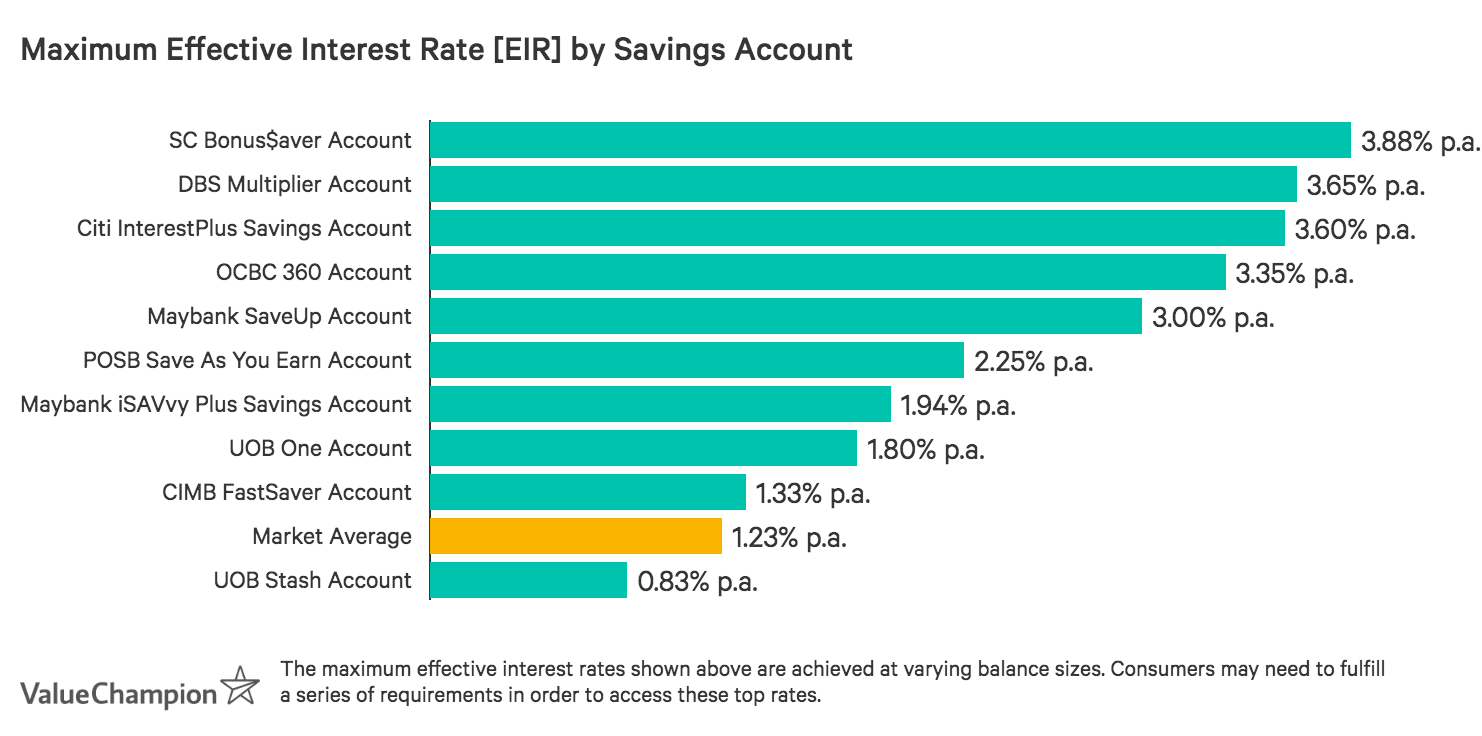

Standard Chartered Bonus$aver Account: Highest Interest for Affluent Savers

Standard Chartered Bonus$aver Account: Highest Interest for Affluent Savers

ValueChampion Rating ![]()

