What is Fire and Home Insurance

Property insurance was the first form of insurance that was offered to consumers, which is not surprising since your home is one of your most valuable assets. In Singapore, there are two main forms of property insurance that serve to protect your home: fire and home insurance. If you are looking to learn about these insurance plans, our guide below will explain their differences, what type of home coverage you may need and which policy will work best for you.

Table of Contents

- Defining Fire vs. Home Insurance

- Why You May Need Home Insurance

- Policy Structure

- How to find the best home insurance policy

Fire Insurance vs. Home Insurance

Even though fire and home insurance may seem like they cover the same things, there are some key differences between the two types of insurance plans. Unlike home insurance, fire insurance provides basic coverage for water, smoke and fire damage suffered to interior and exterior structures in the event of a fire, explosion, force majeure, riots and strikes and malicious intent. It does not cover your personal belongings or renovations. While it is a compulsory purchase for HDB owners who have an HDB mortgage or loan, fire insurance is optional if you live in a landed property and not necessary if you live in a condo or private apartment (your apartment block's management will usually have a master fire insurance plan). HDB owners purchase their policies from FWD at a fixed 5-year rate.

Sum Insured for Fire Insurance (FWD)

| Flat Type | Sum Insured |

|---|---|

| 1-Room | S$29,000 |

| 2-Room/2-Room Flexi/Studio Apt. | S$48,700 |

| 3-Room | S$60,400 |

| 4-Room/S1 | S$82,000 |

| 5-Room/S2/3-Generation | S$97,300 |

| Executive/Multi-Generation | S$106,200 |

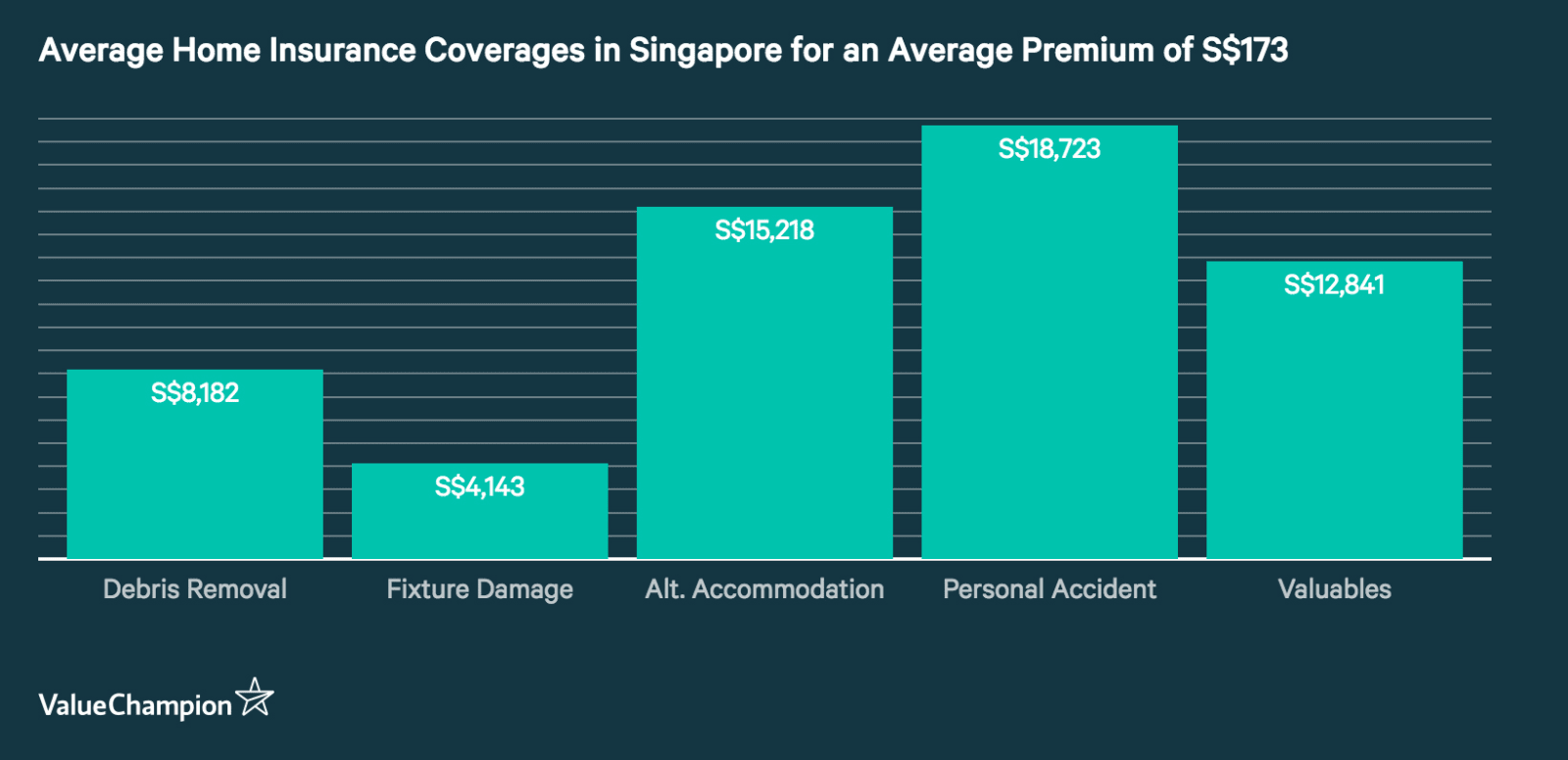

On the other hand, home insurance, or home contents insurance, is an optional form of insurance that you can purchase to supplement or replace fire insurance. It is much more comprehensive than fire insurance and protects you against losses sustained to your personal belongings, interior/exterior house fixtures, renovations and provides liability and medical coverage. You will also find sub-limits for more specific coverages, including landslide damage, mover's damage, loss of valuables such as artwork, hospital expenses and even pet protection. You can expect to pay anywhere from S$50 to over S$300 depending on the policy you get.

Why You May Need Home Insurance

Even though home contents insurance is optional, it is highly advisable to consider purchasing it either to supplement your fire insurance policy or to comprehensively protect a landed property. Not only will you be protected from damage due to natural disasters, fire, water leaks, moving, and burglary, but you will also be covered for medical and accident expenses due to injuries that happen in your home, and liability expenses in the event someone else injures themselves on your property and damages to your renovations.

Most importantly however, home contents insurance will protect your furniture, valuables, and electronics and provide cover temporary relocation if your home becomes completely uninhabitable. Simply having fire insurance alone may not be enough, as it doesn't cover you for these risk events and leaves you vulnerable to out of pocket expenses for damaged or lost assets. If protecting your belongings is a priority, home contents insurance may be a valuable purchase.

Home Insurance Policy Structure

