UOB Stash Savings Account: How Competitive Is It?

UOB Stash Savings Account: How Competitive Is It?

ValueChampion Rating ![]()

Pros

- People with moderate to large balances

- Individuals who can save a little every month

- Consumers with variable saving habits

Cons

- People with loans, investments & more with 1 bank

- Consumers with balances below S$10k

- Inconsistent savers who want a straightforward account

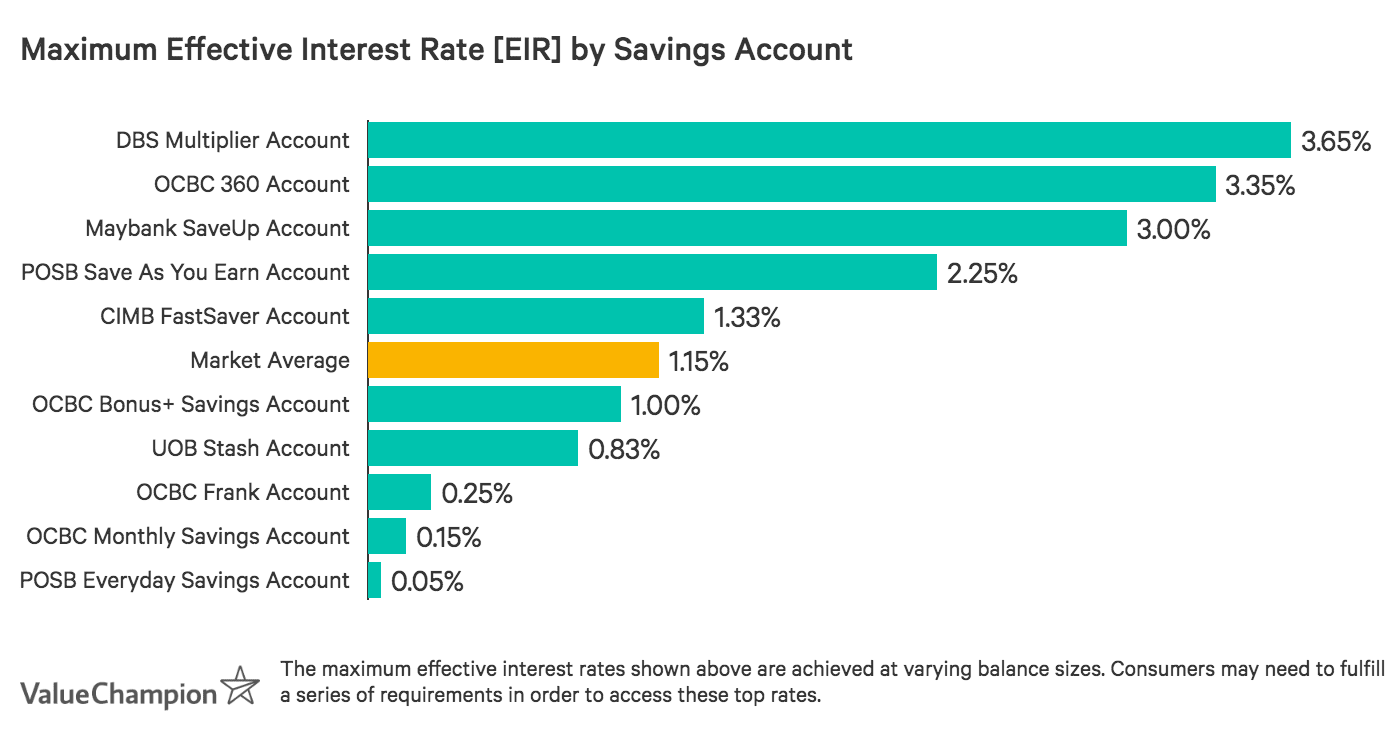

UOB Stash Savings Account is a great option for consumers with moderate-to-large balances and variable saving behaviours. Account holders earn interest rate boosts simply for growing their balance from the previous month, and don't need to worry about long-term deposit or withdrawal-related commitments. Even better, boosts are applied to the account holder's balance–rather than to the amount of increase–meaning growth to any degree is equally rewarded. Altogether, it's possible to earn an effective interest rate of up to 1.00% p.a. at a S$100k balance. While there's a S$1k minimum initial deposit, S$1k minimum balance requirement and S$2 fall-below fee, these factors are unlikely to be an issue for consumers with higher balances who are most likely to benefit from this account.

