Housing Prices in Singapore Feb 2017: How Much Will Your First Home Cost?

A first home is the largest purchase most people will make during their life. What makes up the total cost of buying your first home, and how much should you expect to pay?

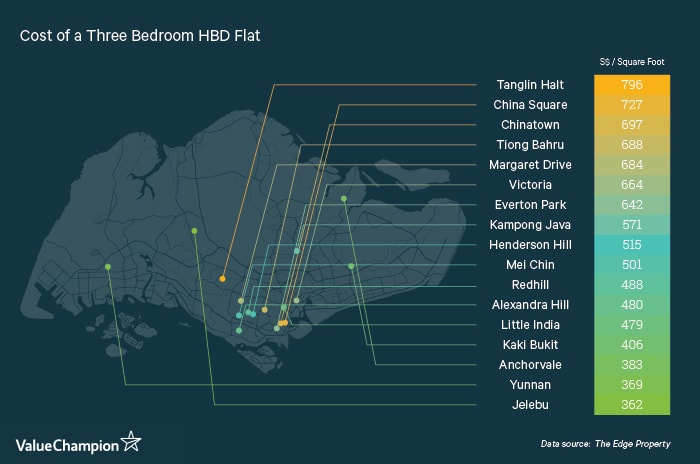

Average Price of Homes in Singapore

Singapore has one of the most expensive real estate markets in the world. For this reason, it can be challenging for a young family or individual to find a good home at a reasonable price on the island. The good news is that our research has shown that real estate prices in Singapore peaked in 2013 and have been on the decline ever since. If you are looking at purchasing for your first home, now may be a good time to buy.

There are several costs that are associated with the purchase of a home which every consumer should be aware of. The big three are:

- The purchase price

- The cost of a bank loan

- Homeowners insurance

While the purchase price is made at the time of purchase, the cost of your bank loan and homeowners insurance are two ongoing costs which will add up significantly over time. Let’s break down each of these costs into their components.

The Purchase Price

A quick search of homes for sale in Singapore will show that most properties sell for between S$400 per square foot and S$2,000 per square foot. Landed property (real estate which includes land ownership) will be at the higher end of this spectrum while apartments, which do not provide any land ownership, can be found closer to S$400 per square foot.

This means that even a 462 square foot, one bed, one bath, HDB apartment will run north of S$200,000. For the average family of four this is much too small and a larger house providing more bedrooms will be optimal. If we look at landed properties with three bedrooms, the price will be S$300,000 or more. This is a good starting point for young families who are searching for a home.

The location will be a major determining factor in price and the table below shows some of the most expensive, and least expensive, three bedroom HDB apartments as of February, 2017.

The Cost of a Loan

Most individuals do not have S$300,000 sitting in a bank account ready for use toward a home. For this reason, many home buyers will use a bank loan to make the purchase of a house possible. We’ve tracked the best home loans in Singapore, and have found that most consumers end up paying between 0.72% and 1.59% annually for a 30-year mortgage.

Each year, a 30-year home loan at 1.59% will cost your family S$12,576 in principle and interest payments. Over the entire life of the loan, this amounts to a S$377,412! While the home in this example cost S$300,000, there were S$77,412 in interest payments required to make the purchase possible. Keep this in mind when thinking about the true cost of a home purchase.

Many homeowners decide to refinance their mortgage periodically. If you are currently paying more than 1.59% on a home loan, this may be an option.

Lastly, is important to note that the Monetary Authority of Singapore has issued rules on the amount of debt a family can take on. In simple terms, your monthly debt payments cannot exceed 60% of your total take home pay. For a family paying S$4,770 per month in home loan payments, they would be required to have S$7,950 in monthly household income. Keep in mind, this assumes the family has no credit card, car loan, or student debt… as your total monthly debt obligations may not exceed 60% of your take home pay.

Homeowners Insurance

If your house is financed through a bank, it is likely that the bank requires you to hold homeowners insurance. In some cases, the bank will even hold this insurance and charge you a monthly fee. The bank requires this type of insurance because technically – they own the property. In the event of a house fire or flood, the entire value of the home could be lost, leaving the bank without any collateral backing the home loan.

There are many types of insurance which consumers can go without. Even if you self-finance the purchase of a home, homeowner’s insurance is a very wise decision. It is important to note that homeowner’s insurance many times covers items within the house in addition to fixtures, walls and windows.

AXA Insurance offers home insurance based on the total value of coverage needed. This is just a summary of benefits and an example from one provider. It is always important to shop around and find the right coverage for you and your family.

| Annual Premium | Fixture, Fitting and Renovation Coverage Limit | Contents (TV, Sofa, Stove…) Coverage Limit | |

|---|---|---|---|

| Standard | S$112.35 | S$50,000 | S$25,000 |

| Classic | S$163.71 | S$80,000 | S$35,000 |

| Deluxe | S$208.65 | S$100,000 | S$45,000 |

| Superior | S$272.85 | S$150,000 | S$55,000 |

| Ultimate | S$353.10 | S$200,000 | S$70,000 |

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.