{"buttonLabel":"Apply Now","productCollection":"credit_cards","productId":"31","productLink":"https:\/\/forms.uob.com\/sg\/apply\/?productId=001843&s_cid=pfs:sg:paid:aff:refprg:na:bu:na:001843:200521-evergreen:na:product:valuechampion&vid=valuechampion&pib=false","productName":"UOB One Credit Card"}

{"buttonLabel":"Apply Now","productCollection":"credit_cards","productId":"31","productImage":"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/v1692164328\/UOB_One_credit_card_vertical_card_face.jpg","productLink":"https:\/\/forms.uob.com\/sg\/apply\/?productId=001843&s_cid=pfs:sg:paid:aff:refprg:na:bu:na:001843:200521-evergreen:na:product:valuechampion&vid=valuechampion&pib=false","productName":"UOB One Credit Card"}

UOB One Credit Card: Highest Flat Rate Cashback Card

For most spenders, there's no better way to maximise cashback than with UOB One Card. Up to 5% flat rebate, boosted to 10% on Dairy Farm, Grab, Shopee & select UOB Travel and 6% on utilities. At this spend level, cardholders can earn up to S$300/quarter, or S$100/month–one of the highest potential earning rates on the market. Lower or inconsistent spenders with budgets as low as S$500/month can also earn a 3.33% cashback. Ultimately, if you’re looking for a convenient card that rewards stable budgets with top rates, there’s no better option than UOB One Card.

UOB One Credit Card Features and Benefits

Annual Fee: S$194.40, Waived for 1 year

Income Requirement: S$30,000 for citizens & PRs, S$40,000 for foreigners

Key Features:

Annual fee: S$192.60 (first year- waived)

5% rebate on general spend, up to S$200/quarter (S$2,000 min spend) with min 5 transactions/mo

Up to 10% on Grab, Shopee, Dairy Farm Singapore & select UOB travel, 1% on utilities bills

3.33% rebate, up to S$100/quarter (S$1,000 min spend)

3.33% rebate, up to S$50/quarter (S$500 min spend)

0.03% rebate on all spend if no rebate earned for calendar year

Up to 21.15% savings at Shell and 22.66% at SPC

Promotions:

Promotions:

Our Evaluation: Great Cashback Rates For Consistent Spenders

We think that one of the best things about UOB One Card is that it earns a pretty high cashback rate on just about any purchase you make with it. Although it does exclude certain types of expenses like bank fees and payment app transactions, most everyday purchases will earn some cashback with UOB One Card. On top of the high base cashback, it also offers many opportunities to boost your rewards by buying from certain merchants.

The UOB One Card is indeed one of the best cashback credit cards in Singapore for those with consistent spending. Offering cash rebates which increase with your total expenditure, it could be a good choice for high and consistent spenders to consider the UOB One Card.

