Compare Rewards Credit Cards in Singapore

Great Maximum Cashback for Stable Budgets

UOB One Credit Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$40,000 |

|---|---|

| Overall Rewards Rate | 5.22% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

If you spend at least S$2,000 per month and want cashback on daily spend and bills, UOB One Card might just be the right fit for you. You can earn up to 5% rebate on general spend, 10% on Grab and 6% on utilities, adding up to S$300/quarter. This card also gets you petrol discounts at Shell and SPC stations.

- Annual fee: S$192.60 (first year- waived)

- 5% rebate on general spend, up to S$200/quarter (S$2,000 min spend) with min 5 transactions/mo

- Up to 10% on Grab, Shopee, Dairy Farm Singapore & select UOB travel, 1% on utilities bills

- 3.33% rebate, up to S$100/quarter (S$1,000 min spend)

- 3.33% rebate, up to S$50/quarter (S$500 min spend)

- 0.03% rebate on all spend if no rebate earned for calendar year

- Up to 21.15% savings at Shell and 22.66% at SPC

If you spend at least S$2,000 per month and want cashback on daily spend and bills, UOB One Card might just be the right fit for you. You can earn up to 5% rebate on general spend, 10% on Grab and 6% on utilities, adding up to S$300/quarter. This card also gets you petrol discounts at Shell and SPC stations.

- Annual fee: S$192.60 (first year- waived)

- 5% rebate on general spend, up to S$200/quarter (S$2,000 min spend) with min 5 transactions/mo

- Up to 10% on Grab, Shopee, Dairy Farm Singapore & select UOB travel, 1% on utilities bills

- 3.33% rebate, up to S$100/quarter (S$1,000 min spend)

- 3.33% rebate, up to S$50/quarter (S$500 min spend)

- 0.03% rebate on all spend if no rebate earned for calendar year

- Up to 21.15% savings at Shell and 22.66% at SPC

| Annual Income Needed | Citizen: S$30,000 Foreign: S$40,000 |

|---|---|

| Overall Rewards Rate | 5.22% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

Maybank Family & Friends Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 4.83% |

| Annual Fee | S$180.00 |

| Annual Fee Waiver Amount | S$12,000 |

Maybank Family & Friends MasterCard is a good option for earning cash back on essential spending with a moderate budget. Earn 5% on groceries, food delivery, transport and more if you spend S$500/month. If you spend over S$800/month, the cashback rate increases to 8% with a cap of S$80.

- Annual fee: S$180 (3 years fee waiver)

- Up to 8% rebate on 5 preferred categories (dining & food delivery, groceries, retail, petrol discounts & online TV streaming)

- Up to S$125 cashback per month with S$800 min spend

- 0.3% rebate all other spend

Maybank Family & Friends MasterCard is a good option for earning cash back on essential spending with a moderate budget. Earn 5% on groceries, food delivery, transport and more if you spend S$500/month. If you spend over S$800/month, the cashback rate increases to 8% with a cap of S$80.

- Annual fee: S$180 (3 years fee waiver)

- Up to 8% rebate on 5 preferred categories (dining & food delivery, groceries, retail, petrol discounts & online TV streaming)

- Up to S$125 cashback per month with S$800 min spend

- 0.3% rebate all other spend

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 4.83% |

| Annual Fee | S$180.00 |

| Annual Fee Waiver Amount | S$12,000 |

Great High Flat-Rate Cashback for Low Spenders

Maybank Platinum Visa Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 3.76% |

| Annual Fee | S$80.00 |

| Annual Fee Waiver Amount | none |

If you are a young adult with a monthly budget of S$300-S$500/month looking for a starter card, then you should consider Maybank Platinum Visa. At 3.33% cashback on S300 spend, it offers the highest cashback on low spend on the market. With monthly spend of S$1,000 you can earn up to S$100/quarter.

- Annual fee: S$80 (3 years fee waiver)

- Subsequently quarterly service fee is waived w/ card use at least 1x/quarter

- Up to 3.33% on all local and foreign currency spend

- $30 quarterly rebate with at least S$300 monthly spend

- S$100 quarterly rebate with at least S$1,000 monthly spend

- Free travel insurance

If you are a young adult with a monthly budget of S$300-S$500/month looking for a starter card, then you should consider Maybank Platinum Visa. At 3.33% cashback on S300 spend, it offers the highest cashback on low spend on the market. With monthly spend of S$1,000 you can earn up to S$100/quarter.

