Best Whole Life Insurance in Singapore 2024

Whole life insurance can be useful if you are looking for comprehensive coverage for death, total & permanent disability and terminal illness. Our life insurance experts analysed dozens of whole life policies on the market to help you find out what options are available for your needs.

- Direct Purchase Whole Life Insurance: eTiQa, Income & more. Competitive DPI Whole Life products you can buy instantly online

- Traditional Whole Life Insurance: Singlife with Aviva, AIA & More. Traditional whole life insurance products ranging from investment linked policies to simple whole life coverage

- Savings/Endowment Insurance: Income, Manulife & Singlife with Aviva. Endowment plans are savings plans with a life insurance component attached. Annual rates are typically higher than regular savings accounts

How Do I Find the Best Whole Life Insurance Plan?

We researched all the life insurance products available in Singapore to help you discover what options you have available for whole life policies. As a rule of thumb, whole life insurance is best for those who are looking to leave a legacy for their children and grandchildren and need high levels of coverage. Alternatively, term life insurance is best for younger couples and individuals as it is cheaper than whole life insurance. As with all long-term commitments, you should discuss your preferred life insurance product with your financial advisor before purchasing.

- Traditional Whole Life Insurance: Singlife with Aviva, AIA & More

- Direct Purchase Whole Life Insurance: eTiQa, Income & more

- Savings/Endowment Insurance: Income, Manulife & Singlife with Aviva

How Do I Find the Best Whole Life Insurance Plan?

We researched all the life insurance products available in Singapore to help you discover what options you have available for whole life policies. As a rule of thumb, whole life insurance is best for those who are looking to leave a legacy for their children and grandchildren and need high levels of coverage. Alternatively, term life insurance is best for younger couples and individuals as it is cheaper than whole life insurance. As with all long-term commitments, you should discuss your preferred life insurance product with your financial advisor before purchasing.

Traditional Whole Life Insurance

A whole life insurance policy provides lifetime financial protection, sometimes offers a non-guaranteed bonus and can build up cash value over time. Upon death or terminal illness, your policy will pay out a lump sum plus any of the bonuses accumulated. If you want a whole life policy that you can purchase online without going through an intermediary, you can consider a Direct Purchase Whole Life insurance plan. Since DPIs are standardised, you can purchase up to S$200,000 in death and coverage.

| Plan: | Singlife with Aviva MyWholeLife Plan IV

|

Income Star Secure

|

AXA Life Treasure (II)

|

|---|---|---|---|

| ^Annual Premium | S$5,138 | S$4,915.20 | S$5,260 |

| Coverage | Death, TPD, Terminal Illness | Death, TPD, Terminal Illness | Death, TPD, Terminal Illness |

| Pay Premiums | Single, Between 5-25 years | 5-30 years up to age 64 | 10, 15, 20, 25 or 30 years |

| Features |

|

|

|

Because whole life insurance can be complicated, you'll need to consider a number of factors including your lifestyle, budget and financial needs.

First, you will need to figure out why you need whole life insurance over term life insurance. If you fall into the group of people who want financial protection for their dependents, want supplemental retirement income or want to leave a financial legacy for future generations, then whole life may be a match for you. On the other hand, if you want the flexibility to invest in the funds you want and have a long investment window (i.e. you are young, working and are experienced with investing), you may look into ILPs.

Since there are different forms of whole life insurance, you will need to identify which type of policy best suits you. There are three types of whole life insurance policies: non-participating (non-par), participating (par) and investment-linked policies (ILP).

Participating whole life policies provide non-guaranteed and guaranteed benefits. Non-guaranteed benefits are bonuses you may receive in addition to your sum assured and they depend on how well the insurer's fund performs. The guaranteed benefits are the sum assured (the payout you get upon an insured event happening). If you want a savings feature (such as a cash value) with your policy so you can get more than just your sum assured at the end of the term, then this type of whole life plan can be useful.

On the other hand, non-participating policies only provide guaranteed benefits (i.e. the sum assured). Investment-linked policies are a combination of life insurance coverage and an investment component. Unlike par and non-par plans, you choose the investment funds rather than the insurer so you bear all the investment risk. Investment-linked policies are generally riskiest life insurance products.

