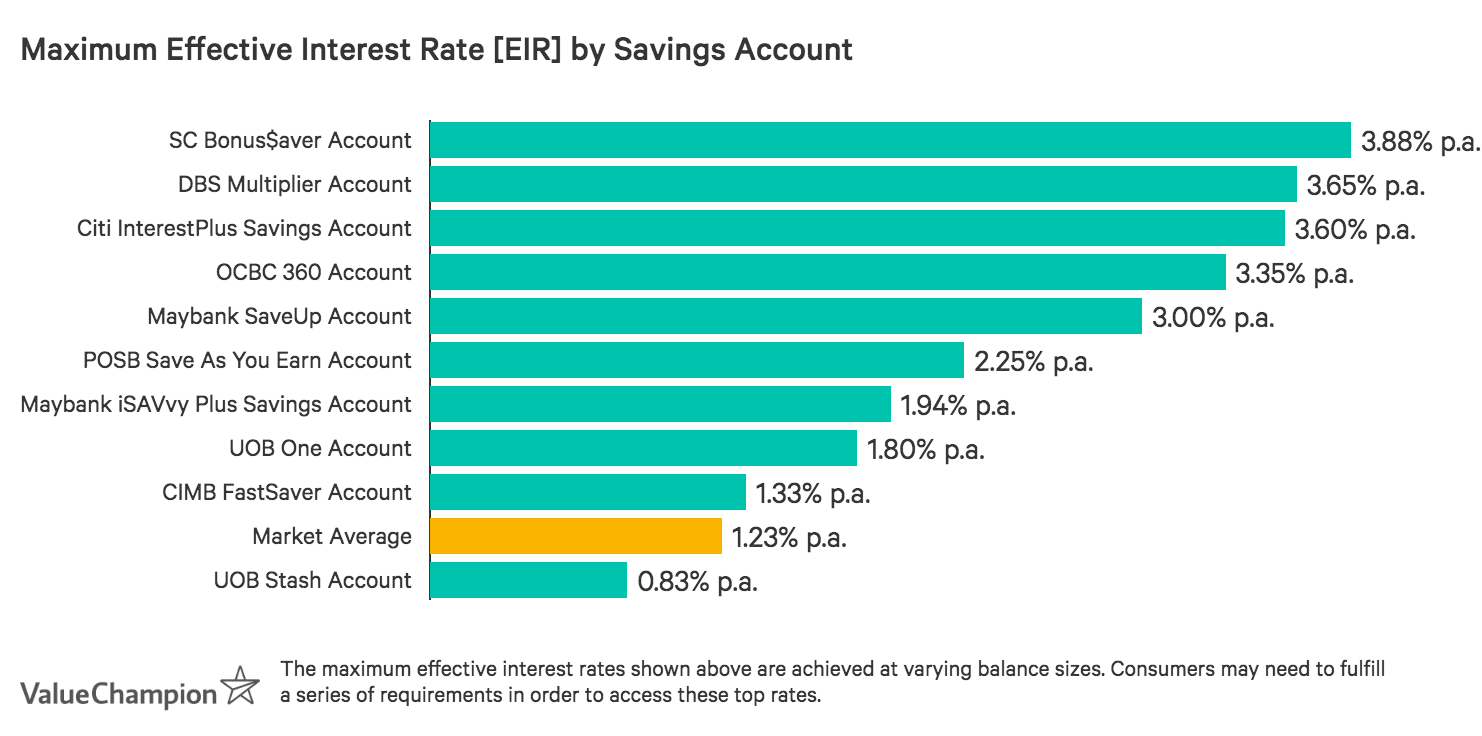

If you're a financially-savvy, salaried adult, you may be able to take advantage of the highest maximum effective interest rate (EIR) on the market with DBS Multiplier Account. Consumers capable of meeting all account criteria can earn up to 3.00% p.a.–higher than with almost any of its competitors. Nonetheless, reaching this rate requires substantial engagement with multiple DBS products (credit cards, home loans, insurance and investments). Engaged consumers comfortable with tracking personal finance are most likely to benefit, especially with a larger balance size (interest peaks at S$100k).

Pros

Cons

High maximum EIR of 3.00% p.a.

Rewards DBS Bank loyalists

No minimum initial deposit req.

Fall-below fees waived if under 29yo

Bonus rates req. multiproduct engagement

Favors those with high balance & high monthly transactions

Salary or dividend crediting req. for bonus rates

Pros & Cons

Pros:

High maximum EIR of 3.00% p.a.

Rewards DBS Bank loyalists

No minimum initial deposit req.

