Ward Classes, Pro-Rations and IP Plans: Here’s What You Need To Know

The healthcare system in Singapore is praised for being one of the most efficient in the world. The way we structure our mixed payment system is second to none. According to the Ministry of Health (MOH) themselves, there are up to 18 different subsidy and financial assistance schemes alone if you are a Singapore Citizen, with MediSave, Medishield Life, CareShield Life ElderShield, CHAS and MediFund being the six most prominent government-assisted programmes for healthcare expenditure.

Government assistance can only do so much when it comes to covering the most basic form of healthcare. In fact, it is encouraged to take up private health insurance in order to get access to better healthcare treatment and accommodation in the hospital.

The Differences Between Ward Tiers

There are different hospitalisation wards in Singapore. In public or government-funded hospitals, wards are split into four classes: C Wards, B1 Wards, B2 Wards, and A Wards. Insurers will also include private hospital wards in their high-tier IP plans.

| Ward Type | Cost per Day | No. Of Beds | Possible Amenities |

|---|---|---|---|

| C | S$34-S$43 | 7-9 | N/A |

| B2 | S$76-S$87 | 5-6 | Semi-automated electric bed |

| B1 | S$230-S$279 | 4 | Bathroom, TV, Phone, Electric Bed, Choice of Meals, Choice of specialist |

| A | S$316-S$544 | 1-2 | Toiletries, TV, Phone, Sleeper Unit, Choice of Meals, Choice of Specialist, Bathroom |

C ward covers the basic necessities, and a C ward is shared with 12 patients. The ward is heavily subsidised, with a 65-80% subsidy level.

A B2 ward is a tier higher than a C ward, with one B2 ward being shared with six patients and each patient getting a semi-automated electric bed. B1 Wards have four patients sharing the ward with more amenities like a television, air conditioning, and bathroom. B wards are moderately subsidised, with the subsidy level for a B2 ward being 50-65% and a B1 ward being 20%

A wards are private wards that provide the most amenities in the room, like air-conditioning and a private bathroom, with no government subsidies.

Subsidies are distributed according to the patient's income level via means-testing, meaning that despite your choice to stay in a C/B2 ward, the higher your monthly income, the less subsidy you will receive to pay for your C/B2 ward expenses. The point of means testing is to ensure that the financially needy people in Singapore can afford healthcare and provide equity of healthcare resources to the lower-income groups.

Here is a list of government hospitals listed from the government website:

| Public Hospital | Phone Number | Location |

|---|---|---|

| Alexandra Hospital | 6472 2000 | Queenstown |

| Changi General Hospital | 6850 3333 | Tampines |

| Khoo Teck Puat Hospital | 6555 8828 | Yishun |

| KK Women's and Children's Hospital | 6294 4050 | Kallang |

| National University Hospital | 6772 2002 | Kent Ridge |

| Ng Teng Fong General Hospital | 6716 2222 | Jurong East |

| Sengkang General | 6930 6000 | Sengkang |

| Singapore General Hospital | 6321 4377 | Bukit Merah |

| Tan Tock Seng Hospital | 6227 7266 | Novena |

Private hospital wards do not receive any government subsidies at all. Here are the list of private hospitals:

| Private Hospital | Phone Number | Location |

|---|---|---|

| Concord International Hospital | 6933 3722 | Bukit Timah |

| Farrer Park Hospital | 6363 1818 | Kallang |

| Gleneagles Hospital | 6473 7222 | Tanglin |

| Mount Elizabeth Hospital | 6737 2666 | Orchard |

| Mount Elizabeth Novena Hospital | 6898 6898 | Novena |

| Parkway East Hospital | 6377 3737 | Telok Kurau |

| Raffles Hospital | 6311 1111 | Rochor |

| Thomson Medical Centre | 6250 2222 | Novena |

What Does a MediShield Life Cover?

If you are a Singaporean or a Permanent Resident (PR), you are automatically covered with MediShield Life, which is a government insurance scheme covering the most basic forms of healthcare that can be paid by MediSave. You can read the details of MediShield Life here.

MediShield Life covers hospitalisation expenses for C and B2 wards. You are entitled to MediShield Life payouts that are calculated based on the subsidised bills payable at Class B2/C wards. For outpatient treatment and day surgery, the payout is also pegged to the applicable subsidised rates.

