Don't Fall for These 7 Myths About Car Insurance

Buying car insurance can be a complex process. But if you want to get the best value for your money, it's important to get off on the right foot by having as clear an understanding of how buying car insurance in Singapore works. That's why our team at ValueChampion has compiled this list of the top 7 myths about car insurance you don't want to fall for.

1. Your car insurance plan will pay for everything after a car accident

If this is your first time buying comprehensive car insurance, you may be under the misconception that as long as you pay your annual premium, you don't have to worry about paying for any other expenses out of pocket if you get into a car accident. That's the whole point of car insurance, right?

Wrong. Every car insurance policy will include something called the "policy excess" or "standard excess," termed alternatively as the "deductible." This is a set amount of money that you will have to pay out of pocket before your insurer will step in to cover the costs of repairing your car and any other bills (medical, etc.) you may have incurred. The excess helps to mitigate the risk insurers take on in covering your potential losses by making sure you have some skin in the game and won't abuse your car insurance plan by engaging in reckless or dangerous driving behavior.

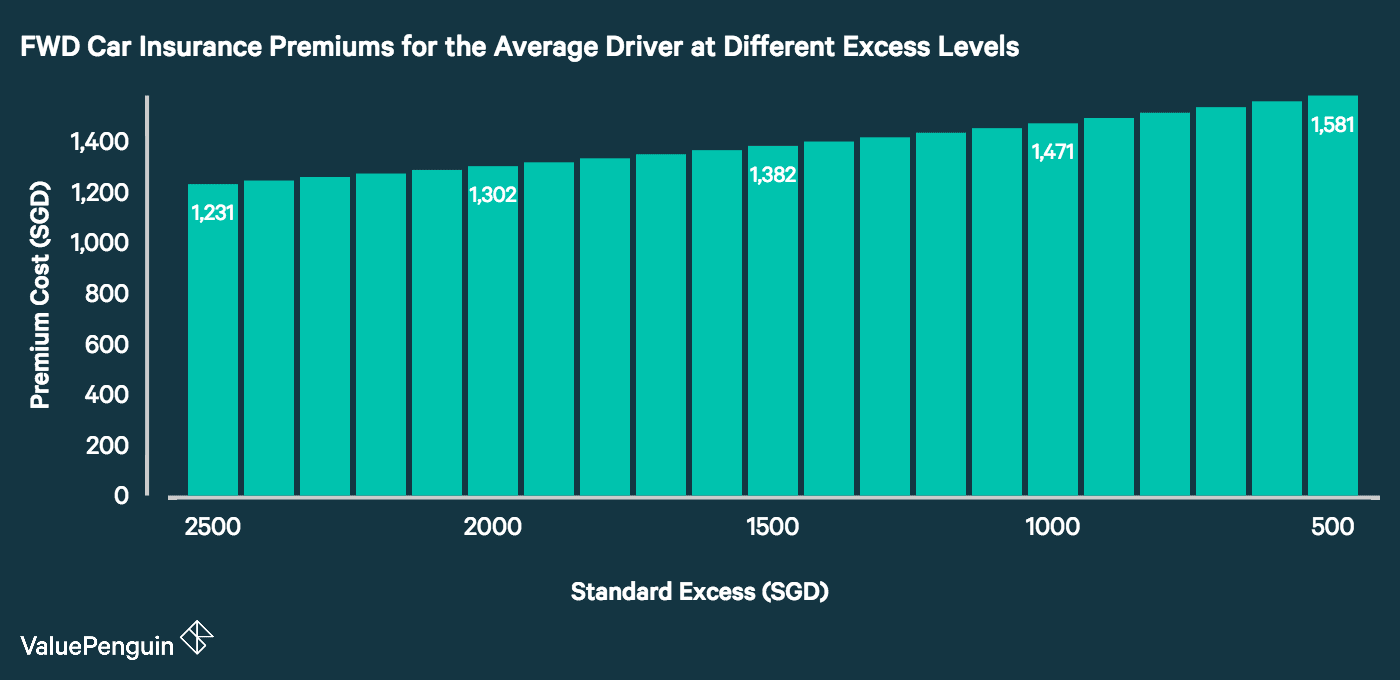

The typical standard excess in Singapore tends to range between S$600 and S$1,000, with insurers differing in how much they'll allow you to adjust it. Some major insurers offer very limited options to adjust your standard excess for a higher or lower premium during the car insurance purchasing process, whereas others are much more flexible. FWD, for example, lets you set your excess anywhere from S$500 to S$2,500, and Etiqa will let you adjust your excess from S$200 to S$2,500.