Fall-below fees waived if under 29yo

Cons:

Bonus rates req. multiproduct engagement

Favors those with high balance & high monthly transactions

Salary or dividend crediting req. for bonus rates

What Makes DBS Multiplier Account Stand Out

DBS Multiplier Account is ideal for salaried consumers who are closely engaged with DBS financial products and who are comfortable managing their own finances. Consumers who meet all account criteria can earn at one of the market's highest potential effective interest rate (EIR) –3.00% p.a.–which is more than 35x higher than rates offered by basic accounts. There's no minimum initial deposit requirement, which makes starting an account fairly easy. While there's a S$3k minimum balance requirement, the S$5 fall-below fee is waived for those 29 years old or younger.

Even though account requirements seem to favour young adults, DBS Multiplier Account does require salary or dividend crediting in order to earn above the 0.05% p.a. base rate. In addition, bonuses are earned by engaging with DBS products like credit cards, home loans, insurance and investments. This favors more established individuals who likely have progressed further into their career and feel very comfortable managing their personal finances. Finally, interest rates increase as the size of the account holder's monthly DBS transactions increase, and consumers must maintain a balance of S$100k in order to fully capitalise on a 3.00% p.a. earning potential.

DBS Multiplier Account Interest Rates Grid

Transactions/Month

Salary/Dividends/SGFin Dex + transactions in 1 category

(up to S$25k)

Salary/Dividends/SGFin Dex + transactions in 2 categories

(up to S$50k)

Salary/Dividends/SGFin Dex + transactions in 3 categories

(S$50k-S$100k)

< S$2k

0.05%

0.05%

0.05%

S$2k – below 2.5k

0.40%

0.60%

1.20%

S$2.5k – below S$5k

0.40%

0.70%

1.40%

S$5k – below S$15k

0.50%

0.80%

1.60%

S$15k – below S$30k

0.50%

1.00%

1.70%

S$30k+

0.60%

2.00%

3.00%

Max Effective Interest Rate: 3.00% p.a. (at S$100k balance)

Products include Credit Card spend, Home Loan Instalments, Insurance and Investments. Salary must be credited to account to qualify for any bonus interest

Considering these factors, DBS Multiplier Account is actually a fantastic option for mid-to-high income adults, especially those with a firm understanding of their personal finances. By properly balancing several financial products and maintaining a high volume in transactions, such individuals can grow their savings more rapidly than with almost any other account. As a result, DBS Multiplier Account is definitely worth considering for established, high earning adults engaged with DBS financial products.

S$5 (Waived if less than 30 years old, or if it's applicant's 1st account with DBS)

How Does DBS Multiplier Compare to Other Accounts?

Read our comparisons of DBS Multiplier Account with other savings accounts and learn what makes each account unique in its own way. We compare and contrast each account to help you to identify which best suits your needs.

DBS Multiplier Account v. OCBC 360 Savings Account

Consider this if you're a consistent saver with a stable budget

Min. Age Requirement

18

Min. Initial Deposit

S$1,000

Min. Balance Requirement

S$3,000

Like DBS Multiplier Account, OCBC 360 Savings Account rewards consumers for salary-crediting and engaging with OCBC bank products like credit cards, insurance and investments. However, OCBC 360 Account stands apart for a few reasons. First, bonus rates are achieved simply by hitting a minimum threshold, rather than varying by monthly transaction size. Next, account holders earn a bonus for making monthly deposits of S$500+. Finally, the maximum EIR of 3.35% p.a. can be reached with just S$70k balance. Overall, OCBC 360 Savings Account rewards steady incremental savers with a predictable budget, while DBS Multiplier may be a better fit for higher-earners with large monthly transactions.

Rate Type

Details & Requirements

Interest Rate

Base Rate

No Requirements; applied to entire balance

0.05% p.a.

Grow Bonus

Maintain balance of at least S$200k

(Bonus interest added to base rate)

+0.80% p.a. on first S$70k

Step-Up Bonus

Deposit at least S$500/month

(Bonus interest added to base rate & applied

to specific band of balance)

+0.20% p.a. on first S$35k

+0.40% p.a. on next S$35k

Spend Bonus

Spend S$500/month on OCBC credit card

(Bonus interest added to base & applied to

specific band of balance)

+0.20% p.a. on first S$35k

+0.40% p.a. on next S$35k

Salary Bonus

Credit S$2k+ salary to account via GIRO

(Bonus rates added to base rate & applied

to specific band of balance)

+1.20% p.a. on first S$35k

+2.40% p.a. on next S$35k

"Wealth" Bonus

Insure or invest with OCBC Bank

(Bonus rates added to base rate & applied

to specific band of balance)

+0.60% p.a. on first S$35k

+1.20% p.a. on next S$35k

Max Effective Interest Rate:

3.35% p.a. (at S$70k balance)

Max EIR is highest at a S$70k balance even with the Grow Bonus left inactive. Promotional rates, if any, are not included

OCBC 360 Account Interest Rates

Base Rate: No requirements (applied to entire balance)

0.05% p.a.