Pros

- Financially savvy individuals comfortable with a more complex account

- Consumers willing to invest with or buy insurance from SC

- Affluent individuals who can maintain a large balance

Cons

- People looking for an easy-to-use or starter account

- Individuals who spend less than S$2k/month

- Lower earners with lower balances

While technically considered a current account, Standard Chartered Bonus$aver Account actually functions quite like a savings account–in fact, affluent consumers can earn at the highest potential effective interest rate on the market, at 2.38% p.a. Account holders earn bonuses beyond the 0.01% p.a. base rate for additional banking and product engagement, including crediting a S$3k+ salary (+0.10% p.a.), investing with or buying insurance from Standard Chartered (+0.90% p.a.) and making 3 GIRO bill payments monthly (+0.07% p.a). These bonuses are applied independently, so it's possible to boost your interest even if you earn a lower salary or don't want to buy insurance. Nonetheless, those who do qualify across the board and who can maintain a S$100k balance are most likely to benefit.

| Pros | Cons |

|---|---|

|

|

| Promotion:

| |

| Pros & Cons |

|---|

Pros:

|

Cons:

|

What Makes Standard Chartered Bonus$aver Account Stand Out

Standard Chartered Bonus$aver Account is the absolute best option on the market for financially-savvy high-earners looking to max out interest on their savings. Account holders can earn up to 2.38% p.a. on their entire balance (up to S$100k) simply by meeting 4 bonus criteria: spending S$2k/month on your card (+0.4% p.a.), crediting a salary of S$3k+/month (0.10% p.a.), investing with or buying an insurance policy from SC (+0.90% p.a.) and paying at least 3 bills online monthly via GIRO (+0.07% p.a.). Each of these boosts can be unlocked individually–there are no connections or contingencies, as with some other accounts–and bonuses apply to the entire balance, rather than to incremental bands.

SC Bonus$aver Account Interest Rates

| Rate Type | Details & Requirements | Interest Rate |

|---|---|---|

| Base Rate | No Requirements; applied to entire balance | 0.01% p.a. |

| Credit/Debit Spend Bonus |

| +0.20% p.a. w/ S$500-S$1.99k spend |

| +0.40% p.a. w/ S$2k+ spend | ||

| Salary Credit Bonus |

| +0.10% p.a. on 1st S$100k |

| Product Bonus |

| +0.90% p.a. on 1st S$100k |

| GIRO Bill-Pay Bonus |

| +0.07% p.a. on first S$100k |

| Max Effective Interest Rate: | 2.38% p.a. (at S$100k balance) | |

| SC Bonus$aver Account Interest Rates |

|---|

Base Rate: No requirements (applied to entire balance)

|

Spend Bonus: Spend monthly on a Bonus$aver credit or debit card (bonus added to base rate)

|

Salary Credit Bonus: Credit S$3k+ salary to account (bonus added to base rate)

|

Product Bonus: Invest with or buy insurance with SC (bonus added to base rate)

|

GIRO Bill-Pay Bonus: Pay 3+ bills online via GIRO (bonus added to base rate)

|

Max Effective Interest Rate:

|

Another benefit of SC Bonus$aver Account is that for the most part, its bonuses are passive. Unlike other accounts that may require monthly tracking with rewards based on transaction amounts, SC Bonus$aver provides a "set it and forget it" structure that makes long-term saving even easier. For example, it's possible for account holders to set up automatic salary crediting and GIRO bill pay, requiring little to no effort thereafter. Additionally, consumers seeking a product bonus receive the +0.90% p.a. boost for a full 12 months after making their upfront insurance policy or unit trust purchase. In fact, the only boost requiring active effort is the card bonus, which isn't especially cumbersome for those who already tend to spend with debit or credit cards.

Unfortunately, SC Bonus$aver Account does have a few drawbacks. Cardholders must spend S$2k+/month on a Bonus$aver credit or debit card to unlock the +0.40% p.a. bonus (0.20% p.a. for S$500-S$1,999/month spend). These cards do not earn points, cashback or miles rewards however–so spending money to reach the card bonus minimum has a significant opportunity cost (as this same spend could be earning S$80-S$100+ with a traditional credit card). As it turns out, this opportunity cost is only eclipsed by interest earning potential for consumers spending S$2k/month and maintaining a S$100k balance. This may be because S$100k is the balance at which the maximum EIR of 2.38% p.a. can ultimately be achieved.

