Is Mobile Phone Insurance Worth the Cost?

According to a survey by the Straits Times, mobile phones are under content threat in Singapore. 18% of Singaporeans reported damaging a mobile phone with water, while 12% have damaged a phone by sitting on it. Another 15% of Singaporeans have damaged a mobile phone after simply bumping into someone. All told, 41% of Singaporeans are currently using a damaged mobile phone and 22% will not get the phone repaired or replaced due to the cost.

One solution to most of these issues is cell phone insurance. But is a cell phone insurance worth your money? Below, we do explain how a phone insurance works, and assess its value through a mathematical analysis.

Mobile Phone Insurance – The Basics

Just like any other types of insurance, mobile phone insurance will compensate you in the event your mobile phone is lost, stolen or damaged. In exchange for a monthly fee paid to an insurance company, the insurer will make sure to reimburse you for the value of your smartphone when you damage or lose it.

Considering the high cost of a smartphone, this agreement can be very attractive for consumers. For instance, an Apple iPhone 7 costs about S$1,048 while an iPhone 7 Plus will set you back S$1,248 in Singapore. With all of the above in mind, mobile phone insurance for Singaporeans could look like a very good thing on the surface.

Here at ValueChampion, we like to consider the math and finances behind any major life decision. Is a phone insurance really worth your money? Let’s explore what you should consider before purchasing mobile phone insurance.

Do The Math

As with any type of insurance, we need to weigh the cost of the insurance against the risk of the insurable event. Ultimately, we need to know if the cost of this insurance is going to be worth it. Clearly it is not possible to determine exactly when your phone will be damaged, but we can estimate how quickly your phone would need to be damaged to compensate you for the cost of the insurance.

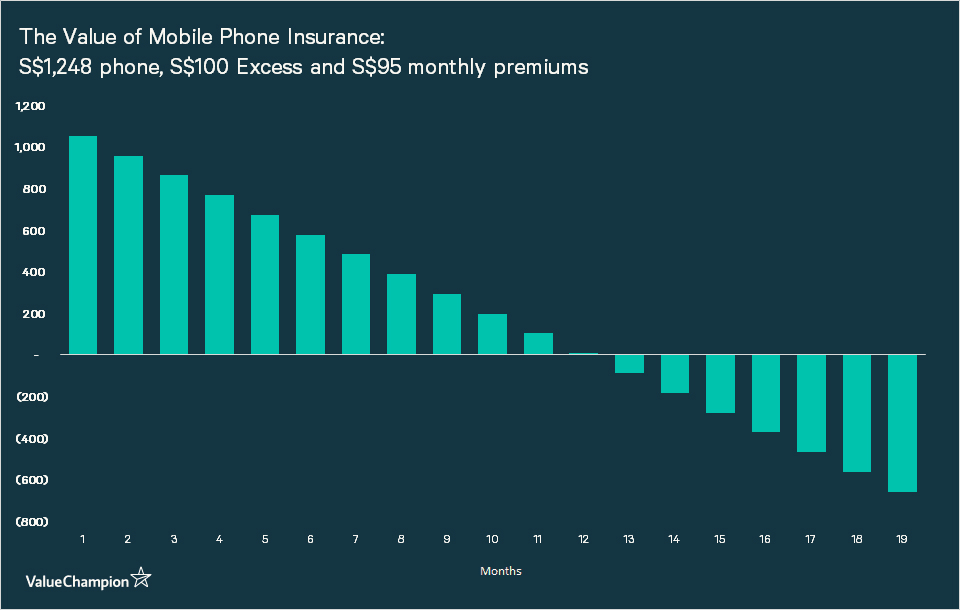

To explain, let’s consider the following example. In July, you purchase a brand-new iPhone 7 Plus for S$1,248. As you purchase your new phone, you also sign up for a mobile phone insurance which will replace this phone in the event it is lost, stolen or damaged. When you get the new phone using your insurance you just need to pay an extra S$100 as an excess fee. From there on, you are required to continue paying the monthly premium of S$95 for the insurance to be effective. In this example illustrated below, July is “month 1”.

Let’s consider one scenario where you break your phone almost immediately. On your way out of the mobile phone store you drop your phone on the pavement and the screen is shattered. While this is certainly less than ideal, the great news is that your damage is covered. You just paid the S$100 for your insurance at the store, and now you can get a brand-new phone. You just received S$1,053 in value from the insurance policy (S$1,248 – S$100 - S$95).

Now let’s consider another scenario. In this scenario, your phone is kept safe and sound for 17 months before you drop your phone in a rain puddle. In this case, it would have been cheaper to have gone without the insurance: you've already paid S$1,615 in monthly insurance premiums and still need to pay S$100 to get a new phone. In this case, you effectively “bought” a new cell phone for S$1,715 while a brand new phone is worth just S$1,248. It's easy to see that using a mobile phone insurance is a “losing value proposition" in this scenario.

The Break Even

An important concept in many financial decisions is the break-even point. This means the point where your total expenses (insurance premiums plus the excess) are equal to the value of the coverage (the price of a new iPhone 7 Plus in this case). If you look at the chart above, you can see that this break-even point is in month 11. This is the point where the value of the mobile phone insurance turns negative.

As you are considering getting a phone insurance, it is critical to keep this break-even point in mind. For someone looking at a policy similar to one the detailed here, it is not worthwhile to get insurance if they only break their phone once every 12, 13 or 14 months. For someone who typically breaks their phone once every six months, it is a wise decision.

This is where the aforementioned survey by the Straits Times comes into play. According to the survey, about 64% of people damage their phones within a year of purchase. If we assume that another 5-15% of people lose or get their phones stolen, it means that less about 70-80% of people can benefit from their phone insurance within a year of purchase. Given that the break-even point is 11 months, this would suggest that a mobile phone insurance is generally not worth your money unless you know you drop or break things quite often. This makes sense given that insurance companies have to make a profit in order to be in business.

Here’s The Catch

The catch is that you never know when accidents are going to happen. A phone insurance can still be worth the money if you know you drop your phones all the time, or if you work near water every day. If you are in a situation where you have bought a phone which you know you cannot afford to replace, the insurance is a great idea. If you are simply worried about incurring the cost of a new phone, it can be a good idea. Everyone’s situation will be slightly different, but by analyzing the break-even point you can make a more informed decision. Run the math on the cost of your phone and insurance policy to see if it is the right move for you and your family.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.