FWD Home Insurance: Why it is Worth a Look

FWD Home Insurance: Why it is Worth a Look

ValueChampion Rating ![]()

Pros

- High value across all plans

- Great customisation options

- No excess on claims due to fire or burst pipes

- Pet-friendly benefits

Cons

- Lower sublimits on coverage may not appeal to high-networth individuals

- Not the highest sub-liit for expensive valuables like artwork or jewelry

FWD Home Insurance's competitive prices and generous coverage makes it one of the highest value-for-money plans on the market for the average HDB and Condo owner-occupier. However, while FWD offers a wide array of coverage, it may not appeal to affluent consumers with expensive valuables, as its sub-limits for artwork, jewelry and other valuable items are quite low. Nonetheless, FWD Home Insurance is still one of the best home insurance plans out there in the market.

| Summary of FWD Home Insurance |

|---|

| One of the highest value options available for the average condo or HDB owner |

| Zero excess on claims due to fire or burst pipes |

| Great option for pet owners |

| Not the best option for high net-worth individuals |

| S$5 off if you have a security system or full-time domestic helper |

Table of Contents

FWD Home Insurance Highlights

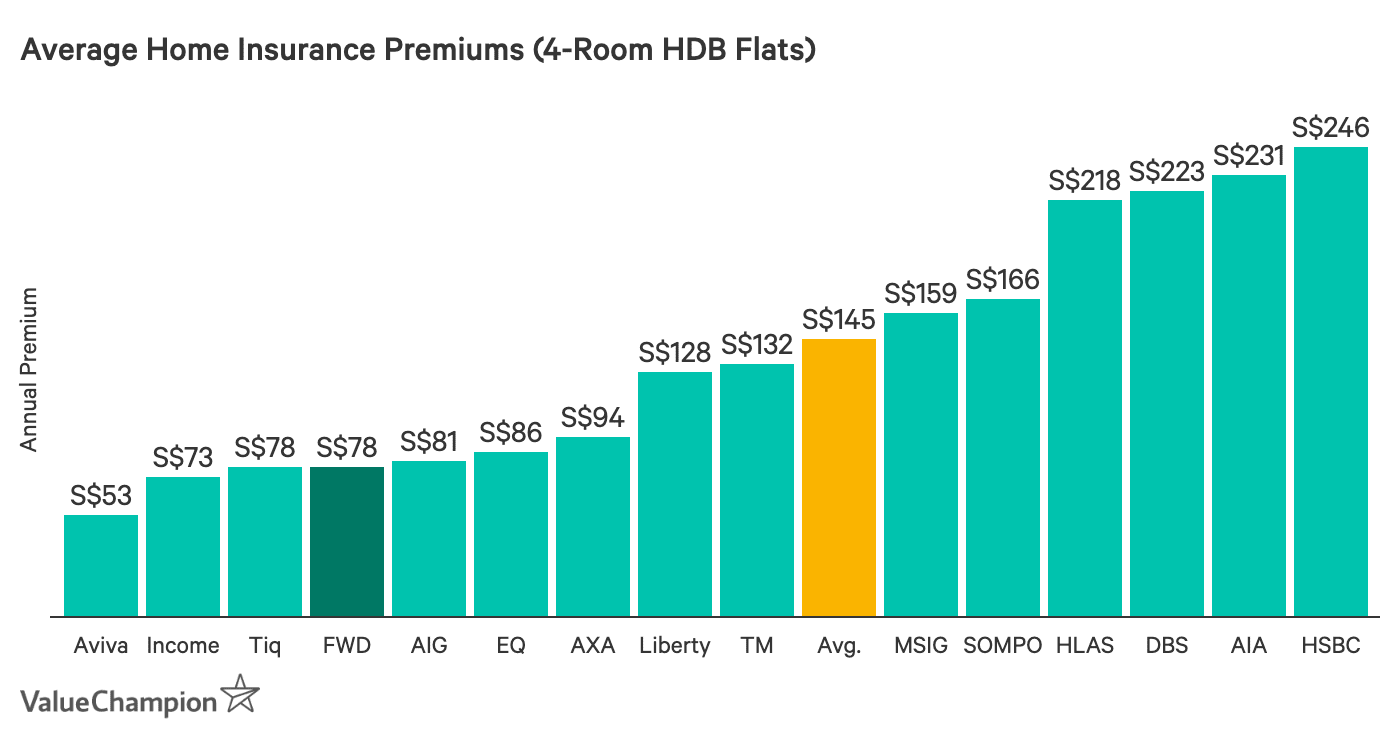

The average HDB or condo owner-occupier can find a winner with FWD's home insurance plan, as it covers all the necessary bases for highly competitive prices. First, its premiums cost 46-51% below the industry average, even when you choose to maximise your contents and renovation coverage. Second, FWD lets you customise your policy based on number of rooms, renovation, content and building coverage. This policy design not only allows for flexibility, but it also lets you pay only for the amount of coverage you need. Renters and landlords also have their own plans, with tailored benefits to match their needs. Since you will be choosing your own coverage limits, you should make sure you know the exact amount you'll need to cover everything sufficiently, although FWD is unique in not penalizing underinsuring. To get an estimate, you can consult our guide on average cost of home contents and average cost of home renovations.

