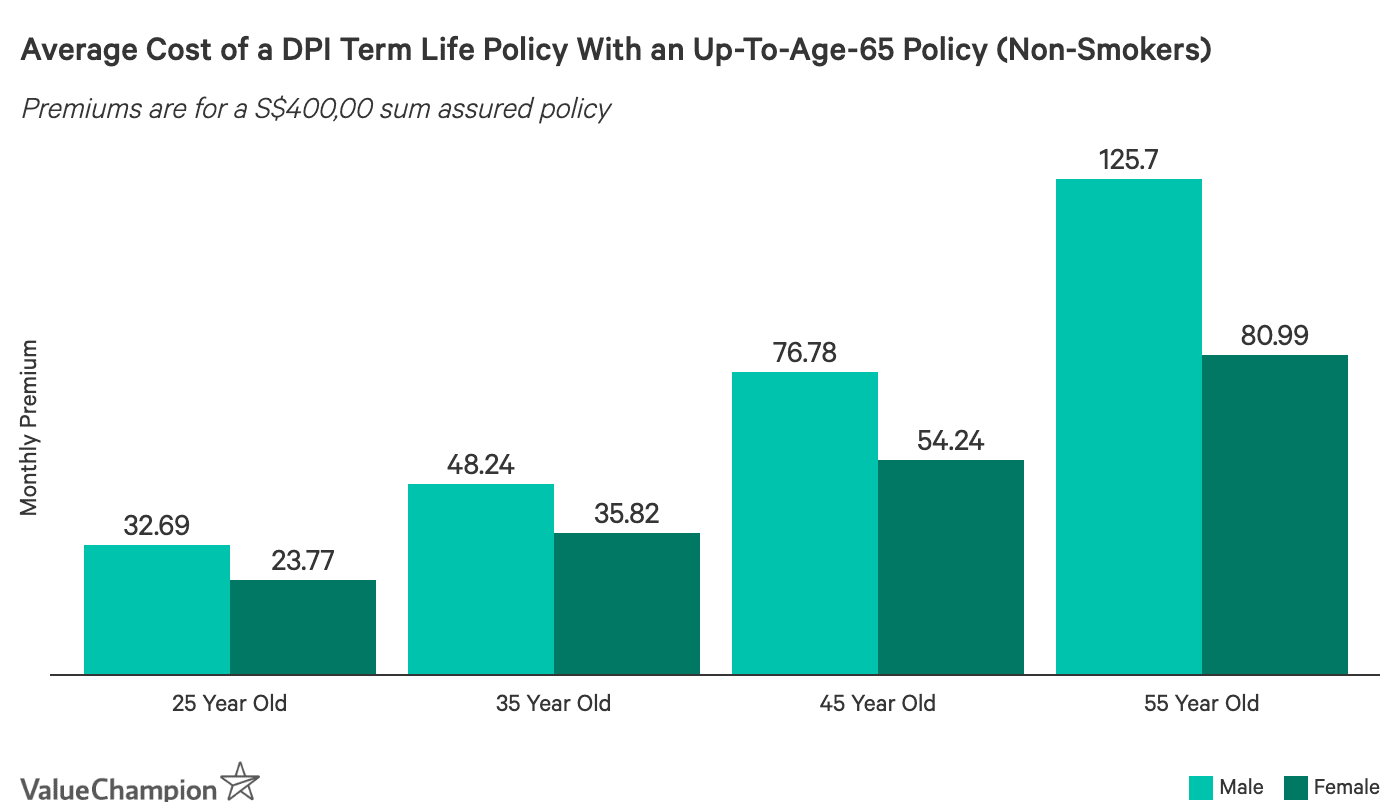

A non-smoking 35-year old male can expect to pay an average premium of S$48 per month for an up to age 65 term life DPI policy with S$400,000 of death, terminal illness and permanent disability coverage. Females will generally pay less, with a 35-year old female paying an average monthly premium of S$36 for the same plan. Younger consumers will see lower premiums as well, with a 25-year old male paying an average monthly premium of S$33 for the same plan—around 30% less per month than his older counterpart.

