POSB Everyday vs. OCBC 365 Credit Card Comparison 2024

POSB Everyday Card and OCBC 365 Card are amongst the most popular options for consumers seeking easy cashback on their daily essentials. While both competitive, these cards are quite different, however. We've closely analysed the comparative strengths and weaknesses between these two cards to help you to determine which is better suited to your lifestyle.

- Details of rebate system & structure

- General & boosted cashback rates

- Minimum spend requirements & monthly rewards caps

- Maximum potential annual earnings

- Travel insurance offerings

- Current petrol promotions & savings

- SimplyGo & mobile pay compatibility

- Extra rebate programmes & card-specific privileges

- Minimum age & minimum income requirements

- Annual fees, spend-based waivers & sign-on bonuses

- Foreign transaction fees

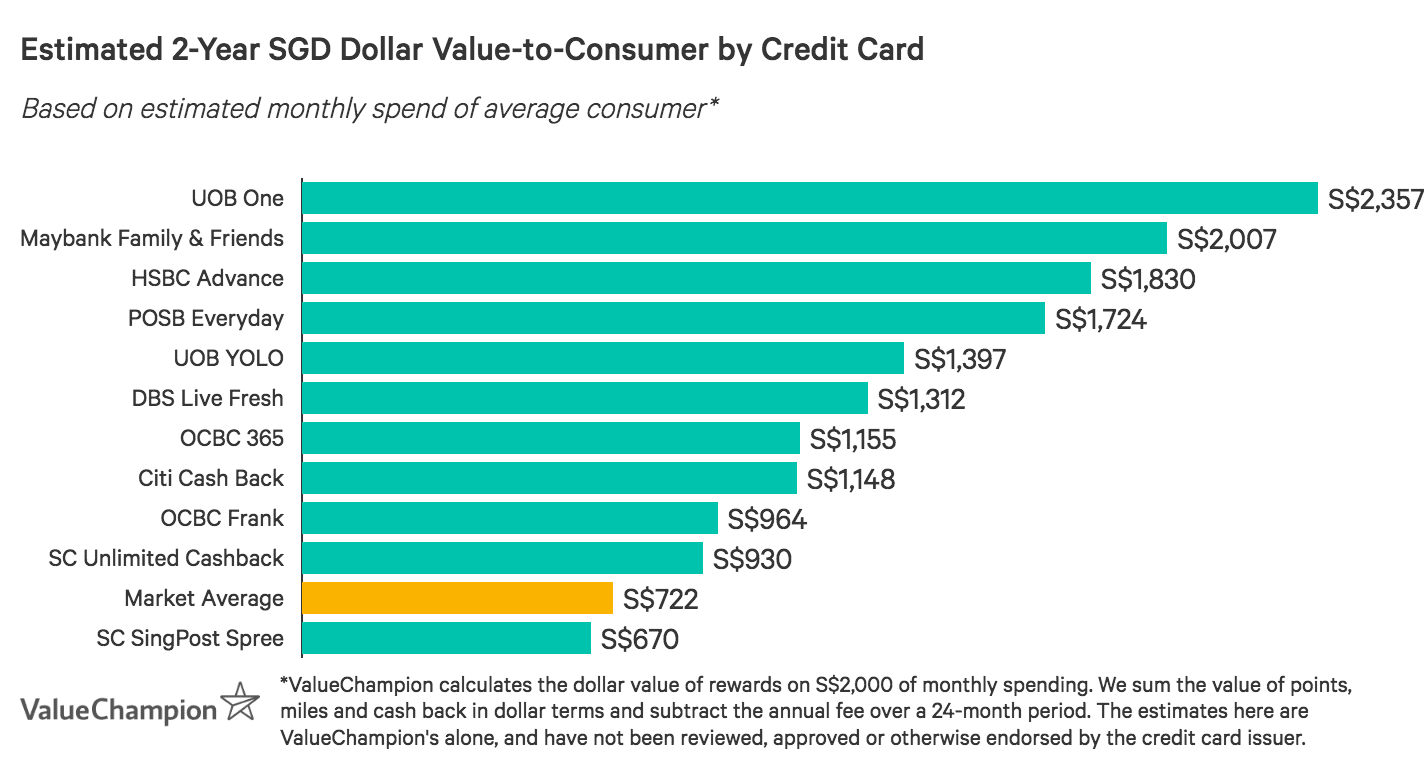

Comparison of Competitive Rebate Cards in Singapore by Dollar Value

Based on an average monthly spend of S$2,000, we analysed some of the most competitive rebate cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Comparison of Competitive Rebate Cards in Singapore by Dollar Value