We recommend getting coverage that is at least 10-15x your annual income regardless of the type of whole life plan you get. You will need to also take into consideration your debt, financial obligations for your children, and lump sum benefits you want to leave for your beneficiaries. Due to the complex nature of whole life insurance products, we recommend speaking with a financial advisor, which you can do by speaking to your partners at PolicyPal.

| Whole Life Policy |

|---|

Aviva MyWholeLife Plan III

|

|

Income Star Assure

|

|

AXA Life Treasure

|

Because whole life insurance can be complicated, you'll need to consider a number of factors including your lifestyle, budget and financial needs.

First, you will need to figure out why you need whole life insurance over term life insurance. If you fall into the group of people who want financial protection for their dependents, want supplemental retirement income or want to leave a financial legacy for future generations, then whole life may be a match for you. On the other hand, if you want the flexibility to invest in the funds you want and have a long investment window (i.e. you are young, working and are experienced with investing), you may look into ILPs.

Since there are different forms of whole life insurance, you will need to identify which type of policy best suits you. There are three types of whole life insurance policies: non-participating (non-par), participating (par) and investment-linked policies (ILP).

Participating whole life policies provide non-guaranteed and guaranteed benefits. Non-guaranteed benefits are bonuses you may receive in addition to your sum assured and they depend on how well the insurer's fund performs. The guaranteed benefits are the sum assured (the payout you get upon an insured event happening). If you want a savings feature (such as a cash value) with your policy so you can get more than just your sum assured at the end of the term, then this type of whole life plan can be useful.

On the other hand, non-participating policies only provide guaranteed benefits (i.e. the sum assured). Investment-linked policies are a combination of life insurance coverage and an investment component. Unlike par and non-par plans, you choose the investment funds rather than the insurer so you bear all the investment risk. Investment-linked policies are generally riskiest life insurance products.

We recommend getting coverage that is at least 10-15x your annual income regardless of the type of whole life plan you get. You will need to also take into consideration your debt, financial obligations for your children, and lump sum benefits you want to leave for your beneficiaries. Due to the complex nature of whole life insurance products, we recommend speaking with a financial advisor, which you can do by speaking to your partners at PolicyPal.