However, while FWD is a great option for the average homeowner or tenant, it may not provide the right coverage for certain niche customers. For instance, affluent consumers with expensive belongings may not find the sublimit for artwork and valuables high enough at S$1,000. Also, there isn't any cover for moving damages. Thus, if you have very expensive belongings or you tend to move around often, insurers such as AXA or MSIG may be a better fit than FWD.

FWD Home Insurance for HDB & Private Property Owners

If you are a cost-conscious HDB or condo owner-occupier, you will be pleasantly surprised with the 40-50% below market average prices for 3,4 or 5 room flats. Additionally, you will receive coverage for repairs or reconstruction, alternative accommodation, storage, conservancy and firefighting appliances, as well as home assistance for electrical, plumbing, locksmithing and air-conditioning. If you insure more than S$40,000 of home contents, you will also increase your alternative accommodation benefit to S$35,000—one of the highest on the market. Combined with no excess for burst pipes and fire claims, and affordable add-ons for pet and personal accident coverage, the average home-owner will get the best valued home insurance plan on the market.

| Home Size | Contents Coverage | Renovation Coverage | Building Coverage | Premium |

|---|---|---|---|---|

| 3-Room | S$20K | S$40K | N/A | S$44.58 |

| 4-Room | S$40K | S$60K | N/A | S$69.38 |

| 5-Room | S$60K | S$80K | N/A | S$98.87 |

| Multi-Gen | S$80K | S$100K | N/A | S$123.71 |

| HDB Industry Average | S$50,623 | S$125,989 | N/A | S$157.00 |

| 2-Bed | S$20K | S$40K | N/A | S$40.36 |

| 3-Bed | S$40K | S$60K | N/A | S$79.74 |

| 4-Bed | S$60K | S$80K | N/A | S$109.27 |

| Condo Industry Average | S$54,896 | S$136,695 | N/A | S$186.00 |

| Home Size | Contents Coverage | Renovation Coverage | Building Coverage | Premium |

|---|---|---|---|---|

| 3-Room | S$20K | S$40K | N/A | S$44.58 |

| 4-Room | S$40K | S$60K | N/A | S$69.38 |

| 5-Room | S$60K | S$80K | N/A | S$98.87 |

| Multi-Gen | S$80K | S$100K | N/A | S$123.71 |

| HDB Industry Average | S$50,623 | S$125,989 | N/A | S$157.00 |

| 2-Bed | S$20K | S$40K | N/A | S$40.36 |

| 3-Bed | S$40K | S$60K | N/A | S$79.74 |

| 4-Bed | S$60K | S$80K | N/A | S$109.27 |

| Condo Industry Average | S$54,896 | S$136,695 | N/A | S$186.00 |

FWD Home Insurance for Landed Property Owners

Landed property owners won't get too much value from FWD home insurance for a few reasons. First is that it simply doesn't offer as great of a value compared to other plans like Income, Great Eastern and AXA. It offers only up to S$100,000 of renovation coverage and up to S$1,000,000 of building coverage. This may be alright for smaller landed properties, like terraces and semi-detached houses, but it will fall short for bungalows, which typically require more than S$1,000,000 of building coverage. Furthermore, the low valuables sub-limit of S$1,000 per item may not be enough for wealthy homeowners. Lastly, we found that even when FWD is offering promotions greater than 20% off, its premiums are still more expensive compared to the aforementioned insurers.

| Home Size | Contents Coverage | Renovation Coverage | Building Coverage | Premium |

|---|---|---|---|---|

| Terrace | S$60K | S$100K | S$400K | S$301.87 |

| Semi-Detached | S$80K | S$100K | S$600K | S$412.12 |

| Bungalow | S$100K | S$100K | S$1M | S$601.13 |

| Landed Property Average | S$77,500 | S$113,462 | S$846,154 | S$570.00 |

| Home Size | Contents Coverage | Renovation Coverage | Building Coverage | Premium |