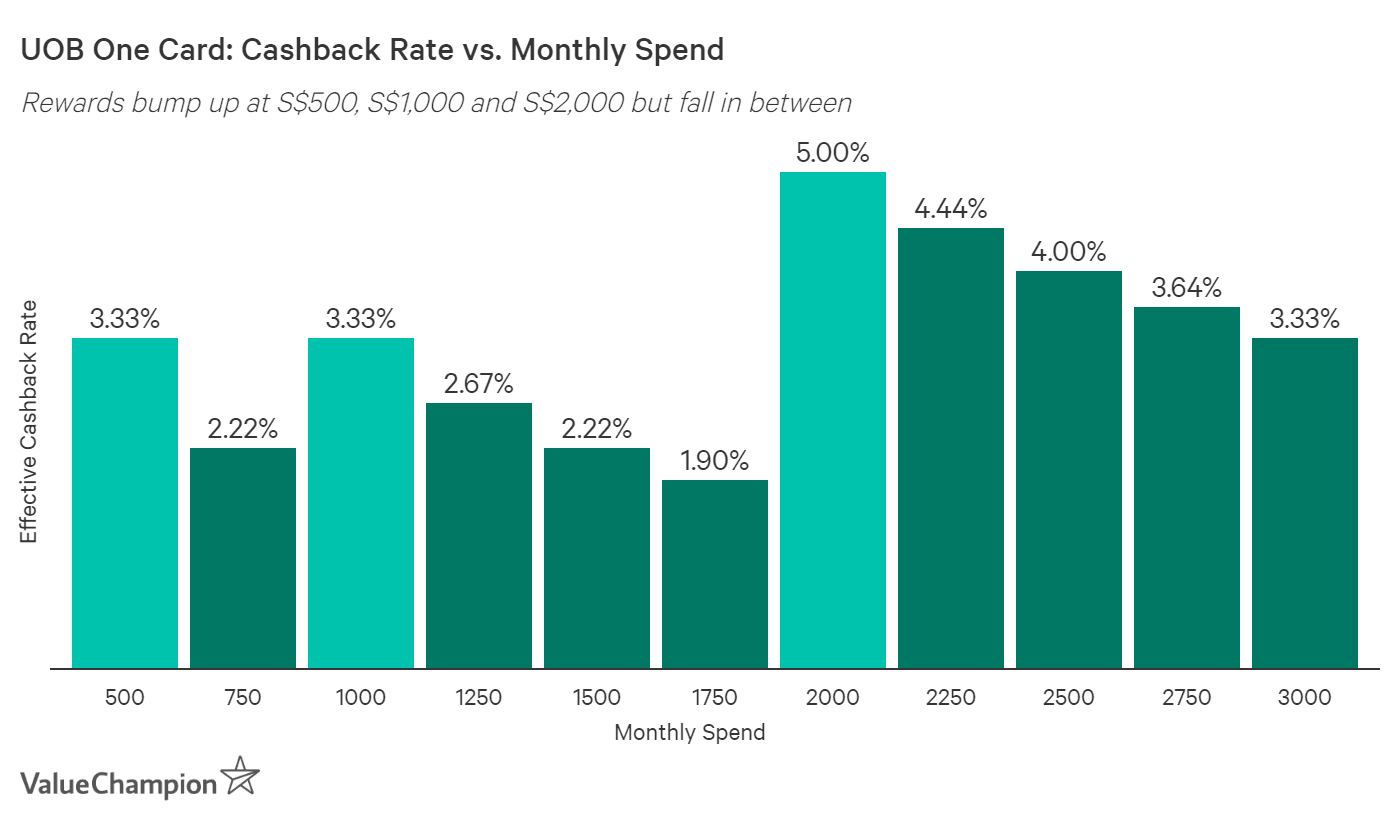

UOB One Card Quarterly Rebate Tiers

Low Spend

Medium Spend

High Spend

Minimum Monthly Spend

S$500

S$1,000

S$2,000

Minimum Spend for Quarter

S$1,500

S$3,000

S$6,000

Total Rebate

S$50

S$100

S$300

Rebate Rate

3.33%

3.33%

5.00%

Cardholder must make 5 transactions per month for all 3 months within the quarter to be eligible for cash rebate

The way UOB One Card's rebate scheme works is unique, and it fits best for people whose monthly spending is consistent. Cardholders earn one of three cashback rates based on their lowest monthly spend within a quarter. Those who spend at least S$2,000 each month and charge at least 5 transactions to their card earn the maximum S$300 cashback for that quarter, equal to up to 5% flat cashback on all purchases and S$1,200 in savings over a full year. This makes the card worth considering, given its high cashback

To optimise your cashback from UOB One Card, you must meet two criteria: reach the minimum monthly spend that is closest to your typical budget, and use the card at least 5 times per month. Apart from the quarterly cashback, you can also earn bonus cashback of up to S$100 per month: +5% for Dairy Farm Singapore, Grab, Shopee and select UOB Travel transactions (up to 10% total) and +1% on Singapore Power bills (up to 6% total). All electric bills are eligible for up to 5% rebate.

Regardless of your spend level, UOB One Card also grants additional cashback on the following select merchants:

UOB Travel transactions (excluding online and flight-only bookings)

Up to 10%

+5%

Utilities

Singapore Power transactions

Up to 6%

+1%

See card terms and conditions for a full list of qualifying merchants.

UOB One Card is not as good if your monthly spending varies a lot or falls too far away from the monthly minimums of S$500, S$1,000 and S$2,000. Because your cashback is based on the lowest monthly spend of the quarter, spending less than these figures reduces your cashback rate.

The closer your lowest monthly spend gets to the next tier, the more cashback you will miss out on until you reach that tier. For instance, spending just S$1 less than S$2,000 in any one month drops a cardholder's rebate from S$300 to S$100 for the whole quarter. The monthly cap on rebates doesn't exist for unlimited cashback cards like American Express True Cashback Card or miles-earning cards like Citi PremierMiles Visa Card.

