Three Reasons Why You Should Own & Use A Credit Card & One Reason Why You Shouldn't

Credit cards are one of the most misunderstood financial instruments. When Singaporeans think of credit cards, some of us might relate them to unhealthy credit card debt (with sky-high interest rates), exorbitant annual fees and pesky minimum spending requirements.

However, when you spend carefully and use your credit card strategically, you can take advantage of cashbacks, points and other perks. Ultimately, using credit cards to save money comes down to discipline. If you make it a point to understand how credit cards work, and exercise the right kind of restraint, you can save - or even earn - significant amounts of money in the long run.

Earning Cashback Directly

All credit cards in Singapore offer some sort of reward for using them for your purchases, which include incentives like cashback, reward points (which can be traded for air miles, discount vouchers or actual products), or airline miles. However, the most common reward, and perhaps the most enticing, would perhaps be cashback.

For the uninitiated, cashback refers to receiving back a percentage of what you spend in the form of money. It is akin to getting a perpetual discount whenever you spend. Sounds too good to be true? It really is not. Credit card companies are constantly competing to provide the most competitive rewards for their customers - some cards offer lucrative sign-up promotions, while others offer higher cashbacks for niche spending categories like travel or sustainability.

With so many cards available on the market to choose from, it is no wonder that Singaporeans have a hard time deciding which is the best credit card in Singapore. In particular, it is hard to compare the different cashback rewards across multiple categories for various credit cards. Luckily, we have combed through hundreds of credit cards in Singapore to distil the best credit card for you!

American Express Singapore Airlines Krisflyer Card: Straightforward Miles

| |

For moderate spenders of above S$2,000 a month, the UOB One Credit Card seems to be head and shoulders above the competition for cashback rates. It offers an astounding 10% cashback for popular merchants like Dairy Farm (not the nature park, but a collection of supermarkets and health stores like Giant, 7-Eleven and Guardian), Grab and Shopee. Furthermore, it offers a high base cashback of 3.33% for all other spend, and even incentivises customers with high fuel savings at Shell and SPC.

| |

|

For moderate spenders of above S$2,000 a month, the UOB One Credit Card seems to be head and shoulders above the competition for cashback rates. It offers an astounding 10% cashback for popular merchants like Dairy Farm (not the nature park, but a collection of supermarkets and health stores like Giant, 7-Eleven and Guardian), Grab and Shopee. Furthermore, it offers a high base cashback of 3.33% for all other spend, and even incentivises customers with high fuel savings at Shell and SPC.

|

Citi Cash Back Card

| |

For more savings-oriented consumers who spend most of their budget on the daily necessities like groceries, dining and transport, the Citi Cash Back Card provides global rebates on food and petrol, with a minimum spend of S$800 per month. Even though it offers similarly competitive petrol savings at Esso and Shell, this card lacks rewards for other categories, like entertainment and shopping.

| |

|

For more savings-oriented consumers who spend most of their budget on the daily necessities like groceries, dining and transport, the Citi Cash Back Card provides global rebates on food and petrol, with a minimum spend of S$800 per month. Even though it offers similarly competitive petrol savings at Esso and Shell, this card lacks rewards for other categories, like entertainment and shopping.

|

Hence, by earning cashbacks on your purchases, you can accumulate multiple savings consistently. Knowing your areas of spending, and the best credit card that complements it, is therefore one way to help save money.

For Those Who Possess a Sense of Wanderlust

Frequent traveller that enjoys spontaneous weekend getaways to Bali or Bangkok? Or are you a high-flying businessperson who travels often for work? Or maybe you are a young adult who still possesses a sense of wanderlust to travel during the summer and winter break? Fear not! You can also save money by earning air miles rewards for every spend.

How do miles work to help save money? Depending on the airline, your miles can be used to book flights, redeem hotel stays and other rewards. So, if you travel often, you can capitalise on your travelling-related expenditure to subsidise your future travelling costs! But in order to do that most efficiently, you would need the correct credit card for air miles.

