DoorDash's IPO Just Makes Uber & Airbnb Look Better

Along with Airbnb, DoorDash is planning one of the most hotly anticipated IPO of 2020. Its anticipated valuation is also similar to Airbnb's at around $32bn. While we have a positive outlook for Airbnb, our evaluation of DoorDash is more negative. In short, DoorDash's tremendous growth and market share gains, particularly during the COVID-19 pandemic, don't seem defensible in the long run. A closer look at the facts and similar industries around the globe actually just makes Uber look more attractive as an investment since there's nothing structure that prevents Uber from making DoorDash into a Lyft of food delivery industry.

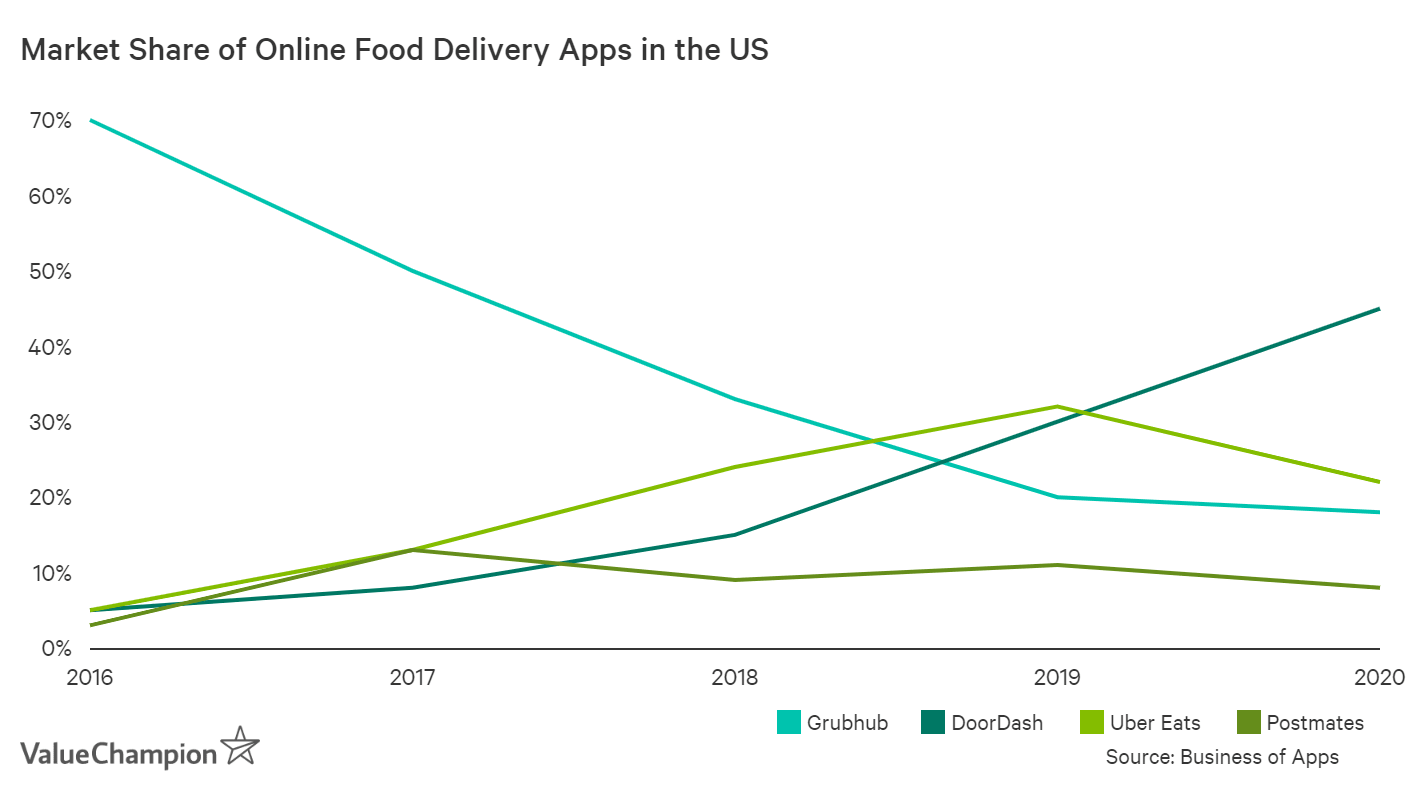

DoorDash's Explosive Growth Is Purely Due to Its Suburban Focus

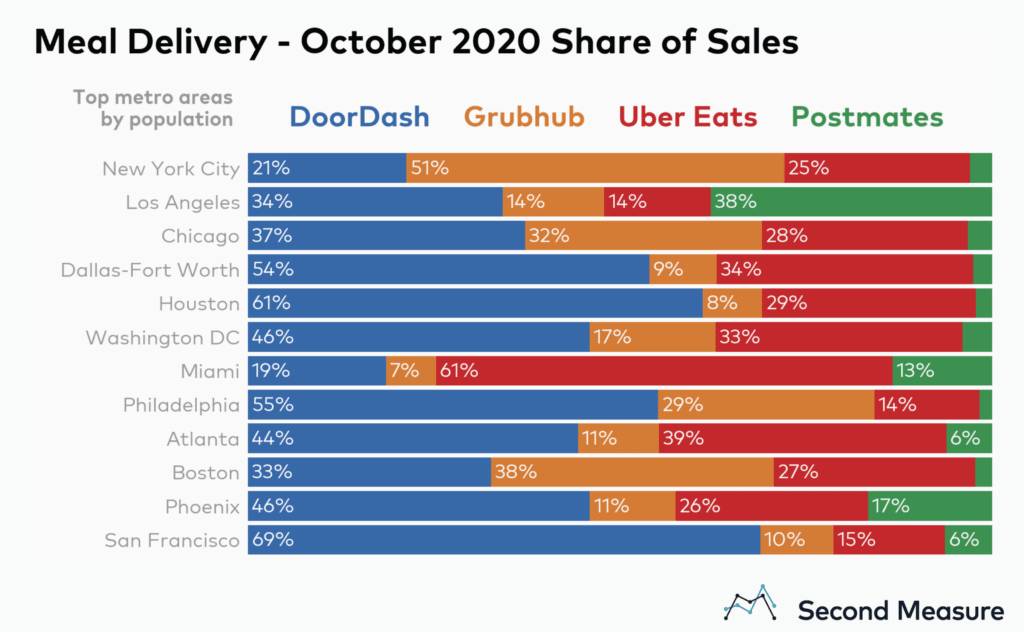

The most prominent bull thesis on DoorDash is that it is, and will continue to be the market leader in a growing market. For instance, its market share in meal delivery has reached 51% as of October 2020, a very impressive feat for a company that has been competing against giants like GrubHub and Uber Eats.

DoorDash's secret sauce has mostly been its focus on suburban areas. While GrubHub, Uber Eats and Postmates have been competing fiercely for market share in urban markets, DoorDash simply casted a wider net on areas that its competitors weren't paying much attention to. And the COVID-19 pandemic boosted its market share even further as consumers and their wallets moved away from cities to suburbs. Competitors like GrubHub and Uber Eats that had a much bigger exposure to markets like New York suffered due to this transition.

DoorDash's Lead in Suburbs Is Not Defensible

Certainly, DoorDash and its management team deserve all the credit for making such a strategic decision and successfully executing on their plan. Even in NYC, where GrubHub has enjoyed a massive market share, we actually see more restaurants on DoorDash in suburban areas outside of Manhattan like Queens and Brooklyn. However, their success doesn't seem defensible for a few reasons.

First, aside from their geographic focus, their product isn't inherently different from those of competitors. They all offer deliveries from restaurants, and charge similar levels of fees. And more importantly, the global travel industry, food delivery industry in China and global ride hailing industry have all proven that merchants who are already using an online marketplace want to be on others in order to maximize their business. Just like hotels and airlines, most restaurants and drivers that are already on DoorDash are highly motivated to get on Uber Eats and Grubhub to get more business as long as these platforms provide similar treatments, especially during a pandemic driven recession. Uber Eats had thus far chosen not to focus on suburbs because it was prioritizing bigger markets while controlling their cost. Now that DoorDash has proven how attractive suburban markets have become due to COVID, there's nothing structural that prevents Uber Eats from aggressively expanding in DoorDash's hometurf.