Grow Bonus: Maintain balance of at least S$200k (bonus interest added to base rate)

+0.80% p.a. on first S$70k

Step-Up Bonus: Deposit at least S$500/month (bonus interest added to base rate & applied to specific band of balance)

+0.20% p.a. on first S$35k

+0.40% p.a. on next S$35k

Spend Bonus: Spend S$500/month on OCBC credit card (bonus interest added to base & applied to specific band of balance)

+0.20% p.a. on first S$35k

+0.40% p.a. on next S$35k

Salary Bonus: Credit S$2k+ salary to account via GIRO (bonus rates added to base rate & applied to specific band of balance)

+1.20% p.a. on first S$35k

+2.40% p.a. on next S$35k

"Wealth" Bonus: Insure or invest with OCBC Bank (bonus rates added to base rate & applied to specific band of balance)

+0.60% p.a. on first S$35k

+1.20% p.a. on next S$35k

Max Effective Interest Rate:

3.35% p.a. (at S$70k balance)

Max EIR is highest at a S$70k balance even with the Grow Bonus left inactive

DBS Multiplier Account v. Maybank SaveUp Savings Account

Consider this if you're a moderate saver in charge of the household

Min. Age Requirement

16

Min. Initial Deposit

S$500 for Singaporeans & PR, S$1,000 for foreigners

Min. Balance Requirement

S$1,000

Moderate savers in charge of their households can especially benefit from Maybank SaveUp Savings Account. As with other multi-product accounts, consumers are rewarded for engagement with Maybank credit cards, investments, insurance and loans. However, this account only requires salary crediting plus engagement with 2 banking products to earn an +2.75% p.a. bonus rate. Essentially, salaried individuals who may be taking out a loan and who spend with credit cards can easily bump their interest rate without much of an added effort.

Additionally, MB SaveUp account holders can earn a total EIR of 3.00% p.a. with a balance of just S$50k–which is quite accessible for moderate savers. DBS Multiplier is a better fit for high earners with large savings as interest rates factor in monthly transaction volume.

Rate Type

Details & Requirements

Interest Rate

Base Rate

No requirements

(Rate varies according to band of balance)

0.15% p.a. on 1st S$3k

0.25% p.a. on next S$47k

0.25% p.a. beyond S$50k

Product Bonus

Use at least 1 Maybank service or product,

ie loan, insurance, investment, credit card etc.

(Bonus interest based on number of products

& applied to entire balance, up to 1st S$50k)

+0.10% p.a. for 1 product

+0.7% p.a. for 2 products

+2.75% p.a. for 3+ products

Max Effective Interest Rate:

3.00% p.a. (at S$50k balance)

Promotional rates, if any, are not included

Maybank SaveUp Savings Account Interest Rates

Base Rate: No requirements (rate varies according to band of balance)

0.15% p.a. on 1st S$3k

0.25% p.a. on next S$47k

0.25% p.a. beyond S$50k

Product Bonus: Use at least 1 Maybank service or product, ie loan, insurance, investment, credit card etc. (bonus interest based on number of products & applied to entire balance, up to 1st S$50k)

+0.10% p.a. for 1 product

+0.7% p.a. for 2 products

+2.75% p.a. for 3+ products

DBS Multiplier Account v. Standard Chartered Bonus$aver Account

Consider this if you're a high-earner open to a banking relationship with Standard Chartered

Min. Age Requirement

18

Min. Initial Deposit

S$0

Min. Balance Requirement

S$3,000

Affluent savers can potentially earn at one of the highest effective interest rates on the market with Standard Chartered Bonus$aver Account. Account holders earn bonuses beyond the 0.05% p.a. base rate by crediting a S$3k+/month salary, spending S$2k+/month with a Bonus$aver credit or debit card, buying a S$12k insurance policy or S$30k unit trust subscription, and paying at least 3 bills online via GIRO. While each of these boosts can be earned independently, those that fulfill requirements for all four can earn up to 2.38% p.a. (achieved at a S$100k balance). While these qualifications are a bit of a stretch for the average consumer, SC Bonus$aver is ideally suited to higher earning, higher spending individuals open to a banking relationship with Standard Chartered.

Rate Type

Details & Requirements

Interest Rate

Base Rate

No Requirements

(Applied to entire balance)

0.01% p.a.

