How to Prevent Bankruptcy Amid The Covid-19 Pandemic

With the world economy running into a state of uncertainty amid the COVID-19 pandemic, many people are realizing the need for maintaining good financial health and managing their funds more effectively. This also includes the subject of bankruptcy and insolvency as the number of bankruptcy applications has reached a 15-year high in March this year. If not for temporary measures that were implemented in April to raise the thresholds for bankruptcy, the number of bankruptcy applications may have continued to skyrocket.

Downside of Filing for Bankruptcy

How does one become bankrupt? According to the Bankruptcy and Insolvency Act of Singapore, creditors may file a bankruptcy application against a debtor or a debtor can file a voluntary application to start the bankruptcy proceedings. Either way, bankruptcy is not an easy way to get out of debt and should not be taken lightly. For one, there are heavy financial consequences because the bankrupt individual's assets will be seized and divided (with the exception of some protected assets) to repay the creditors. Furthermore, bankrupt individuals will have to continue to repay their debts, with a portion of their monthly income and all expenses incurred on their remaining income to be documented and justified during routine checks from a court-appointed Official Assignee. These checks ensure that the individuals are committed to repaying their debts and not spending their incomes on luxuries.

Aside from financial difficulties, bankruptcy can impact one's employment opportunities because bankruptcy details are published in Singapore’s bankruptcy register which can be accessed by the public and employers. There are also restrictions in terms of managing a business or acting as a director of a company after declaring bankruptcy.

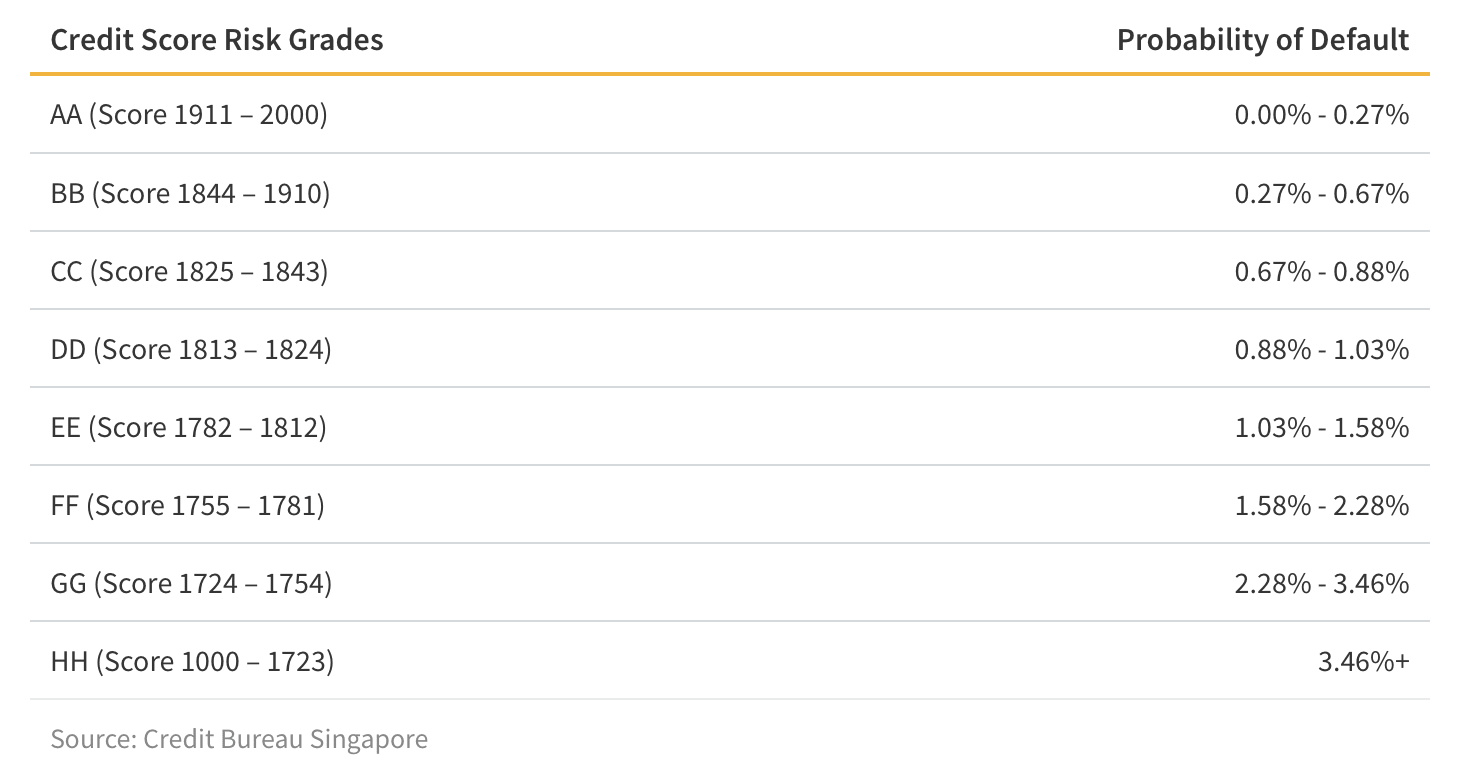

On the personal front, bankrupt individuals are seldom granted permission to travel unless they have displayed satisfactory conduct during bankruptcy and are placed in the Green Zone. They are also black marked on their credit ratings which can sometimes take years to rebuild.