Ultimately, UOB One Card is best for average consumers with a stable monthly spend of around S$2,000. While the annual fee of S$192.6 is only waived the first year, the rebate potential of UOB One Card offers an easy way to quickly and conveniently recoup the cost. This card is a great fit if you're more concerned with saving money than with miles, rewards, or vouchers.

How the UOB One Credit Card Rewards Program Works

Every 1 dollar of cashback earned is equal to S$1

Cash rebate is credited to the cardholder's account 1 month after the end of each quarter

Cash rebate earned must be used to offset future transactions

Cash rebate expires 2 calendar years from the quarter in which it was earned

Cashback is automatically forfeited and is non-transferable when an account is closed

Before You Apply: Caps, Minimums, and Exclusions

While we consider UOB One Card to be stronger than many other credit cards in Singapore, it does carry some limitations that you should keep in mind. First, know that this card's system gives you the cashback in quarterly installments, which means you'll only see the benefit appear in your account four times a year as opposed to every month.

Second, the fixed cashback amounts that you can earn each quarter max out at S$300, which is unlocked by spending S$2,000 and making at least 5 transactions each month. Since there's no added bonus for spending more than that, it's a good idea to start using a different card once you've reached the monthly spend requirement on UOB One Card.

Put together, these terms and conditions mean that UOB One Card is best-suited to people who naturally tend to spend the same amount month after month. Consistent spending will make it easier to hit the monthly spend requirements.

Keep in mind that the following credit card expenditures are ineligible for cash back or rebate with UOB One Card:

Cash advances; interest, fees and charges imposed by the bank, including late payment charges, interest charges, and annual or monthly fees; balance and/or funds transfers to or from the card account; any credit card transaction that was subsequently cancelled, voided or reversed; monthly instalments under 0% Instalment Payment Plan and SmartPay; wire transfers/remittances

Quasi cash remote stored value load merchant rentals & money transfers; stored value card purchase & load; transactions made with the following: AXS, CITYINDEX, EZ-LINK, FLASHPAY, NETSFLASHPAY, MONEYBOOKERS, OANDA ASIA PAC, PAYPAL (Plus500, Bizconsulta & more), PLUS500, Saxo Cap Mkts, SKR, SKRILL, TRANSIT, TRANSITLINK, IGMARKETS, MYEZLINK & more

Direct marketing for insurance services and insurance sales/underwriting; member financial institution merchandise and services; quasi cash financial institutions merchandise and services; quasi cash merchant non-financial institutions (foreign currency, non-fiat currency, cryptocurrency); securities brokers & dealers; school (elementary and secondary); colleges, universities, professional schools and junior colleges; correspondence schools; business and secretarial schools; trade and vocational schools; charitable, social service, religious, and/or political organisations; court costs including alimony and child support; fines, bail & bond payments; tax payments; postal services (government only); intra-government purchases (government only); all other government services

Nondurable goods; real estate agents & managers, rentals; cleaning, maintenance and janitorial services or property management; quasi cash truck stop transactions; gambling & betting (lottery tickets, casino, gaming chips, off-track betting, wagers at race tracks)

Finally, remember that any cashback that you earn using UOB One Card is applied forward: in other words, the cashback only offsets future spending and will not apply as statement credit on the spending that originally generated the cashback. Also, cashback you accumulate expires 2 calendar years after the quarter in which you earn it or immediately when you close your credit card account.

