Best Personal Loans for Foreigners in Singapore 2024

Personal loans can be useful to help you pay for large or unexpected expenses. Our analysts highlighted the best loan options available to foreigners living in Singapore in order to help you compare interest rates and salary requirements, and ultimately find financing that fits your needs.

- Best Overall Personal Loan: HSBC Personal Loan

- Cheapest Moneylender Loans: Lendela Personal Loans

- Best Cash-On-Instalment: OCBC Cash-On-Instalment Loan

- Best Debt Consolidation Plan: HSBC Debt Consolidation Loan

- Best Personal Lines of Credit: HSBC & Maybank

- How to Choose a Personal Loan

Our Top Picks for the Best Personal Loans for Foreigners in Singapore

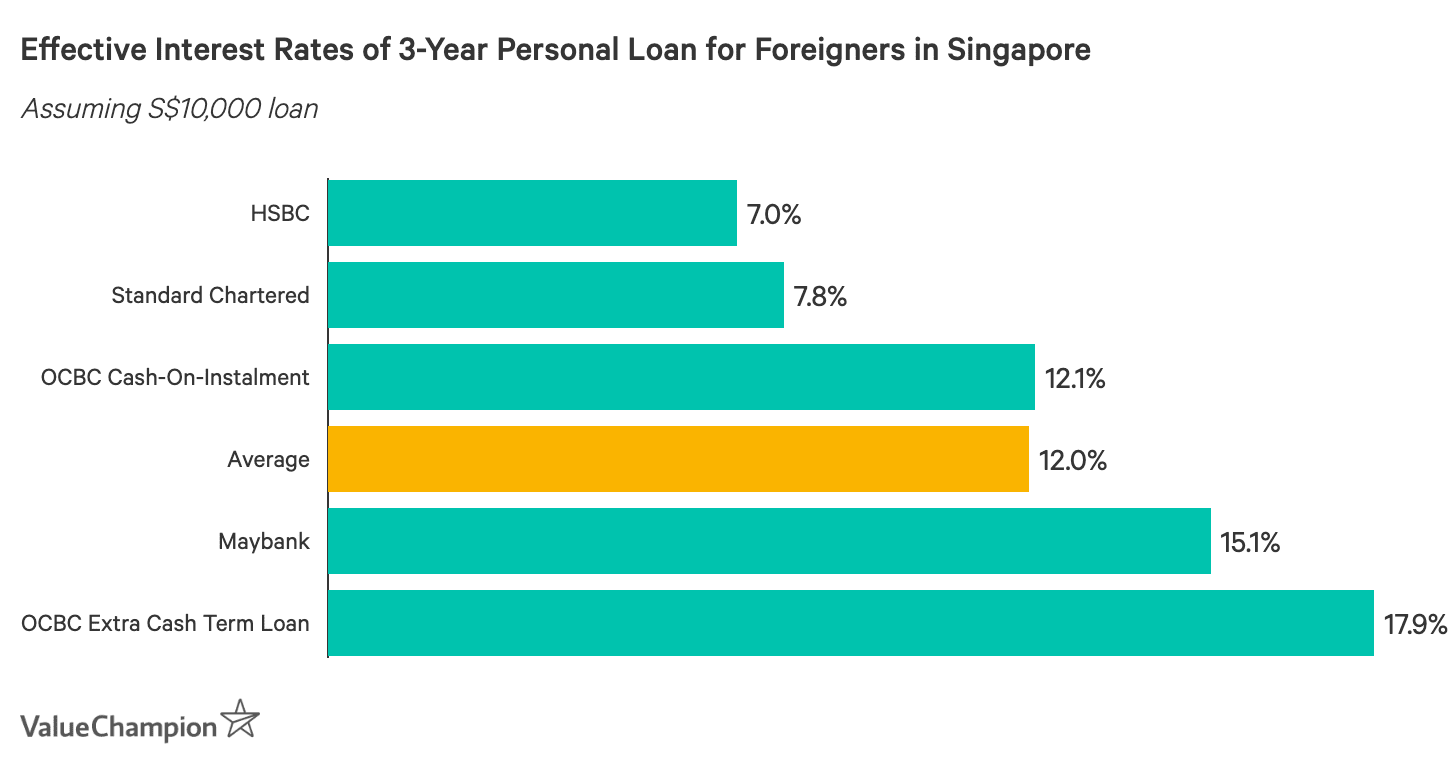

This list represents our recommendations for the best personal loans available to foreigners living in Singapore. We considered factors including interest costs, fees, loan tenures and promotions. The average effective interest cost of all personal loans in Singapore is about 13% to 15%; however, many of the loans in this list charge much lower interest rates making them more affordable. In addition to low interest rates, you should choose a loan that allows you to make affordable monthly payments with the shortest tenure you can manage.