Interest Earned from Card Bonus vs. Potential Credit Card Rewards at S$2k/mo Spend

| Balance Size | Interest from Card Bonus Alone | Cashback Rewards Potential | Difference |

|---|---|---|---|

| S$25,000 | S$30.79 | S$100.00 | -(S$69.21) |

| S$50,000 | S$61.58 | S$100.00 | -(S$38.42) |

| S$75,000 | S$92.37 | S$100.00 | -(S$7.63) |

| S$100,000 | S$123.15 | S$100.00 | S$23.15 |

As a result, SC Bonus$aver Account is best fit for the affluent. The $3k+/month minimum requirement to earn the salary bonus is above the market average, and only those spending S$2k+/month and who can maintain a S$100k balance will benefit from the card spend bonus. In terms of products, account holders must either purchase an insurance policy with a minimum annual premium of S$12k or subscribe for an eligible unit trust with a minimum single subscription sum of S$30k–both of which may be a reach for the average consumer. Overall, consumers who find these qualifications a bit unreasonable may want to consider competitive alternatives with lower barriers to access bonuses (like OCBC 360 or Maybank SaveUp).

On a final note, SC Bonus$aver Account does not have a minimum initial deposit requirement (quite rare), but there is a minimum average balance of S$3k and a monthly fall-below fee of S$5 (both quite high). These requirements are unlikely to bother the affluent consumers most likely to benefit from this account, however. Ultimately, wealthier individuals can earn at a higher interest rate than with any alternative with SC Bonus$aver Account.

SC Bonus$aver Account Details & Requirements

| Details & Requirements | |

|---|---|

| Minimum Age Requirement | 18 |

| Minimum Initial Deposit | S$0 |

| Minimum Balance Requirement | S$3,000 |

| Fall-Below Fee |

|

How Does SC Bonus$aver Account Compare to Other Accounts?

Read our comparisons of SC Bonus$aver Account with other savings accounts and learn what makes each account unique in its own way. We compare and contrast each account to help you to identify which best suits your needs.

SC Bonus$aver Account v. OCBC 360 Savings Account

- Min. Age Requirement

- 18

- Min. Initial Deposit

- S$1,000

- Min. Balance Requirement

- S$3,000

OCBC 360 Savings Account is one of the best savings accounts available for average consumers due to its high interest rates and easy-to-access bonuses. As with SC Bonus$aver, account holders earn boosts for crediting their salary, spending with an OCBC credit card, and purchasing insurance or investing with OCBC. However, OCBC 360 account holders only need to earn S$2k/month for the salary bonus (compared to S$3k+), and earn a boost for spending on a rewards-earning OCBC credit card (therein avoiding a cashback opportunity cost). OCBC 360 Account also rewards incremental saving, which SC Bonus$aver does not. Overall, with a max EIR of 3.35% p.a. achievable at S$70k balance, OCBC 360 Account is a better option for average consumers who don't mind managing a more complex account.

| Rate Type | Details & Requirements | Interest Rate |

|---|---|---|

| Base Rate | No Requirements; applied to entire balance | 0.05% p.a. |

| Grow Bonus |

| +0.80% p.a. on first S$70k |

| Step-Up Bonus |

| +0.20% p.a. on first S$35k |

| +0.40% p.a. on next S$35k | ||

| Spend Bonus |

| +0.20% p.a. on first S$35k |

| +0.40% p.a. on next S$35k | ||

| Salary Bonus |

| +1.20% p.a. on first S$35k |

| +2.40% p.a. on next S$35k | ||

| "Wealth" Bonus |

| +0.60% p.a. on first S$35k |

| +1.20% p.a. on next S$35k | ||

| Max Effective Interest Rate: | 3.35% p.a. (at S$70k balance) | |

| OCBC 360 Account Interest Rates |

|---|

Base Rate: No requirements (applied to entire balance)

|

Grow Bonus: Maintain balance of at least S$200k (bonus interest added to base rate)

|

Step-Up Bonus: Deposit at least S$500/month (bonus interest added to base rate & applied to specific band of balance)

|

Spend Bonus: Spend S$500/month on OCBC credit card (bonus interest added to base & applied to specific band of balance)