Uber's Structural Advantage

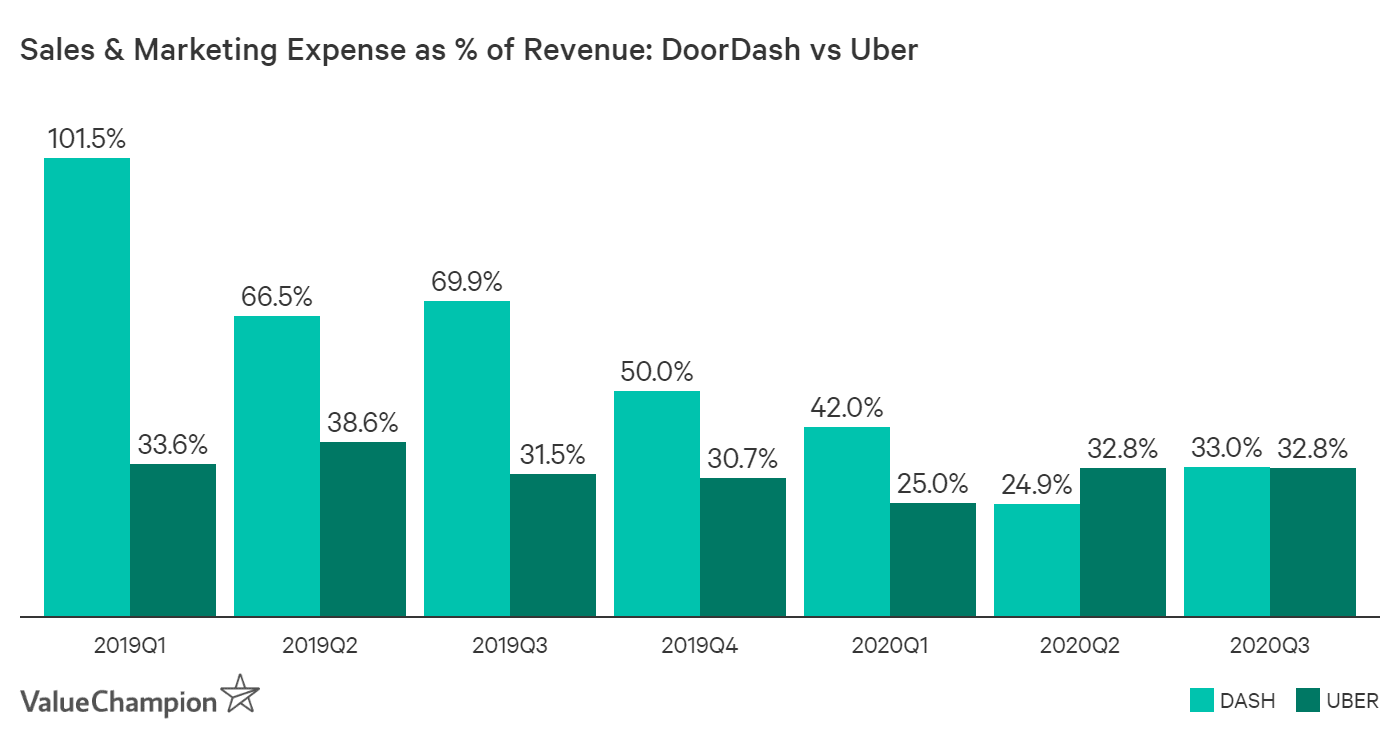

And Uber has every motivation to grow its delivery business aggressively because its main ridesharing business has been suffering due to the pandemic. This is where Uber's structural advantage comes into play. First, unlike its rivals, Uber can make money from the same user and rider in 2 different ways, rides and food delivery. This means that Uber could potentially acquire customers more efficiently, shown by its lower S&M marketing expense historically (prior to COVID). This also means that Uber could potentially afford to spend more than its competitors to acquire customers (i.e. marketing and promotions) to or to simply charge them slightly less. Secondly, Uber's warchest of $8bn of cash sitting in its bank account (compared to roughly $4.5bn DoorDash is about to have after its IPO) means it can indeed do exactly this.

Uber already has drivers and riders in many suburban markets. All it has to do is to call restaurants that are already on DoorDash in those areas, and spend some money on marketing and promotions to get consumers to use Uber Eats in those areas. When DoorDash was private, it could afford to spend aggressively because it didn't have investors who care about profit. Now that it's publicly listed, it will be playing on the same field as Uber under public scrutiny. With a smaller warchest, and a structural disadvantage of just playing in food delivery (as opposed to delivery and rides), DoorDash starts to look a lot like Lyft. On the flipside, Uber starts to look more attractive because its potential to grow its food delivery business seems more sure than ever.

Tale of Two IPOs

Airbnb and DoorDash may seem similar at first glance. Both are hot consumer technology companies valued at around $30bn, competing against larger companies valued at around $85bn. However, there's a big difference between the two companies. Airbnb has a distinctive competitive advantage in being the trusted network of travelers and single-home owners who aren't motivated solely by money. The travel leader Booking.com has been trying to compete against it for several years with limited success.

| Company | Valuation |

|---|---|

| ABNB | $35bn |

| BKNG | $86bn |

| DASH | $32bn |

| UBER | $90bn |

On the other hand, DoorDash's success has been a result of different choices the company made compared to its major competitors. While DoorDash expanded into suburban areas, Uber Eats chose to care more about urban markets. And while Airbnb's core user base that keeps it unique (i.e. single-home owner hosts) is loyal to the platform, DoorDash's core customer base that keeps it unique (i.e. restaurant owners in suburbs) have every motivation to not be loyal. This crucial difference implies that the valuation of $30bn is much more favorable for Airbnb than it is for DoorDash.

Nothing herein should be construed as any past, current, or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.