Best Credit Cards in Singapore 2024

Selecting the right credit card to maximise your monthly earnings is deeply dependent on your spend behaviour – both how much you tend to spend, as well as what you spend on. Our research team analysed 100+ of Singapore's top credit cards to make your decision easier, identifying those with the highest value-to-consumer across a variety of metrics (minimum requirements, earnings caps, rewards rates & more).

- UOB One: Highest flat rebate on the market, earn up to $300/qtr

- POSB Everyday: Rebates up to 10% in Singapore

- Maybank Family & Friends: 8% cashback with S$800 min. spend requirement

- DBS Altitude: Earn 5 miles per S$1 spend on online flight & hotel transactions (capped at S$5,000 per month) and overseas spend (at point-of-sale), earn S$1 = 2 miles on overseas spend (online transactions), earn S$1 = 1.2 miles on local spend. All miles earned through this card is via DBS Points and thus will never expire.

- Citi PMV: 45,000 Welcome Citi Miles with S$9,000 spend in 3 mo

- KrisFlyer UOB: 3mi/S$1 on dining, transport, shopping & travel

- UOB PRVI Miles: Fee-Waiver + 20k bonus miles, 2.4 miles per $1 overseas

- OCBC 365: 6% rebate on dining, 3% rebate on groceries, utilities and travel, Visa Concierge Services

- Maybank Horizon: Market-leading 3.2 miles per S$1 select local spend

- Unlimited Cards: Uncapped rebates up to 1.6%

- HSBC Advance: Up to 3.5% cashback capped at S$300/month

- Citi Prestige: Unlimited lounge access, bonus hotel nights & more

- SC Visa Infinite X: Bonus S$6,000 w/ S$200k fund placement

- DBS Woman's World: Get up to 10X DBS Points (or 20 miles) for online purchases, 3X DBS Point (or 6 miles) for overseas purchases and 1X DBS Point (or 2 miles) for other purchases

- OCBC Cashflo: Rewards for split payments, no processing fee

- OCBC Frank: Up to 6% rebate for FX, online and mobile purchases, low S$600 min. spend requirement

- UOB EVOL: Rebates on online and contactless spend with easy fee-waiver

- Citi SMRT: 5% everyday rebates w/S$500 min spend

- Citi Lazada: Up to 4 miles per S$1 spend on Lazada

Best Credit Cards for Cashback:

Best Credit Cards for Air Miles: Best Credit Cards with No Annual Fee: Best Credit Cards for High-Income Individuals: Best Credit Cards with 0% Interest Instalment Plans: Best Credit Cards for Young Adults:How We Compare the Best Credit Cards by Dollar Value

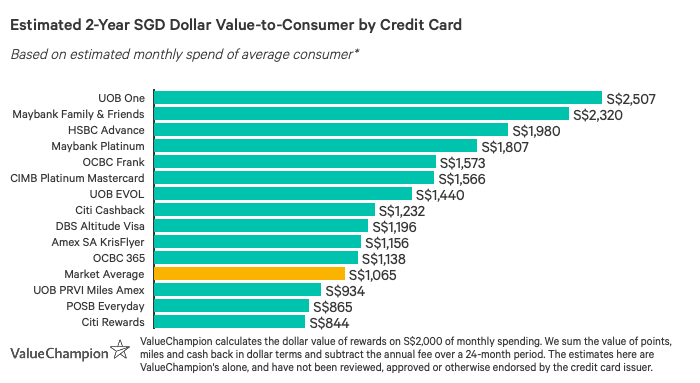

Based on an average monthly spend of S$2,000, we analysed the best credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits, which is why we've selected different cards for different needs. We also weigh the intangible benefits such as ease of use, free travel insurance and airport lounge access that are valuable but difficult to quantify.

Best Cashback Credit Cards in Singapore

Cashback cards are straightforward and easy-to-use, and rewards can offset your monthly bill.