|---|---|---|---|---|

| Terrace | S$60K | S$100K | S$400K | S$301.87 |

| Semi-Detached | S$80K | S$100K | S$600K | S$412.12 |

| Bungalow | S$100K | S$100K | S$1M | S$601.13 |

| Landed Property Average | S$77,500 | S$113,462 | S$846,154 | S$570.00 |

FWD Home Insurance for Landlords & Tenants

If you are a landlord looking for peace of mind benefits in your home insurance policy, you will find them with FWD. Though it may not offer the highest landlord-related benefit limits on the market, it is still one of the highest value plans due to its low cost and comprehensive coverage. On top of the standard renovation coverage of your choosing, you will also receive S$3,000 of loss of rent coverage for 3 months (after the first two months of tenant default) and S$3,000 of landlord-tenant legal dispute coverage. There is also a workmanship guarantee feature that will ensure FWD's repairs for up to 6 months (when done by their recommended contractors). This can be a good peace of mind addition in the event your apartment is damaged and you don't want to waste time looking for a contractor yourself.

If you are a tenant, FWD offers flexible plans that are also budget friendly. It is currently the cheapest tenant plan on the market if you choose their smallest level of contents coverage, with premiums that cost 60% below average. In addition to providing an option to choose between S$20,000 and S$100,000 of contents coverage, FWD offers tenant-specific protections like S$500,000 of liability coverage for accidental damages to the apartment, as well as S$3,000 of legal coverage costs for tenancy disputes. Other than that, you will have the same features as homeowners do, which includes mirror and glass, alternative accommodation, conservancy, home assistance and temporarily stored contents coverage as well as options to add pet and personal accident coverage. Though its value is high due to the low price, its valuables coverage is quite low so those who want to protect expensive items are better off with insurers like Sompo or NTUC Income.

| Coverage | Price |

|---|---|

| HDB Renovation per S$20,000 | S$6.04 |

| Private Renovation per S$20,000 | S$7.40 |

| HDB Contents per S$20,000 | S$24.61 |

| Private Contents per S$20,000 | S$29.53 |

| Coverage | Price |

|---|---|

| HDB Renovation per S$20,000 | S$6.04 |

| Private Renovation per S$20,000 | S$7.40 |

| HDB Contents per S$20,000 | S$24.61 |

| Private Contents per S$20,000 | S$29.53 |

Policy Excess

Home insurance plans generally have excesses in place to prevent very small claims. An excess is your financial obligation before the insurance company steps in to pay for the rest of the claim. Unlike other home insurers, FWD has no excess in place.

Claims & Contact Information

To successfully file a claim with FWD, you must first report the claimable incident as soon as it happens by calling either their emergency assistance or customer service number (linked below). After this, you can find the right form on their website and file your claim online through their portal along with the required documentation. If you are a tenant (renter) and are filing a liability claim, you should provide a police report and and correspondence with your landlord. You must inform FWD of the claim within 30 days. You should also take note that you can not file a claim if your residence has been unoccupied for more than 60 days.

| Contact Information | |

|---|---|

| Emergency Assistance | +65 6322 2072 |

| Customer Service | +65 6820 8888 |

| Claims Information | Guide and Forms |

| Mailing Address | The Chief Executive Officer, FWD Singapore Pte. Ltd. 6 Temasek Boulevard, #1801 Suntec Tower Four, Singapore 038986 |

FWD Home Insurance Summary

Your home is your most expensive investment and also your most valuable asset. Therefore, finding the best home insurance plan can mean considerable savings in the event of unforeseen events. Below, you'll find FWD's features and coverage. If you would like to compare FWD to other policies in the market, you can read our guide to the best home insurance plans in Singapore.

| Benefits | Coverage | Price |

|---|---|---|

| Home Contents | S$20,000-S$100,000 | S$20-S$25 per S$20,000 increment |

| Renovations | S$20,000-S$100,000 | S$5-6 per S$20,000 increment |

| Item Sub-limits | S$1,000 | N/A |

| Temporary Accommodation | S$300/day | N/A |

| Fixed Mirrors and Glass | S$1,000 | N/A |

| Theft or Damage (Temporarily Displaced Contents) | S$5,000 | N/A |

| Home Assistance | S$400/year | N/A |

| Personal Accident | S$100,000/household | S$3 |

| Medical | S$5,000 | |

| Pet Cover (Death, Stolen) | S$1,000 | S$2 |

| Pet Cover (Medical) | S$1,000 | |

| Pet Accommodation | S$50/day |

Protected up to specified limits by SDIC. This is only product information provided. You may wish to seek advice from a qualified adviser before buying the product. If you choose not to seek advice from a qualified adviser, you should consider whether the product is suitable for you. Buying an insurance product that is not suitable for you may impact your ability to finance your future financial needs. If you decide that the policy is not suitable after purchasing the policy, you may terminate the policy in accordance with the free-look provision, if any, and the insurer may recover from you any expense incurred by the insurer in underwriting the policy.