POSB Everyday Savings Account: Best for Low Income Adults

POSB Everyday Savings Account: Best for Low Income Adults

ValueChampion Rating ![]()

Pros

- Low income consumers and full-time NSFs

- People looking to avoid added fees and requirements

- Individuals who cannot maintain a S$500+ balance

Cons

- Salaried adults with steady income

- Young adults under 26 years old

- People who can maintain a balance of at least S$500

Low income adults will find no better savings account than POSB Everyday Account. In fact, a variety of people can benefit–NSFs, individuals younger than 26 years old or older than 60 years old, on public assistance, or opening their first POSB account online are all exempt from the minimum balance requirement of S$500. Additionally, there's no minimum initial deposit requirement, making the account easy to open. Consumers earn 0.05% p.a. interest on their entire balance, which is somewhat competitive for those with low balances looking to avoid fees. Overall, POSB Everyday Savings Account is set to benefit those who maintain balances below S$500, including full-time NSFs (who for the most part, aren't offered fee waivers elsewhere).

| Pros | Cons |

|---|---|

|

|

| Promotion: None currently available | |

| Pros & Cons |

|---|

Pros:

|

Cons:

|

What Makes POSB Everyday Savings Account Stand Out

If you're a low income adult likely to maintain a balance below S$500, look no further than POSB Everyday Savings Account. To begin with, there's no minimum initial deposit requirement, making it fairly easy to open an account. Additionally, while there's a S$500 minimum balance requirement, fall-below fees are waived for a variety of individuals: people younger than 21 years old or older than 60 years old, public assistance recipients, people opening their first POSB account online, and full-time NSFs. These features, overall, make POSB Everyday Savings Account quite accessible, making it one of the best savings accounts in Singapore for many.