Best Personal Loan for Foreigners in Singapore: HSBC Personal Loan

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||

HSBC's personal loan is the best option for most borrowers. First of all, HSBC's effective interest rate of 6% is the lowest available for personal loans available to foreigners living in Singapore. Additionally, HSBC has the lowest income requirement for foreigners (S$40,000) and waives its S$88 processing fee. Finally, HSBC's personal loan is the only loan that provides tenures up to 7 years, compared to some other banks that only offer personal loans with tenures of up to 5 years. This allows borrowers to reduce their monthly payments by spreading the loan out over a longer period of time. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

- Most Competitive Interest Rates: starting at 6% EIR

- Longest Loan Durations: 1 - 7 years

- Promotions:

- New BAU Promo: S$100 Cashback

- Read Our Full Review

| Loan Duration | Flat Rate | Processing Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 3.2% | 1% | 6% | S$860.00 | S$420 |

| 2 years | 3.2% | 1% | 6% | S$443.33 | S$740 |

| 3 years | 3.2% | 1% | 6% | S$304.44 | S$1,060 |

| 4 years | 3.2% | 1% | 6% | S$235.00 | S$1,380 |

| 5 years | 3.2% | 1% | 6% | S$193.33 | S$1,700 |

| 6 years | 3.2% | 1% | 6% | S$165.56 | S$2,020 |

| 7 years | 3.2% | 1% | 6% | S$145.71 | S$2,340 |

| *Assuming S$10,000 loan and income of S$40,000 (Note that rates above are not indicative of your customised loan offer) | |||||

HSBC's personal loan is the best option for most borrowers. First of all, HSBC's effective interest rate of 6% is the lowest available for personal loans available to foreigners living in Singapore. Additionally, HSBC has the lowest income requirement for foreigners (S$40,000) and waives its S$88 processing fee . Finally, HSBC's personal loan is the only loan that provides tenures up to 7 years, compared to some other banks that only offer personal loans with tenures of up to 5 years. This allows borrowers to reduce their monthly payments by spreading the loan out over a longer period of time.

Best Moneylender Loans for Low-Income Borrowers: Lendela

| |||||||||||||

If you are unable to obtain a cheaper loan from a bank, Lendela is a great way to compare the best moneylender loans. This platform gives prospective borrowers a selection of custom loan offers for their comparison. Lendela also has a relatively low salary requirement (S$1,200 monthly) and most applicants receive more than 1 same-day loan offer. Therefore, Lendela is a solid choice for those that are not eligible for bank loans. | |||||||||||||

- Low Minimum Income Requirement: S$1,200 monthly

- Fast Loan Disbursement: within 1 day

- Promotions:

- No promotions currently offered

- Read Our Full Review

| Loan Details | |

|---|---|

| Monthly Interest Rates | from 0.8% (lower rates for returning borrowers) |

| Lendela Application | Free |

| Processing Fees | Vary by lender |

| Loan Size | S$500 to S$100,000 (or 6x monthly income) |

| Loan Disbursement | Within 1 day |

If you are unable to obtain a cheaper loan from a bank, Lendela is a great way to compare the best moneylender loans. This platform gives prospective borrowers a selection of custom loan offers for their comparison. Lendela also has a relatively low salary requirement (S$1,200 monthly) and most applicants receive more than 1 same-day loan offer. Therefore, Lendela is a solid choice for those that are not eligible for bank loans.

Best Cash-On-Instalment for Foreigners in Singapore: OCBC Cash-On-Instalment

| |||||||||||||||||||||||||||||||||||||||||||

OCBC's Cash-On-Instalment loans are among the cheapest personal loans available to foreigners living in Singapore. This is due, in part, to the fact that the bank offers an exclusive rate of 3.5% to new-to-bank applicants that apply through ValueChampion. With that said, OCBC's Cash-On Instalment loan is not the cheapest personal loan options for those that currently bank with OCBC. | |||||||||||||||||||||||||||||||||||||||||||

- Competitively Priced Long-Term Loans for New Customers

- Exclusive Rate for New Customers 3.5% p.a. (from 6.96% EIR)

- Low minimum loan amount: S$1,000

- Promotions:

- Receive up to S$3,888 cashback when you apply for Cash-on-Instalments online. Valid Until 31 Mar 2023

- Get an additional $100 cashback if you are new to Cash-on-Instalments.

