"Spring Clean" Your Way into Having More Money

Spring cleaning is often associated with re-organising your closet or taking that extra step in cleaning out your home. However, this concept can go beyond simply throwing things away. In fact, you may actually find yourself saving a few extra thousand dollars a year when you extend spring cleaning to other areas of your life. Whether it's going beyond simple housework to check for things that might need repairs or re-evaluating your investment portfolio, we discuss the ways uncluttering and re-organising your life can help save you money.

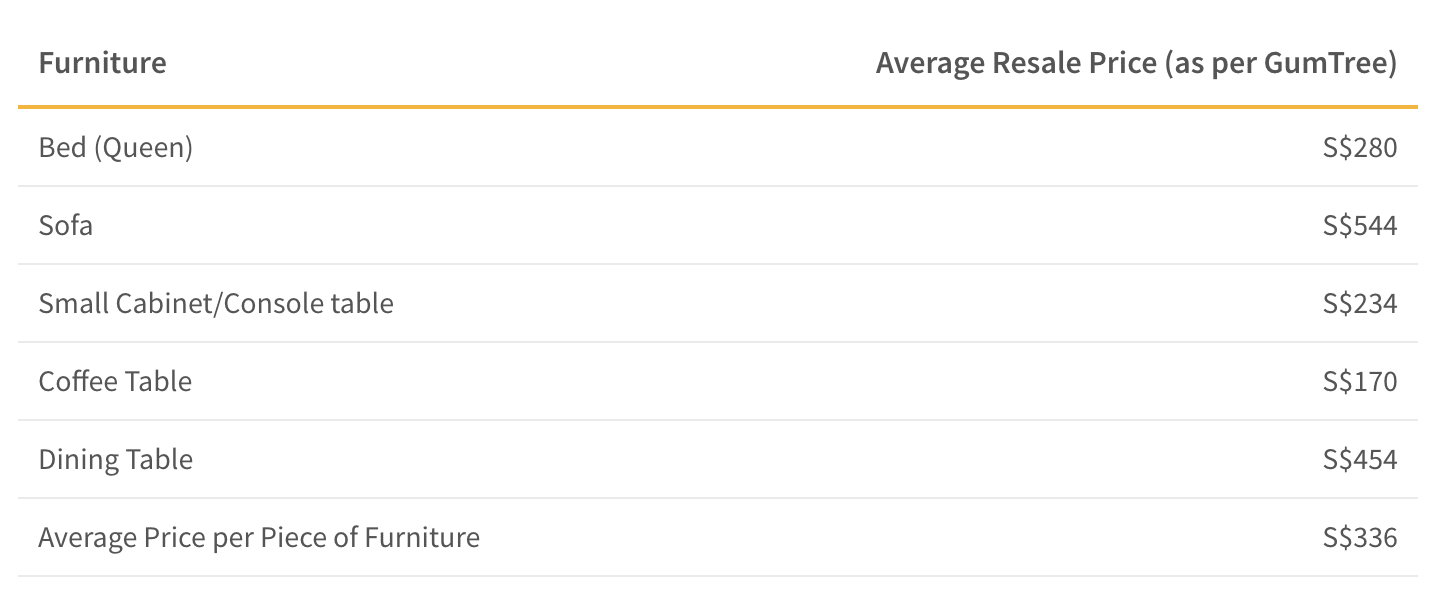

Sell Your Unused Furniture

Decluttering your home can reap more than just the feeling of satisfaction when you're finally done—it can also be a good way to earn some extra income along the way. You should sort through your furniture for things that are broken, redundant or even seldom used items that you simply don't enjoy anymore and find ways to sell or salvage them. You can make some extra money with your broken items by recycling them through a "Cash-for-Trash" programme. Though the money earned from these programmes isn't high enough to write home about, it is still a good financial incentive to both clear out your home and do your part for the environment. You can sell gently used items on classifieds or donate them to second-hand stores. Reducing the amount of items in your home will help you evaluate what you truly need versus impulse buys, leading to smarter spending habits in the future.