POSB Everyday Savings Account Interest Rates

| Rate Type | Details & Requirements | Interest Rate |

|---|---|---|

| Base Rate |

| 0.05% p.a. on entire balance |

| Max Effective Interest Rate: | 0.05% p.a. (at any balance) | |

| POSB Everyday Savings Account Interest Rates |

|---|

Base Rate: No requirements

|

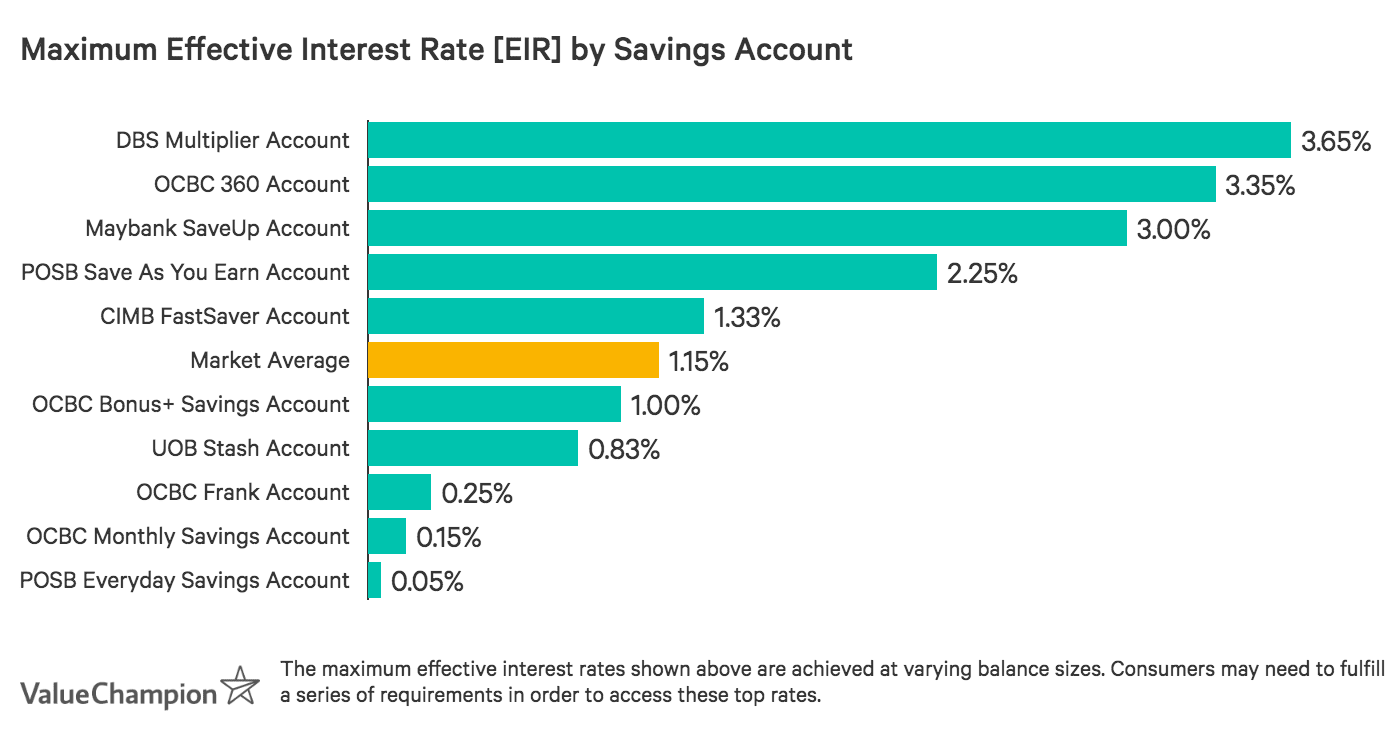

Nonetheless, it's important to note that account holders earn just 0.05% p.a. interest on their entire balance. This rate aligns with the market norm for a base rate–however, most accounts offer bonuses that elevate earnings beyond this base. POSB Everyday Savings Account does not offer bonus rates, which means individuals with moderate-to-high balance sizes will earn more elsewhere.

Consumers with lower incomes or who aren't capable of maintaining consistent balances can greatly benefit from POSB Everyday Account, however. Most savings accounts have minimum balance requirements of S$500+ and charge fall-below fees of S$2 for the month. In most cases, the fees associated with falling below the minimum are greater than any interest accrued, resulting in a nett loss. With POSB Everyday Account's fee-waiver, however, it's possible to avoid such loss while continuing to accrue interest.

Impact of Fall-Below Fees on Monthly Interest Earned for Low Income Consumers

| Account Details | POSB Everyday | RHB High Yield | OCBC Frank (26yo+) |

|---|---|---|---|

| Minimum Balance Requirement | (waived) | S$500 | S$1,000 |

| Fall-Below Fee | N/A | S$10 | S$2 |

| Base Interest Rate (% p.a.) | 0.05% | 0.08% | 0.20% |

| Interest Earned (on S$450 balance) | S$0.02 | S$0.03 | S$0.08 |

| Nett After Fee | S$0.02 | -(S$9.97) | -(S$1.92) |

Ultimately, while young adults have access to no-fee alternatives (like OCBC Frank Account), low income adults are best off with POSB Everyday Savings Account. Not only is it possible to avoid extra costs regardless of balance size, it's also possible to continue earning interest along the way.

POSB Everyday Savings Account Details & Requirements

| Details & Requirements | |

|---|---|

| Minimum Age Requirement | 16 |

| Minimum Initial Deposit | S$0 |

| Minimum Balance Requirement | S$500 |

| Fall-Below Fee | S$2 (Waived if less than 21 or greater than 60 years old, recipient of public assistant, full-time National Service man or if it’s the applicant's 1st account with POSB) |

How Does POSB Everyday Savings Account Compare to Other Accounts?

Read our comparisons of POSB Everyday Savings Account with other savings accounts and learn what makes each account unique in its own way. We compare and contrast each account to help you to identify which best suits your needs.