- Annual fee: S$80 (3 years fee waiver)

- Subsequently quarterly service fee is waived w/ card use at least 1x/quarter

- Up to 3.33% on all local and foreign currency spend

- $30 quarterly rebate with at least S$300 monthly spend

- S$100 quarterly rebate with at least S$1,000 monthly spend

- Free travel insurance

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 3.76% |

| Annual Fee | S$80.00 |

| Annual Fee Waiver Amount | none |

Great Unlimited Cashback for High Spenders

Standard Chartered Simply Cash Credit Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 2.67% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

Standard Chartered Unlimited Cashback Card offers just that, unlimited 1.5% cashback on all purchases with no minimum spend. Best option for affluent spenders with a monthly budget of S$7,000, with this card you can also enjoy 21% fuel savings at Caltex.

- Annual fee waived for two years

- Unlimited 1.5% cashback on all spend

- Caltex petrol discounts up to 21%

Standard Chartered Unlimited Cashback Card offers just that, unlimited 1.5% cashback on all purchases with no minimum spend. Best option for affluent spenders with a monthly budget of S$7,000, with this card you can also enjoy 21% fuel savings at Caltex.

- Annual fee waived for two years

- Unlimited 1.5% cashback on all spend

- Caltex petrol discounts up to 21%

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 2.67% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

CIMB Visa Signature

| Annual Income Needed | Citizen: S$30,000 Foreign: N/A |

|---|---|

| Overall Rewards Rate | 2.63% |

| Annual Fee | S$0.00 |

| Annual Fee Waiver Amount | none |

With CIMB Visa Signature Card, you can earn 10% cashback on online retail, beauty, pet shops, groceries, and cruise line transactions. In addition to the no annual fee, you can enjoy complimentary travel insurance and concierge service.

- Annual fee: free for life

- 10% cashback on groceries, online shopping, beauty, petcare & cruises

- Unlimited 0.2% cashback on all other retail purchases

- Free travel insurance & global concierge

- CIMB 0% Interest i.Pay Instalment Plan

With CIMB Visa Signature Card, you can earn 10% cashback on online retail, beauty, pet shops, groceries, and cruise line transactions. In addition to the no annual fee, you can enjoy complimentary travel insurance and concierge service.

- Annual fee: free for life

- 10% cashback on groceries, online shopping, beauty, petcare & cruises

- Unlimited 0.2% cashback on all other retail purchases

- Free travel insurance & global concierge

- CIMB 0% Interest i.Pay Instalment Plan

| Annual Income Needed | Citizen: S$30,000 Foreign: N/A |

|---|---|

| Overall Rewards Rate | 2.63% |

| Annual Fee | S$0.00 |

| Annual Fee Waiver Amount | none |

UOB EVOL Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$40,000 |

|---|---|

| Overall Rewards Rate | 2.6% |

| Annual Fee | S$192.60 |

| Annual Fee Waiver Amount | none |

UOB EVOL is a great and easy-to-use card for young adults who primarily shop online. With a minimum spend of S$600 per month, you can earn 8% rebate on all online and mobile transactions.

- Annual fee: S$192.60 (first year- waived)

- 8% cashback on online and mobile contactless spend

- 0.3% cashback on all other spend

- S$600 min spend, S$60 cashback cap

- Southeast Asia’s first bio-sourced card

UOB EVOL is a great and easy-to-use card for young adults who primarily shop online. With a minimum spend of S$600 per month, you can earn 8% rebate on all online and mobile transactions.

- Annual fee: S$192.60 (first year- waived)

- 8% cashback on online and mobile contactless spend

- 0.3% cashback on all other spend

- S$600 min spend, S$60 cashback cap

- Southeast Asia’s first bio-sourced card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$40,000 |

|---|---|

| Overall Rewards Rate | 2.6% |

| Annual Fee | S$192.60 |

| Annual Fee Waiver Amount | none |

Best for Getting Cashback on Everyday Purchases

Citi Cash Back Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$42,000 |

|---|---|

| Overall Rewards Rate | 2.56% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

The Citi Cash Back Card is a good choice for everyday spend, with a generous 8% cash back on groceries, 6% cash back on dining, and discounted petrol at Esso and Shell. Be prepared for the S$800 monthly spend requirement and the annual fee.

- Annual fee: S$194.40 (first year- waived)

- 8% cashback on groceries

- 6% cashback on dining

- Up to 20.88% fuel savings at Esso & Shell and 8% cashback at other petrol stations

- 0.25% cashback on all other purchases

- Min. monthly spend of S$800 required to earn bonus cashback

- Cashback capped at S$80/month

The Citi Cash Back Card is a good choice for everyday spend, with a generous 8% cash back on groceries, 6% cash back on dining, and discounted petrol at Esso and Shell. Be prepared for the S$800 monthly spend requirement and the annual fee.