MediShield Life, however, has an annual deductible of S$1,500 for patients under 80 and S$2,000 for patients above 80 if they want to stay in a Class C ward and use MediShield, as well as S$2,000 for patients under 80 and S$3,000 for patients above 80 for stay in a Class B2 ward and above. You will also be subjected to co-insurance after paying for deductibles, which typically varies between 3% and 10% of the total bill amount and falls as the value of the bill rises.

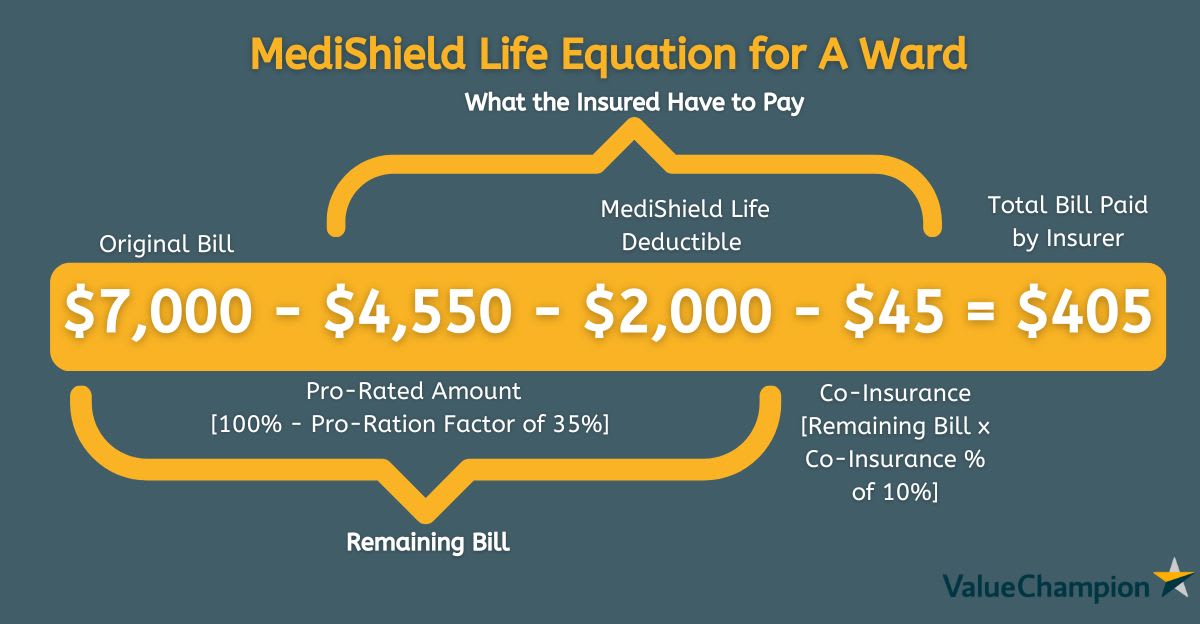

MediShield Life Pro-Rated for A Wards

| Hospital Bill | $7,000 |

|---|---|

| Deductible ($2,000) | $2,000 |

| Co-Insurance (10%) | $45 |

| Pro-Ration (100% - 35%) | ($7,000 - $2,450 = $4,550) |

| Total Claims | $405 |

| Total Bill Paid By Insured | $6,595 |

However, if you stay in a Class A/B/B2+ ward in a public or private hospital, the payout will be reduced on a pro-rated basis. For example, if your bill is $7,000, since the pro-ration factor for A wards under MediShield Life is 35%, you would have to pay 65% of the bill. You have to pay a deductible of $2,000 (assuming that you are 80 years old or below). You will then need to pay another 10% co-insurance. The 90% of the remaining amount will be covered by MediShield Life.

If you do not have an IP covering an A ward, and you use MediShield Life, you need to pay a total of the Balance of the pro-rated amount ($7,000 - $2,450) + Deductible ($2,000) + co-insurance amount ($45) = $6,595, MediShield Life will only cover $405.

What Does Integrated Shield Plan Cover?

An integrated shield plan is an add-on to the MediShield Life by private insurers providing coverage for B1, A wards, and private hospitals. As of 1 May 2016, all IP insurers must sell the Standard IP regulated by MOH. The benefits of Standard IP are identical across all IP insurers and have claim limits sized to fully cover nine out of ten Class B1 bills.