| Pros | Cons |

|---|---|

|

|

| |

| Pros & Cons |

|---|

Pros:

|

Cons:

|

What Makes UOB Stash Savings Account Stand Out

UOB Stash Savings Account is ideal for people who already have a substantial amount of funds set aside for savings, but who may not be able to make large deposits to their account every month. To begin with, consumers as young as 15 years old can apply–though there's a S$1,000 minimum initial deposit requirement, which may be a bit of a reach for young adults. However, those who can open an account can earn a maximum effective interest rate of up to 1.00% p.a., which is reasonably competitive–especially as account holders are not required to engage with other financial products or even credit a salary in order to earn boosted rates. This max EIR is achieved at S$100k, so people with larger savings are more likely to benefit.

What really makes UOB Stash stand out is how well it accommodates variable saving behaviours. Account holders earn an interest rate boost every month that their end balance is higher than the previous month's. This bonus boost varies depending on the size of the balance, where the first S$10k doesn't receive a boost but the next S$40k earns +0.60% p.a. and the next S$50k (up to S$100k) earns up to +1.0% p.a. Bonuses are applied regardless of the amount of growth and cover the entire balance, rather than just the amount of increase. This means consumers can access higher interest rates even if their account grows only slightly. And, while many competitors require consistent saving without withdrawals for 6-24 months, UOB Stash Account rewards consumers on a month-to-month basis. This is helpful for those who may need to access their funds and cannot make a long-term commitment.

| Rate Type | Details & Requirements | Interest Rate |

|---|---|---|

| Base Rate |

| 0.05% p.a. |

| Balance Increase |

| (base rate on 1st S$10k) |

| +0.60% p.a. on next S$40k | ||

| +1.00% p.a. on next S$50k | ||

| Max Effective Interest Rate: | 1.00% p.a. (at S$100k balance) | |

| UOB Stash SA Interest Rates |

|---|

Base Rate: No requirements (applied to entire balance)

|

Balance Increase: Balance is greater than previous month's (bonus added to base rate & applied to specific bands of balance)

|

| Max EIR: 1.0% p.a. (at S$100k balance) |

Still, UOB Stash has a few drawbacks. There's a S$1,000 minimum average daily balance requirement, and those who fall below this amount must pay a S$2 fee. While this may seem minor, it can quickly negate any interest earned for those with smaller balances. Additionally, consumers with balances below S$10k earn just 0.05% p.a. and are not eligible for any bonus boosts. However, as consumers with larger balances are more likely to benefit from UOB Stash Account, it's unlikely they'll need to worry about such issues.

Ultimately, UOB Stash Account is an excellent option for people who do have moderate-to-large balances and who save at least a little every month. Its flexibility is especially accommodating for those who may need access to their funds within the upcoming months and for people who are unlikely to make consistently large deposits across an extended period.

UOB Stash Savings Account Details & Requirements

| Details & Requirements | |

|---|---|

| Minimum Age Requirement | 15 |

| Minimum Initial Deposit | S$1,000 |

| Minimum Balance Requirement | S$1,000 |

| Fall-Below Fee |

|

How Does UOB Stash Savings Account Compare to Other Accounts?

Read our comparisons of UOB Stash Savings Account with other savings accounts and learn what makes each account unique in its own way. We compare and contrast each account to help you to identify which best suits your needs.

UOB Stash Savings Account v. POSB Save As You Earn (SAYE)

- Min. Age Requirement

- 16

- Min. Initial Deposit

- S$0

- Min. Balance Requirement

- S$50

If you're salaried, can commit to long-term saving, and are looking for a truly maintenance-free account, POSB Save As You Earn Account may be the best option for you. Consumers who are crediting their salary to another DBS or POSB account can set up auto-depositing and transfer S$800–S$3k/month to their POSB SAYE Account. If they don't make a withdrawal for a full 2 years, they'll earn up to an incredible 2.25% p.a. interest on their balance, one of the highest rates on the market.