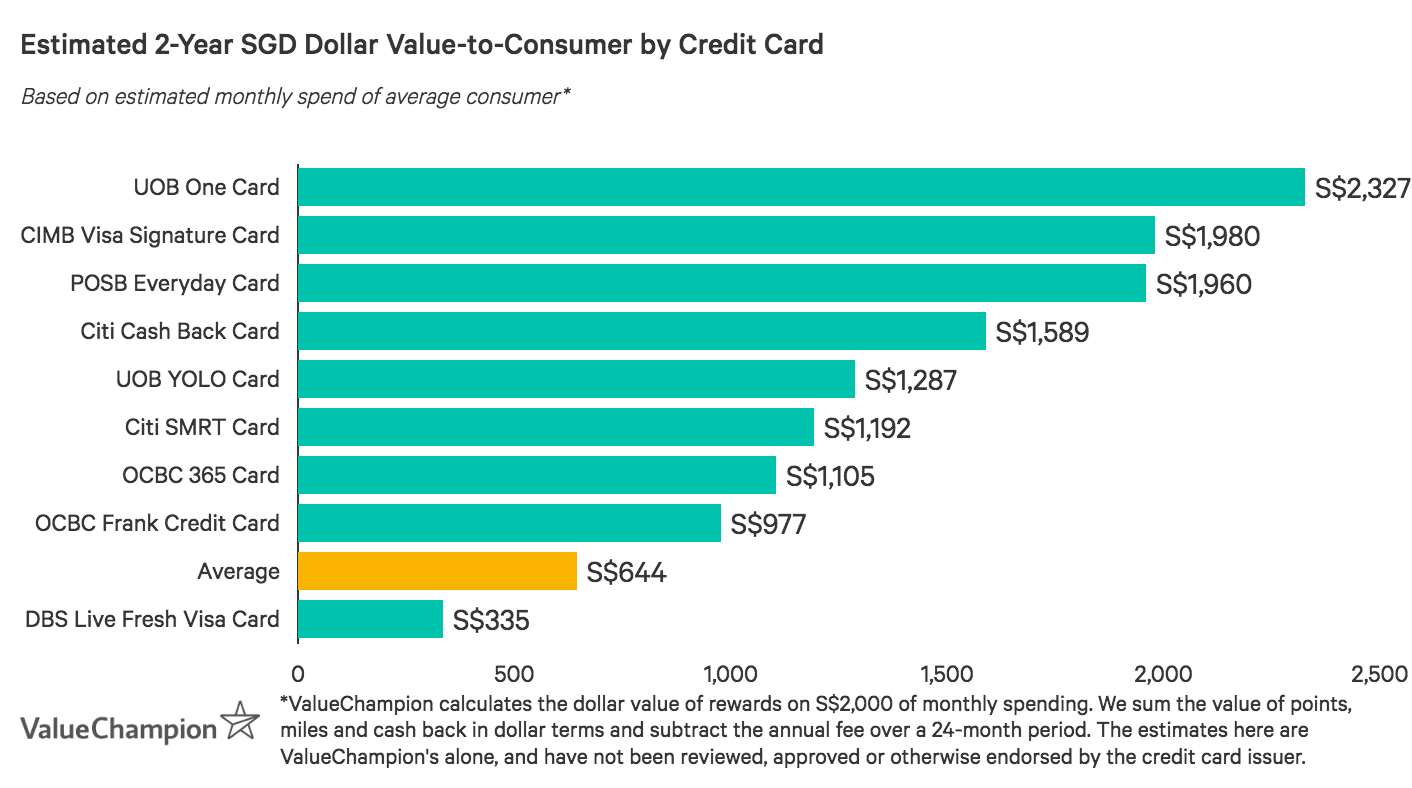

How UOB One Credit Card Compares to Other Cards

Read our comparisons of UOB One Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need. In case you would like to compare the rewards value of this card or any other card yourself, go to our RealValue Credit Card Rewards Calculator to compare the cards' rewards, promotions, rates and other unique features.

UOB One Credit Card vs Maybank FC Barcelona Card vs American Express True Cashback Card vs Standard Chartered Unlimited Cashback Credit Card