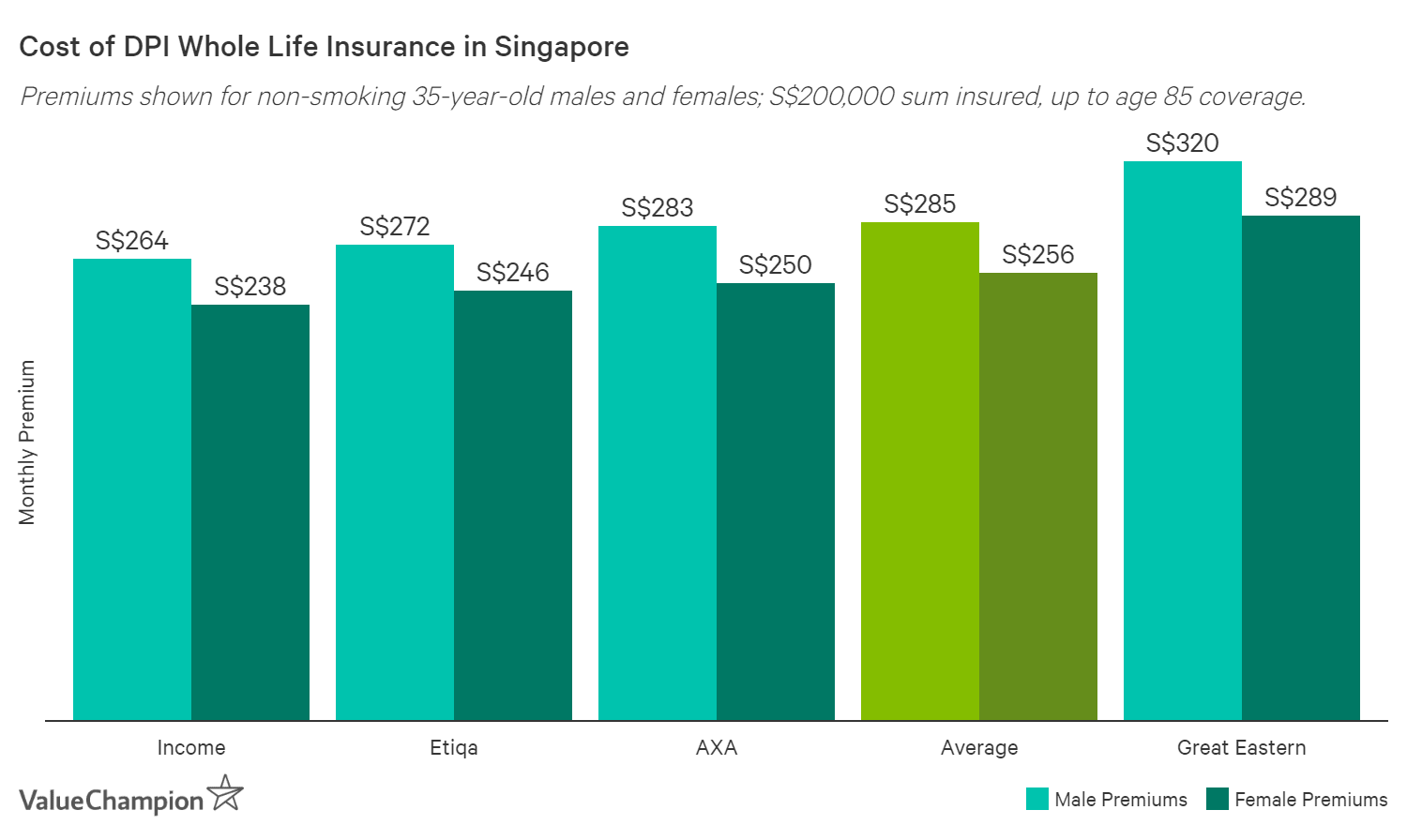

Cheapest Direct Purchase Whole Life Insurance

Direct Purchase Insurance (DPI) plans are simple life insurance policies you can buy online without speaking to a financial advisor. Whole life DPI plans provide up to S$200,000 of coverage for death and sometimes terminal illness and total & permanent disability (TPD). Since the benefits of these plans are standardised, the biggest differentiator for consumers will be price.

| Amount Insured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | Age 70 | S$58 | S$80 | S$123 |

| Age 85 | S$55 | S$74 | S$106 | |

| S$100,000 | Age 70 | S$110 | S$155 | S$241 |

| Age 85 | S$105 | S$144 | S$207 | |

| S$150,000 | Age 70 | S$165 | S$233 | S$362 |

| Age 85 | S$158 | S$215 | S$311 | |

| S$200,00 | Age 70 | S$217 | S$308 | S$480 |

| Age 85 | S$208 | S$285 | S$412 |

Etiqa Direct Purchase Whole Life Insurance

| Sum Insured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | Age 70 | S$54.12 | S$74.42 | S$114.17 |

| Age 85 | S$51.39 | S$68.07 | S$96.56 | |

| S$100,000 | Age 70 | S$108.25 | S$148.85 | S$228.35 |

| Age 85 | S$102.79 | S$136.14 | S$193.12 | |

| S$150,000 | Age 70 | S$162.37 | S$223.27 | S$342.52 |

| Age 85 | S$154.18 | S$204.21 | S$289.68 | |

| S$200,000 | Age 70 | S$216.49 | S$297.70 | S$456.70 |

| Age 85 | S$205.57 | S$272.28 | S$386.24 |

Etiqa's Direct-Whole Life premiums cost slightly below average and if you choose to pay your premiums annually, you will save around 2.3%. Your plan tenure options are up to age 75 and up to age 85 plans and Etiqa will cover you up to S$200,000 until your death or a specified maturity date. Since it is a participating policy, there is also a cash value and reversionary bonus accumulation attached to the plan. For extra coverage, you can also add a critical illness rider. Etiqa's current credit rating is A-.