The reason you might want to adjust your standard excess to a higher or lower amount is because doing so will affect how much you have to pay in premium costs. If you set a higher excess, you can lower your premium; and if you set a lower excess, your premium will increase. For example, the average 45-year-old male driver with 5 years' driving experience and 0% NCD of a 2016 Toyota Corolla Altis 1.6 could save up to S$350 on car insurance from FWD just by changing how much he wanted his standard excess to be. If you want to minimise the shock that a mandatory outlay of hundreds of dollars out of pocket after an unexpected event like a car crash will have on your wallet, you may wish to opt for a higher premium. But if you are less risk-averse or more concerned with minimising certain costs as opposed to potential or unlikely costs, you may consider setting a slightly higher standard excess for a slightly lower premium.

2. You have to pay more for car insurance if you drive a red car

You might suspect that consistent with the urban legend that red cars get pulled over and ticketed more frequently, drivers of red cars have to pay more for car insurance. It turns out that this is not usually the case, however, for the simple reason that most insurers won't even ask you to provide them with the color of your car when you apply for car insurance. If they don't know what color your car is, they can't charge you more or less on your premium based on that variable. There can be exceptions, however. In the course of our research, we noticed that a few insurers may actually collect this data and use it when calculating how much your premium should be. It may impact your premium by anywhere in the range of S$5 to S$40. As always, we recommend that you compare the quote you get from one insurer against a good number of others based on your driver profile to see which insurers may offer you the best deal for the amount of coverage you require.