Credit/Debit Bonus

Spend/mo on Bonus$aver card

(Bonus added to base rate)

+0.20% p.a. w/ S$500-S$1.99k spend

+0.40% p.a. w/ S$2k+ spend

Salary Credit Bonus

Credit S$3k+/month salary

(Bonus added to base rate)

+0.10% p.a. on 1st S$100k

Product Bonus

Invest with or buy insurance from SC

(Bonus added to base rate)

+0.90% p.a. on 1st S$100k

GIRO Bill-Pay Bonus

Make 3+ online bill payments via GIRO

(Bonus added to base rate)

+0.07% p.a. on first S$100k

Max Effective Interest Rate:

2.38% p.a. (at S$100k balance)

Promotional rates, if any, are not included

SC Bonus$aver Account Interest Rates

Base Rate: No requirements (applied to entire balance)

0.01% p.a.

Spend Bonus: Spend monthly on a Bonus$aver credit or debit card (bonus added to base rate)

+0.20% p.a. w/ S$500-S$1.9k spend

+0.40% p.a. w/ S$2k+ spend

Salary Credit Bonus: Credit S$3k+ salary to account (bonus added to base rate)

+0.10% p.a. on first S$100k

Product Bonus: Invest with or buy insurance with SC (bonus added to base rate)

+0.90% p.a. on first S$100k

GIRO Bill-Pay Bonus: Pay 3+ bills online via GIRO (bonus added to base rate)

+0.07% p.a. on first S$100k

Max Effective Interest Rate:

2.38% p.a. (at S$100k balance)

Promotional rates, if any, are not included

DBS Multiplier Account v. UOB One Savings Account

Consider this if you're interested in a UOB credit card in addition to your savings account

Min. Age Requirement

18

Min. Initial Deposit

S$1,000

Min. Balance Requirement

S$1,000

UOB One Savings Account not only offers a relatively high maximum EIR of 2.50% p.a., but is also very easy to manage. Unlike more complex products, like DBS Multiplier, UOB One Account bases bonus rates on just 3 criteria: salary crediting, credit card use and balance size. Consumers need only spend S$500+/month on their UOB credit card to earn a +0.20% p.a. boost, and can further boost their interest rate by crediting their salary or making 3 GIRO debit transactions per month. Beyond these criteria, interest rates vary simply by balance size. UOB One Account is a great match for working consumers who are perhaps just starting to build their skills in managing personal finances. Those who are more established and who can track a more complex interaction of products may be able to earn more interest with DBS Multiplier Account.

Rate Type

Details & Requirements

Interest Rate

Base Rate

No Requirements; applied to entire balance

0.05% p.a.

Credit Card Bonus

Spend S$500/month on UOB One,

UOB YOLO, or UOB Lady's credit card

(Bonus interest added to base rate)

+0.25% p.a.

Salary/GIRO Bonus

Credit S$2k+ salary to account or

make 3 GIRO debit transactions per month

(Bonus rates added to base rate &

applied to specific band of balance)

+0.50% p.a. on first S$15k

+0.55% p.a. on next S$15k

+0.65% p.a. on next S$15k

+0.80% p.a. on next S$15k

+2.50% p.a. on next S$15k

Max Effective Interest Rate:

2.50% p.a. (at S$75k balance)

Promotional rates, if any, are not included

UOB One Account Interest Rates

Base Rate: No requirements (applied to entire balance)

0.05% p.a.

Credit Card Bonus: Spend S$500/month on UOB One, UOB YOLO, or UOB Lady's Card (bonus interest added to base rate)

+0.25% p.a.

Salary/GIRO Bonus: Credit S$2k+ salary to account or make 3 GIRO debit transactions per month (bonus rates added to base rate & applied to specific band of balance)

Carrie is a Senior Analyst at ValueChampion, helping consumers find the best credit cards and other financial products based on quantitative and qualitative analysis. She previously led consumer studies worldwide as a Senior Research Executive at MMR Research, and led development & operations and BellaVetro. She attended Duke University and Penn State University, graduating with a degree in Political Science and Government. Her work has been featured on a variety of major media such as Yahoo Finance, Asia One, Buro, Zuu Online and more.

Advertiser Disclosure: ValueChampion is a free source of information and tools for consumers. Our site may not feature every company or financial product available on the market. However, the guides and tools we create are based on objective and independent analysis so that they can help everyone make financial decisions with confidence. Some of the offers that appear on this website are from companies which ValueChampion receives compensation. This compensation may impact how and where offers appear on this site (including, for example, the order in which they appear). However, this does not affect our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services

We strive to have the most current information on our site, but consumers should inquire with the relevant financial institution if they have any questions, including eligibility to buy financial products. ValueChampion is not to be construed as in any way engaging or being involved in the distribution or sale of any financial product or assuming any risk or undertaking any liability in respect of any financial product. The site does not review or include all companies or all available products.