POSB Everyday Savings Account v. OCBC Frank Savings Account

- Min. Age Requirement

- 16

- Min. Initial Deposit

- S$0

- Min. Balance Requirement

- S$0 if younger than 26 years old, S$1,000 for 26+

If you're a young adult thinking of starting your first savings account–but don't want to worry about requirements and fees–OCBC Frank Savings Account may be the right option for you. Consumers as young as 16 years old can apply, and there are no minimum initial spend requirements. Even further, account holders under 26 years old are exempt from minimum balance requirements and associated fall below fees. Overall, OCBC Frank Savings Account is both low-risk and low-maintenance for young adults.

OCBC Frank Account is also easy to manage and understand. Consumers earn 0.10% p.a. on the 1st S$25k in their account, 0.20% p.a. on the next S$25k, and 0.05% p.a. on amounts beyond S$50k (essentially, the base rate). These rates are quite competitive compared to other no-fee, requirement-free accounts. Nonetheless, this account loses its edge for low income individuals above 26 years old; such individuals might instead consider POSB Everyday Savings Account.

| Rate Type | Details & Requirements | Interest Rate |

|---|---|---|

| Base Rate |

| 0.10% p.a. on 1st S$25k |

| 0.20% p.a. on next S$25k | ||

| 0.05% p.a. above S$50k | ||

| Max Effective Interest Rate: | 0.20% p.a. (at S$50k balance) | |

| OCBC Frank Interest Rates |

|---|

Base Rate: No requirements (varies according to band of balance)

|

| Max EIR: 0.20% p.a. (at S$50k balance) |

POSB Everyday Savings Account v. CIMB StarSaver Savings Account

- Min. Age Requirement

- 16

- Min. Initial Deposit

- S$1,000

- Min. Balance Requirement

- N/A

CIMB StarSaver Savings Account is likely the easiest starter account for young professionals, minimising risk while also providing competitive interest rates. Account holders earn a flat 0.80% p.a. on their entire balance, regardless of size, which is substantially higher than the standard market standard base of 0.05% p.a. Additionally, there is no minimum balance requirement and therefore no fall-below fees, making the account both low risk and low maintenance. Nonetheless, only balances above S$1k earn interest, and an initial deposit of S$1k+ is required. For these reasons, very low income individuals may find CIMB StarSaver Account a bit less accessible. In this case, POSB Everyday Savings Account, which has no initial deposit and no minimum balance requirements, may be a better alternative.

| Rate Type | Details & Requirements | Interest Rate |

|---|---|---|

| Base Rate |

| 0.80% p.a. |

| Max Effective Interest Rate: | 0.80% p.a. (at any balance) | |

| CIMB StarSaver SA Interest Rates |

|---|

Base Rate: No requirements (applies to entire balance)

|

| Max EIR: 0.80% p.a. (at any balance) |

POSB Everyday Savings Account v. RHB High Yield

- Min. Age Requirement

- 18

- Min. Initial Deposit

- S$1,000

- Min. Balance Requirement

- S$1,000

RHB Yield Savings Account is an easy-to-open option with a very simple interest rate structure. Consumers can open an account without making a minimum initial deposit, and subsequently can earn up to 0.91% p.a. EIR (though this is achieved at S$100k balance). A lower balance, below S$10k, earns at 0.08% p.a., which is still higher than the 0.05% p.a. base rate offered by some competitors. Nonetheless, there is a S$500 minimum balance requirement paired with a very high fall-below fee of S$10. At this cost level, falling below S$500 would actually lead to a substantial loss for account holders. As a result, those who are unlikely to maintain a balance of S$500+ would definitely benefit more from POSB Everyday Savings Account.

| Rate Type | Details & Requirements | Interest Rate |

|---|---|---|

| Base Rate |

| 1.05% p.a. on 1st S$50k |

| 1.55% p.a. on next S$25k | ||

| 2.00% p.a. on next S$25k | ||

| 0.60% p.a. beyond S$100k | ||

| Max Effective Interest Rate: | 1.41% p.a. (at S$100k balance) | |

| RHB High Yield SA Interest Rates |

|---|

Base Rate: No requirements (rate varies according to band of balance)

|

| Max EIR: 1.41% p.a. (at S$100k balance) |