UOB One Credit Card: Highest Flat Rebate Card

| |

If you have a consistent budget, you may be able to maximise earnings on all spend with UOB One Card. Cardholders earn 5% rebate on all purchases if they spend S$2k/month for 3 months in a row), boosted to 10% on Grab transactions and 6% on recurring bills. This quarterly system is beneficial for those with stable spending, but people with lower spend–or who are inconsistent from month to month–will earn somewhat less. Spending S$1k/month or S$500k/month for the quarter earns 3.33% rebate, up to S$100/quarter or S$50/quarter respectively. Nonetheless, all cardholders can benefit from UOB SMART$ Rebate Programme, which supplement cashback with additional savings and discounts.

| |

|

|

If you have a consistent budget, you may be able to maximise earnings on all spend with UOB One Card. Cardholders earn 5% rebate on all purchases if they spend S$2k/month for 3 months in a row), boosted to 10% on Grab transactions and 6% on recurring bills. This quarterly system is beneficial for those with stable spending, but people with lower spend–or who are inconsistent from month to month–will earn somewhat less. Spending S$1k/month or S$500k/month for the quarter earns 3.33% rebate, up to S$100/quarter or S$50/quarter respectively. Nonetheless, all cardholders can benefit from UOB SMART$ Rebate Programme, which supplement cashback with additional savings and discounts.

|

POSB Everyday Card: Rebates on Essentials + SimplyGo/ABT

| |

If you're interested in high promotional rebates on daily essentials, consider POSB Everyday Card. Cardholders can earn high rates ranging up to 10% rebate even, in categories such as online food delivery, dining, groceries, transport, personal care and recurring bills. While these rates change, they typically reward everyday purchases. Higher rebates require hitting a Personalised Spend Goal which is based on individual spending behaviour and assigned by POSB.

| |

|

|

If you're interested in high promotional rebates on daily essentials, consider POSB Everyday Card. Cardholders can earn high rates ranging up to 10% rebate even, in categories such as online food delivery, dining, groceries, transport, personal care and recurring bills. While these rates change, they typically reward everyday purchases. Higher rebates require hitting a Personalised Spend Goal which is based on individual spending behaviour and assigned by POSB.

|

Maybank Family & Friends MasterCard: Top Rebates in Singapore & Malaysia

| |

Maybank Family & Friends Card offers a great way for average and lower spenders to maximise rewards on local or regional spend. Cardholders earn 5% rebate on fast food & food delivery, groceries, transport, petrol, data communications/online TV streaming & more after S$500 minimum spend, or 8% with S$800 minimum spend. Even more, consumers can max out rewards at S$80/month with just S$1k monthly spend. This spend level would not only earn S$960/year, but also qualify for a fee-waiver: the S$180.0 fee is waived 3 years, and then with S$12k annual spend. Rewards rates are limited to spend in Singapore & Malaysia, but there are nearly no merchant restrictions making the card easy and convenient to use.

| |

|

|

Maybank Family & Friends Card offers a great way for average and even lower spenders to maximise rewards on local or regional spend. Cardholders earn 5% rebate on fast food & food delivery, groceries, transport, petrol, data communications/online TV streaming & more after S$500 minimum spend, or 8% with S$800 minimum spend.

|

Best Miles Credit Cards in Singapore

Frequent travellers can benefit from the perks and high miles rewards rates of these travel cards.

DBS Altitude Visa Card: Affordable Perks w/ Fee-Waiver

| |

DBS Altitude Visa Card stands out as one of the most affordable travel credit cards that offers both high miles rates as well as luxury perks. Cardholders enjoy 1.2 miles per S$1 local spend, 2 miles overseas, and 3 miles for online travel bookings–and miles earned never expire. Even better, consumers receive 2 free lounge visits annually as part of the perks. The already reasonable S$194.4 fee is waived with S$25,000 annual spend, making DBS Altitude Visa a great card for average travellers seeking affordable perks.

| |

|

|

DBS Altitude Visa Card stands out as one of the most affordable travel credit cards that offers both high miles rates as well as luxury perks. Cardholders enjoy 1.2 miles per S$1 local spend, 2 miles overseas, and 3 miles for online travel bookings–and miles earned never expire. Even better, consumers receive 2 free lounge visits annually as pert of the travel perks. The already reasonable S$194.40 fee is waived with S$25,000 annual spend, making DBS Altitude Visa a great card for average travellers seeking affordable perks.

|

Citi PremierMiles Visa Card: Yearly Bonus Miles + Free Lounge Access

| |

Travellers who want to enjoy great travel perks without having to pay a high annual fee may want to consider Citi PremierMiles Visa Card. Consumers earn 2 miles per S$1 spend overseas and 1.2 miles locally, which is reasonably competitive. Citi PMV Card stands out, however, by offering perks like 2 free lounge visits annually and complimentary travel insurance, plus up to a bonus of 45,000 miles upon sign-up and 10,000 yearly renewal miles. Many travel cards that offer luxury benefits and bonus miles charge annual fees of S$400+. Citi PMV Card, on the other hand, costs just S$192.6, which is waived the 1st year. Ultimately, average consumers looking for an affordable travel credit card with extra perks should definitely consider Citi PMV Card.

