Who Should Buy Personal Accident Insurance?

Optional insurance policies can often lead to confusion regarding their necessity. While it may seem like getting as much protection as possible can decrease the risk of financial loss, getting too much protection can end up in redundant coverage and be unnecessarily expensive. Personal accident (PA) insurance is an optional insurance policy that some may find beneficial, and others may simply not need it. Below, you'll find a guide on how to know whether or not you'll benefit from getting a PA plan.

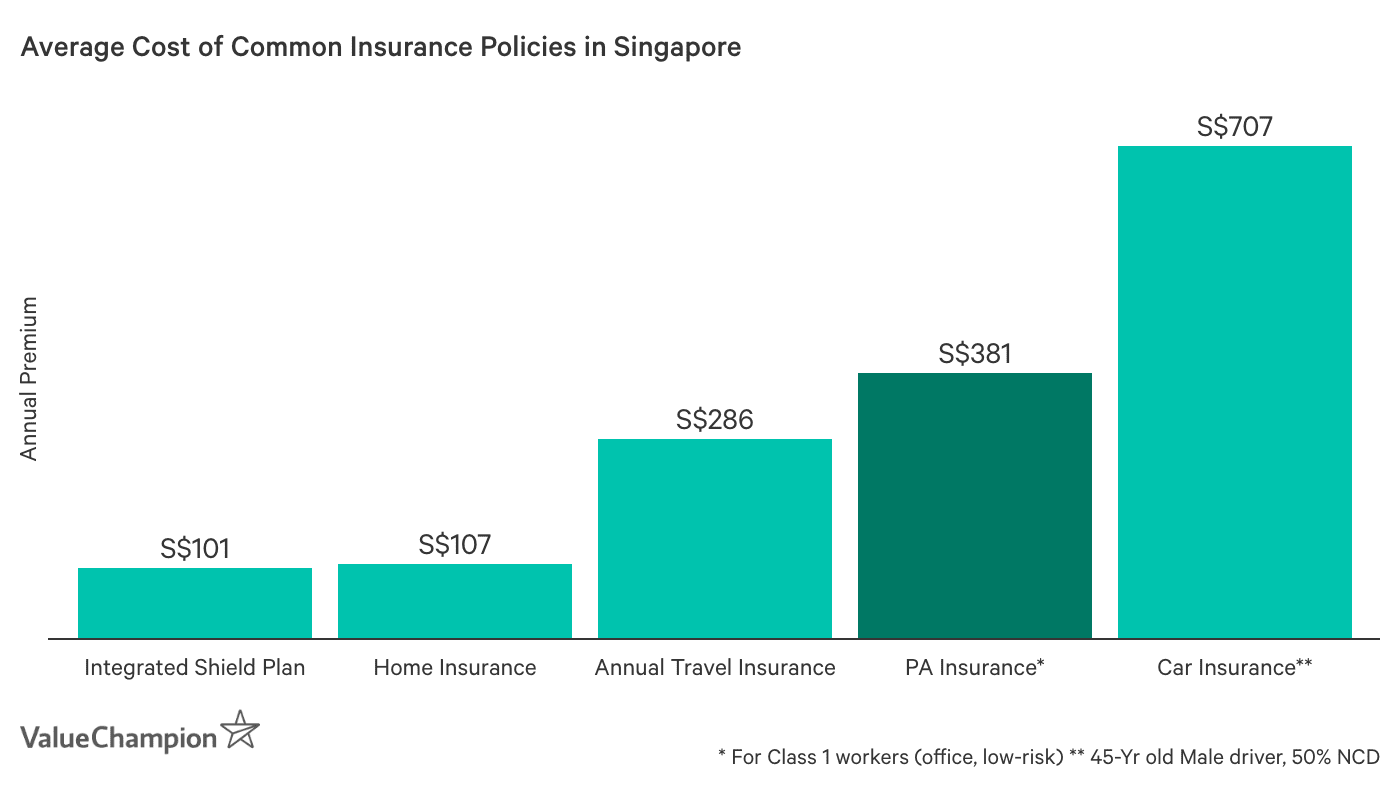

Table of Contents

When to Get Personal Accident Insurance

Those who are self-employed, elderly or participate in risky activities may get the most benefit from PA plans. First, those who are self-employed don't have the benefit of having company-sponsored insurance. This means that if these individuals were to get into a serious accident, they would have to pay for medical bills and lose wages by taking time off work. Personal accident insurance offers protection against both of those cases, as it offers coverage for accident-related medical bills and a weekly income benefit to make up for the lost wages.