- Read Our Full Review

| Loan Duration | Flat Rate | Processing Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 3.5% | 1% | 8.27% | S$862.50 | S$430 |

| 2 years | 3.5% | 1% | 7.57% | S$445.83 | S$780 |

| 3 years | 3.5% | 1% | 7.27% | S$306.94 | S$1,130 |

| 4 years | 3.5% | 1% | 7.09% | S$237.50 | S$1,480 |

| 5 years | 3.5% | 1% | 6.96% | S$195.83 | S$1,830 |

| *Assuming new-to-bank customer, S$10,000 loan and income of S$30,000, promotion | |||||

OCBC's Cash-On-Instalment loans are among the cheapest personal loans available to foreigners living in Singapore. This is due, in part, to the fact that the bank offers an exclusive rate of 3.5% to new-to-bank applicants that apply through ValueChampion. With that said, OCBC's Cash-On Instalment loan is not the cheapest personal loan options for those that currently bank with OCBC.

Best Debt Consolidation Plan for Foreigners in Singapore: HSBC Debt Consolidation Plan

| |||||||||

HSBC offers the most affordable debt consolidation plans for foreigners living in Singapore due to its low interest rates. For example, for loan tenures of 1 to 7 years, HSBC only charges a flat rate of 4%, compared to other banks that typically charge 5% - 6%. For longer tenures of 8 to 10 years, its rates are still the cheapest at 5.7% compared to other lenders that charge at least 6%. Additionally, online applicants receive S$100 in cashback and have their processing fee waived. | |||||||||

- Lowest Guaranteed Interest Rates: 4% EIR

- Flexible Loan Tenure: 1-10 Years

- Promotions:

- Read Our Full Review

| Details | |

|---|---|

| Processing Fee | Waived |

| Flat Interest Rate 1-7 Years | 4.0% (7.5% EIR) |

| Flat Interest Rate 8-10 Years | 5.7% (10.0% EIR) |

HSBC offers the most affordable debt consolidation plans for foreigners living in Singapore due to its low interest rates. For example, for loan tenures of 1 to 7 years, HSBC only charges a flat rate of 4%, compared to other banks that typically charge 5% - 6%. For longer tenures of 8 to 10 years, its rates are still the cheapest at 5.7% compared to other lenders that charge at least 6%. Additionally, online applicants receive S$100 in cashback and have their processing fee waived.

Best Personal Lines of Credit

Unlike personal instalment loans, personal lines of credit give borrowers the ability to draw from available credit and functions similar to a credit card. This type of loan is beneficial because it only charges interest on the amount that you actually borrow. Because of this, it can actually be cheaper than a traditional personal loan depending on your borrowing habits.

Best Long-Term Personal Line of Credit: HSBC Personal Line of Credit

- Eligibility

- S$30,000 of annual income

- Max. Credit Limit

- 4x monthly salary (8x for annual income > S$120,000; Foreigners 1x), up to S$200,000

- Annual Fee

- S$60, waived for 1 year

- Standard Prevailing Interest Rate: 18.5%

- Standard Annual Fee: S$60 (waived for 1 year)

- Revolution & Advance Interest Rate: 16.5%

- Revolution & Advance Annual Fee: S$60 (waived for 2 years)

- Read Our Full Review

HSBC is the best long-term personal line of credit available to foreigners living in Singapore. The bank charges the lowest effective interest rate for this type of loan at 18.5%, while other banks tend to charge 20%, or more. Additionally, HSBC waives its annual fee (S$60) for 1 year for new customers and 2 years for Revolution, Advance and Premier customers.

Best Short-Term Personal Line of Credit: Maybank CreditAble

- Promotional First-Year Interest Rate: 9.0%

- Prevailing Interest Rate: 19.8%

- Annual Fee: Waived for 2 years (S$80 from year 3)

- Maximum Credit Limit: 4x monthly salary

- Read Our Full Review

Maybank's Creditable is another great personal line of credit that foreigners might want to consider. While this loan charges higher effective interest rates (from 19.8%) than HSBC, Maybank's promotional interest rate during the first year of its personal lines of credit is very low at 9%. This factor makes Creditable a good choice for those who want a line of credit for 2 years or less.

How to Find the Best Personal Loan

Like any other significant financial decision, we strongly suggest that you compare all of your options before choosing a personal loan. While personal loans charge lower interest rates than credit cards and typically have smaller principal amounts than home loans, they are not insignificant endeavors. With that in mind, we suggest that you carefully consider a few factors before applying for a loan.

First, it is imperative to compare the total cost of each loan. This is comprised of interest rate cost and various fees. When comparing interest rates it is essential to understand the difference between effective and flat rates. The flat rate helps you calculate the total interest you will owe over the course of the loan tenure. On the other hand, the effective interest rate (EIR) represents the true economic cost of your loan and helps you compare the interest rates of various loan types. Other costs include fees ranging from loan processing to late fees. It is important to review each loan's fees before applying, in order to understand any cost differences.