| |

|

|

Travellers who want to enjoy great travel perks without having to pay a high annual fee may want to consider Citi PremierMiles Visa Card. Consumers earn 2 miles per S$1 spend overseas and 1.2 miles locally, which is reasonably competitive. Citi PMV Card stands out, however, by offering perks like 2 free lounge visits annually and complimentary travel insurance, plus up to a bonus of 45,000 miles upon sign-up and 10,000 yearly renewal miles. Many travel cards that offer luxury benefits and bonus miles charge annual fees of S$400+. Citi PMV Card, on the other hand, costs just S$192.6, which is waived the 1st year. Ultimately, average consumers looking for an affordable travel credit card with extra perks should definitely consider Citi PMV Card.

|

KrisFlyer UOB Credit Card: Miles for SIA-Loyal Millennials

| |

If you're a young, frequent traveller and don't mind committing to a single airline, KrisFlyer UOB Card may be the best option for you. Cardholders earn 3 miles per S$1 spend with SIA brands (SIA, SilkAir, Scoot, KrisShop) and 1.2 miles per S$1 on general local and overseas purchases. However, those who spend at least S$500 on SIA within a year receive a boost to 3 miles per S$1 on transport, dining, online shopping & travel bookings. These rates are amongst the highest on the market and fit well with a millennial or young adult lifestyle.

| |

|

|

If you're a young, frequent traveller and don't mind committing to a single airline, KrisFlyer UOB Card may be the best option for you. Cardholders earn 3 miles per S$1 spend with SIA brands (SIA, SilkAir, Scoot, KrisShop) and 1.2 miles per S$1 on general local and overseas purchases. However, those who spend at least S$500 on SIA within a year receive a boost to 3 miles per S$1 on transport, dining, online shopping & travel bookings. These rates are amongst the highest on the market and fit well with a millennial or young adult lifestyle.

|

UOB PRVI Miles American Express Card: Best for Rapid Miles Accumulation

| |

With UOB PRVI Miles American Express Card, above-average spenders can enjoy some of the highest overseas rates on the market–plus bonus miles–while potentially even earning an annual fee waiver. In terms of rewards, cardholders earn 1.4 miles per S$1 spend locally, 2.4 miles overseas and 6 miles with major hotels and airlines. Not only can consumers enjoy perks like free airport transfers and travel insurance, they can also avoid the S$256.8 fee with S$50k annual spend (approx. S$4,167/mo). At this spend level, cardholders even receive 20,000 bonus miles. Overall, travellers with above-average annual spend can rapidly accrue miles with UOB PRVI Miles Card.

| |

|

|

With UOB PRVI Miles American Express Card, above-average spenders can enjoy some of the highest overseas rates on the market–plus bonus miles–while potentially even earning an annual fee waiver. In terms of rewards, cardholders earn 1.4 miles per S$1 spend locally, 2.4 miles overseas and 6 miles with major hotels and airlines. Not only can consumers enjoy perks like free airport transfers and travel insurance, they can also avoid the S$256.8 fee with S$50k annual spend (approx. S$4,167/mo). At this spend level, cardholders even receive 20,000 bonus miles. Overall, travellers with above-average annual spend can rapidly accrue miles with UOB PRVI Miles Card.

|

Best Credit Cards with No Annual Fee

The following credit cards offer easy waivers so you can avoid paying an annual fee.

OCBC 365 Card: Rebates on Everyday Essentials

| |

OCBC 365 Card offers a great no-fee way to earn cashback on daily purchases. Cardholders earn up to 6% rebates on dining and 3% on groceries, land transport, online travel bookings and recurring electricity and telco bills. There are no merchant restrictions (unlike competitors) and rewards are capped at a lofty S$80/month. Another perk is that cardholders can enjoy a fee waiver with S$10k annual spend–thats just S$833/month. This spend level also meets minimum spend requirements, ensuring top rewards rates. Overall, OCBC 365 Card is definitely one of the best everyday options with a fee-waiver.

| |

|

|

OCBC 365 Card offers a great no-fee way to earn cashback on daily purchases. Cardholders earn up to 6% rebates on dining and 3% on groceries, land transport, online travel bookings and recurring electricity and telco bills. There are no merchant restrictions (unlike competitors) and rewards are capped at a lofty S$80/month. Another perk is that cardholders can enjoy a fee waiver with S$10k annual spend–thats just S$833/month. This spend level also meets minimum spend requirements, ensuring top rewards rates. Overall, OCBC 365 Card is definitely one of the best everyday options with a fee-waiver.