Second, if your lifestyle involves any kind of risk (e.g. you play contact sports every weekend) you may benefit from a PA plan as well. However, in these cases it is necessary to read the policy wording to make sure your occupation and activities are covered. This lifestyle risk can include retirement. Those who are getting close to the retirement age may benefit from a personal accident policy, as they will receive financial protection from slips and falls that can result in life-threatening injuries and long-term rehabilitation. However, you should make sure you know the age limits of the plan you are purchasing, as some plans cover until age 70 and others until age 85.

Personal accident insurance is also available for your children and can be a suitable option if you notice they are accident-prone. As kids become more active, accidents are bound to happen, whether it's a fall in the playground or an accident at school. A PA policy can complement any medical insurance your child might have to offset the financial costs of these accidents. Furthermore, some policies may cover against common childhood diseases like Hand-Foot-Mouth disease.

When To Skip Personal Accident Insurance

If you either have workers compensation or you have a low-risk lifestyle and can get by with a good travel insurance policy, you most likely won't need personal accident insurance. For example, your worker's compensation should provide coverage for any accidents acquired on the job and your travel insurance policy will cover injuries and accidents while abroad. Adding a personal accident policy on top of these policies may result in extra costs and duplicate coverage.

Certain occupations provide accident insurance or worker's compensation as part of your benefits package. This means a personal accident plan may end up being redundant. For instance, Singapore's Work Injury Compensation insurance provides protection for manual laborers and non-manual workers that earn less than S$2,600 per month. It offers similar benefits to PA plans, including coverage for lost wages, medical expenses and lump sum payments for death and permanent disability. In fact, this may be a better option for these workers, since PA plans may not cover all types of manual labor. Similarly, if you work as a military or police officer, you will be eligible for the MINDEF & MHA's Group Personal Accident (GPA) insurance. It provides coverage for death, disability, medical expenses, home rehabilitation expenses and other benefits you'd find in traditional PA plans.

You can consider skipping personal accident insurance if you are not the sole income-earner in your household. Provided that your family will be financially secure if you have to be out of work for a while, you can easily save that money for an emergency budget or on a good life insurance policy. Furthermore, you can consider skipping personal accident insurance if the riskiest activities you do are when you travel. In this case, a robust travel insurance policy may suffice. Not only will it provide coverage for accidents, injuries and death while travelling, but it will also cover lost baggage, trip cancellations and flight delays. Furthermore, you may already have enough coverage with your life insurance plan.

Comparison of Personal Accident Insurance and Travel Insurance Benefits

| Benefits & Coverage | Avg. Personal Accident Plan | Avg. Travel Insurance Plan |

|---|---|---|

| Emergency Evacuation | S$500,000-S$1 Million | S$1,113,171 |

| Death & Permanent Disability Coverage | S$314,286 | S$338,293 |

| Temporary Disability Coverage | Yes | No |

| Medical Coverage | S$5,339 (Outpatient) | S$849,381 (Hospitalisation & Specialist) |

| 24/7 Worldwide Assistance | Yes | Yes |

Before Purchase, Analyse Your Current Coverage and Budget

Those who are on the fence about getting a personal accident plan may find it beneficial to go over all of their current insurance coverage (including potential travel insurance they may buy in the future). There may be instances where you think you have enough coverage, and then find out that you actually have a gap that PA plans can fill. For instance, while some medical insurance policies don't cover outpatient expenses, PA plans do. This ends up saving you money if you get into an accident that only requires an outpatient visit to get an MRI, CAT scan or other examinations. On the other hand, you may find you have adequate medical expense, death & accident coverage and can go without a separate PA plan.

Furthermore, it is important to make sure this plan will fit into your budget. While in most cases, PA plans are one of the more affordable insurance options, they can still end up making a dent in your budget. In fact, you can over S$1,000 per year for a policy if you are looking for a high coverage plan or work in a risky occupation. This is a considerable sum, especially if you are already paying for a plethora of other insurance policies. Thus, budget constrained consumers may fare better with saving a little bit here and there for an emergency fund as opposed to buy insurance policies.

Read More:

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.