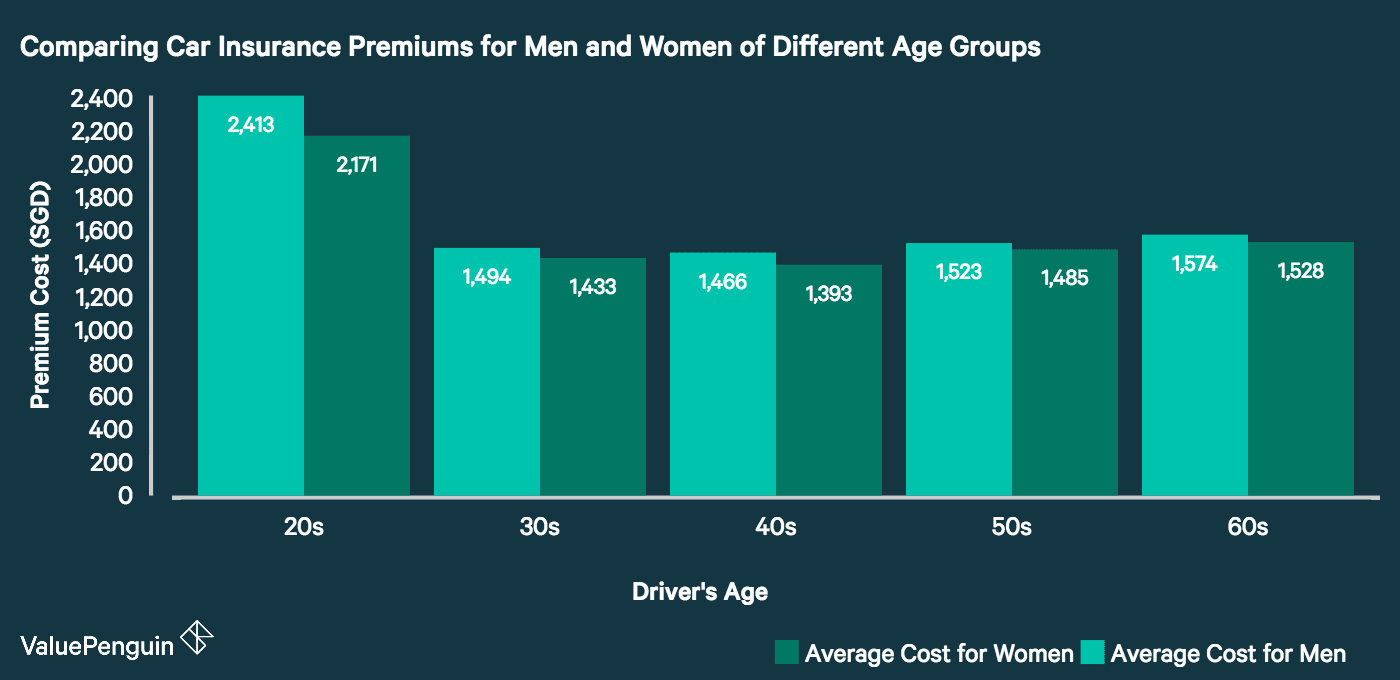

3. Women have to pay more for car insurance because they're worse drivers

One popular stereotype that has held up through the ages is that women are, for whatever reason, worse drivers than men. As such, you'd expect them to get into more accidents and consequently have to pay more for car insurance based on being a statistically more risky demographic.

Actually, insurance companies consider men to be a much riskier bet to insure than women, since it turns out that men are statistically more accident-prone than women - and we know exactly how much more accident-prone they are. Based on Aviva's claims data from 2015, men are 1.4 times more likely to get into a car crash as women. So it comes as no surprise that holding all other variables such as age and driving experience equal, we found that male drivers always pay more on car insurance premiums than female drivers. If you're a woman, depending on your age, you might expect to pay anywhere from about S$40 to about S$250 less than a man sharing your driver profile would.

The premiums reflected in the above chart assume a driver with 5 years of driving experience and 0% NCD with a 2016 Toyota Corolla Altis 1.6.

