How to Find the Best Motorcycle Insurance Plan

Because there aren't a lot of motorcycle insurers in Singapore, the comparison process is relatively less overwhelming compared to other types of insurance. However, the plans that are available are still distinctive enough that certain options may be better suited to you than others. So what should you look for to make sure you are getting the best motorcycle insurance plan? We break down what you should know to ensure you will purchase the best policy for your needs.

Table of Contents

Which Motorcycle Insurance Plan is Right for You: Comprehensive vs. TPFT vs. Third Party Plans

When you are shopping for a motorcycle insurance plan, you will notice that insurers offer three types of options: Third Party, Third Party, Fire & Theft (TPFT)and Comprehensive plans. Identifying which of these three plans you need will be the first step to narrowing down your options.

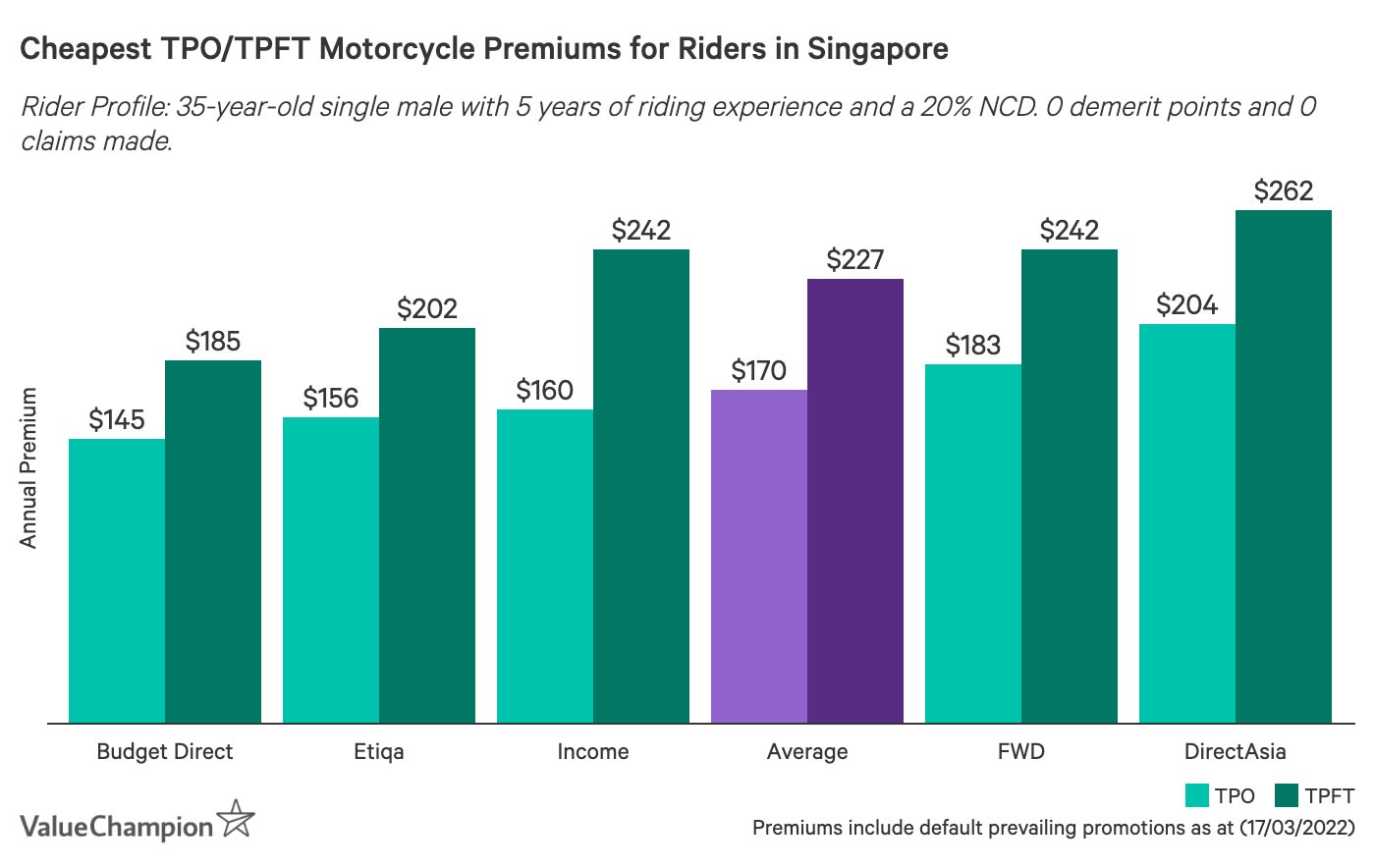

Third Party & Third Party, Fire & Theft Plans

Third Party plans only cover damage done to someone else's motorcycle or any injury or death you caused to a third party. It is the most basic motorcycle insurance plan in Singapore and all riders must have at least third party coverage. A TPFT plan provides third party coverage and also includes damage to your motorcycle caused by fire or theft, making it more expensive than Third Party plans. If you have an old motorcycle a Third Party or TPFT plan will be the two plans you'll be able to choose from. This is because insurers don't offer comprehensive plans to motorcycles that were registered over 8 years ago.