Conduct Maintenance Checks to Reduce Utility Bills and Prevent Costly Repairs

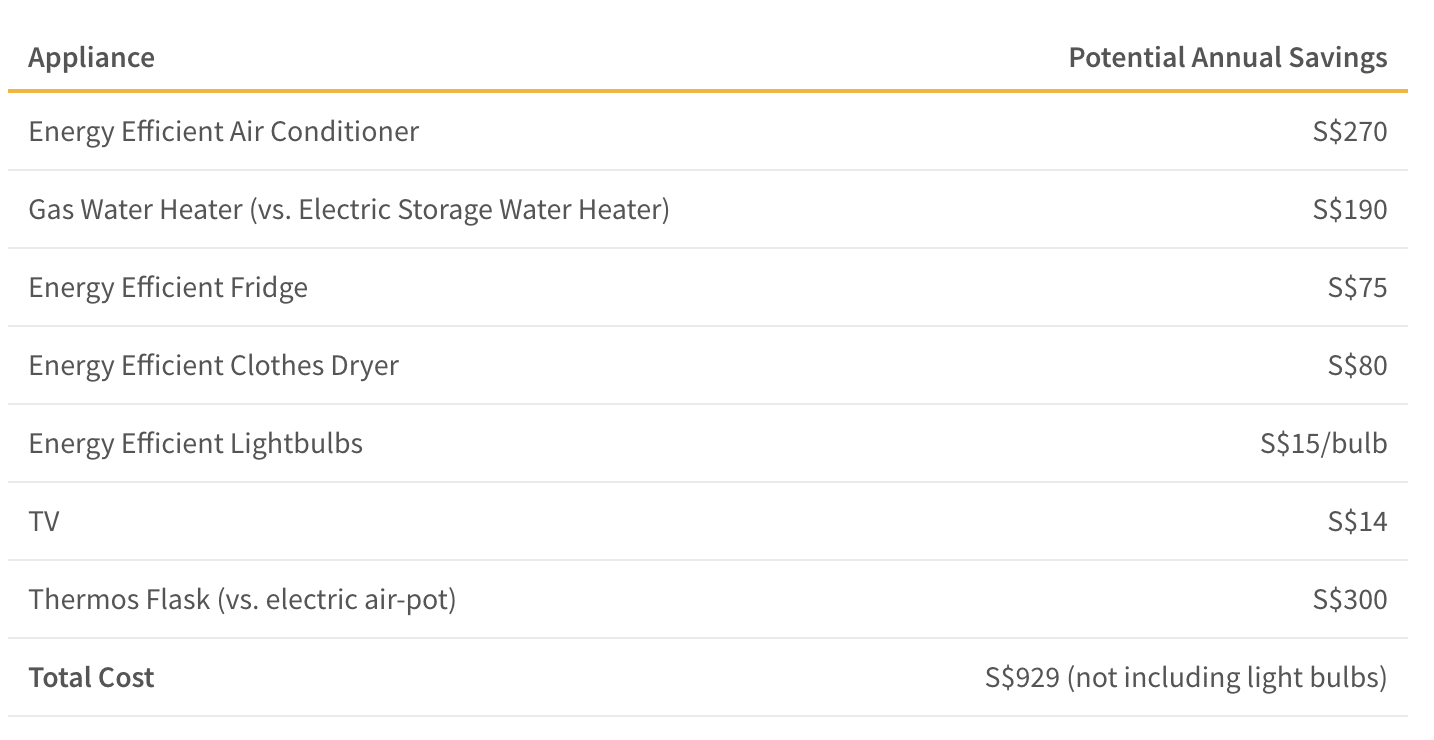

Dirty, leaking appliances are likely to run up your utilities bill. The top three most utilised appliances (air conditioner, refrigerator, water heater) account for 75% of Singaporean's overall household energy consumption and are also the culprits for excessively high utility bills. To reduce your utility bill and prevent costly repairs due to neglect, you should consider doing maintenance and efficiency checks on these appliances a few times a year. For instance, you should consider cleaning out the filter of your air conditioner to improve its energy efficiency and schedule it to run only when necessary. Additionally, clearing out your fridge and checking for leaks can also help reduce your utility bills by reducing the work on its compressor and by improving its air circulation. If you notice your appliances are struggling to perform well or they're costing you more than you expect, you can consider replacing them with energy efficient models. Though this will cost you money in the beginning, your energy savings can add up to S$1,000 per year.