Home insurance benefits are usually separated into 4 separate categories: building or renovation coverage, contents coverage, liability coverage and medical/accident coverage, with sub-limits within those categories detailing specific coverage. Insurers offer a couple of different plans to choose from, differing in scope and total coverage. You can either get all the coverages bundled under one premium, or buy a flexible plan where you choose a custom amount for either renovation/building coverage or contents coverage. If you are opting for the flexible plan, your premium will depend on a set rate per certain amount of coverage (i.e. .05% of an x amount of coverage). There are also options to purchase additional contents, liability, medical and renovation coverage.

Furthermore, insurers make a distinction between "all-risks" and "insured/named-perils" plans. The difference between the two comes from the scope of coverage. While an insured perils policy covers only what is explicitly stated in your policy (water damage, fire, vehicular impact, lightning, burglary, etc.), all-risks policies will cover a wider range of expenses, including accidental damage. However, both policies carry exceptions, so you should read the policy wording to make sure you know exactly what kind of coverage you are getting.

Notable Exclusions and Disclaimers

Home insurance policies will not cover damage that comes from faulty workmanship, natural wear and tear or willful malicious property damage by the policyholder. Usually, insurers will not pay for losses incurred on an unoccupied property. Additionally, some insurers will not pay for damage incurred to musical instruments or property damaged by leaking water from household appliances such as dishwashers and washing machines.

For contents protection, it is imperative that you have receipts for all of the assets you want to protect and that you read the policy wording to see the per item coverage coverage limits. This is because insurers only offer a set amount of coverage for individual items. If you want protection for an item that exceeds a plan's limit, insurers will either have a relevant form attached to their policy application or you can speak to your insurer to ask for an exception to their limit. Additionally, the total cost of what you can insure is what it would take to rebuild your property—not your property's market value.

How to Find the Best Home Insurance Plan

If you are looking to purchase a home insurance policy but don't know where to start, choosing based on your property could be a good jumping off point. For instance, if you live in a landed property, you would most likely benefit the most from a comprehensive home insurance plan that provides both building and contents coverage. If you are a tenant in an HDB flat, then you may benefit from a home insurance plan focused on contents coverage only. If you live in a condo or private apartment building, you will benefit from contents and/or renovation coverage depending on your budget and what you want coverage for.

Similarly, if you want to protect certain valuables or insuring your pet is important to you, then you can look for policies with generous coverage amounts in those areas. Insurance companies want to make their products and out so it is highly likely you can find an insurance policy that caters to whatever you want protection for. If you are still stuck and are feeling overwhelmed with the amount of home insurance policies available, our guides can make finding the right policy for you much easier.

Read More:

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.