If you decide that a Third Party plan provides enough coverage for you, then you can choose a policy based on cost, as insurers typically offer the same benefits. Furthermore, a Third Party plan can be a better choice compared to a TPFT if your motorcycle has lost most of its value or isn't frequently used. This is because it may not be worth paying higher premiums for damage coverage if the risk of damage is low and you can't justify the motorcycle's value to be worth the extra cost of getting a TPFT plan. If your bike still has considerable value, you can compare TPFT plans based on features in addition to price. Unlike Third Party plans, some TPFT plans offer add-ons such as hospitalisation, personal accident and towing, making it a good option for customers for customers who want more than just 3rd party liability coverage.

Comprehensive Plans

Comprehensive plans are the most expensive out of the three, but they offer the most benefits. If you just got your license or you bought a new motorcycle, a comprehensive plan may be a good fit because it will provide liability, damage and miscellaneous peace of mind coverage such as towing services, damage protection beyond just fire and theft, and roadside assistance. The fully-fledged nature of comprehensive policies ensures that motorcyclists will receive coverage from a variety of scenarios, making it appealing to all types of riders. Lastly, your bank may require you to purchase a comprehensive policy if your motorcycle is under financing.

Choosing the Right Features

Once you know what kind of plan you are looking for, you should figure out which features are most important to you. To do this, you should consider your experience on the road and find plans with benefits that match your concerns. For instance, novice riders may fare best with plans that provide peace of mind benefits like roadside assistance. Those who paid for their motorcycles in full may appreciate a policy with a new-for-old benefit, which will provide a replacement motorcycle in the event it is stolen or totalled. Owners of unique or imported motorcycles may appreciate a plan that allows them to choose their own workshop.

Core Benefits of Motorcycle Insurance

| Benefit | Average Coverage Limit |

|---|---|

| 3rd Party Injury/Death | Unlimited |

| 3rd Party Damage | S$500,000 |

| Theft/Fire Damage | 100% of Market Value |

| Towing | S$50 |

Because motorcycle insurers in Singapore offer a similar set of benefits in their core plans, you will be making decisions based on optional add-ons, such as hospitalisation coverage, personal accident coverage and daily transportation benefits. Typically, the additional cost of these add-ons range from S$30-S$55, but some insurers provide a couple of add-ons for as low as S$3-S$10. While paying extra for coverage may initially seem like a drawback, it can actually work to your benefit. First, it reduces the possibility that you will overpay for a plan due to benefits you won't utilise. Second, it lets you customise your policy, making it easier for you to create a plan that fits within your budget while offering the benefits you care most about.

What to Know About Motorcycle Insurance Excess

Another feature you should consider when choosing your motorcycle insurance plan is the excess. An excess (aka deductible) is what you are responsible for paying for before the insurance coverage kicks in.

Standard Excess

The first type of excess in motorcycle insurance policies is called standard excess. Standard excess applies for loss or damage claims and is typically between S$500-S$750. Unlike car insurance, where you can choose to customise your excess in exchange for paying higher or lower premiums, motorcycle insurers provide a set excess. DirectAsia is the one exception, as it lets you choose from a variety of excesses, making it a good option for those who prefer to pay less out of pocket.

Young/Inexperienced Rider Excess

The second type of excess you'll encounter is the young/inexperienced rider excess. This excess is an addition to the standard excess and is applicable to riders with 2 years of riding experience or who are younger than 27. Motorcycle insurers typically charge S$300 or S$500 for the young/inexperienced rider excess. If you are a rider in your 20's it will be important that you pay attention to this benefit because insurers consider different ages to fall under the "young rider" category. Thus, to avoid paying an additional excess, it may be worthwhile looking for an insurer that classifies you as regular rider rather than a young rider.

Choosing a Plan Based on Price

Your ability to pay for any insurance plan should be an important factor when browsing for the best plan, but you should avoid choosing a plan solely on price. This is because the cheapest plans typically offer the least amount of benefits, and may thus not provide enough coverage for your needs. This can result in you paying out-of-pocket expenses for things that you may have otherwise been covered for (for instance, daily transportation while your motorcycle is being repaired). Instead, you should focus on finding plans with the right coverage first, and then consider which of those plans fit in your budget. You should also remember that your premiums may even decrease as you start to increase your No Claim Discounts (NCDs), so while a plan may initially seem expensive, there is the chance of it becoming more affordable.

What to Keep in Mind as a Motorcyclist

While motorcycles are a popular form of transportation in Singapore, it is not without risks. For instance, according to the Annual Road Traffic report for 2018, motorcyclist and pillion rider fatalities accounted for almost half of all road traffic fatalities. This means that the best motorcycle insurance policy for you will be one that provides coverage for a wide range of situations and will be there for you in the event of an accident. You should also be sure to read the policy wording of all the insurance plans you are comparing to make sure there are no surprise exclusions. If you want to check out our top picks, you can read our guide to the best motorcycle policies currently available in Singapore.

Read More:

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.