|

Maybank Horizon Visa Signature: High Local Miles Rewards

| |

Maybank Horizon Visa Signature Card is an exceptional option for people who sometimes travel and want to earn miles, but primarily maintain a local budget. Cardholders earn 3.2 miles per S$1 local spend on dining, taxis & Grab, petrol, and hotel bookings with Agoda. Spend on air tickets, travel packages and overseas earns a still-impressive 2 miles per S$1. These rates allow the average consumer to rapidly accrue miles when at home, as well as when they plan for vacations. Even better, the S$180.0 annual fee is waived 3 years, then with S$18k annual spend. Ultimately, Maybank Horizon is one of the most affordable travel cards and offers market-leading miles rates for local spenders.

| |

|

|

Maybank Horizon Visa Signature Card is an exceptional option for people who sometimes travel and want to earn miles, but primarily maintain a local budget. Cardholders earn 3.2 miles per S$1 local spend on dining, taxis & Grab, petrol, and hotel bookings with Agoda. Spend on air tickets, travel packages and overseas earns a still-impressive 2 miles per S$1. These rates allow the average consumer to rapidly accrue miles when at home, as well as when they plan for vacations. Even better, the S$180.0 annual fee is waived 3 years, then with S$18k annual spend. Ultimately, Maybank Horizon is one of the most affordable travel cards and offers market-leading miles rates for local spenders.

|

Best Credit Cards for High-Income Earners

Wealthy individuals can benefit from these cards' unlimited rewards and luxury perks.

Citi Cash Back+ Card: Highest Unlimited Flat Rebate Rate

| |

If you're a high spender with a budget of S$7,000+/month, you're most likely to maximise cashback from your purchases with Citi Cash Back+ Card. Cardholders earn an impressive 1.6% rebate with no minimum spend requirement or earning limit–which is ideal for affluent consumers who typically feel constrained by cards with earnings caps. While there aren't many extra perks or privileges, Citi Cash Back+ Card's rewards rate is higher than the 1.5% offered by most comparable credit cards. As a result, Citi Cash Back+ is the best option for people with large budgets who are focused primarily on earning to their full potential.

| |

|

|

If you're a high spender with a budget of S$7,000+/month, you're most likely to maximise cashback from your purchases with Citi Cash Back+ Card. Cardholders earn an impressive 1.6% rebate with no minimum spend requirement or earning limit–which is ideal for affluent consumers who typically feel constrained by cards with earnings caps. While there aren't many extra perks or privileges, Citi Cash Back+ Card's rewards rate is higher than the 1.5% offered by most comparable credit cards. As a result, Citi Cash Back+ is the best option for people with large budgets who are focused primarily on earning to their full potential.

|

Standard Chartered Simply Cash Credit Card: Uncapped Rebates Worldwide

| |

Capped cashback credit cards can prevent high-spenders from reaching their full rewards potential. Standard Chartered Simply Cash Credit Card offers a great alternative, providing an unlimited 1.5% cashback on all spend, with no caps or minimum requirements. The S$192.6 fee is waived for 2 years, allowing consumers to earn without worrying too much about added costs.

| |

|

|

Capped cashback credit cards can prevent high-spenders from reaching their full rewards potential. Standard Chartered Simply Cash Credit Card offers a great alternative, providing an unlimited 1.5% cashback on all spend, with no caps or minimum requirements. The S$192.6 fee is waived for 2 years, allowing consumers to earn without worrying too much about added costs.

|

American Express True Cashback Card: Unltd Rewards + Amex Perks

|

|

American Express True Cashback Card is perhaps the absolute best unlimited cashback credit card currently on the market. Cardholders earn a flat 1.5% rebate on spend locally and overseas, boosted to 3% for the first 6 months (up to S$150 total bonus). In addition to this stand-out welcome deal, consumers have access to special perks like American Express Selects, card-specific discounts and free travel insurance. Many of these deals relate to wedding expenses, making Amex True Cashback Card a great option for those planning their big day.

| |

|

|

|---|

|

|

American Express True Cashback Card is perhaps the absolute best unlimited cashback credit card currently on the market. Cardholders earn a flat 1.5% rebate on spend locally and overseas, boosted to 3% for the first 6 months (up to S$150 total bonus). In addition to this stand-out welcome deal, consumers have access to special perks like American Express Selects, card-specific discounts and free travel insurance. Many of these deals relate to wedding expenses, making Amex True Cashback Card a great option for those planning their big day.