On average, we found that 5-year renewable term life DPI plans had the cheapest premiums and up to age 65 term life DPI had the most expensive premiums—with one exception. While up to age 65 plans are generally 100-200% more expensive than either 5-year plans or 20-year plans for younger consumers, they are around 55% cheaper than 20-year policies for consumers over 50. 20-year policies were priced in between the two. We also found that S$400,000 term life DPI plans are around 4.5x more expensive than S$50,000 term life DPI plans, regardless of gender and age. Lastly, females paid 25-45% less than their male counterparts, regardless of age, amount insured and plan tenure.

| Amount Insured | Plan Tenure | Age 25 | Age 35 | Age 45 | Age 55 |

|---|---|---|---|---|---|

| S$50,000 | 5-Years | S$3.26 | S$3.92 | S$6.71 | S$16.01 |

| 20-Years | S$3.41 | S$5.31 | S$12.14 | S$31.55 | |

| Age 65 | S$5.47 | S$7.68 | S$11.84 | S$18.96 | |

| S$200,000 | 5-Years | S$9.80 | S$12.68 | S$24.64 | S$62.09 |

| 20-Years | S$10.79 | S$18.66 | S$46.57 | S$137.09 | |

| Age 65 | S$17.32 | S$25.57 | S$44.53 | S$64.67 | |

| S$400,000 | 5-Years | S$18.14 | S$23.23 | S$44.53 | S$113.13 |

| 20-Years | S$19.91 | S$33.70 | S$80.53 | S$249.37 | |

| Age 65 | S$32.69 | S$48.24 | S$76.78 | S$125.70 |

Average Cost of Direct Purchase Whole Life Insurance

Whole Life DPI plans come in two types: up to age 70 plans and up to age 85 plans. The maximum sum assured is S$200,000. Similar to term life DPI policies, premiums can change depending on age, gender, plan tenure and amount insured.