Re-analyse Your Insurance to Save on Premiums

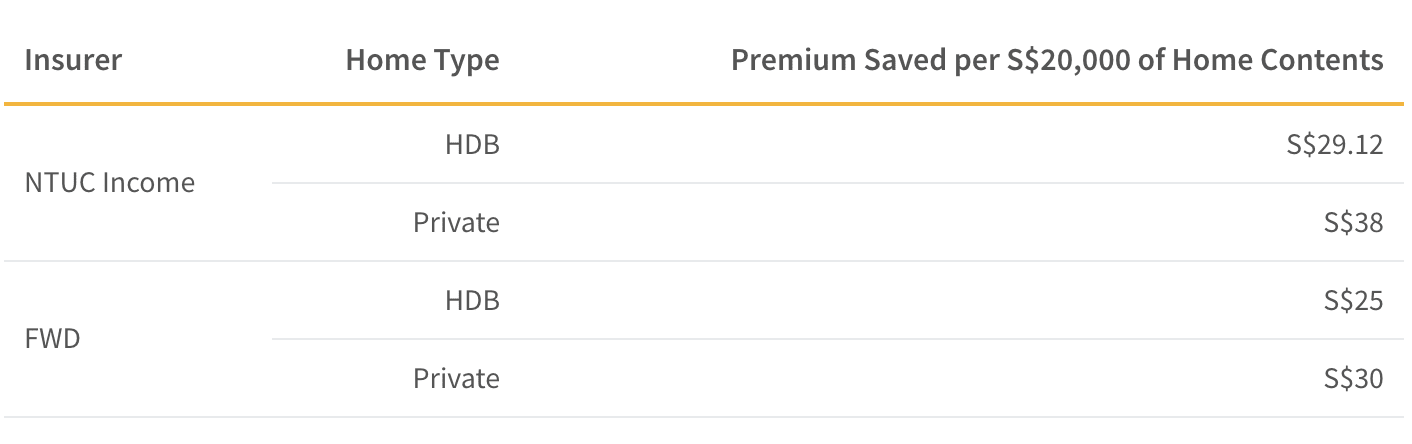

While not the most exciting chore, reviewing your insurance expenditures can help you identify where you can cut costs. Re-evaluating your insurance policies can be especially beneficial if you have been getting the feeling that you are overpaying for benefits you are not utilising. Obligatory policies such as car, maid or home insurance can often be found at more competitive rates than the default policies you would get from your maid agency or car dealer.