Based on an average monthly spend of S$2,000, we analysed some of the most competitive rebate cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Overview: POSB Everyday Card vs. OCBC 365 Card

POSB Everyday Card and OCBC 365 Card are perhaps the two best-known cards for daily expenses in Singapore. Each of these options, however, is meaningfully different. The first frequently offers higher promotional rates, but comes with a few rebate complications and merchant restrictions; the latter rewards similar spending and offers a fee-waiver, but tends to provide fewer merchant-exclusive deals. We've provided a detailed breakdown of how these two cards actually compare, to help you decide which might be the better option for you.

Summary Comparison Table: POSB Everyday vs. OCBC 365

| Category | Feature | POSB Everyday Card | OCBC 365 Card |

|---|---|---|---|

| Rates | Min. Spend Req. | Varies | S$800/mo |

| Rebate Boosts |

|

| |

| Earnings Cap |

|

| |

| Perks | Petrol Savings | Up to 20.1% + 2% fuel savings at SPC | Up to 22.1% savings at Caltex, 20.2% at Esso, 26.8% at Sinopec and 5% cashback at all other petrol stations |

| Compatibility | SimplyGo & Mobile Pay Compatible | SimplyGo & Mobile Pay Compatible | |

| Card Privileges | POSB Exclusive Merchant Deals | Visa Concierge & Luxury Hotels Privileges | |

| Fees | Annual Fee | S$192.60 | S$194.40 |

| Waiver Option | Waived for 1 year | Waived for 2 years with min spend of S$10,000/year |

Rewards Rates: POSB Everyday Card vs. OCBC 365 Card

Both POSB Everyday Card and OCBC 365 Card are worth considering if you're seeking rewards on daily essentials. While both rewarding similar areas of spend, however, each of these options vary in ease-of-use.

POSB Everyday Card stands out by offering competitive rebate rates of up to 10% rebate on online food delivery, catering and more. These high rates are described as promotional on the bank's site, but we've seen them be renewed consistently, so it's safe to view them as long-term benefits. The card's truly permanent rebates typically span 3% to 5% and cover areas such as groceries, online shopping, transportation and utilities.

While attractive, these rates weren't that simple to navigate until recently. To unlock POSB Everyday Card's elevated rates, you must spend at least S$800 per month. This is a welcome change from the card's old system, which calculated a unique Personalised Spend Goal for each cardholder that they would then have to meet.

Additionally, because promotional rates change, POSB Everyday cardholders may have difficulty balancing their spending to truly optimise their rewards. Finally, some rewards are merchant restricted. This may require consumers to pay closer attention to where they're shopping and perhaps even to alter their habits.

Comparison Table: Cashback Rewards

| Feature | POSB Everyday Card | OCBC 365 Card |

|---|---|---|

| Rebate Structure | Monthly System | Monthly System |

| Rate Structure | Category Boosts | Category Boosts |

| Base Rate | 0.30% | 0.30% |

| Min. Spend Req. | S$800 | S$800 |

| Boosts |

|

|

| Mo. Rewards Cap | S$30 | S$80 |

| Max Annual Earnings | S$360 | S$960 |

OCBC 365 Card, on the other hand, is fairly easy to use. While there's a S$800 minimum spend requirement, this aligns with market competitors' and is reasonably achievable. Rewarded categories are fairly static and there are no merchant restrictions to track or worry about. Finally, cardholders can fairly easily max out the S$80/month rewards cap with as little as S$1,333 spend. Ultimately, OCBC 365 Card is both competitive and predictable–and therefore, a lower-maintenance pick for most consumers.

Perks & Privileges: POSB Everyday Card vs. OCBC 365 Card

POSB Everyday Card and OCBC 365 vary significantly in terms of perks. The first stands out for its extensive POSB Exclusive Merchant Deals. Given that the card already has several merchant-restricted categories, this special perk ties into the rewards structure almost seamlessly. Consumers have access to savings in 3 different categories, for the most part: utilities (extra rebates on power bills upon sign-up), shopping (fashion and retail promotions with brands like Zalora), and health (anything from check-up discounts to deals on supplements). These savings change every month or so, so it's important to check for expiration dates.