- Annual fee: S$194.40 (first year- waived)

- 8% cashback on groceries

- 6% cashback on dining

- Up to 20.88% fuel savings at Esso & Shell and 8% cashback at other petrol stations

- 0.25% cashback on all other purchases

- Min. monthly spend of S$800 required to earn bonus cashback

- Cashback capped at S$80/month

| Annual Income Needed | Citizen: S$30,000 Foreign: S$42,000 |

|---|---|

| Overall Rewards Rate | 2.56% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

Load More

If you're interested in more information about the best rewards cards on the market, we've come up with a list of top picks that we think stand out from the rest.

- UOB One: Highest flat rebate on the market, earn up to $300/qtr

- Maybank Family & Friends: 8% cashback with S$800 min. spend requirement

- Citi Cash Back: Up to 8% rebate on groceries & petrol, 6% on dining

- POSB Everyday: Rebates up to 10% in Singapore

- DBS Altitude: Earn 5 miles per S$1 spend on online flight & hotel transactions (capped at S$5,000 per month) and overseas spend (at point-of-sale), earn S$1 = 2 miles on overseas spend (online transactions), earn S$1 = 1.2 miles on local spend. All miles earned through this card is via DBS Points and thus will never expire.

- Citi PremierMiles: 45,000 Welcome Citi Miles with S$9,000 spend in 3 mo

- KrisFlyer UOB: 3mi/S$1 on dining, transport, shopping & travel

- Amex SIA KrisFlyer: Directly earn KrisFlyer miles, S$150 SIA credit

- UOB PRVI Amex: Fee-Waiver + 20k bonus miles, 2.4 miles per $1 overseas

- OCBC 365: 6% rebate on dining, 3% rebate on groceries, utilities and travel, Visa Concierge Services

- MB Horizon Visa: Market-leading 3.2 miles per S$1 select local spend

- Citi Cash Back+: Unlimited 1.6% cashback on all spend

- HSBC Advance: Up to 3.5% cashback capped at S$300/month

- SC Visa Infinite X: Bonus S$6,000 w/ S$200k fund placement

- OCBC Voyage: Flexible miles redemption, boosted rewards for overseas spend

- OCBC Frank: Up to 6% rebate for FX, online and mobile purchases, low S$600 min. spend requirement

- Citi SMRT: 5% everyday rebates w/S$500 min spend

- MB Platinum Visa: Up to 3.33% rebate on local and foreign currency spend

- HSBC Revolution: 4 miles per S$1 spent online and on contactless payments

- DBS Live Fresh: Get up to 10% cashback w/ S$600 min. spend - 5% cashback on Online and Visa Contactless Spend, 5% green cashback at selected eco-eateries, retailers and transport services. Additional 0.3% cashback on all other spend

How to Select the Best Credit Card for You

In order to select the best credit card for you, the first step is to figure out whether you are looking for a card that rewards your spend in miles or in monthly cashback. The second step is to figure out whether you want a card that rewards a particular spend category or one that more broadly saves you money on general spend. Third, you need to decide what your monthly budget is and what categories you spend the most money in.

Typically, if your monthly budget is below S$1,000, most cards will have a cashback cap, a minimum spend required to earn cashback and a higher cashback rate. Most credit cards in this budget are categorized as young adults credit cards. If your monthly spend is between S$1,000 and S$2,000 you can expect to meet the minimum spend for cards, but most will still have a cap on cashback. For budgets above S$2,000 per month, most cashback cards will not have a minimum spend requirement, and will often offer unlimited and uncapped cashback. The main downside of these cards is that the cashback rate tends to be lower for unlimited rewards cards.

Credit Cards Category Breakdown

| Sort Credit Cards By... | Option A | Option B |

|---|---|---|

| Rewards Type | cashback cards | miles cards |

| Expenditure | General spend | Rewards on specific spend (dining, groceries, shopping and many more) |

| Income | High Income Earners | Medium earner/ Young Adults |

| Minimum Spend | Minimum spend required for rewards | No minimum spend required |

| Additional categories | Expats & foreigners | Seniors |

Learn More About the Best Rewards Credit Cards

Choosing a Rewards Card Based on Your Spending Behaviour

While most consumers shopping for a rewards credit card just want to find out "What is the best rewards card?", the answer unfortunately depends on many different factors. Which rewards card will be the best for you will depend entirely on your personal spending, travel and credit habits. Taking a moment to consider your personal preferences before searching for a card will go a long way in helping you find the best deal.