| Sum Insured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | Age 70 | S$54.12 | S$74.42 | S$114.17 |

| Age 85 | S$51.39 | S$68.07 | S$96.56 | |

| S$100,000 | Age 70 | S$108.25 | S$148.85 | S$228.35 |

| Age 85 | S$102.79 | S$136.14 | S$193.12 | |

| S$150,000 | Age 70 | S$162.37 | S$223.27 | S$342.52 |

| Age 85 | S$154.18 | S$204.21 | S$289.68 | |

| S$200,000 | Age 70 | S$216.49 | S$297.70 | S$456.70 |

| Age 85 | S$205.57 | S$272.28 | S$386.24 |

Etiqa's Direct-Whole Life premiums cost slightly below average and if you choose to pay your premiums annually, you will save around 2.3%. Your plan tenure options are up to age 75 and up to age 85 plans and Etiqa will cover you up to S$200,000 until your death or a specified maturity date. Since it is a participating policy, there is also a cash value and reversionary bonus accumulation attached to the plan. For extra coverage, you can also add a critical illness rider. Etiqa's current credit rating is A-.

Income Star Secure Whole Life Insurance

| Sum Insured | Age 25 | Age 35 | Age 45 |

|---|---|---|---|

| S$50,000 | S$85.50 | S$106.50 | S$139.50 |

| S$100,000 | S$171.00 | S$213.00 | S$279.00 |

| S$150,000 | S$256.50 | S$219.00 | S$418.50 |

| S$200,000 | S$342.00 | S$292.00 | S$558.00 |

Income's DIRECT Life insurance plan is competitively priced for older consumers compared to other DPI Whole Life plans. You'll be covered for death and terminal illness until age 99 and total and permanent disability before you turn 65. You will receive the sum assured and any accumulated bonuses upon a claimable event. Plan tenures are either up to age 70 or age 85, with the up to age 85 plans costing slight less than the up to age 70 plans. Income's current credit rating is AA-.

| Sum Insured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | Age 70 | S$51.00 | S$73.00 | S$112.50 |

| Age 85 | S$49.00 | S$66.00 | S$93.50 | |

| S$100,000 | Age 70 | S$102.00 | S$146.00 | S$225.00 |

| Age 85 | S$98.00 | S$132.00 | S$187.00 | |

| S$150,000 | Age 70 | S$153.00 | S$219.00 | S$337.50 |

| Age 85 | S$147.00 | S$198.00 | S$280.50 | |

| S$200,000 | Age 70 | S$204.00 | S$292.00 | S$450.00 |

| Age 85 | S$196.00 | S$264.00 | S$374.00 |

Income's DIRECT Star Classic Life insurance plan is competitively priced for older consumers compared to other DPI Whole Life plans. You'll be covered for death and terminal illness until age 99 and total and permanent disability before you turn 65. You will receive the sum assured and any accumulated bonuses upon a claimable event. Plan tenures are either up to age 70 or age 85, with the up to age 85 plans costing slight less than the up to age 70 plans. Income's current credit rating is AA-.

Best Savings Endowment Plans

An endowment plan is a savings plan with a life insurance component attached. If you are looking to save for the future, while also receiving supplemental coverage for death, and endowment plan could be a suitable option. Below, we have examples of long and short-term endowment plans that provide at least 100% capital guarantee at the end of your plan's term. If you would like to purchase one of these plans, or simply learn more, click on get a quote to be connected with one of our advisors at PolicyPal.

| Plan: |

Tiq eEASY save V

|

Goal 9

| MyChoiceSaver

|

|---|---|---|---|

| Best For | Long-term savings | Short-term savings | Long-term Savings |

| Capital Guaranteed | 100% | 100% | 100% |

| Policy Term | 6+ years (until age 100) | 4 years | 10-25 years |

| Premium Term | Single Premium; 2 years | Single Premium | 10-25 years |

| Life Coverage | Death | Death | Death, Accidental Death, Terminal Illness |

| Yearly Cash Benefit | None | 1.80% of Premium | None |

| Credit Rating | A | AA- | A- |

| Learn More | Full Review | Full Review | Full Review |

Tiq by Etiqa' Tiq eEasy Save V is a whole life non-participating endowment plan that has a single or 2-year premium payment term. It offers a guaranteed 2.68% per annum crediting rate for the first 6 years and a non-guaranteed loyalty bonus of 0.6% of the account value at the end of the 6th year and every subsequent 6th year interval. This is a whole life endowment plan, so you will accumulate savings until you turn 100, but you won't receive any yearly cash benefits or a final cash bonus. Lastly, have the option to withdraw a partial amount within the 6 year period in the event you are diagnosed with a terminal illness or disability.