American Express Singapore Airlines Krisflyer Card

|

|

For flying, American Express cards in Singapore are optimised for this purpose. The Amex SIA Krisflyer Card rewards you for flying on our local airline, Singapore Airlines. In particular, it gives almost double the miles rewards for peak vacation periods in June and December, saving you money especially when air fares are at their highest. It also provides air miles with spending on shopping like KrisShop in-flight stores. Beyond that, it also provides you with free travel insurance - which is a must to protect yourself overseas.

| |

|

|

|---|

|

For flying, American Express cards in Singapore are optimised for this purpose. The Amex SIA Krisflyer Card rewards you for flying on our local airline, Singapore Airlines. In particular, it gives almost double the miles rewards for peak vacation periods in June and December, saving you money especially when air fares are at their highest. It also provides air miles with spending on shopping like KrisShop in-flight stores. Beyond that, it also provides you with free travel insurance - which is a must to protect yourself overseas.

|

Credit cards can also provide you with other travel benefits excluding just miles. For the higher spenders, a card that grants you access to luxury travel perks is definitely worth it. In this case, the Citi Prestige MasterCard is unparalleled for those seeking the ultimate travel experience.

Citi Prestige MasterCard

|

|

To begin, Citi Prestige Credit Card cardholders enjoy free unlimited airport lounge access, with bonus nights at hotels worldwide, free limo transfers as well as golfing privileges. It also offers excellent rates, at 1.3 miles for every S$1 local spend, with a 25,000 bonus miles annually. However, the drawback would be that this card is designed for the more affluent spender, with high annual fees and annual income requirements.

| |

|

|

|---|

|

To begin, Citi Prestige Credit Card cardholders enjoy free unlimited airport lounge access, with bonus nights at hotels worldwide, free limo transfers as well as golfing privileges. It also offers excellent rates, at 1.3 miles for every S$1 local spend, with a 25,000 bonus miles annually. However, the drawback would be that this card is designed for the more affluent spender, with high annual fees and annual income requirements. |

Wait... But How Do Credit Card Companies Earn Money Themselves?

With so much cashback, rewards, discounts and air miles credit card companies give out annually, have you ever wondered how do they even stay profitable in the first place? And how is it related to you saving money? Here is the secret.

Credit card companies pay for rewards with revenue from two main sources: you, and the merchants who accept their cards. You are likely aware of your contribution. Remember the annual fees and the high interest rates if you default on your credit card debt? Yes, credit card companies earn their revenues through these.