Do You Keep A Balance On Your Credit Card?

In exchange for giving you bonuses and rewards, rewards credit cards always charge an extremely high interest rates around 25%. If you're unable to pay off your monthly charges in entirety, additional interest will easily exceed what you earn in rewards. Therefore, rewards cards are only beneficial for consumers who pay off their credit card bills on time on a monthly basis. If you are having difficulty in doing this, you should consider getting a low interest credit card or sticking to using cash. You're much better off reducing your interest payments than trying to get a few percentage points in rewards.

How Do You Use Your Rewards?

For you to benefit from rewards cards, you actually have to use them. People tend to rack up miles and points that are never used. Even worse, many miles and reward points expire within a certain time frame. For those consumers these rewards might as well be worth nothing. Since some rewards expire, you might want to consider whether you like save up towards one big redemption or want to be redeem rewards as frequently as possible.

Also, consider what kind of rewards you actually will be likely to use. Do you travel frequently, and would like to get free air tickets? Or would you rather receive cashback for daily purchases? Lastly, you should consider how much you value flexibility. While cashback rewards are often immediately awarded, redeeming miles often take weeks of preparation because of processing time, and it may be more difficult to earn a free trip than you would like.

How Much Money Can You Spend?

Cards with the highest rewards rates often come with a high annual fee and minimum spend requirements. With many no-fee rewards credit card options available, the decision to pay an annual fee will depend on the amount you will spend on the card. As a rule of thumb, you should plan to spend at least S$500 a month per card for a fee-based rewards card to be viable.

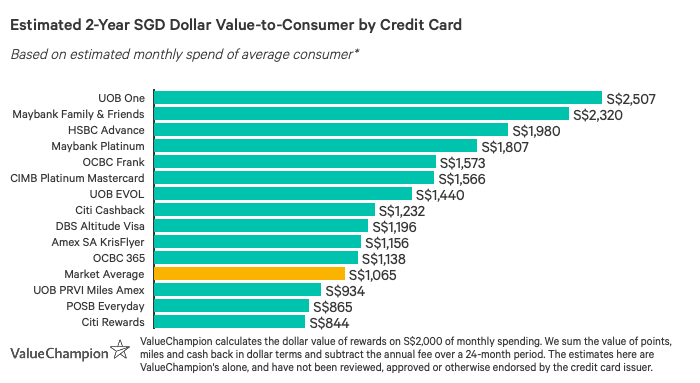

What credit card you should choose should depend first on how much money you spend. For example, my friend Robert makes S$50,000 a year, and spends about S$2,000 on his UOB One Card on a monthly basis. UOB One Card is a great cashback card that provides up to 5% cash rebate for all of your expenditures, plus some other benefits like discounts on petrol. Based on Rob's spending level, this translates to about S$1,200 of cash rebate annually, which nets out to S$2,207.4 in rebate over 2 years after subtracting S$192.6 of annual fee (which is waived for 1 year). While this may seem great, one should wonder: what if Robert spends less money?

Because UOB One Card requires at least S$2,000 of monthly spend to qualify for the 5% rebate, anything less would only earn maximum 3.33% of flat rate cashback. This means that my other friend Henry, who only spends S$1,000 on his card every month, can only earn S$607.4 in net cash rebate over 2 years if he uses the UOB One Card. In this case, Henry may have been better off by using a card like OCBC 365 Card, which earns cash rebate and waives the annual fee for anyone who spends S$10,000 per year on the card. To be specific, OCBC 365 earns 24% on petrol, 3% on online shopping, up to 6% on dining and 3% on groceries, among other things.

Let's now assume that my third friend Tom is a foodie who loves to eat well. However, he doesn't care that much about traveling, shopping or entertainment (i.e. bars, karaokes, etc.). Therefore, he spends about 60% of his monthly budget on dining and groceries, while Henry only spends 35% of his spending on these two categories. In this case, Tom should prefer to use Citi Cash Back Card over using OCBC 365 Card, since Citi Cash Back card earns 8% cash rebate on all of his dining and grocery bills.

There are many other factors besides your spending patterns that you must consider before choosing the right credit card. For instance, you may want to go for an air miles credit card instead of a cash back card if you tend to travel frequently. This is especially so for people who like to redeem their miles for business class or first class seats. Our study has shown that 1 mile can be worth up to S$0.08 for longer and more expensive flights, compared to S$0.01 conversion rate for economy flights.