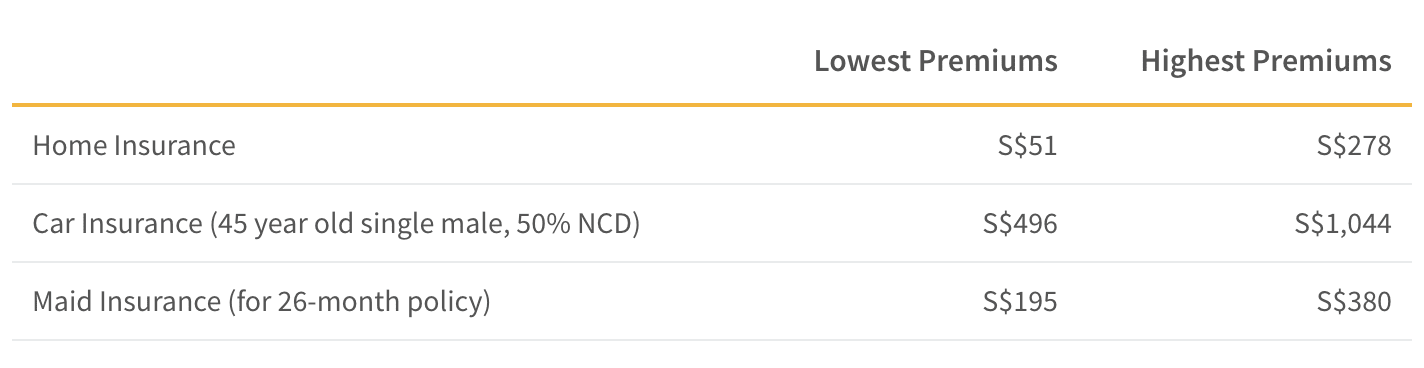

For example, the current cheapest home insurance policies cost between S$50-S$60 for a basic plan. Comparatively, the most expensive basic plans cost between S$230-S$280. In this case, switching insurers can save you up to S$230 per year. If you end up selling a significant chunk of your unused furniture (for instance, your children moved out and you need to get rid of their old furniture), you may even be able to lower your home insurance premium by reducing your home content coverage.

Car insurance is a bit tricky since it depends on many factors, including ones that are out of your control. However, you can still save a couple hundred dollars by shopping around for the cheapest car insurance policy. Maid insurance follows the same story. In total, you can save around almost S$1,000 simply by annually re-analysing your insurance options.

In some cases, you may find that certain insurers are cheapest across all of your insurance sectors. In this case, consolidating your insurance policies can save you money and make for better organisation. Some insurers even offer discounts if you have taken out multiple policies with them. You should also take the time to update your insurer of any life-changing events, such as getting married, buying a house or having children. Your new life event may qualify you for lower premiums, as is the case with car insurance premiums after getting married.

Get Rid of Superfluous Credit Cards to Decrease Debt

The average Singaporean is known to hold about 3.9 credit cards. While this number of credit cards may be manageable for people who keep meticulous track of their finances, reducing your number of credit cards to 2 can be more beneficial in the long run. This is for several reasons. First, people tend to assume that credit cards can be used as free cash—and end up racking up a lot of debt because of it. Case in point, credit card debt is one of the fastest growing categories of consumer debt in Singapore. Second, reducing the number of credit cards can help quell your spending by limiting your credit limit, making it easier to keep track of your bills and reduce reward points overlap.

If you want to have two credit cards, you should opt for one based on your current spending habits. Additionally, while credit card marketing in Singapore can be very persuasive, you should avoid getting cards just because they entice you with rewards you'll never use. If you don't travel, it's highly unlikely that your miles rewards credit card will reap real rewards. If you don't own a car, there's really no use for a credit card that provides discounts on petrol. You should take a realistic look at your spending habits and choose two credit cards that will reward you generously for the things you spend money on most.

To that extent, you should always use your credit cards wisely: spend only what you can afford and actively utilise your rewards when necessary. If you are having problems paying off your credit card debt, you can consider a debt consolidation loan, which can not only make payments easier and in one place, but can also provide a lower interest rate than your credit cards.

Take a Second Look at Your Investments

Just as it is important to declutter your closet and home, it is just as important to declutter your investment portfolio. If your investment portfolio has become unwieldy or you are noticing very lackluster returns, re-evaluating and cleaning up your investments can help get you back on track. You should re-evaluate your broker by comparing their commission rates, ease of use and market access. If you are still a novice investor, you should find one good brokerage that meets your needs and stick to it.