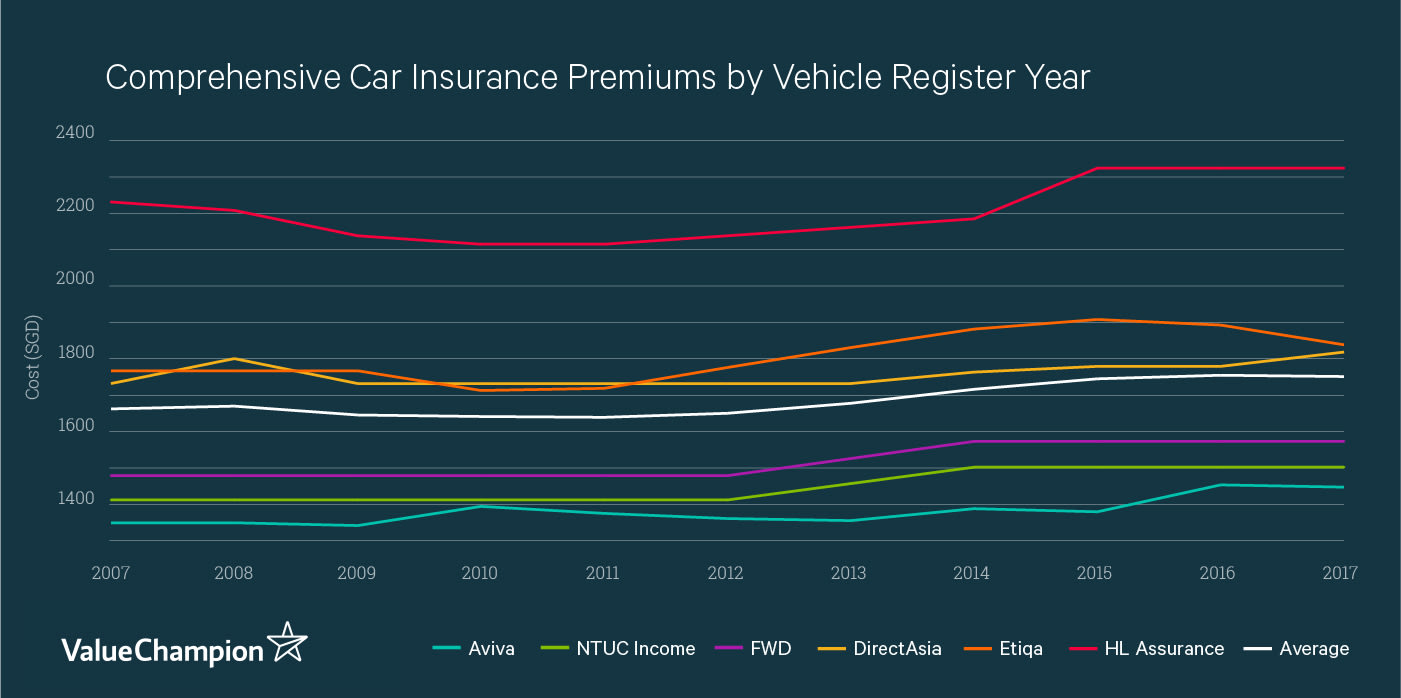

4. You have to pay a higher premium as your car ages

What happens to your car insurance premium as your car gets older? If asked, the average person might guess off-hand that it rises as your car's parts start to wear down from age and use. But the truth is a little more complicated. Our team at ValueChampion looked at how car insurance premiums for comprehensive and third party plans change as the reported age or registration year of the vehicle to be insured changes. We found that in aggregate, the cost of car insurance is highest when a car is newest (in its first 2-3 years on the road), falls as it ages up to 10 years old, and then tends to begins to rise again in small increments.

However, the average is not always reflective of how individual insurers handle this matter. Some insurers actually decrease their prices or hold them constant as the car in question begins to age past 10 years old, presumably having accumulated a significant amount of mileage by that time. And some insurers don't just increase their premiums a little for aging cars, they increase them quite significantly. That's why it's always in your interest to continually survey the competition each year it's time to renew your car insurance plan to see if there's a better deal out there.

5. Comprehensive car insurance is always worth it

The most common type of car insurance bought in Singapore is comprehensive car insurance, which covers not only your liability to losses or damages caused to the other party in a car accident but also your own losses and damages, to your car, your person, your belongings and even your passengers. It's the most popular kind of car insurance for good reason, as it offers you significantly more protection of your assets in the case of an accident and is often worth spending the extra cash on.

But not always. What makes a comprehensive car insurance plan most valuable is the insurer's commitment to paying the full cost (minus the excess) of repairing your car after a crash, or paying out the amount of its Open Market Value (OMV) if the cost of repairing is determined to exceed its OMV. This is great when your car is on the newer side, because its OMV will not have depreciated too much yet. But after enough years, your car's OMV will have depreciated to the point where it's much more likely that if you get in a bad crash, your insurer will simply pay out its remaining OMV and scrap the car - and the payout you receive may be extremely low. So low, in fact, so as to not be worth the cost of paying for a comprehensive plan. In this scenario, you may be better suited by a third party only (TPO) or third party, fire and theft (TPFT) car insurance plan with a significantly lower premium.

6. Your insurance covers you if you get into a car crash driving someone else's car

Be careful not to assume that your car insurance plan covers you when you're driving someone else's car. If you read the terms and conditions of most car insurance policies, it becomes clear that you (and however additional named or unnamed drivers your policy accommodates) are insured under your plan when driving only your vehicle. So if you drive another person's car, whether or not you are covered will depend on the specific terms of their car insurance plan, not yours. So before you get behind the wheel of your friend's car, make sure that you're not setting yourself up for unnecessary risk and unanticipated expense should something go wrong.

7. It's not worth the hassle to scope out the competition when it's time to renew your plan

Going through the process of buying car insurance can be a bit of a hassle, and it's certainly not a task most of us want to spend any more time and energy on than is necessary. But taking the time to do your research can save you from paying much more than you actually need to for solid coverage. While you might think that many insurers will tend to offer you similar premiums and that the difference between prices you're quoted may not be enough to justify going to all the extra trouble, our study of the best cheapest car insurance plans in Singapore found that the average Singapore driver could save up to about S$800 just by scoping out the competition to find a better deal - without having to sacrifice crucial benefits and coverage levels.