How to Pick the Best Critical Illness Insurance Plan

Critical illnesses such as cancers, heart disease and strokes are some most prevalent illnesses in Singapore, with almost 1 in 4 Singaporeans being diagnosed with a critical illness everyday. They can be deadly and expensive to treat. To mitigate against the risk of financial ruin due to a critical illness, there are certain insurance policies that aim to protect you, should you get diagnosed with one. But while this coverage can offer peace of mind—especially to those with genetic predispositions for these illnesses—is it necessary for everyone? Below, we discuss who may need critical illness coverage, and who may be able to do without this type of insurance.

Table of Contents

What is Critical Illness Insurance?

Critical illness insurance is a plan that covers you for 37 major critical illnesses (as defined by the LIA) and their relevant surgeries. It can be purchased separately or as part of your life insurance policy. It offers a lump sum upon diagnosis of a critical illness that can be used for whatever you need, in contrast to a health insurance policy, which only covers hospitalisation stays and medical expenses.

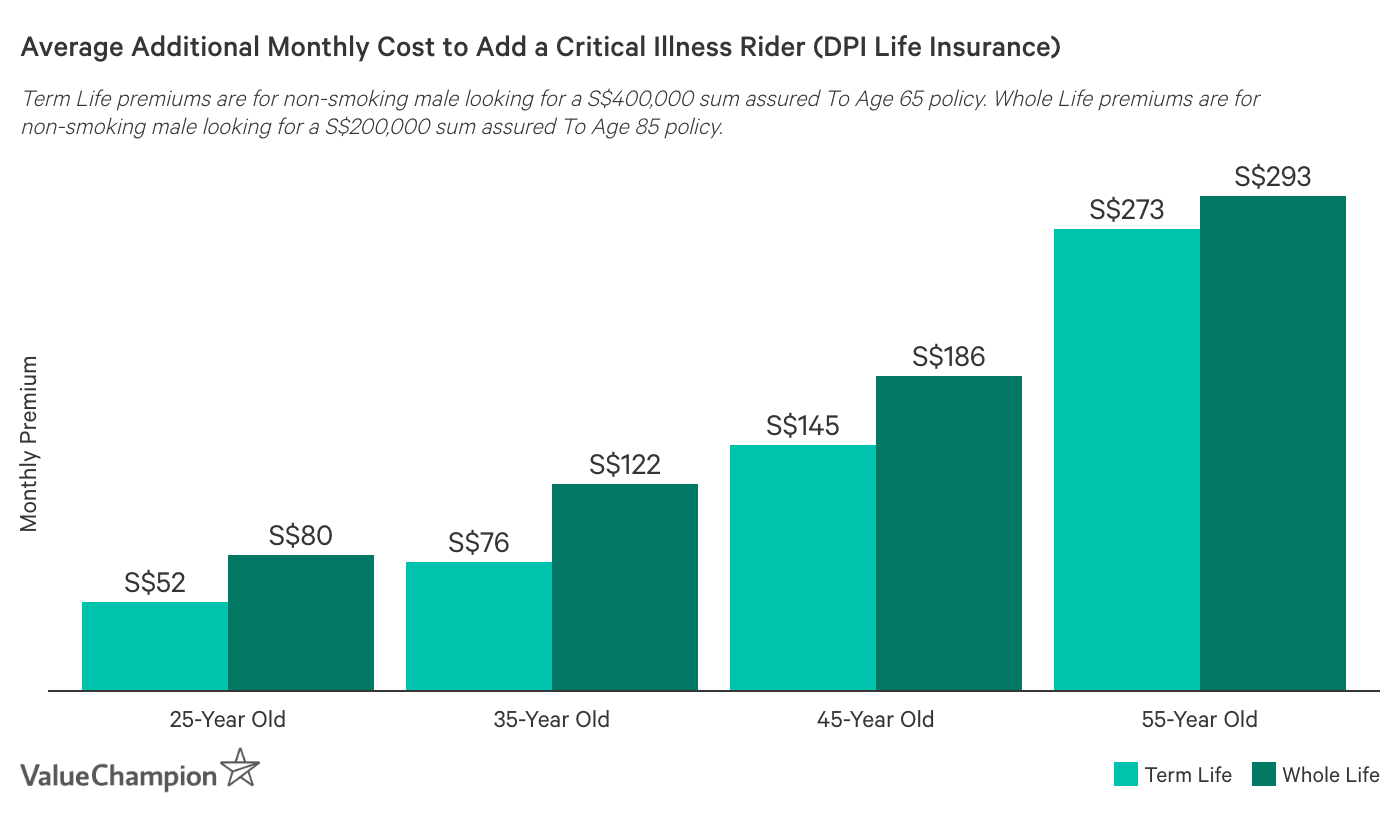

Those who are purchasing Direct Purchase Life Insurance have the option of adding a critical illness rider to their plan. It offers a one lump sum payment upon diagnosis of a covered critical illness. On the other hand, standalone critical illness plans may also provide additional benefits like reconstruction surgery coverage, juvenile disease coverage and early payouts. Some critical illness plans also let make up to 5 claims, which can be a lifesaver when you have a disease that often leads to the development of others. These standalone plans can be bought online, but you should still consult a financial advisor before purchasing one.

Who Should Get It?

Critical illness insurance can be a suitable option to consider if cancer, heart disease, diabetes or other conditions are common in your family. In fact, you should consider a plan as early as possible to avoid getting denied coverage due to a pre-existing condition. For instance, coronary artery disease and high blood cholesterol may be hereditary, meaning you will have a hard time preventing these diseases if your family has them.