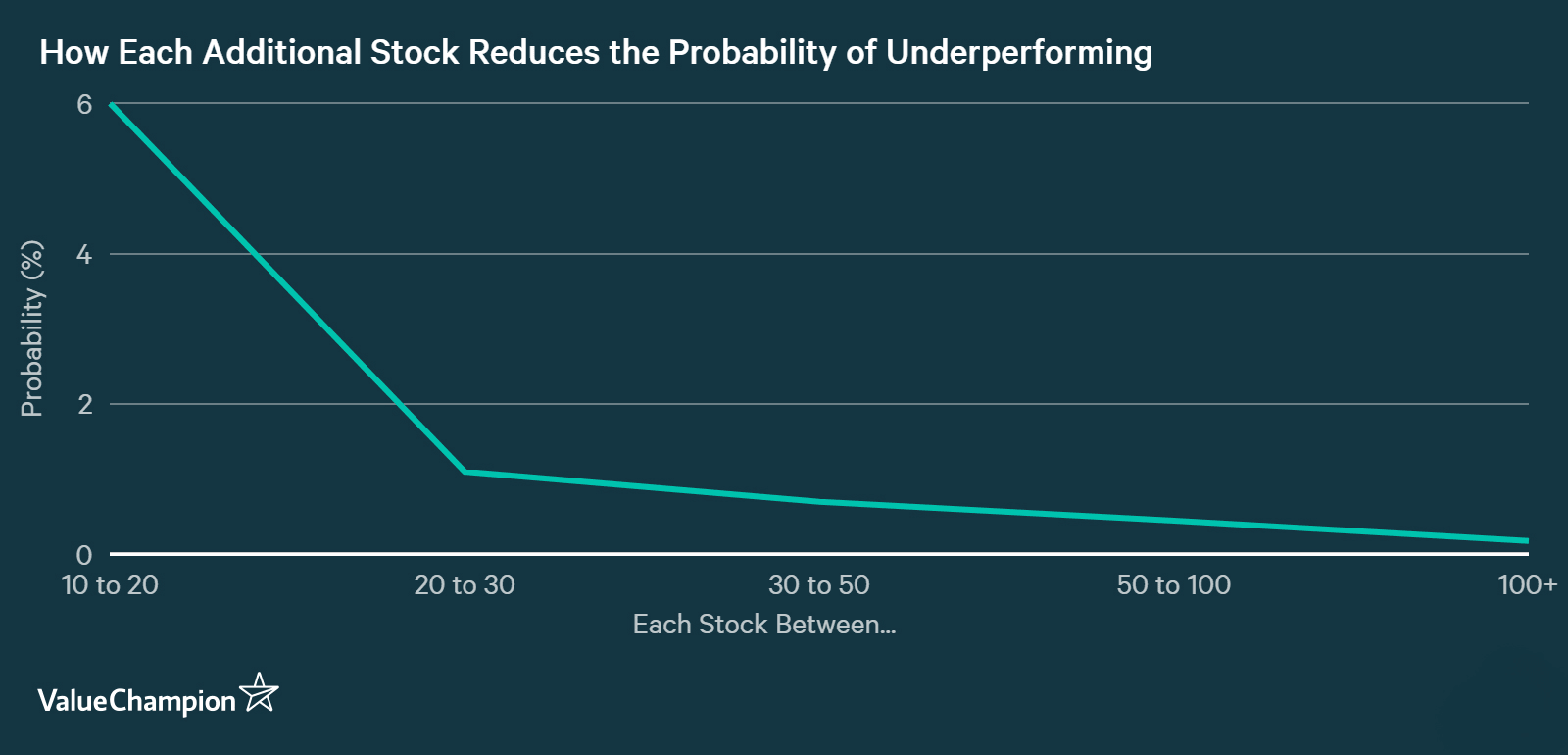

Additionally, you should look at the purpose of each of your investments and see whether or not they add value to your overall portfolio. You should only invest in what you know and what you feel comfortable putting your money in. For instance, you can consider consolidating investing in an Electronically Traded Fund (ETF) if you notice you have a lot of individual stocks that belong to a single industry. An ETF is a "basket" of stocks or bonds in a single fund and will generally be less risky than holding individual stocks. Furthermore, you shouldn't mistake diversification to mean having as many different investments just for the sake of it. In fact, diversifying too much can actually hurt your portfolio. Having a few well-researched investments that balance each other out can help mitigate market risk in the long run, as well make tracking and revising your investment strategies that much easier.

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.