|

Salary Bonus: Credit S$2k+ salary to account via GIRO (bonus rates added to base rate & applied to specific band of balance)

|

"Wealth" Bonus: Insure or invest with OCBC Bank (bonus rates added to base rate & applied to specific band of balance)

|

Max Effective Interest Rate:

|

SC Bonus$aver Account v. DBS Multiplier Account

- Min. Age Requirement

- 18

- Min. Initial Deposit

- S$0

- Min. Balance Requirement

- S$3,000

DBS Multiplier Account is a great option for financially-savvy consumers with high incomes and large budgets. Account holders who credit their salary can earn bonus interest based on their level of engagement with DBS products (like credit cards, insurance, home loans and investments). Those with higher monthly transaction volumes with these products earn at higher interest rates. In fact, those who engage with 3+ products and maintain a monthly transaction volume of S$30k+ can earn up to 3.00% p.a. effective interest, which is one of the highest rates on the market. This level of engagement may not be feasible for everyday consumers, however; affluent individuals who want to earn at an even higher rate without committing to so much tracking may prefer SC Bonus$aver Account.

| DBS Multiplier Interest Rate Grid | |||

|---|---|---|---|

| Transactions/Month |

|

|

|

| < S$2k | 0.05% | 0.05% | 0.05% |

| S$2k – below 2.5k | 0.40% | 0.60% | 1.20% |

| S$2.5k – below S$5k | 0.40% | 0.70% | 1.40% |

| S$5k – below S$15k | 0.50% | 0.80% | 1.60% |

| S$15k – below S$30k | 0.50% | 1.00% | 1.70% |

| S$30k+ | 0.60% | 2.00% | 3.00% |

| |||

| Max Effective Interest Rate: | 3.00% p.a. (at S$100k balance) | ||

| DBS Multiplier Interest Rate Grid | |||

|---|---|---|---|

| Transactions/Month |

|

|

|

| < S$2k | 0.05% | 0.05% | 0.05% |

| S$2k – below 2.5k | 0.40% | 0.60% | 1.20% |

| S$2.5k – below S$5k | 0.40% | 0.70% | 1.40% |

| S$5k – below S$15k | 0.50% | 0.80% | 1.60% |

| S$15k – below S$30k | 0.50% | 1.00% | 1.70% |

| S$30k+ | 0.60% | 2.00% | 3.00% |

| |||

| Max Effective Interest Rate: | 3.00% p.a. (at S$100k balance) | ||

SC Bonus$aver Account v. Maybank SaveUp Savings Account

- Min. Age Requirement

- 16

- Min. Initial Deposit

- S$500 for Singaporeans & PR, S$1,000 for foreigners

- Min. Balance Requirement

- S$1,000

If you're a moderate saver in charge of your household, you may want to consider Maybank SaveUp Savings Account. Account holders earn rate boosts for everyday activities like spending with a Maybank credit card, crediting their salary, and paying monthly loan instalments. Every product a consumer engages with unlocks another rate boost, with up to +2.75% p.a. rewarded for those who engage with at least 3 products. At just S$50k balance–quite attainable–account holders can earn the maximum EIR of 3.00% p.a. This structure makes Maybank SaveUp Savings Account a great option for the average adult who may have several ongoing financial responsibilities.

| Rate Type | Details & Requirements | Interest Rate |

|---|---|---|

| Base Rate |

| 0.15% p.a. on 1st S$3k |

| 0.25% p.a. on next S$47k | ||

| 0.25% p.a. beyond S$50k | ||

| Product Bonus |

| +0.10% p.a. for 1 product |

| +0.7% p.a. for 2 products | ||

| +2.75% p.a. for 3+ products | ||

| Max Effective Interest Rate: | 3.00% p.a. (at S$50k balance) | |

| Maybank SaveUp Savings Account Interest Rates |

|---|

Base Rate: No requirements (rate varies according to band of balance)

|

Product Bonus: Use at least 1 Maybank service or product, ie loan, insurance, investment, credit card etc. (bonus interest based on number of products & applied to entire balance, up to 1st S$50k)

|