{"items":["\u003Cdiv class=\"AffiliateBannerMobile--root\"\u003E\n \u003Cdiv class=\"AffiliateBanner--root \"\u003E\n \u003Cdiv class=\"AffiliateBanner--image\"\u003E\n \u003Cdiv class=\"ShortcodeImage--root \"\u003E\n \u003Cdiv class=\"ShortcodeImage--image-container\"\u003E\n \u003Ca class=\"js-event-click\" data-eventcategory=\"Affiliate credit_cards: Maybank FC Barcelona Visa Signature Card - Image\" data-eventlabel=\"Maybank FC Barcelona Visa Signature Card\" rel=\"nofollow noopener\" target=\"_blank\" title=\"Maybank FC Barcelona Visa Signature Card\" href=\"\/redirect\/credit_cards\/63?link=https%3A%2F%2Faffiliate.valuechampion.sg%2Fredirect%3Flink%3Dhttps%253A%252F%252Fapply.maybank.com.sg%252Fpackage%252Fcob%252Findex.htm%253Fsc%253Dinfo6\"\u003E\u003Cimg alt=\"Maybank FC Barcelona Visa Signature Card\" class=\"ShortcodeImage--image lazyload\" style=\"width: 200px;\" data-src=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/maybank-fcb-visasig\" src=\"\/\/res.cloudinary.com\/valuechampion\/image\/upload\/e_blur:1000,q_1,f_auto\/referral_logos\/sg\/credit_cards\/maybank-fcb-visasig\" data-srcset=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/maybank-fcb-visasig 1x, https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_2.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/maybank-fcb-visasig 2x\"\u003E\u003C\/a\u003E\n \n \u003C\/div\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003Cdiv class=\"AffiliateBanner--link\"\u003E\n \u003Cdiv class=\"AffiliateButton--root \"\u003E\n \u003Ca data-eventcategory=\"Affiliate credit_cards: Maybank FC Barcelona Visa Signature Card - Button\" data-eventlabel=\"Maybank FC Barcelona Visa Signature Card\" class=\"ShortcodeLink--root AffiliateButton--button js-event-click\" rel=\"nofollow noopener\" target=\"_blank\" title=\"Maybank FC Barcelona Visa Signature Card\" href=\"\/redirect\/credit_cards\/63?link=https%3A%2F%2Faffiliate.valuechampion.sg%2Fredirect%3Flink%3Dhttps%253A%252F%252Fapply.maybank.com.sg%252Fpackage%252Fcob%252Findex.htm%253Fsc%253Dinfo6\"\u003EApply Now \u003C\/a\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003Cdiv class=\"AffiliateBanner--link\" style=\"margin-top: 10px;\"\u003E\n \u003Cdiv class=\"AffiliateButton--root \"\u003E\n \u003Ca data-eventcategory=\"Affiliate Alternate credit_cards: Maybank FC Barcelona Visa Signature Card - Button\" data-eventlabel=\"Maybank FC Barcelona Visa Signature Card\" class=\"ShortcodeLink--root AffiliateButton--button AffiliateButton--alternate js-event-click\" rel=\"nofollow\" title=\"Maybank FC Barcelona Visa Signature Card\" href=\"https:\/\/apply.maybank.com.sg\/cards\/index.htm#\/creditcardstart?sc=acq6&_ga=2.157255611.1666599270.1615254429-326056336.1588140604\"\u003EForeigners\u003C\/a\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003C\/div\u003E\n\u003C\/div\u003E\n\u003Cdiv class=\"AffiliateBannerDesktop--root\"\u003E\n \u003Cdiv class=\"AffiliateBanner--root \"\u003E\n \u003Cdiv class=\"AffiliateBanner--image\"\u003E\n \u003Cdiv class=\"ShortcodeImage--root \"\u003E\n \u003Cdiv class=\"ShortcodeImage--image-container\"\u003E\n \u003Ca class=\"js-event-click\" data-eventcategory=\"Affiliate credit_cards: Maybank FC Barcelona Visa Signature Card - Image\" data-eventlabel=\"Maybank FC Barcelona Visa Signature Card\" rel=\"nofollow noopener\" target=\"_blank\" title=\"Maybank FC Barcelona Visa Signature Card\" href=\"\/redirect\/credit_cards\/63?link=https%3A%2F%2Faffiliate.valuechampion.sg%2Fredirect%3Flink%3Dhttps%253A%252F%252Fapply.maybank.com.sg%252Fpackage%252Fcob%252Findex.htm%253Fsc%253Dinfo6\"\u003E\u003Cimg alt=\"Maybank FC Barcelona Visa Signature Card\" class=\"ShortcodeImage--image lazyload\" style=\"width: 200px;\" data-src=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/maybank-fcb-visasig\" src=\"\/\/res.cloudinary.com\/valuechampion\/image\/upload\/e_blur:1000,q_1,f_auto\/referral_logos\/sg\/credit_cards\/maybank-fcb-visasig\" data-srcset=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/maybank-fcb-visasig 1x, https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_2.