Let's consider our example of Robert again from the scenario above, who spends about S$2,000 per month on his card. If he used a Citi PremierMiles Visa Card, he could be earning about 110,920 of miles over 2 years, plus additional savings on petrol, according to our calculations. This is because Citi PMV card awards 1.2 miles for every S$1 you spend locally, 2 miles for S$1 you spend overseas, 15,000 miles for customers who use the card within the first 3 months, and another 10,000 miles when you pay the S$192.6 of annual fee to renew your card. It can also earn 14-15% discounts on petrol in Singapore. If you were to convert the 111,000 miles you earn at a S$0.03 to 1 mile rate (i.e. short-haul business class seat), that's worth significantly more than the cashback Robert would earn on UOB One Card even after subtracting the annual fees. On the other hand, if Rob used his miles at a S$0.01 per mile rate, or never redeemed his miles at all, then UOB One Card would be the better deal.

In examining the different rewards credit cards, we looked at different factors that should influence your decision. Understanding all these different aspects can help you figure out just how good a card really is.

How Do the Rewards Work?: While most cards use the same set of terms (points, miles, cash back), the ways these rewards work will vary significantly. Some rewards can be applied as statement credits, as cashback, as reward points or as miles. Some cards will even allow for conversion between rewards points and miles. While cashback and statement credits are two best options for most people, miles can be highly valuable for those who redeem them for long-haul flights on business class or better. Some cards also allow you to transfer your rewards to other loyalty programs giving you another way to use what you've earned.

Rewards Rate: If your rewards card is going to be your primary card then the rewards rate for general spending is very important. For everyday spending you can expect to earn up to 5% of what you spend as rewards. As a rule of thumb, the more flexible the type of reward you get, the lower the rewards rate you can expect. Otherwise, you could pick a few cards that collectively offer high award rates on most of your expenditures.

Welcome & Renewal Bonuses Matter: The promotions offered to new card holders and renewal bonuses are major contributors of the value you can get from rewards cards. Most of these bonuses require you to either make a purchase on the card or spend a certain amount within a set time limit. Because the value of welcome bonuses and renewal bonuses can range from S$50 - S$500, you should make sure to fulfill the qualifications.

FAQs

That largely depends on your spending habits. There are credit cards best suited for high or low spenders, for frequent travelers and those looking for no fee credit cards. For example, DBS Altitude Visa credit card is a great option for frequent travelers looking for affordable luxury perks, while OCBC 365 Card card may be a better option for those looking for those with broad spending habits seeking daily rebates.

Rewards credit cards can be worth it if you can find one that fits your needs and your spending profile. The best option is to find a card which rewards your spending behavior without requiring you to change your habits. Read our guide to figure out which one is the best fit for you.

Rewards credit cards generally reward certain spending habits and spending amounts, based on the terms of the given credit card. Cashback credit cards do just that: they give you cashback on certain everyday purchases. While cashback cards provide a nearly immediate reward, that is cash on your credit card, rewards credit cards work differently. Some in addition to providing cashback and rebates, reward you with accumulating points on certain purchases which in turn, provide other travel and entertainment perks over time. Rewards credit cards can often be part of a rewards program, which come with their own benefits.

- Overall Best Credit Cards

- Best Rewards Credit Cards

- Best Credit Card Promotions

- Best Cashback Credit Cards

- Best Air Miles Credit Cards

- Best Agoda Credit Card Promotions

- Best Expedia Credit Card Promotions

- Best Booking.com Credit Card Promotions

- Best Credit Cards with Klook Promo Codes

- Best No Annual Fee Credit Cards

- Best Miles Cards with No Annual Fee

- Best Cashback Cards with No Annual Fee

- Best Petrol Credit Cards

- Best Cards for SPC Discounts

- Best Cards for Esso Promotions

- Best Cards for Shell Discounts

- Best Shopping Credit Cards

- Best Student Credit Cards

- Best Credit Cards for Seniors

- Best Expat Credit Cards

- Best Unlimited Cashback Credit Cards

- Best Cards for High Income

- Best Dining Credit Cards

- Best Cards for Food Delivery

- Best Credit Card 1 for 1 Buffet Promotions

- Best Grocery Credit Cards

- Best Entertainment Credit Cards

- Best Credit Cards for TransitLink SimplyGo

- Best EZ-Link Credit Cards

- Best Cards for Insurance

- Medical Credit Cards

- Wedding Credit Cards

- Best Debit Cards

- Best Cards for Seniors