CIMB AWSM Credit Card Review: What's the Verdict?

CIMB AWSM Credit Card Review: What's the Verdict?

ValueChampion Rating ![]()

Pros

- Students, NSFs & low-income consumers earning less than S$30,000/year

- People with high spend on dining, entertainment, online shopping & telco

- Individuals interested in discounts & deals in Indonesia and Malaysia

Cons

- Individuals who earn more than S$30,000/year

- People who tend to eat in, and prefer to shop offline

- Young adults looking for cashback on their utilities spend

CIMB AWSM Card is the best on the market for low income working adults earning less than S$30,000/year. In fact, CIMB AWSM Card is the only no-fee cashback card available to individuals who are under 35 years old and earning just S$18,000/year. As standard, CIMB AWSM Card is also available to students and NSFs with no income. All cardholders earn a respectable 1% cashback on dining, entertainment, online shopping, and telco, and have access to special offers across SE Asia with CIMB Deals & Discounts.

CIMB AWSM Credit Card Features and Benefits

|

|---|

Key Features:

|

What Makes CIMB AWSM Credit Card Stand Out

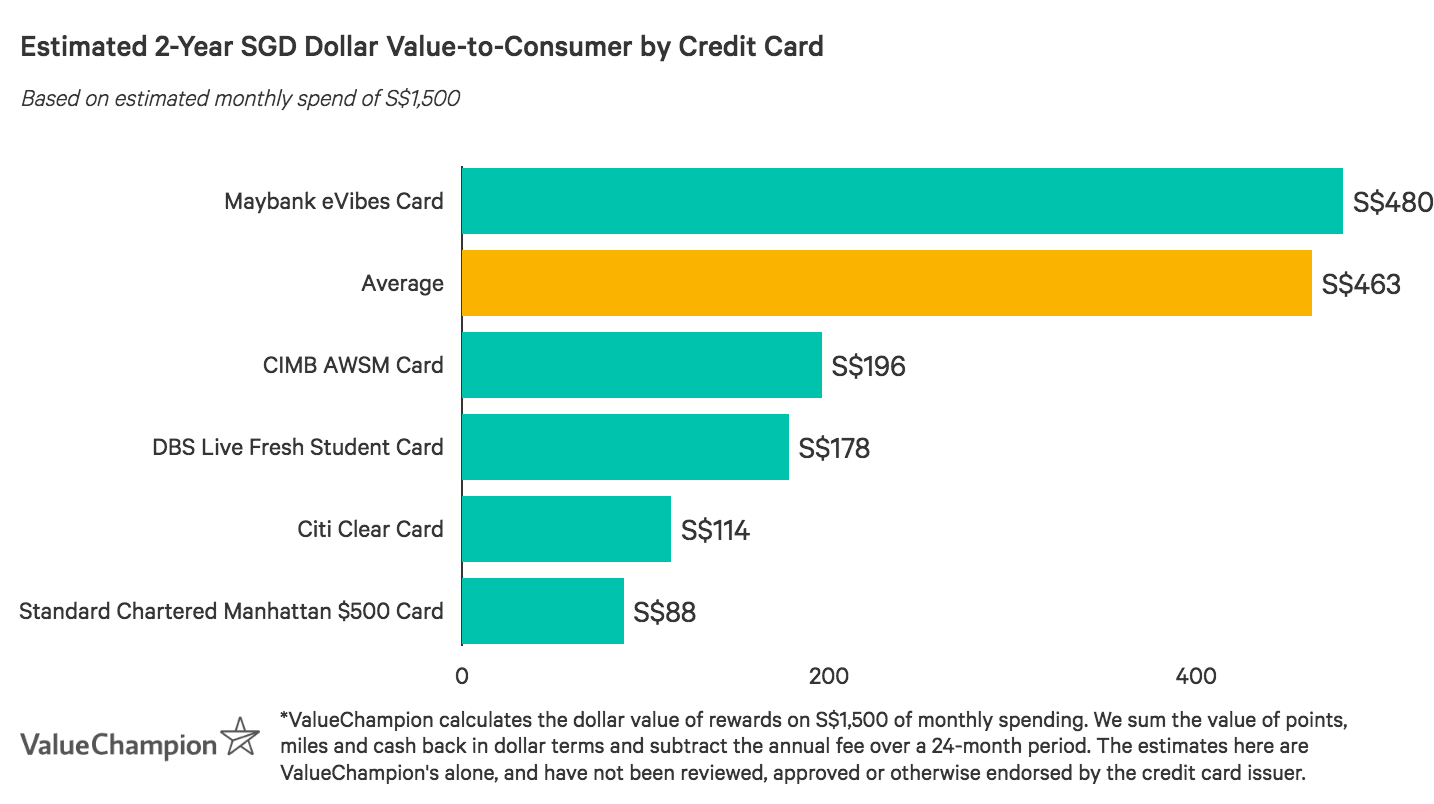

CIMB AWSM Card offers students, NSFs, and low-income working adults a great way to earn cashback in key spend categories. In fact, CIMB AWSM Card is one of the few available to salaried employees earning just S$18,000–the other being Standard Chartered Manhattan S$500 Card–and unlike its competitor, CIMB AWSM Card does not charge an annual fee. Cardholders also earn cashback at a respectable 1% rate, compared to as little as 0.25% with competitors.

Unlike a few similar cards, however, CIMB AWSM Card only rewards spend in select categories. Cardholders earn 1% cashback on dining, entertainment, online shopping, and telco. While these are key spend areas for most consumers, groceries, petrol, offline retail and more do not earn rebates. Utility payments are also ineligible for rewards. Consumers looking for cashback on practical expenses may prefer a flat rate alternative like Maybank eVibes Card.

Ultimately, CIMB AWSM Card is great for students, NSFs, and low income working adults because of its accessibility (no minimums, no caps, no fee) and respectable rewards rate.

How Does CIMB AWSM Credit Card’s Rewards Program Work?

Use our quick and easy-to-read guide below to learn how you you can redeem card rewards.

- Every 1 dollar of cashback earned is equal to S$1

- Cashback is credited to the cardholder's account in the following month

- Cashback is automatically forfeited and is non-transferable when an account is closed

CIMB AWSM Credit Card Rewards Exclusions