Temporary Amendments to Bankruptcy & Insolvency Laws Due to Covid-19

To aid the growing number of debtors who are affected by the recent pandemic, the Ministry of Law has put in place additional relief measures under the Covid-19 (Temporary Measures) Actto help individuals and businesses cope with potential bankruptcy in Singapore. Such a move increased the threshold for bankruptcy, hence reducing the number of applicants who will qualify for bankruptcy proceedings. Here are key changes to the Bankruptcy & Insolvency Laws for both creditors and debtors:

Increased Monetary Threshold

The inclusion of the recent Act has increased the monetary threshold for bankruptcy from S$15,000 to S$60,000 for individuals, and S$10,000 to S$100,000 for businesses. The significant increase in the minimum debt amounts provides a safety net for debtors who are faced with financial difficulties because of the Covid-19 pandemic. This measure enables business owners to continue operating without having to shut their business down due to insolvency.

Prolonged Statutory Period

Taking into consideration that the nationwide lockdown has caused inconvenience and delays for many debtors, the Act also attempts to prolong debtors’ response period to creditors' demands. The new measure provides temporary relief to debtors from creditors’ legal action for up to 6 months from April 20. This implies that any statutory demand served on or after this date, debtors can take up to 6 months, instead of 21 days, to fulfil creditors’ demands.

Alternatives to Avoid Bankruptcy

Bankruptcy is no laughing matter, and everyone should exhaust all possible avenues to resolve credit issues before surrendering to the bankruptcy option. Fortunately, there are some methods for recourse that are recommended by the Ministry of Law:

Covid-19 Temporary Relief Measures

For individuals and business owners who are affected by the Covid-19 pandemic, they can seek protection from the Covid-19 (Temporary Measures) Act to guard against bankruptcy proceedings due to their inability to fulfil contractual obligations.

The Act protects those who entered into contracts for rentals in the industrial and commercial sectors, construction, supply and secured loan facilities granted by financial institutions to small and medium-sized enterprises. Debtors who require protection from creditors’ legal proceedings can apply for a notification for relief from the Ministry of Law and to the creditors, guarantors and issuers of the performance bond before they will receive relief under the Act. Appointed assessors by the Ministry will then resolve disputes. Parties involved will not be allowed to be represented by lawyers, and there will be no costs orders.

Voluntary Arrangement (VA)

A voluntary arrangement arrangement allows debtors to present creditors with a formal repayment plan to convince them to hold back on bankruptcy proceedings. Before entering into a VA agreement, debtors must first apply for an interim order to stop further bankruptcy proceedings against them. This application must be accompanied by a proposal containing the debtor’s assets, liabilities and repayment plan.

Every VA must be supervised by a nominee such as a registered public accountant or an advocate and solicitor. The appointed supervisor will assist in the implementation of the agreements and ensure that the repayment plan is fulfilled accordingly. Both the nominee and creditor may proceed to file a bankruptcy application against the debtor if the latter fails to comply with the VA terms.

Debt Repayment Scheme (DRS)

The Debt Repayment Scheme (DRS) allows individual debtors to repay their debts while retaining possession of their property and continuity of their business activities without becoming bankrupt. It also prevents creditors from proceeding with any legal action against the debtor unless permitted by the court.

Since April, the Covid-19 (Temporary Measures) Act has amended the monetary threshold for DRS from S$100,000 to S$250,000 to assist more individuals who may need this scheme because of the sudden economic downturn. This suggests that such a scheme is now available to those with debts of up to S$250,000. To apply for the DRS, debtors are required to file a bankruptcy application with the Singapore court. If bankruptcy proceedings have been filed by creditors, the court will refer the debtors to the Insolvency Office to assess their eligibility for such schemes.

Be Financial Savvy

The first step to prevent bankruptcy is to be financially savvy. There is also ample help available across many professional and government channels, so we encourage consumers to make sure to leverage these supports before surrendering to your creditors’ demand. For those that are considering taking on debt during this uncertain time, we strongly recommend that you research various loan options, and compare rates and features before applying.