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/maybank-fcb-visasig 2x\"\u003E\u003C\/a\u003E\n \n \u003C\/div\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003Cdiv class=\"AffiliateBanner--link\"\u003E\n \u003Cdiv class=\"AffiliateButton--root \"\u003E\n \u003Ca data-eventcategory=\"Affiliate credit_cards: Maybank FC Barcelona Visa Signature Card - Button\" data-eventlabel=\"Maybank FC Barcelona Visa Signature Card\" class=\"ShortcodeLink--root AffiliateButton--button js-event-click\" rel=\"nofollow noopener\" target=\"_blank\" title=\"Maybank FC Barcelona Visa Signature Card\" href=\"\/redirect\/credit_cards\/63?link=https%3A%2F%2Faffiliate.valuechampion.sg%2Fredirect%3Flink%3Dhttps%253A%252F%252Fapply.maybank.com.sg%252Fpackage%252Fcob%252Findex.htm%253Fsc%253Dinfo6\"\u003EApply Now \u003C\/a\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003Cdiv class=\"AffiliateBanner--link\" style=\"margin-top: 10px;\"\u003E\n \u003Cdiv class=\"AffiliateButton--root \"\u003E\n \u003Ca data-eventcategory=\"Affiliate Alternate credit_cards: Maybank FC Barcelona Visa Signature Card - Button\" data-eventlabel=\"Maybank FC Barcelona Visa Signature Card\" class=\"ShortcodeLink--root AffiliateButton--button AffiliateButton--alternate js-event-click\" rel=\"nofollow\" title=\"Maybank FC Barcelona Visa Signature Card\" href=\"https:\/\/apply.maybank.com.sg\/cards\/index.htm#\/creditcardstart?sc=acq6&_ga=2.157255611.1666599270.1615254429-326056336.1588140604\"\u003EForeigners\u003C\/a\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003C\/div\u003E\n\u003C\/div\u003E\n","\n\u003Cdiv class=\"AffiliateBannerMobile--root\"\u003E\n \u003Cdiv class=\"AffiliateBanner--root \"\u003E\n \u003Cdiv class=\"AffiliateBanner--image\"\u003E\n \u003Cdiv class=\"ShortcodeImage--root \"\u003E\n \u003Cdiv class=\"ShortcodeImage--image-container\"\u003E\n \u003Cimg alt=\"American Express True Cashback Card\" class=\"ShortcodeImage--image lazyload\" style=\"width: 200px;\" data-src=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/amex-true-cashback\" src=\"\/\/res.cloudinary.com\/valuechampion\/image\/upload\/e_blur:1000,q_1,f_auto\/referral_logos\/sg\/credit_cards\/amex-true-cashback\" data-srcset=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/amex-true-cashback 1x, https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_2.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/amex-true-cashback 2x\"\u003E\n \n \u003C\/div\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003C\/div\u003E\n\u003C\/div\u003E\n\u003Cdiv class=\"AffiliateBannerDesktop--root\"\u003E\n \u003Cdiv class=\"AffiliateBanner--root \"\u003E\n \u003Cdiv class=\"AffiliateBanner--image\"\u003E\n \u003Cdiv class=\"ShortcodeImage--root \"\u003E\n \u003Cdiv class=\"ShortcodeImage--image-container\"\u003E\n \u003Cimg alt=\"American Express True Cashback Card\" class=\"ShortcodeImage--image lazyload\" style=\"width: 200px;\" data-src=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/amex-true-cashback\" src=\"\/\/res.cloudinary.com\/valuechampion\/image\/upload\/e_blur:1000,q_1,f_auto\/referral_logos\/sg\/credit_cards\/amex-true-cashback\" data-srcset=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/amex-true-cashback 1x, https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_2.0,f_auto,h_1600,q_auto,w_200\/v1\/referral_logos\/sg\/credit_cards\/amex-true-cashback 2x\"\u003E\n \n \u003C\/div\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003C\/div\u003E\n\u003C\/div\u003E\n","\n\u003Cdiv class=\"AffiliateBannerMobile--root\"\u003E\n \u003Cdiv class=\"AffiliateBanner--root \"\u003E\n \u003Cdiv class=\"AffiliateBanner--image\"\u003E\n \u003Cdiv class=\"ShortcodeImage--root \"\u003E\n \u003Cdiv class=\"ShortcodeImage--image-container\"\u003E\n \u003Ca class=\"js-event-click\" data-eventcategory=\"Affiliate credit_cards: Standard Chartered Simply Cash Credit Card - Image\" data-eventlabel=\"Standard Chartered Simply Cash Credit Card\" rel=\"nofollow noopener\" target=\"_blank\" title=\"Standard Chartered Simply Cash Credit Card\" href=\"\/redirect\/credit_cards\/61?link=https%3A%2F%2Faffiliate.valuechampion.sg%2Fredirect%3Flink%3Dhttps%253A%252F%252Fpixel.ekosconnect.com%252Fpx%253Fa%253D239%2526c%253D86%2526p%253D68%2526ev%253Daffclk%2526k%253D81a52a31ba11dd91\"\u003E\u003Cimg