Comparison Table: Card Perks & Privileges

| Feature | POSB Everyday Card | OCBC 365 Card |

|---|---|---|

| Travel Insurance | N/A | S$200k Personal Accident; S$500 Medical; Travel Inconvenience |

| Petrol Savings | Up to 20.1% + 2% fuel savings at SPC | Up to 22.1% savings at Caltex, 20.2% at Esso, 26.8% at Sinopec and 5% cashback at all other petrol stations |

| Transit Perks | SimplyGo Compatible | SimplyGo Compatible |

| Mobile Pay | Google Pay, Apple Pay, Samsung Pay & more | Google Pay, Apple Pay, Samsung Pay, Fit Bit, Garmin & more |

| Card Privileges | POSB Exclusive Merchant Deals | Visa Concierge Services, Visa Luxury Hotels Privileges |

OCBC 365 Card's perks extend beyond deals and discounts. In fact, cardholders receive free travel insurance and privileges like dining credits, complimentary WiFi and room upgrades via the Visa Luxury Hotels programme. These benefits are a great fit for everyday consumers who occasionally travel.

Fees, Promos & Requirements: POSB Everyday vs. OCBC 365 Card

Consumers who want a low-maintenance card may already have come to the conclusion that OCBC 365 Card is a better fit. This is also true when considering fees and requirements. While POSB Everyday Card has a S$192.6 fee, waived just 1 year, OCBC 365 Card's S$192.6 fee is waived for 2 full years and then with just S$10k annual spend. This averages out to about S$833/month, which is roughly equal to the minimum spend requirement to even unlock its upper rates. As a result, someone who is taking full advantage of OCBC 365 Card also won't need to worry about paying its annual fee–perfect for consumers looking for an easy and affordable cashback option.

Comparison Table: Requirements, Promos & Fees

| Feature | POSB Everyday Card | OCBC 365 Card |

|---|---|---|

| Minimum Age | 21 yo | 21 yo |

| Minimum Income |

|

|

| Annual Fee | S$192.60 | S$194.40 |

| Waiver Option | Waived for 1 year | Waived for 2 years with min spend of S$10,000/year |

| Sign-on Bonus | ||

| FX Fee | 3.25% | 3.25% |

Comparison to Similar Rebate Credit Cards

While POSB Everyday Card and OCBC 365 Card are well-known for their value as everyday cards, there are several alternatives that are also worth considering. We've reviewed them in detail below.

Citi Cash Back Card: Boosted Rebates on Food & Fuel

| |

If you spend a great deal on food and fuel, consider Citi Cash Back Card. Cardholders who spend at least S$888/month earn 8% rebate on global dining, groceries and petrol. These rates are quite high–even when compared to POSB Everyday and OCBC 365 Card. However, each category is individually capped at S$25/month (maxed out with S$312.5 spend), which may be limiting for those with higher or skewed spending.

| |

|

|

If you spend a great deal on food and fuel, consider Citi Cash Back Card. Cardholders who spend at least S$888/month earn 8% rebate on global dining, groceries and petrol. These rates are quite high–even when compared to POSB Everyday and OCBC 365 Card. However, each category is individually capped at S$25/month (maxed out with S$312.5 spend), which may be limiting for those with higher or skewed spending.

|

Maybank Family & Friends Card: Top Rates in SG & MY

| |

If you mostly spend in Singapore & Malaysia, Maybank Family & Friends Mastercard may just be the best option for you. Cardholders who spend S$500/month in these countries earn 5% cashback on fast food & online food delivery, groceries, transport, petrol and data communications/online TV streaming–amongst the highest rates available for lower spenders. Even better, consumers who spend S$800/month earn 8% in these categories, up to S$80/month. This cap can be maxed out with just S$1k spend–which qualifies the cardholder for a fee-waiver. After all, the S$180.0 fee is waived 3 years and subsequently with just S$12k annual spend.

| |

|

|

If you mostly spend in Singapore & Malaysia, Maybank Family & Friends Mastercard may just be the best option for you. Cardholders who spend S$500/month in these countries earn 5% cashback on fast food & online food delivery, groceries, transport, petrol and data communications/online TV streaming–amongst the highest rates available for lower spenders. Even better, consumers who spend S$800/month earn 8% in these categories, up to S$80/month. This cap can be maxed out with just S$1k spend–which qualifies the cardholder for a fee-waiver. After all, the S$180.0 fee is waived 3 years and subsequently with just S$12k annual spend.