|

Maybank FC Barcelona Visa Signature: Unlimited Local Cashback

| |

High-spenders can definitely benefit from Maybank FC Barcelona Visa Signature Card, which offers the highest unlimited flat cashback rate on the market for local spend. Cardholders enjoy 1.6% rebate on local spend, compared to 1.5% with other unlimited cards. In addition, the card comes with perks like discounts at FC Barcelona stores, the chance to win free game tickets and free travel insurance. Overseas spend earns the equivalent of 0.8% cashback, however, so Maybank FC Barcelona Card is best fit for people with high local budgets who travel infrequently.

| |

|

|

High-spenders can definitely benefit from Maybank FC Barcelona Visa Signature Card, which offers the highest unlimited flat cashback rate on the market for local spend. Cardholders enjoy 1.6% rebate on local spend, compared to 1.5% with other unlimited cards. In addition, the card comes with perks like discounts at FC Barcelona stores, the chance to win free game tickets and free travel insurance. Overseas spend earns the equivalent of 0.8% cashback, however, so Maybank FC Barcelona Card is best fit for people with high local budgets who travel infrequently.

|

OCBC 90°N Card: Cashback + Miles for High Spenders

| |

OCBC 90°N Card is incredibly unique in allowing high overseas spenders to fully maximise cashback, with the option to switch to miles without expiration dates. First of all, purchases are rewarded in Travel$. Each Travel$ can be redeemed for the equivalent of S$0.01 cash rebate or 1 air mile. As such, cardholders opting for cashback rewards earn an unlimited 1.3% rebate locally and 2.1% overseas. This overseas rate is higher than that offered by any other unlimited cashback card, and there are no minimum spend requirements to earn at this rate. The closest cashback competitor offers 2% rebate overseas and requires a S$2k monthly minimum spend.

On a final note, OCBC 90°N cardholders can also enjoy a few perks and privileges. Cardholders receive 10,000 Travel$ yearly–equivalent to S$100 cash rebate or 10,000 air miles–which go a long way to offset the S$180.00 annual fee. Overall, affluent individuals looking for unlimited rewards–both in cashback and miles–should definitely consider OCBC 90°N Card. | |

|

|

OCBC 90°N Card is incredibly unique in allowing high overseas spenders to fully maximise cashback, with the option to switch to miles without extra redemption fees or expiration dates. First of all, purchases are rewarded in Travel$. Each Travel$ can be redeemed for the equivalent of S$0.01 cash rebate or 1 air mile. As such, cardholders opting for cashback rewards earn an unlimited 1.2% rebate locally and 2.1% overseas. This overseas rate is higher than that offered by any other unlimited cashback card, and there are no minimum spend requirements to earn at this rate. The closest cashback competitor offers 2% rebate overseas and requires a S$2k monthly minimum spend.

On a final note, OCBC 90°N cardholders can also enjoy a few perks and privileges. Cardholders receive 10,000 Travel$ yearly–equivalent to S$100 cash rebate or 10,000 air miles–which go a long way to offset the S$192.6 annual fee. In addition, consumers can access 1,000+ lounges worldwide at a discounted US$32/person, through Mastercard Airport Experiences. Overall, affluent individuals looking for unlimited rewards–both in cashback and miles–should definitely consider OCBC 90°N Card. |

HSBC Advance Card: Rebates for Affluent Advance Customers

| |

HSBC Advance Card provides an opportunity to earn up to S$1,500 in annual rebates with just S$3,570/monthly spend–which is great for higher spenders seeking cashback. Cardholders can earn up to 3.5% flat rebate with S$2k/month spend (2.5% if below) and up to S$125/month in rewards, as long as they are current Advance customers. Such customers are also exempt from the annual fee. Non-Advance customers earn lower rates, have a lower cap, and must pay a fee. As a result, it's worth checking out an Advance account. Thereafter, HSBC Advance Card may just be the best flat rate rebate credit card on the market for above-average spenders.

| |

|

|

HSBC Advance Card provides an opportunity to earn up to S$1,500 in annual rebates with just S$3,570/monthly spend–which is great for higher spenders seeking cashback. Cardholders can earn up to 3.5% flat rebate with S$2k/month spend (2.5% if below) and up to S$125/month in rewards, as long as they are current Advance customers. Such customers are also exempt from the annual fee.