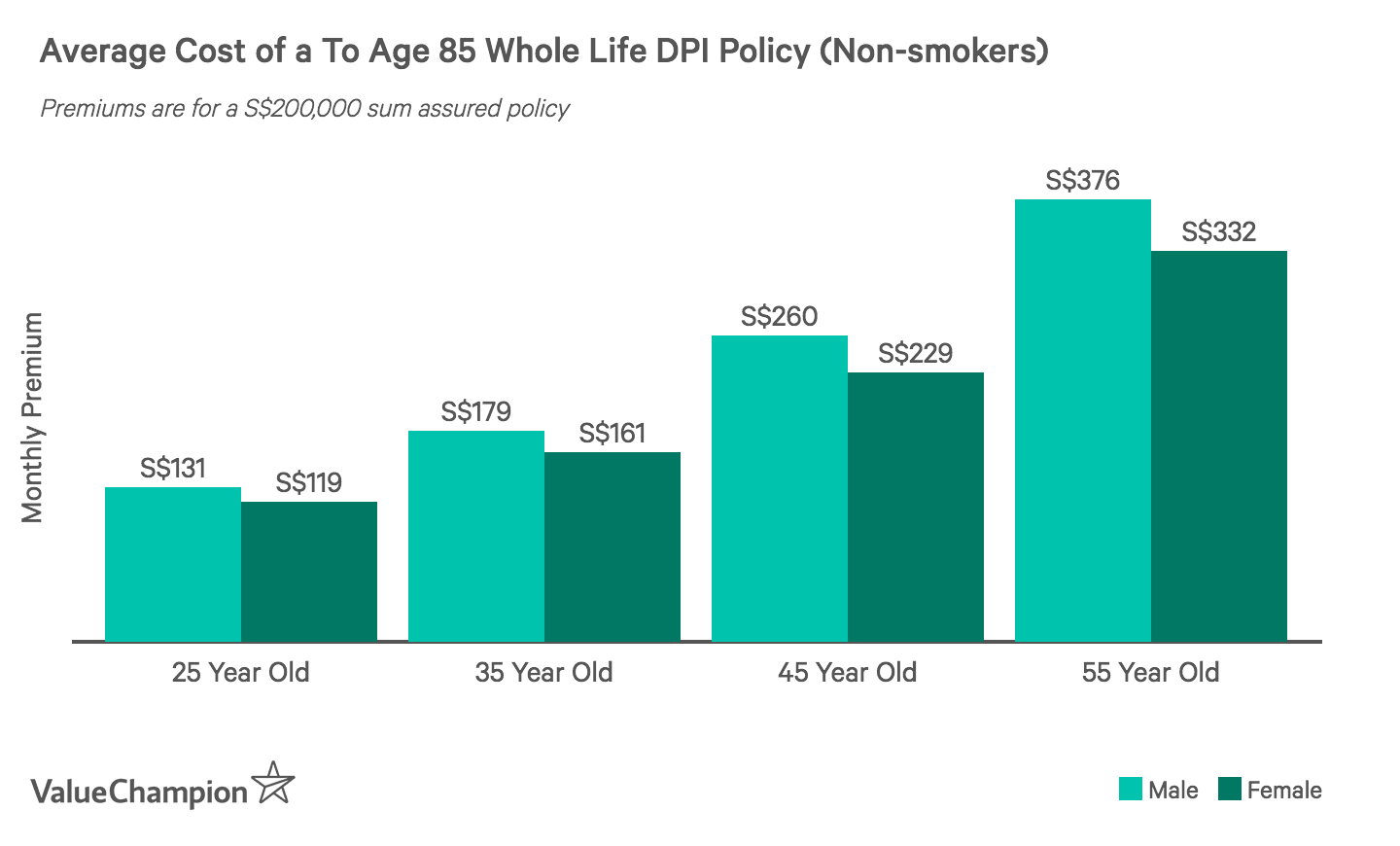

The average cost of an up to age 85 whole life DPI plan with S$200,000 of death, terminal illness and total and permanent disability coverage is S$284 per month for a 35-year old non-smoking male. Females can expect to pay slightly less, with average premiums for the same plan costing S$255/month for a 35-year old non-smoking female. In fact, similar to term life DPI policies, females will see 10% cheaper premiums on average compared to males. Up to age 85 whole life DPI plans cost 15% less than up to age 70 plans regardless of gender and amount insured. Lastly, we found that whole life DPI plans with S$50,000 of death coverage cost around 75% less than S$200,000 plans.