alt=\"Standard Chartered Simply Cash Credit Card\" class=\"ShortcodeImage--image lazyload\" style=\"width: 200px;\" data-src=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/singapore_credit_cards\/simply-cash-prev-unlimited-cashback-card.png\" src=\"\/\/res.cloudinary.com\/valuechampion\/image\/upload\/e_blur:1000,q_1,f_auto\/singapore_credit_cards\/simply-cash-prev-unlimited-cashback-card.png\" data-srcset=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/singapore_credit_cards\/simply-cash-prev-unlimited-cashback-card.png 1x, https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_2.0,f_auto,h_1600,q_auto,w_200\/v1\/singapore_credit_cards\/simply-cash-prev-unlimited-cashback-card.png 2x\"\u003E\u003C\/a\u003E\n \n \u003C\/div\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003Cdiv class=\"AffiliateBanner--link\"\u003E\n \u003Cdiv class=\"AffiliateButton--root \"\u003E\n \u003Ca data-eventcategory=\"Affiliate credit_cards: Standard Chartered Simply Cash Credit Card - Button\" data-eventlabel=\"Standard Chartered Simply Cash Credit Card\" class=\"ShortcodeLink--root AffiliateButton--button js-event-click\" rel=\"nofollow noopener\" target=\"_blank\" title=\"Standard Chartered Simply Cash Credit Card\" href=\"\/redirect\/credit_cards\/61?link=https%3A%2F%2Faffiliate.valuechampion.sg%2Fredirect%3Flink%3Dhttps%253A%252F%252Fpixel.ekosconnect.com%252Fpx%253Fa%253D239%2526c%253D86%2526p%253D68%2526ev%253Daffclk%2526k%253D81a52a31ba11dd91\"\u003EApply Now \u003C\/a\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003C\/div\u003E\n\u003C\/div\u003E\n\u003Cdiv class=\"AffiliateBannerDesktop--root\"\u003E\n \u003Cdiv class=\"AffiliateBanner--root \"\u003E\n \u003Cdiv class=\"AffiliateBanner--image\"\u003E\n \u003Cdiv class=\"ShortcodeImage--root \"\u003E\n \u003Cdiv class=\"ShortcodeImage--image-container\"\u003E\n \u003Ca class=\"js-event-click\" data-eventcategory=\"Affiliate credit_cards: Standard Chartered Simply Cash Credit Card - Image\" data-eventlabel=\"Standard Chartered Simply Cash Credit Card\" rel=\"nofollow noopener\" target=\"_blank\" title=\"Standard Chartered Simply Cash Credit Card\" href=\"\/redirect\/credit_cards\/61?link=https%3A%2F%2Faffiliate.valuechampion.sg%2Fredirect%3Flink%3Dhttps%253A%252F%252Fpixel.ekosconnect.com%252Fpx%253Fa%253D239%2526c%253D86%2526p%253D68%2526ev%253Daffclk%2526k%253D81a52a31ba11dd91\"\u003E\u003Cimg alt=\"Standard Chartered Simply Cash Credit Card\" class=\"ShortcodeImage--image lazyload\" style=\"width: 200px;\" data-src=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/singapore_credit_cards\/simply-cash-prev-unlimited-cashback-card.png\" src=\"\/\/res.cloudinary.com\/valuechampion\/image\/upload\/e_blur:1000,q_1,f_auto\/singapore_credit_cards\/simply-cash-prev-unlimited-cashback-card.png\" data-srcset=\"https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_1.0,f_auto,h_1600,q_auto,w_200\/v1\/singapore_credit_cards\/simply-cash-prev-unlimited-cashback-card.png 1x, https:\/\/res.cloudinary.com\/valuechampion\/image\/upload\/c_fit,dpr_2.0,f_auto,h_1600,q_auto,w_200\/v1\/singapore_credit_cards\/simply-cash-prev-unlimited-cashback-card.png 2x\"\u003E\u003C\/a\u003E\n \n \u003C\/div\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003Cdiv class=\"AffiliateBanner--link\"\u003E\n \u003Cdiv class=\"AffiliateButton--root \"\u003E\n \u003Ca data-eventcategory=\"Affiliate credit_cards: Standard Chartered Simply Cash Credit Card - Button\" data-eventlabel=\"Standard Chartered Simply Cash Credit Card\" class=\"ShortcodeLink--root AffiliateButton--button js-event-click\" rel=\"nofollow noopener\" target=\"_blank\" title=\"Standard Chartered Simply Cash Credit Card\" href=\"\/redirect\/credit_cards\/61?link=https%3A%2F%2Faffiliate.valuechampion.sg%2Fredirect%3Flink%3Dhttps%253A%252F%252Fpixel.ekosconnect.com%252Fpx%253Fa%253D239%2526c%253D86%2526p%253D68%2526ev%253Daffclk%2526k%253D81a52a31ba11dd91\"\u003EApply Now \u003C\/a\u003E\n\u003C\/div\u003E\n \u003C\/div\u003E\n \u003C\/div\u003E\n\u003C\/div\u003E"],"offsetPercentage":20}