|

Citi Prestige MasterCard: Best for Exclusive Luxury Perks

|

|

If luxury perks are your number one priority when travelling, look no further than Citi Prestige MasterCard. From unlimited airport lounge access to free bonus hotel nights, free limo transfers, golfing privileges, free travel insurance & more, consumers can enjoy the utmost convenience and comfort when they travel. Even more, cardholders receive top rates of 1.3 miles per S$1 local spend and 2 miles overseas.

| |

|

|

|---|

|

|

If luxury perks are your number one priority when travelling, look no further than Citi Prestige MasterCard. From unlimited airport lounge access to free bonus hotel nights, free limo transfers, golfing privileges, free travel insurance & more, consumers can enjoy the utmost convenience and comfort when they travel. Even more, cardholders receive top rates of 1.3 miles per S$1 local spend and 2 miles overseas, plus an annual bonus of up to 30% based on the tenure of their relationship with Citibank.

|

Standard Chartered Visa Infinite X: Biggest Sign Up Bonus for the Wealthy

| |

Standard Chartered Visa Infinite X Card offers affluent consumers one of the absolute best sign-on bonuses across all travel cards on the market. New cardholders who place S$300k fresh funds in a Priority Banking account and maintain this amount for 3 months receive an incredible 100,000 KrisFlyer miles–worth approximately S$10k when redeemed for business or first class tickets. Those who can place S$800k in funds receive 150,000 bonus miles (worth S$15k), and Priority Private Banking customers who place S$1.5m+ receive a total of 300,000 miles (worth S$30k). These bonuses far exceed any other offering on the market and easily offset the (albeit expensive) S$695.5 non-waivable fee.

| |

|

|

Standard Chartered Visa Infinite X Card offers affluent consumers one of the absolute best sign-on bonuses across all travel cards on the market. New cardholders who place S$300k fresh funds in a Priority Banking account and maintain this amount for 3 months receive an incredible 100,000 KrisFlyer miles–worth approximately S$10k when redeemed for business class tickets. Those who can place S$800k in funds receive 150,000 bonus miles (worth S$15k), and Priority Private Banking customers who place S$1.5m+ receive a total of 300,000 miles (worth S$30k). These bonuses far exceed any other offering on the market and easily offset the (albeit expensive) S$695.5 non-waivable fee.

|

Best Credit Cards for 0% Interest Instalment Plans

If you frequently make large purchases that you cannot pay for all at once, consider the cards below.

DBS Woman's World MasterCard: Miles for Online Shopping Spend

| |

DBS Woman’s World Card is another great option for people who shop online and make bigger purchases than they can immediately pay for. DBS Woman's World MasterCard accommodates interest-free instalments across up to 24 months with a waived processing fee (3%–5% of trasaction amount in the case of longer tenures). While purchases on the plan don't earn rewards, cardholders still avoid the extra costs inherent to most other shopping cards' plans.

| |

|

|

DBS Woman’s World Card is another great option for people who shop online and make bigger purchases than they can immediately pay for. DBS Woman's World MasterCard accommodates interest-free instalments across up to 24 months with a waived processing fee (3%–5% of trasaction amount in the case of longer tenures). While purchases on the plan don't earn rewards, cardholders still avoid the extra costs inherent to most other shopping cards' plans.

|

OCBC Cashflo Card: Rebates on Instalment Payments

|

|

If you're a frequent shopper who prefers to make payments in instalments, OCBC Cashflo Card is the best option for you. Cardholders can set a trigger system to automatically split transactions at a specific amount across 3–6 months. There's 0% interest on instalment payments, and the processing fee–typically 3%–5% of the transaction amount–is waived completely. The best part of OCBC Cashflo Card is that purchases made on the instalment plan are still eligible to earn rebates; no other credit card accommodates such earning.

| |

|

|

|---|

|

|

If you're a frequent shopper who prefers to make payments in instalments, OCBC Cashflo Card is the best option for you. Cardholders can set a trigger system to automatically split transactions at a specific amount across 3–6 months. There's 0% interest on instalment payments, and the processing fee–typically 3%–5% of the transaction amount–is waived completely. The best part of OCBC Cashflo Card is that purchases made on the instalment plan are still eligible to earn rebates; no other credit card accommodates such earning.

|

Best Credit Cards for Young Adults

These options are specially tailored to young adults who are looking for a first credit card.