Prudential - For A Ward Hospitals

- Co-Insurance

- 10%

- Hospital Type

- Public Ward A and below

- Eligibility Requirement

- Singapore Citizens, Permanent Residents, Foreigners

- Last Entry Age

- 75 (Age Next Birthday)

| Benefits | Benefit Limit | Ward A Avg. |

|---|---|---|

| Annual Limit | S$600,000 | S$528,571 |

| Hospitalisation & Surgical Benefits | As Charged | As Charged |

| Pre-Hospitalisation (Days) | 180 | 120 |

| Post-Hospitalisation (Days) | 365 | 180 |

| Outpatient Cancer Treatment | As Charged | As Charged |

| Pregnancy & Childbirth Complications | As Charged | As Charged |

| Total Psychiatric Treatment (including Pre- and Post- hospitalisation expenses incurred) | S$7,000 | S$8,286 |

The best hospitalisation insurance for the average value-seeking consumer is Prudential's PRUShield Plus. First, its premiums are around 23-47% lower than average for all ages, despite a higher than average annual limit of S$600,000 compared to other Ward A plans in the market. Its 365 post-hospitalisation coverage is also one of the longest on the market. Additionally, you can purchase Prudential's PRUExtra Plus CoPay Rider, which will cover 95% of your deductible, half your co-insurance and provide miscellaneous coverage for things like parental ward accommodation, ambulance services and emergency outpatient treatment. Combined with the Plus plan, the total cost comes out around 27-39% below average for base plan and Rider packages.

In terms of its specific coverage benefits, cancer treatment, dialysis, pregnancy complications, surgery, and room and board expenses are covered on an "as charged" basis, meaning they will be paid in the full amount (subject to limits, deductibles and co-insurance). On top of this, you will also receive a final expense provision benefit of S$3,000 and be covered for hyperbaric oxygen therapy (for treatment of carbon monoxide poisoning, severe anemia and other blood-oxygen related maladies). However, Prudential's PRUShield Plus does lack comprehensive coverage for severe psychological disorders and critical illnesses, which are better covered by Great Eastern or Aviva.

- Co-Insurance

- 10%

- Hospital Type

- Public Ward A and below

- Eligibility Requirement

- Singapore Citizens, Permanent Residents, Foreigners

- Last Entry Age

- 75 (Age Next Birthday)

| Benefits | Benefit Limit | Ward A Avg. |

|---|---|---|

| Annual Limit | S$600,000 | S$528,571 |

| Hospitalisation & Surgical Benefits | As Charged | As Charged |

| Pre-Hospitalisation (Days) | 180 | 120 |

| Post-Hospitalisation (Days) | 365 | 180 |

| Outpatient Cancer Treatment | As Charged | As Charged |

| Pregnancy & Childbirth Complications | As Charged | As Charged |

| Total Psychiatric Treatment (including Pre- and Post- hospitalisation expenses incurred) | S$7,000 | S$8,286 |

The best hospitalisation insurance for the average value-seeking consumer is Prudential's PRUShield Plus. First, its premiums are around 23-47% lower than average for all ages, despite a higher than average annual limit of S$600,000 compared to other Ward A plans in the market. Its 365 post-hospitalisation coverage is also one of the longest on the market. Additionally, you can purchase Prudential's PRUExtra Plus CoPay Rider, which will cover 95% of your deductible, half your co-insurance and provide miscellaneous coverage for things like parental ward accommodation, ambulance services and emergency outpatient treatment. Combined with the Plus plan, the total cost comes out around 27-39% below average for base plan and Rider packages.

In terms of its specific coverage benefits, cancer treatment, dialysis, pregnancy complications, surgery, and room and board expenses are covered on an "as charged" basis, meaning they will be paid in the full amount (subject to limits, deductibles and co-insurance). On top of this, you will also receive a final expense provision benefit of S$3,000 and be covered for hyperbaric oxygen therapy (for treatment of carbon monoxide poisoning, severe anemia and other blood-oxygen related maladies). However, Prudential's PRUShield Plus does lack comprehensive coverage for severe psychological disorders and critical illnesses, which are better covered by Great Eastern or Aviva.

There are tiers where you can upgrade your IP from a standard shield plan covering B1 wards without pro-ration, to an A class IP covering A wards, and the highest tier covering private hospitals. You are still subjected to deductibles and co-insurance.