This account does require a long-term commitment, which may not be feasible for some. As a result, consumers who may need access to their funds or who might make deposits of variable size might prefer UOB Stash.

| Rate Type | Details & Requirements | Interest Rate |

|---|---|---|

| Base Rate |

| 0.05% p.a. if no deposit made |

| 0.05% p.a. for S$50–290 deposit | ||

| 0.20% p.a. for S$300–790 deposit | ||

| 0.25% p.a. for S$800–3k deposit | ||

| 0.05% p.a. for S$3k+ deposit | ||

| No Withdrawals + Deposit |

| +2.00% p.a. |

| Max Effective Interest Rate: | 2.25% p.a. (at S$800–3k deposit) | |

| POSB SAYE Account Interest Rates |

|---|

Base Rate: No requirements (applied to entire balance)

|

No Withdrawals + Deposit: Bonus interest added to base rate and applied to entire balance

|

| Max EIR: 2.25% p.a. (at S$800–3k deposit) |

UOB Stash Savings Account v. OCBC Bonus+

- Min. Age Requirement

- 16

- Min. Initial Deposit

- S$5,000

- Min. Balance Requirement

- S$3,000

OCBC Bonus+ Savings Account is a great option for people who save consistently, but who may not be able to commit to long-term deposits without withdrawals. Account holders earn 0.05% p.a. base interest, boosted +0.10% p.a. on months without withdrawals, and another +0.25% p.a. (up to 0.40% p.a. total) if account holders also make a S$500+ deposit. Because consumers earn these boosts on a month-to-month basis, there's no need to worry about access to funds.

While this maximum effective interest rate is higher than that offered by UOB Stash, the latter does not require account holders to forgo withdrawals in order to unlock a boosted rate. As a result, UOB Stash Account is an even more flexible option for consumers who can frequently boost their monthly balance but might still have variable saving behaviours.

| Rate Type | Details & Requirements | Interest Rate |

|---|---|---|

| Base Rate |

| 0.05% p.a. |

| No Withdrawals |

| +0.10% p.a. |

| Extra Deposit |

| +0.25% p.a. |

| Max Effective Interest Rate: | 0.40% p.a. (any balance size) | |

| OCBC Bonus+ Savings Account Interest Rates |

|---|

Base Rate: No requirements (applied to entire balance)

|

No Withdrawals: No withdrawals during month (bonus interest added to base rate & applied to entire balance)

|

Extra Deposit: No withdrawals + deposit at least S$500 (bonus interest added to base rate & applied to entire balance)

|

UOB Stash Savings Account v. CIMB FastSaver Savings Account

- Min. Age Requirement

- 16

- Min. Initial Deposit

- S$1,000

- Min. Balance Requirement

- N/A

CIMB FastSaver Savings Account is one of the absolute best maintenance-free savings accounts currently on the market. Account holders earn interest based on their balance size, and can earn a maximum effective interest rate of 1.33% p.a. at a S$100k balance. Those with smaller balances still benefit–in fact, consumers earn 1.00% p.a. on their 1st S$50k, which is one of the highest base rates on the market. There are no requirements to unlock boosts, no minimum balance requirements, and no fall below fees. Overall, CIMB FastSaver Account is extremely competitive, even for consistent savers.

| Rate Type | Details & Requirements | Interest Rate |

|---|---|---|

| Base Rate |

| 1.00% p.a. on 1st S$50k |

| 1.50% p.a. on next S$25k | ||

| 1.80% p.a. on next S$25k | ||

| 0.60% p.a. beyond S$100k | ||

| Max Effective Interest Rate: | 1.33% p.a. (at S$100k balance) | |

| CIMB FastSaver SA Interest Rates |

|---|

Base Rate: No requirements (rate varies according to band of balance)

|

| Max EIR: 1.33% p.a. (at S$100k balance) |