Maybank FC Barcelona Visa Signature Card, American Express True Cashback Card and Standard Chartered Unlimited Cashback Credit Card are decent alternatives for UOB One Card. These cards provide unlimited cashback of about 1.5% on nearly all purchases without a minimum spend requirement. Given this, these cards may be better than UOB One Card for consumers who spend at least S$6,000 per month. Overall, Maybank FC Barcelona Card stands out for its slightly higher rebate of 1.6% and an easy annual fee waiver, Amex True Cashback Card comes with the renowned customer service, and SC Unlimited Cashback Card offers a 0% instalment payment plan for up to 36 months and doubles as a SimplyGo Card.

Ultimately, UOB One Card benefits average consumers who spend of S$2,000/month, while only the highest spenders can earn greater cashback with Amex True Cashback Card or SC Unlimited Cashback Credit Card.

Great fit for budgets between S$2,000 and S$8,000/month

Easy, low-maintenance cashback

Cons

Lacks travel perks

Doesn't fit highly specialised spend behaviors

HSBC Advance customers can maximise cashback rewards with flat-rate HSBC Advance Credit Card. Banking customers earn 3.5% cashback, 2.5% base rate + 1% bonus rate, for spending at least S$2,000 and depositing a minimum of S$2,000 per month in fresh funds and charging at least five transactions to their account. With this bonus rate, monthly cashback is capped at S$300 (compared to UOB One Card's S$300/quarter), which is S$3,600 per year in savings.

Failing to deposit S$2,000 in fresh funds monthly will result in rate drop to 2.5% when monthly spend is S$2,000 and up, and just 1.5% for monthly spend below S$2.000. The monthly cap is only S$70/month (S$210/quarter vs UOB's S$300), and an annual fee of S$192.60 applies. For customers who cannot deposit fresh funds on a monthly basis to earn the bonus cashback rate, UOB One Card is likely a better alternative.

UOB EVOL Card is a great fit for young adults looking to maximise cashback on most expenses. Cardholders receive 8% cashback on any purchases made either online or via mobile payment apps like Apple Pay and Google Pay. UOB EVOL Cardholders can also earn cashback after reaching a minimum spend of just S$600, with no quarterly contingencies like the UOB One Card.

However, UOB EVOL Card limits your monthly rewards to S$60, or S$180 per quarter - far lower than the S$300 quarterly rebate on UOB One Card. UOB Evol Card is still a versatile choice for lower budgets concentrated in online purchases and contactless payments, but those who spend at least S$2,000 per month can earn far more from UOB One Card.

Methodology: How We Review Credit Cards

At ValueChampion, we analyse nearly every credit card available in Singapore. Our process involves measuring the value of each card's rewards rates, bonuses, and benefits versus its spending requirements, monthly rewards caps and annual fees.

Most cards earn miles or cashback at rates that change depending on what type of spending your budget includes. Different categories also have different monthly caps on their rewards potential. Some cards also require you spend a minimum amount every month before they earn rewards.

Applying all of these factors to a typical budget allows us to estimate how much the credit card will earn in rewards. Annually recurring fees and bonuses are also considered in our calculation. We use our results to evaluate how effective the card is compared to other options.

To try our calculations for yourself, use our RealValue Rewards Calculator and find out how easy it is to compare the rewards potential of every credit card in Singapore.

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.

Keep up with our news and analysis.

Stay up to date.

{"endpoint":"\/newsletter\/subscribe","style":"blue","title":"Keep up with our news and analysis.","version":"sidebar"}

Advertiser Disclosure: ValueChampion is a free source of information and tools for consumers. Our site may not feature every company or financial product available on the market. However, the guides and tools we create are based on objective and independent analysis so that they can help everyone make financial decisions with confidence. Some of the offers that appear on this website are from companies which ValueChampion receives compensation. This compensation may impact how and where offers appear on this site (including, for example, the order in which they appear). However, this does not affect our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services

We strive to have the most current information on our site, but consumers should inquire with the relevant financial institution if they have any questions, including eligibility to buy financial products. ValueChampion is not to be construed as in any way engaging or being involved in the distribution or sale of any financial product or assuming any risk or undertaking any liability in respect of any financial product. The site does not review or include all companies or all available products.