OCBC Frank Card: No-Fee Rebates for Online Spend

|

|

Young adults seeking access to high rebates after just S$600 spend might want to check out OCBC Frank Card, which offers 6% on FX, online, and mobile contactless spend. Cardholders can earn an additional rate of 0.3% on all other purchases with no minimum spend requirement. Eligible online spend is quite comprehensive, ranging from online retail to travel bookings and more. The S$600 minimum spend requirement is one of the lowest on the market, and consumers who spend S$10k annually also earn an annual fee-waiver. These features make OCBC Frank Card especially accessible, and a great option for young adults with lower budgets who still want to earn at high rates.

| |

|

|

|---|

|

|

Young adults seeking access to high rebates after just S$600 spend might want to check out OCBC Frank Card, which offers 6% on FX, online, and mobile contactless spend. Cardholders can earn an additional rate of 0.3% on all other purchases with no minimum spend requirement. Eligible online spend is quite comprehensive, ranging from online retail to travel bookings and more. The S$600 minimum spend requirement is one of the lowest on the market, and consumers who spend S$10k annually also earn an annual fee-waiver. These features make OCBC Frank Card especially accessible, and a great option for young adults with lower budgets who still want to earn at high rates.

|

UOB EVOL Card: Cashback for Young Adults

| |

UOB EVOL Card offers young adults some of the highest rewards rates on the market for social weekend spending. Cardholders earn up to 8% cashback on online and contactless spend, and 0.3% cashback on all other spend. The minimum required spend to qualify for those rates is S$600 per month, and cashback cap is now S$20 per category, with a total of S$60 per month (S$720/year). UOB EVOL is also Southeast Asia's first bio-sourced card supporting green initiatives and offering a variety of sustainable deals.

| |

|

|

UOB EVOL Card offers young adults some of the highest rewards rates on the market for social weekend spending. Cardholders earn up to 8% cashback on online and contactless spend, and 0.3% cashback on all other spend. The minimum required spend to qualify for those rates is S$600 per month, and cashback cap is now S$20 per category, with a total of S$60 per month (S$720/year). UOB EVOL is also Southeast Asia's first bio-sourced card supporting green initiatives and offering a variety of sustainable deals.

|

Citi SMRT Card: Everyday Rebates + EZ-Link

|

|

One of the best credit cards for young professionals is Citi SMRT Card. This card has a low minimum monthly spend requirement of just S$500, which makes it extremely accessible. In terms of rewards, cardholders can earn up to 5% rebate on groceries, 5% on online shopping, and 5% on taxis and private-hire rides. Most of these categories are merchant-limited, but eligible vendors are quite popular: Sheng Siong, Grab, Gojek & many more. Finally, Citi SMRT Card is EZ-Link compatible and offers 5% rebate on Auto Top-Ups. When it comes down to it, young professionals can take advantage of the affordability and convenience of Citi SMRT Card to maximise cashback on daily spend.

| |

|

|

|---|

|

|

One of the best credit cards for young professionals is Citi SMRT Card. This card has a low minimum monthly spend requirement of just S$500, which makes it extremely accessible. In terms of rewards, cardholders can earn up to 5% rebate on groceries, 5% on online shopping, and 5% on taxis and private-hire rides. Most of these categories are merchant-limited, but eligible vendors are quite popular: Sheng Siong, Grab, Gojek & many more. Finally, Citi SMRT Card is EZ-Link compatible and offers 5% rebate on Auto Top-Ups. When it comes down to it, young professionals can take advantage of the affordability and convenience of Citi SMRT Card to maximise cashback on daily spend.

|

Citi Lazada Card: Miles on Lazada & Local Social Spend

|

|

With Citi Lazada Card, online shoppers who favour Lazada can easily accrue miles on their purchases, while also earning rewards for local social spend. Cardholders currently earn up to an incredible 4 miles (10pts) per S$1 spend on Lazada and have access to exclusive offers and discounts. Furthermore, shoppers receive a S$1.99 shipping rebate on purchases of S$50+ (up to 4x/month), which translates to up to 4% cashback on each purchase. The best part of Citi Lazada Card, however, is that consumers can enjoy respectable miles rates even when they're not shopping online. Cardholders earn 2 miles (5pts) per S$1 spend on local dining, entertainment, travel and transport, including Grab and Gojek rides (but not public transit).