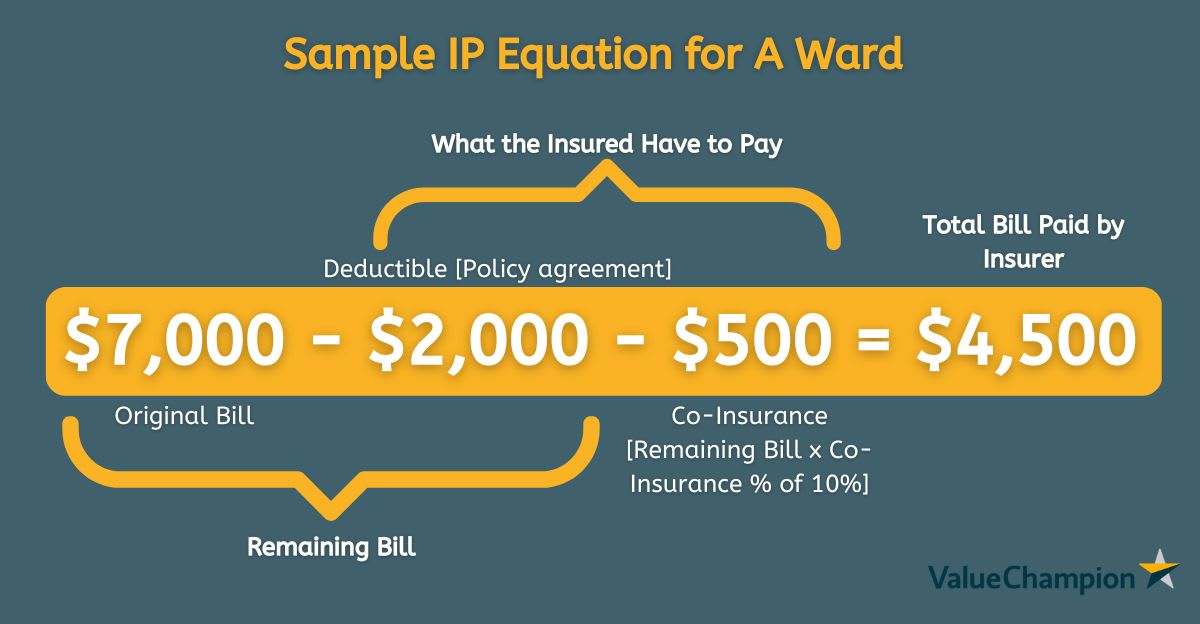

IP (P) Ward A Hospitalisation Bill

| Hospital Bill | $7,000 |

|---|---|

| Deductible ($2,000) | $2,000 |

| Co-Insurance (10%) | $500 |

| Total Bill Paid By Insured | $2,500 |

| Total Claims | $4,500 |

From the example above, assuming that you have a base shield plan from insurer P (without riders that cover deductibles or co-insurance) that covers an A ward for a government hospital or higher, assuming that the deductible amount is still $2,000 (Some plans' annual deductible can be as low as $1,000) and the co-insurance is still 10% (Some plans’ co-insurance can go as low as 5%).

The total bill paid by you will only be Deductible + Co-Insurnace = $2,500, and your IP provider will pay the remaining $4,500, which is ten times more than MediShield Life for the same treatment, making your expenses lower as a result. You can even pay as low as $1,250 if you select the right plan or even lower as you get a rider.

Great Eastern SupremeHealth P - For Private Hospitals

- Co-Insurance

- 10%

- Hospital Type

- Private

- Eligibility Requirement

- Singapore Citizens, Permanent Residents, Foreigners

- Last Entry Age

- 75 (Age Next Birthday)

| Benefits | Benefit Limit | Private Hospital Avg. |

|---|---|---|

| Annual Limit | S$1,500,000 | S$1,050,000 |

| Hospitalisation & Surgical Benefits | As Charged | As Charged |

| Pre-Hospitalisation (Days) | 120 | 150 |

| Post-Hospitalisation (Days) | 180 | 173 |

| Outpatient Cancer Treatment | As Charged | As Charged |

| Pregnancy & Childbirth Complications | As Charged | As Charged |

| Total Psychiatric Treatment | S$25,000 | S$10,583 |

If you are looking to receive maximum private hospital coverage regardless of cost, you can consider Great Eastern's GREAT SupremeHealth P Plus plan along with its Great TotalCare Classic P Rider. The P Plus plan offers the highest annual limit for private hospitals of S$1,500,000, and provides full medical bill coverage for cancer treatment, dialysis, pre and post-hospitalisation treatment. You will also receive the highest psychiatric, speech and occupational therapy benefits currently offered, as well as a combined S$20,000 of coverage for congenital abnormalities for your child. This is all for a cost that is 20-40% cheaper compared to other Private Hospital plans.