| Amount Insured | Plan Tenure | Age 25 | Age 35 | Age 45 | Age 55 |

|---|---|---|---|---|---|

| S$50,000 | Age 70 | S$58 | S$80 | S$123 | S$207 |

| Age 85 | S$56 | S$75 | S$107 | S$154 | |

| S$100,000 | Age 70 | S$110 | S$154 | S$238 | S$408 |

| Age 85 | S$105 | S$143 | S$208 | S$301 | |

| S$150,000 | Age 70 | S$165 | S$231 | S$315 | S$612 |

| Age 85 | S$158 | S$215 | S$312 | S$451 | |

| S$200,000 | Age 70 | S$217 | S$305 | S$474 | S$813 |

| Age 85 | S$207 | S$284 | S$412 | S$599 |

Average Cost of Direct Purchase Critical Illness Insurance Riders

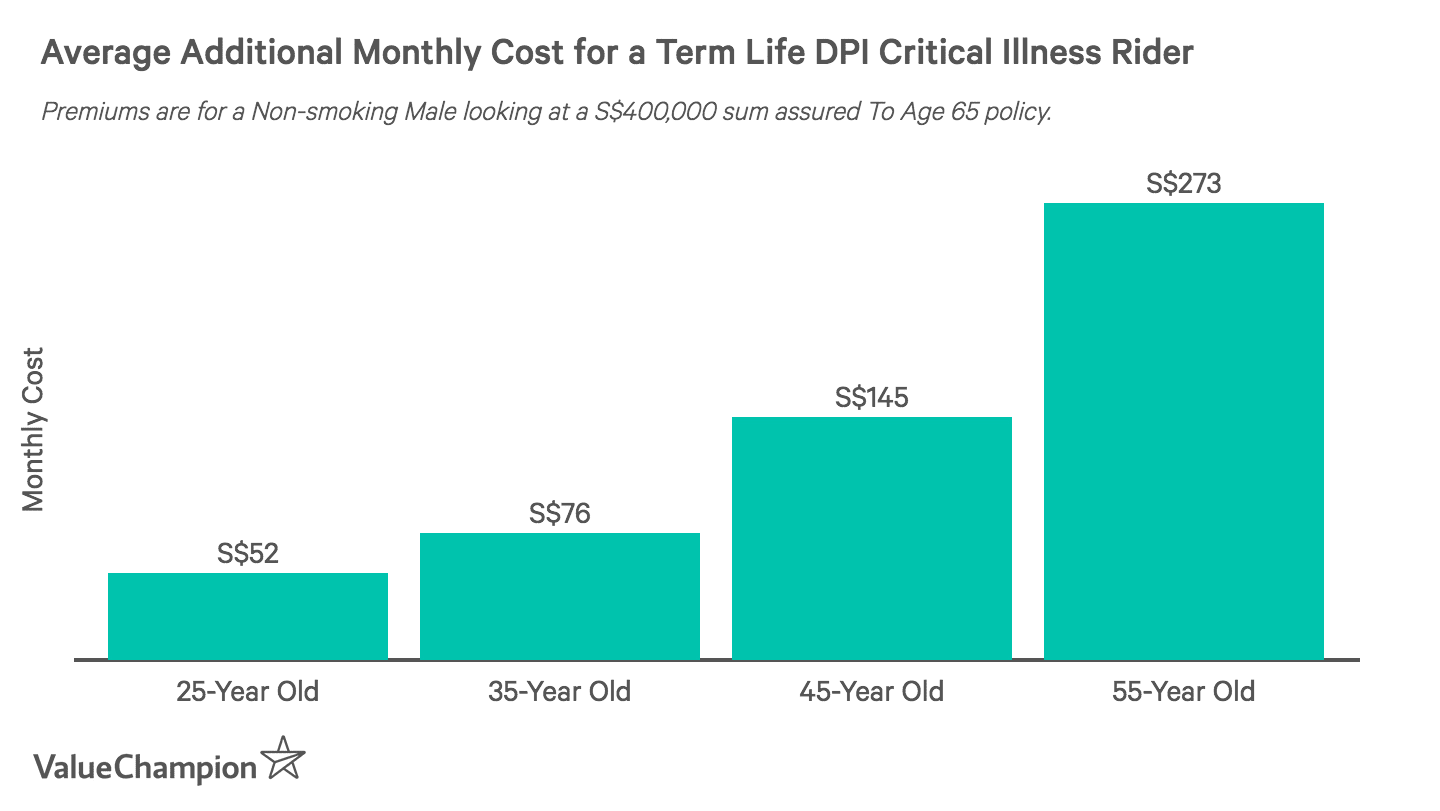

The average cost to add a critical illness rider for a S$400,000 term life policy for a 35-year old male is S$77.50 per month. Unlike term and whole life DPI base plans, females will pay more than their male counterparts. For instance, women can expect to see critical illness riders cost up to 114% more than for males for a 5-year renewable plan. Beyond that, critical illness riders follow the same pricing structure as the base term DPI plans. For example, prices increase as coverage amount increases, prices increase with age and Up to age 65 plans start off as more expensive for younger consumers than 5 or 20-year plans, but become cheaper for consumers over 50.