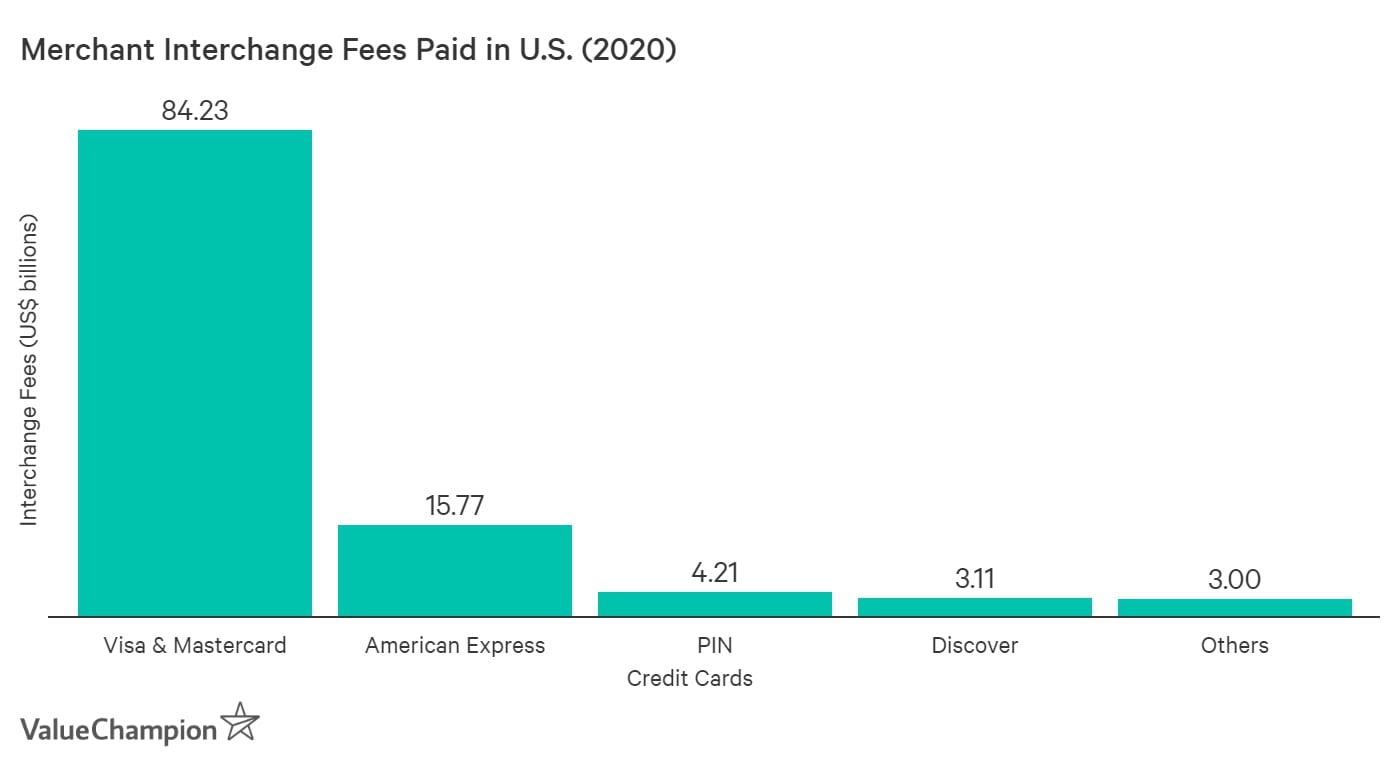

But most consumers don’t know about the fees that retailers pay card issuers behind the scenes. These fees, called interchange fees, are set by credit card processing networks like Visa and MasterCard to cover both the risk and cost of processing credit card payments.

Interchange fees generate billions of dollars in revenue. For instance, American Express collected $6.6 billion in fees from merchants in the second quarter of 2019. In the same quarter, cardholder rewards cost the company just $2.7 billion. Such figures are usually made public through investor relations reports such as this.

Okay, but so what? Unfortunately, merchants usually try to recoup the cost of credit cards by passing down the costs onto consumers like us. What this means is that retailers may raise their prices to compensate for interchange fees, so consumers who pay in cash end up subsidising credit card rewards programs indirectly. A study published in 2010 found that the average cash user effectively pays $149 to card users each year. Meanwhile, the average card buyer receives $1,133 from cash users.

The bottom line is this: if you are not using a credit card for purchases, you are actually losing out by paying for people who do use credit cards. Compounded with the cashbacks and other benefits you might be getting, getting a credit card is indeed crucial in helping you save your finances when adulting.

The Unspoken Dangers of Credit Cards

The word ‘credit’ lends a clue in the nature of credit cards: they are essentially pre-approved loans. In other words, whenever you swipe your card on a payment machine, you are spending on borrowed money. The interest rates on unpaid credit card bills are indeed mind-bogglingly high - most rates are between 25-27% per annum, and the interest is charged on a daily basis. This does not include other miscellaneous fees such as late fees and finance charges, which can add another $100 to the bill.

In comparison, personal loans only have an interest rate between 6-9% per annum.

Repeatedly missing out on your credit card repayments is a good way to ruin your credit score. A bad credit rating spells disaster on your other loans, such as a lower loan amount for mortgage and education loans. In the worst case scenario, you won’t be able to qualify for them at all. Indeed, missing out on credit card repayments could lead to a disastrous snowball effect.

So are credit cards for everyone? If you are earning a stable income, prompt on your bills and want to accumulate savings and benefits as you spend, then go for it! Otherwise, it might be better to hold off until you are in a better financial position to do so.

Curious about other aspects in your financial journey? Check out our other useful guides to learn more about loans, insurance and savings accounts.

Fiona is a full-stack marketer working in the digital sphere for more than six years.

A self-proclaimed foodie and bargain hunter, she wants to bring the best deals and value to the community around the world. When not working on her pet projects, Fiona can be found sipping a coffee while reading a paperbacks or watching mystery thrillers on Netflix and Disney+.