Additionally, it is important to consider your monthly payment under each loan. For instance, you want to choose a loan that you will be able to repay in a timely manner and that won't significantly restrict your budget. Typically, loans with longer durations require smaller monthly payments. However, these loans also typically have larger total costs. You must balance these factors in order to find a loan that works best for your financial situation.

What Types of Foreigner Loans Are Available in Singapore?

There are a handful of personal loan types offered in Singapore. Personal instalment loans are the most common. These loans offer borrowers a lump sum upfront, which borrowers then repay in monthly instalments during the tenure of the loan. Personal instalment loans are useful for individuals that need cash in order to pay for a large, one-time expense. Credit lines, or personal lines of credit, are another common type of personal loan. With a personal line of credit, borrowers can "draw" funds as needed based on a limit determined by their bank.These borrowers are charged interest based only on the amount that they actually borrow. Therefore, these loans can be cheaper than other personal loans, depending on your borrowing habits. Personal lines of credit are particularly useful for individuals that plan to borrow small amounts of money on an ongoing basis.

If you've already accumulated a significant amount of personal debt and are looking for a personal loan to pay off your existing debts, you should consider balance transfer or debt consolidation loans . Both loan types help borrowers consolidate and repay their existing loans. For example, balance transfers create one new loan by combining a borrower's existing debts. These loans are particularly attractive to borrows that expect to repay their debts in a short-period of time because these loans typically offer an interest-free period of 3 to 12 months. On the other hand, debt consolidation loans are best for borrowers that require a longer-term option for consolidating their personal debt. These loans provide a lump sum of cash specifically to be used for paying down various existing loans.

What Documents Do You Need to Obtain a Personal Loan?

Typically, licensed money lenders require loan applicants to provide proof of identify, address and income. For proof of identity, foreigners generally must provide a copy of their employment pass and passport. Applicants can typically provide any official document to prove their address, such as a utility bill with name and address shown. Finally, for proof of income borrowers typically need to submit their Central Provident Fund (CPF) contribution history statement, latest Income Tax Notice of Assessment or latest computerised payslip or have salary crediting into the lender’s bank account.

Compare the Best Personal Loans

Please refer to our summary table for the foreigner loan offerings offered by licensed money lenders for foreigners living in Singapore.

| Personal Loans | Best For... | Min. Annual Income | |

|---|---|---|---|

| HSBC Personal Loan | Best Personal Loan | S$40,000 | |

| Standard Chartered CashOne | Best Promotions | S$60,000 | |

| OCBC Cash-On-Instalment | Small, Short-Term Year Loan | S$45,000 | |

| HSBC Debt Consolidation Plan | Best Debt Consolidation Plan | S$30,000 | |

| HSBC Personal Line of Credit | Long-Term Credit Line | S$30,000 | |

| Maybank CreditAble | Short-Term Credit Line | S$30,000 |

| Personal Loans | Best For... | Min. Annual Income | |

|---|---|---|---|

| HSBC Personal Loan | Best Personal Loan | S$40,000 | |

| Standard Chartered CashOne | Best Promotions | S$60,000 | |

| OCBC Cash-On-Instalment | Small, Short-Term Loans | S$45,000 | |

| HSBC Debt Consolidation Plan | Best Debt Consolidation Plan | S$30,000 | |

| HSBC Personal Line of Credit | Long-Term Credit Line | S$30,000 | |

| Maybank CreditAble | Short-Term Credit Line | S$30,000 |

Methodology

To arrive at our best personal loan list for foreigners in Singapore, we collected data on all the personal loans from over 10 major loan providers in Singapore, listed in our table below.

Then, we calculated the total cost of each loan. This cost includes everything that a borrower ends up paying to the bank aside from of the loan principal, including processing fees, administrative fees, interest rates. We also considered promotions, such as fee waivers or cashback, which decrease the total cost of a loan. We assume that borrowers make timely monthly installments, which helps them avoid additional fees, such as late payment fees or early payment fees. This page only considers the loans that are offered to foreigners living in Singapore. For those who are interested, we've also developed a complete list of the best personal loans in Singapore.

Read More:

Stephen Lee is a Senior Research Analyst at ValueChampion, specializing in insurance. He holds a Bachelor of Arts degree in International Studies from the University of Washington, and his prior work experience include risk management and underwriting for professional liability and specialty insurance at Victor Insurance. Additionally, Stephen is a former US Peace Corps Volunteer in Myanmar (serving between 2018-2020), where he continues to provide business development consulting services to HR companies in Asia Pacific.