| |

|

|

|---|

|

|

With Citi Lazada Card, online shoppers who favour Lazada can easily accrue miles on their purchases, while also earning rewards for local social spend. Cardholders currently earn up to an incredible 4 miles (10pts) per S$1 spend on Lazada and have access to exclusive offers and discounts. Furthermore, shoppers receive a S$1.99 shipping rebate on purchases of S$50+ (up to 4x/month), which translates to up to 4% cashback on each purchase. The best part of Citi Lazada Card, however, is that consumers can enjoy respectable miles rates even when they're not shopping online. Cardholders earn 2 miles (5pts) per S$1 spend on local dining, entertainment, travel and transport, including Grab and Gojek rides (but not public transit).

|

FAQs

Credit cards allow you to spend credit provided by the bank which you then have to repay. When you receive a credit card, your credit card limit is the maximum amount you have been approved for at the time of your application. This is highly dependent on your annual income. The great benefit of having a credit card is that, depending on the card itself, you can receive cashback on various purchases, discounts and perks on travel, dining, sports and other activities.

Depending on whether you are a student, an employed citizen or foreigner, the requirements you must meet to apply for a credit card vary. Typically, you are required to have a minimum annual salary of S$30,000, and to provide your payslips, most recent Tax Assessment and a copy of your NRIC. Read our guide to see specific details about these requirements.

With more than 100 credit cards available in Singapore, there is a credit card for every spending profile, income level and spending preference. Read our guide to find out which credit card is best for you.

- Cashback: Cashback credit cards, also known as rebate cards, are named as such because they reward spend with cash credit equal to a given percentage of the transaction amount. For example, a credit card may offer 5% cashback on dining. Using that credit card to pay a S$100 restaurant bill will then earn S$5 in cash credit rewards. Cashback credits usually cannot be redeemed as actual cash. Instead, rebates are usually automatically applied to the next monthly card statement to offset the bill. Because of this automation, cashback cards are quite simple to use. This makes them a great choice for credit card beginners or those seeking an easy-to-use card for daily essentials.

- Miles: Travel cards offer cardholders air miles for their purchases. Unlike cashback cards, rewards are usually differentiated by local vs. overseas spend, rather than by individual spend category (ie dining, transport, etc). Miles cards also typically offer higher rewards rates for purchases made in foreign currency. They also often offer luxury perks ranging from airport lounge access to free travel insurance, golfing privileges & more. For these reasons, travel cards are understandably popular with frequent travellers who can take advantage of miles rewards while enjoying luxury perks. Miles cards also rarely have minimum spend requirements or rewards earning caps, but they tend to have higher (and often non-waivable) annual fees.

- Points: The most typical kind of points credit cards is shopper cards. In this case, a certain number of points are earned per S$1 spend. However, points are often represented in miles form instead. For example, if S$1 spend earns 10 points, but cardholders can redeem 10 points for 4 miles on the rewards platform, it's safe to say that spending S$1 earns 4 miles. Points can also be redeemed for other rewards such as cash vouchers, merchandise, or credit with select vendors. However, the value gained from redeeming points for such items is typically lower that the redemption rate for miles.

Selecting the right credit card depends both on spending behaviour & a few key factors.

To begin with, nearly all credit cards have annual fees that can limit accessibility or diminish earnings. Travel credit cards tend to have higher annual fees, but some–alongside several rebate cards–offer condition-based fee-waivers. In these cases, a consumer can avoid paying the annual fee if they achieve a minimum spend by the end of the year (ie, waiver granted with S$12k annual spend). Many cards also waive the annual fee for the first 1-3 years after approval, making it easy to get started with the card upfront. Nonetheless, even if the annual fee seems achievable, it's possible to end up with a nett loss by the end of the year. In other words, if earnings from the credit card do not exceed the fee, you'll actually end up losing money. This is one reason it's important to pick a card that rewards your lifestyle.

In addition to annual fees, minimum spend requirements are important to consider. Minimum spend requirements reflect how much a cardholder must spend in order to unlock higher rewards rates as advertised. For example, a card might require S$800 minimum spend for the month in order to earn a 8% rebate that month. Spending even S$1 less than the minimum may result in the cardholder earning at a base rate of just 0.2%–0.3%, which translates to a massive loss in earnings potential. It's incredibly important to review a card's minimum spend requirement before applying. If you can't reliably achieve the given amount, you won't be able to access meaningful rewards rates.

Finally, make sure to review the overall rewards system structure. Choose a card that rewards categories you're most likely to spend on. Many cards cater to specific profiles (retail shoppers, travellers, everyday spenders & more) which can make selection a bit easier. It's essential to keep in mind that while high rewards rates can be very tempting, they won't prove beneficial unless you're likely to spend in the rewarded category.

Considering these factors together can help you to find a credit card that will truly maximise earnings for your spend.

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.