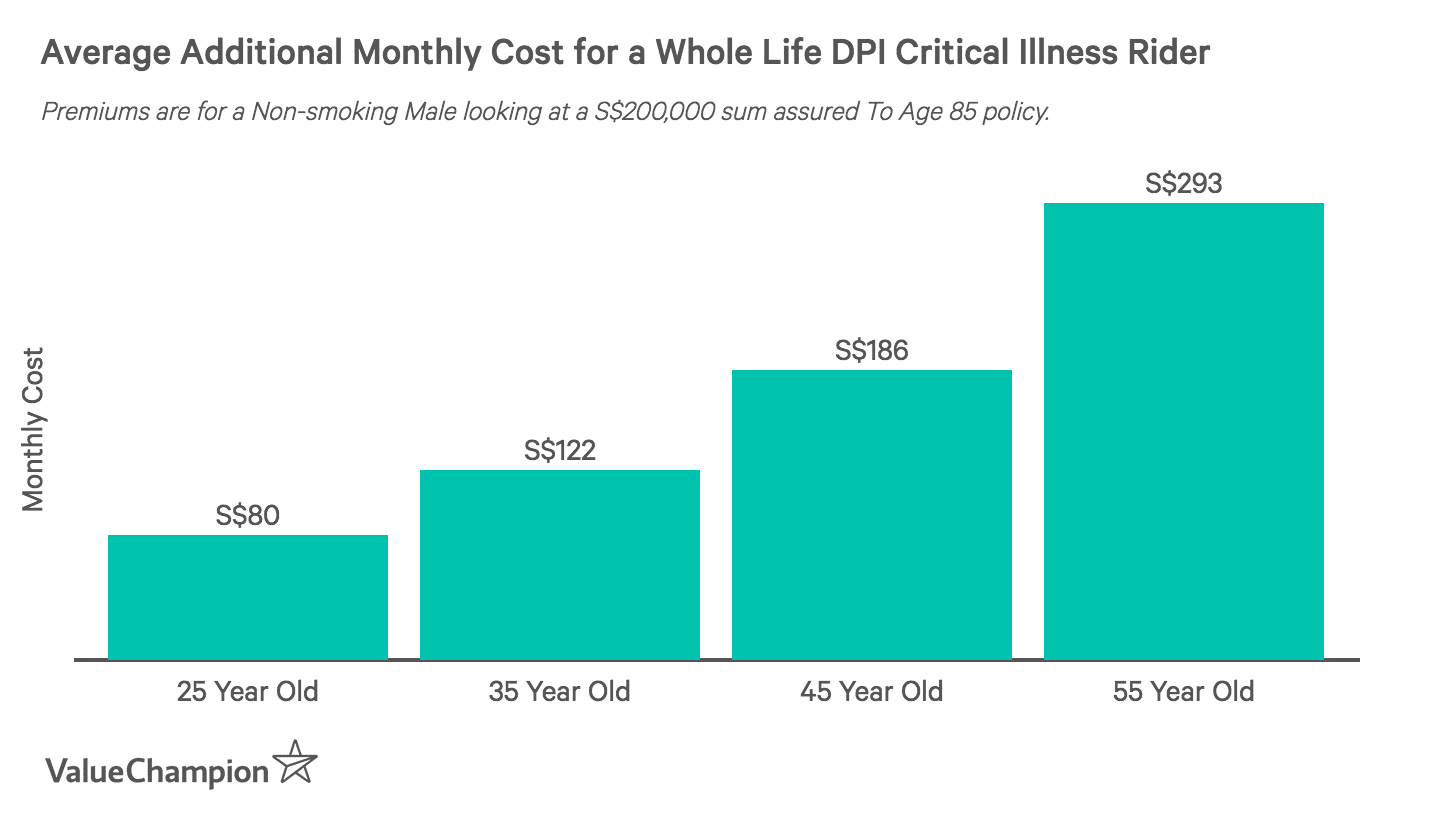

The average total premium that a 35-year old male can expect to pay for a S$200,000 whole life DPI plan with the critical illness rider included averages to S$406 per month. On average, we found that adding the critical illness rider will increase your whole life DPI premiums by around 45% regardless of which whole life DPI plan you choose. Furthermore, we found that critical illness riders cost around 10% more for up to age 70 plans than for up to age 85 plans.

Average Benefits of Direct Purchase Life Insurance

Direct Purchase Insurance benefits are all fairly standardised, offering death, terminal illness, total and permanent disability and optional critical illness coverage. The maximum amount you can insure yourself for is S$200,000 for a whole life DPI plan and S$400,000 for a term life DPI plan.

A typical term life DPI policy provides a death and total and permanent disability benefit of 100%, but doesn't offer an applicability of surrender benefit (you won't get anything if you choose to surrender your policy before its maturity date). You will be covered between ages 18 to 60 or 65. On the other hand, a typical whole life DPI policy also provides 100% coverage for death and total and permanent disability but has a cash value added, potential bonuses and provides a surrender benefit. You will also receive lifetime coverage or choose to be covered until a specified maturity date. However, total and permanent disability benefits will end at age 65 for both term life and whole life DPI plans.

Your critical illness rider will fully cover 30 of the 37 standardised critical illnesses, with the exception of Angioplasty and other invasive coronary artery treatments. Insteand, these conditions will receive a payout of 10% of the sum insured or S$25,000 (whichever is lower). The remaining 6 conditions that aren't covered are listed below.

Critical Illness Conditions Not Covered in DPI plans

- Poliomyelitis

- Progressive Scleroderma

- Systemic Lupus Erythematosus with Lupus Nephritis

- Loss of Independent

- Other Serious Coronary Artery Disease

- Apallic Syndrome

Considerations

To get a picture of the average cost of term and whole life DPI policies, we gathered quotes from all of the insurers who provided quotation options online. We segmented these quotes based on gender and age. Because not all insurers provide quotations online, we recognise that the average may be slightly off— especially in the case of whole life insurance where there was limited data available. However, the average prices and overall fee structure can still be used to understand what to expect when deciding on DPI policies. Your individual quotes may vary based on your age, risk profile and other factors.

Read More:

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.