Manulife's Goal 9 endowment plan is another single premium, short-term savings plan that matures in 4 years. It provides guaranteed yearly income payouts with the option to reinvest them and receive a lump sum when your policy expires. The minimum premium is S$10,000 but you can pay this either in cash or with your Supplementary Retirement Scheme funds. Manulife's Goal 9 endowment plan offers an annual payout of 1.8% of your premium at the end of years 1 to 3, which is smaller than Income's but still a relatively generous amount. Upon policy maturity, you will receive at least 100% of your premiums and you may be eligible for a maturity bonus as high as 1.8% of your premium.

Singlife with Aviva MyChoiceSaver can be a good option for people who are looking for long-term savings. It guarantees a 100% return on your premiums upon policy maturity and provides death, accidental death and terminal illness coverage. It can be suitable for long-term savers who want to commit between 10-25 years to a savings plan.

If you're interested in these plans and would like to learn more, please speak to one of our financial advisors at PolicyPal by clicking the "Get a Quote" button.

| Policy |

|---|

|

Tiq eEASY save V

|

|

Manulife Educate

|

|

Tiq by Etiqa' Tiq eEasy Save V is a whole life non-participating endowment plan that has a single or 2-year premium payment term. It offers a guaranteed 2.68% per annum crediting rate for the first 6 years and a non-guaranteed loyalty bonus of 0.6% of the account value at the end of the 6th year and every subsequent 6th year interval. This is a whole life endowment plan, so you will accumulate savings until you turn 100, but you won't receive any yearly cash benefits or a final cash bonus. Lastly, have the option to withdraw a partial amount within the 6 year period in the event you are diagnosed with a terminal illness or disability.

Manulife's Goal 9 endowment plan is another single premium, short-term savings plan that matures in 4 years. It provides guaranteed yearly income payouts with the option to reinvest them and receive a lump sum when your policy expires. The minimum premium is S$10,000 but you can pay this either in cash or with your Supplementary Retirement Scheme funds. Manulife's Goal 9 endowment plan offers an annual payout of 1.8% of your premium at the end of years 1 to 3, which is smaller than Income's but still a relatively generous amount. Upon policy maturity, you will receive at least 100% of your premiums and you may be eligible for a maturity bonus as high as 1.8% of your premium.

Singlife with Aviva MyChoiceSaver can be a good option for people who are looking for long-term savings. It guarantees a 100% return on your premiums upon policy maturity and provides death, accidental death and terminal illness coverage. It can be suitable for long-term savers who want to commit between 10-25 years to a savings plan.

If you're interested in these plans and would like to learn more, please speak to one of our financial advisors at PolicyPal by clicking the "Get a Quote" button.

Methodology

We gathered quotes and data from all of the whole life insurance policies available in Singapore for non-smoking males and females of a variety of ages. For plans that provided quotes online, we compared premiums to see which plan offered more competitive rates for different demographics. For continuity's sake, premiums for non-DPI term life plans that you can purchase online included total & permanent disability riders, since these plans are similar to DPI plans which already include total & permanent disability in their base coverage. For plans where pricing wasn't available, we separated plans based on the category of life insurance they fell under as well as the different features offered.

| Insurance Companies Sampled | ||

|---|---|---|

| FWD | Etiqa | Income |

| ManuLife | SingLife | AIA |

| AXA | Singlife with Aviva | Great Eastern |

| Prudential | Tokio Marine | Raffles Medical |

Disclaimer

Regardless of the policy you are thinking of getting, analysing all of your life insurance options and speaking to a licensed financial advisor is key to making sure you are getting the right plan. We do not claim to endorse, promote or recommend any product on this page. All products listed here are examples of different types of life insurance and their benefits and is meant to be for educational purposes only.

Read More:

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.