Furthermore, if you find out if you are genetically predisposed to contracting a certain illness (e.g. higher risk of breast cancer due to mutations in the BRCA1 or BRCA2 gene), a critical illness plan can help you prepare for something that may be inevitable. However, even if you find yourself to be genetically predisposed to a disease, environmental factors like your lifestyle can play a large role in whether you will inherit the disease. Thus, if you lead a healthy lifestyle and monitor your health, insurers may not always pit the genetic mutation against you by charging very high premiums.

You should also consider critical illness insurance if you are worried that you may not have enough to pay for your your medical treatment and your familial obligations. Considering the average critical illness recovery period is 5 years, you should figure out how much you coverage you'd need to support your family during that time. Additionally, you should take into consideration how much cash you'd need if you were diagnosed with a second critical illness down the line. This is because if your critical illness plan doesn't cover multiple payouts, it may be challenging for you to get a new policy after a history of illness.

How Much Coverage Should You Get?

The LIA recommends a coverage amount of 3.9x your annual income. So for instance, if you earn S$60,000 per year, you should consider a plan with around S$234,000 of critical illness coverage. However, you should get as much protection as necessary to support yourself and any dependents if you have to take time off work. If this means getting more insurance coverage, then you should strongly consider getting more. On the other hand, if you feel like you have enough savings to cover being out of work, you opt for less coverage.

Recommended CI Coverage Based on Income Deciles (Annual Salary, Excluding CPF)

| Income Decile | Avg. Individual Salary | Recommended Coverage |

|---|---|---|

| 1st-10th | S$6,100 | S$24,800 |

| 11th-20th | S$11,800 | S$46,000 |

| 21st-30th | S$16,300 | S$63,700 |

| 31st-40th | S$20,800 | S$81,100 |

| 41st-50th | S$25,800 | S$100,800 |

| 51st-60th | S$31,800 | S$124,200 |

| 61st-70th | S$39,200 | S$152,700 |

| 71st-80th | S$49,700 | S$193,700 |

| 81st-90th | S$67,900 | S$264,700 |

| 91st-100th | S$148,300 | S$578,700 |

| *Figures are rounded to nearest whole number | ||

How to Get the Best CI Plan

If you don't need extra benefits with your CI plan, you can opt for the available add-on with your life insurance policy. Alternatively, other insurers offer multiple CI plans to choose to add to your life insurance plan. They may also let you purchase a CI plan as a standalone policy. So, how do you choose which one is suitable for you in this scenario? First, you can consider your health and family medical history. For instance, you may benefit from a multi-claim policy or just a cancer insurance policy if you believe you are at a risk for cancer. This is because after developing cancer, the risk of getting other cancers increases as do other diseases caused by your cancer treatment (e.g. heart problems after chemotherapy or radiation treatment).

Individuals concerned about getting a gender specific illness can opt for a critical illness plan that specialises in gender-specific critical illnesses. These plans offer coverage for cancers and illnesses that are more prevalent in one gender over another (e.g. cervical cancer vs. prostate cancer). They also offer benefits such as biennial health check-ups, reconstructive surgery coverage and outpatient psychiatric benefits.

Consumers who prioritise prevention can consider an early stage critical illness plan. These plans offer coverage for all stages of critical illness in contrast to the average critical illness plan that only covers late stage illnesses. This can be a good option for cash-strapped individuals because it may be more economical to treat a critical illness in its initial stages than to wait until it becomes harder to treat.

Important Things to Look Out For

There are several critical things to know about critical illness coverage regarding certain exclusions and how certain illnesses are covered. First, if you are diagnosed with angioplasty or require invasive treatment for a coronary artery, you will only receive 10% of the sum assured (or a maximum sum of S$25,000). You will still be able to claim for other critical illness, but the total amount you'll be insured for will be your original amount minus the amount taken out for the angioplasty. Furthermore, you will find that under certain conditions, your critical illness won't be covered at all. For instance, comas and end-stage liver failure are not covered if they were caused by alcohol or drug abuse. Additionally, only 30 of the 37 critical illnesses are covered if you are purchasing the DPI critical illness add-on.

| Critical Illness | Example of Common Exclusions |

|---|---|

| Major Cancer | Premalignant/non-invasive tumours, tumors in presence of HIV |

| Heart Attack | Angina, a rise in cardiac biomarkers |

| Stroke with Permanent Neurological Deficit | Brain damage due to accident/injury/infection/inflammation, transient ischaemic attack |

| End-Stage Liver Failure | Liver disease caused by alcohol or drug abuse |

| Coma | Resulting directly from alcohol or drug use |

| Irreversible Loss of Speech | Caused by psychiatric conditions |

| Open Chest Surgery to Aorta | minimally invasive surgeries |

| Alzheimer's/Severe Dementia | Caused by neurosis/psychiatric illness, alcohol-related damage |

| Severe Encephalitis | Caused by HIV |

| Paralysis (Irreversible Loss of Use of Limbs) | Self-Inflicted Injury |

| Loss of Independent Existence | Caused by neurosis or psychiatric illnesses |

Second, if you are purchasing a critical illness rider for a Direct Purchase Insurance life insurance plan, you should note that any claim for a critical illness will get taken out from your death sum insured. For instance, let's suppose you have S$200,000 of death coverage for you base life insurance policy and you purchase S$50,000 of critical illness coverage. If you were to get a critical illness and claim that S$50,000, your total death coverage would reduce by that amount. If you were to get a critical illness rider that is the same as the sum assured for your life insurance policy, both policies would cease after the payout.

Last, there are also a few illnesses and surgeries that are only covered 90 days after you purchase your policy. These are heart attacks, cancers, coronary artery bypass surgery and angioplasty. This highlights the importance of getting critical illness coverage well before you are likely to get sick.

Read More:

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.