To top off your coverage to the maximum, you can purchase the TotalCare Classic P Rider to reduce your deductible and coinsurance responsibility to 5% of your bill (or deductible if its higher). You will also receive S$250 of ambulance, S$80 per day of parental accommodation coverage (for parents with children in the hospital) and S$2,000 of accidental outpatient treatment. Lastly, Great Eastern can save you thousands of dollars if you have their A Plus plan and choose to get care at a Private hospital. This is because its pro-ration factor for getting care above your ward level is 70% instead of the 50% implemented by other insurers (Great Eastern will pay 70% of the incurred cost rather than only 50% if you choose to get care at a ward above your level).

- Co-Insurance

- 10%

- Hospital Type

- Private

- Eligibility Requirement

- Singapore Citizens, Permanent Residents, Foreigners

- Last Entry Age

- 75 (Age Next Birthday)

| Benefits | Benefit Limit | Private Hospital Avg. |

|---|---|---|

| Annual Limit | S$1,500,000 | S$1,050,000 |

| Hospitalisation & Surgical Benefits | As Charged | As Charged |

| Pre-Hospitalisation (Days) | 120 | 150 |

| Post-Hospitalisation (Days) | 180 | 173 |

| Outpatient Cancer Treatment | As Charged | As Charged |

| Pregnancy & Childbirth Complications | As Charged | As Charged |

| Total Psychiatric Treatment | S$25,000 | S$10,583 |

If you are looking to receive maximum private hospital coverage regardless of cost, you can consider Great Eastern's GREAT SupremeHealth P Plus plan along with its Great TotalCare Classic P Rider. The P Plus plan offers the highest annual limit for private hospitals of S$1,500,000, and provides full medical bill coverage for cancer treatment, dialysis, pre and post-hospitalisation treatment. You will also receive the highest psychiatric, speech and occupational therapy benefits currently offered, as well as a combined S$20,000 of coverage for congenital abnormalities for your child. This is all for a cost that is 20-40% cheaper compared to other Private Hospital plans.

To top off your coverage to the maximum, you can purchase the TotalCare Classic P Rider to reduce your deductible and coinsurance responsibility to 5% of your bill (or deductible if its higher). You will also receive S$250 of ambulance, S$80 per day of parental accommodation coverage (for parents with children in the hospital) and S$2,000 of accidental outpatient treatment. Lastly, Great Eastern can save you thousands of dollars if you have their A Plus plan and choose to get care at a Private hospital. This is because its pro-ration factor for getting care above your ward level is 70% instead of the 50% implemented by other insurers (Great Eastern will pay 70% of the incurred cost rather than only 50% if you choose to get care at a ward above your level).

Conclusion

MediShield provides the bare minimum in terms of hospitalisation coverage; despite insuring every Singaporean and PR regardless of pre-existing conditions for C and B2 class wards, there are limitations, with it mainly being that there is a pro-ration factor for B1 wards and above.

We have added a comparison table for MediShield LIfe vs the median benefits for IP by private insurers.

Benefits of MediShield LIfe vs IP Plans Median

| Premiums & Coverage | MediShield Life | B1 Standard Ward Median | A Ward Median | Private Hospital Median |

|---|---|---|---|---|

| 25-Year-Old Premiums | S$250 | S$49 | S$90 | S$218 |

| 45-Year-Old Premiums | S$525 | S$103 | S$229 | S$638 |

| 65-Year-Old Premiums | S$1,020 | S$254 | S$664 | S$1,592 |

| Value (Limit/S$ Premium) | N/A | $1,494 | $2,421 | $2,379 |

| Annual Limit | S$150,000 | S$150,000 | S$600,000 | S$1,000,000 |

| Inpatient Psychiatric | S$160/day (60 days) | S$17,500 | S$6,000 | S$6,000 |

| Surgery Benefits | S$240 - S$2,600 | As Charged | ||

| Daily Ward (Non-ICU) | $800/day | As Charged | ||

| Pre-Hospitalisation Benefits | N/A | 120 | 150 | |

| Post-Hospitalisation Benefits | N/A | 180 | 173 | |

The benefit of IP Plans is that they provide higher coverage for better hospital wards and hospital treatments. You can check this page for a detailed comparison between different IPs and which IP suits you depending on your condition.

Read Also

Boon Hun spent over five years in the content marketing space as the managing editor of Goody Feed creating interesting and relevant content for the social media generation. In 2022, he moved to the FinTech space while remaining true to his roots, intending to bring financial literacy to more people in Singapore. When not doing his work, he can be found watching people build homes on YouTube.