|

UOB One Card: Flat Rebate for Stable Spenders

| |

If you consistently spend about S$2k/month, you may be able to earn more with UOB One Card than with any other option currently on the market. Cardholders earn on a quarterly basis, based on their minimum spend within the 3 months. Those who spend at last S$2k every month earn 5% cashback on all spend, up to S$100/month (S$200/quarter). This is quite remarkable, adding up to a potential S$800 cashback within a year. Even better, there's no need to track categories or merchants, as the 5% rate is applied to all purchases–including recurring bills.

| |

|

|

If you consistently spend about S$2k/month, you may be able to earn more with UOB One Card than with any other option currently on the market. Cardholders earn on a quarterly basis, based on their minimum spend within the 3 months. Those who spend at last S$2k every month earn 5% cashback on all spend, up to S$100/month (S$300/quarter). This is quite remarkable, adding up to a potential S$1.2k cashback within a year. Even better, there's no need to track categories or merchants, as the 5% rate is applied to all purchases–including recurring bills.

|

Cashback Credit Card Comparison Tables

| Credit Card | Min. Spend | Rebates | Cap |

|---|---|---|---|

| Citi Cash Back | S$800 |

| S$80/mo |

| Citi SMRT | N/A |

| S$50/mo |

| DBS Live Fresh | S$600 |

| S$60/mo |

| OCBC 365 | S$800 |

| S$80/mo |

| OCBC Frank | S$600 |

| S$75/mo |

| POSB Everyday | Varies |

| Varies |

| UOB One | S$500-S$2k |

| S$100+/mo |

| UOB EVOL | S$600 |

| S$60/mo |

| Credit Card | Travel Ins | Petrol Savings | Card Perks |

|---|---|---|---|

| Citi Cash Back | Coverage up to S$1M | Up to 20.88% fuel savings at Esso & Shell | Citi World Privileges, Citi Gourmet Pleasures |

| Citi SMRT | N/A | Up to 20.88% fuel savings at Esso & Shell | Citi World Privileges, Citi Gourmet Pleasures |

| DBS Live Fresh | N/A | Up to 14% fuel savings at Esso | #FreshDropFriday Sweeps |

| OCBC 365 | Coverage up to S$500k | Up to 22.1% savings at Caltex, 20.2% at Esso, 26.8% at Sinopec and 5% cashback at all other petrol stations | Visa Concierge & Luxury Hotels |

| OCBC Frank | N/A | Up to 23% fuel savings at Sinopec, 16% at Caltex, 14% at Esso | Frank Hot Deals |

| POSB Everyday | N/A | Up to 20.1% + 2% fuel savings at SPC | POSB Merchant Deals |

| UOB One | Coverage up to S$500k | Up to 22.66% fuel savings at SPC, 21.15% at Shell | UOB SMART$, UOB Travel & Dining Advisors |

| UOB EVOL | Coverage up to S$500k | Up to 20% fuel savings at SPC, 14% at Shell | UOB SMART$, YOLO events |

| Credit Card | Annual Fee | Spend Waiver | Promotion |

|---|---|---|---|

| Citi Cash Back | S$194.40 | Waived for 1 year | |

| Citi SMRT Back | S$194.40 | Waived for 2 years | |

| DBS Live Fresh | S$194.40 | Waived for 1 year | |

| OCBC 365 | S$194.40 | Waived for 2 years with min spend of S$10,000/year | |

| OCBC Frank | S$80 | Waived 2 years, & subsequently with S$10,000 annual spend | |

| POSB Everyday | S$192.60 | Waived for 1 year | |

| UOB One | S$194.40 | Waived for 1 year | |

| UOB EVOL | S$192.60 | Waived for 1 year, no annual fees if min. 3 transactions per month for 12 consecutive months |

Learn More About Finding the Best Credit Card for You

- In-Depth Comparison: OCBC Frank Card vs. OCBC 365 Card

- In-Depth Comparison: UOB One Card vs. OCBC 365 Card

- In-Depth Comparison: UOB One Card vs. UOB YOLO Card

- In-Depth Comparison: DBS Live Fresh Card vs. UOB YOLO Card

- In-Depth Comparison: DBS Live Fresh Card vs. POSB Everyday Card

- How to Use a Credit Card

- How to Find the Best Rewards Credit Card

- Comparing Fee Credit Cards to No Annual Fee Cards in Singapore

- Understanding Credit Cards' Minimum Spend Requirements

- Understanding Rewards Caps on Monthly Earnings

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.