Some credit card expenditures are ineligible for earning rewards. We identify these exclusions below.

How does CIMB AWSM Credit Card Compare Against Other Cards?

- Pros

- Students, NSFs & low-income consumers earning less than S$30,000/year

- People with high spend on dining, entertainment, online shopping & telco

- Individuals interested in discounts & deals in Indonesia and Malaysia

- Cons

- Individuals who earn more than S$30,000/year

- People who tend to eat in, and prefer to shop offline

- Young adults looking for cashback on their utilities spend

Read our comparisons of CIMB AWSM Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need.

CIMB AWSM Card v. Standard Chartered Manhattan S$500 Card

- Pros

- Low-income young adults earning less than S$30,000/year

- People looking for a straightforward cashback card

- Cons

- Students & NSFs looking to maximise cashback rewards

- Consumers seeking cards with extra benefits & rebates

- People who want to avoid card fees altogether

Standard Chartered Manhattan S$500 Card is also available to low income working adults making just S$18,000/year. However, it charges a S$32.1 fee (waived 1 year). Also, cardholders earn just 0.25% cashback. While this is a flat rate–rather than category specific–it’s much lower than that offered by CIMB AWSM Card. Low income employees who spend more on groceries than on dining, or shop offline, might prefer SC Manhattan S$500 Card.

CIMB AWSM Card v. Citi Clear Card

- Pros

- Great for student/young adult budgets

- Good rewards at Starbucks, Dunkin’ Donuts and Subway

- Cons

- Not suitable for salaries above S$30,000/year

- Lacks rewards on education and bills

Students and NSFs without income can earn the equivalent of 0.4 miles per S$1 spend with Citi Clear Card. Cardholders also have access to great dining discounts through Citi Gourmet Pleasures. Low income working adults, however, are not eligible for the card. Such individuals, as well as those with spend focused on entertainment or online shopping, may instead be interested in CIMB AWSM Card.

CIMB AWSM Card v. Maybank eVibes Card

- Pros

- Students & NSF earning less than S$30,000/year

- People looking for easy cashback on all spend

- Individuals hoping to avoid paying an annual fee

- Cons

- Young adults who’d prefer a card with EZ-Link functionality

Maybank eVibes Card offers top rewards rates to students and NSFs, with 1% rebate on all spend with no minimums or earning caps. New cardholders also receive an Adidas wristwatch as a welcome gift. However, this card isn’t available to low income working adults; such individuals may benefit instead from CIMB AWSM Card.

Read Also:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.