What Type of Insurance Will Charge You More Just For Being a Woman?

News of gender differentiated premiums for CareShield Life have sparked a hot debate. While industry professionals cited differences in risk between males and females as well as the importance of prioritising actuarial fairness, others felt that making women pay more just for living longer was outrageous. However, gender differentiating premiums are not a new phenomenon. In fact, several types of insurance policies follow this type of scheme. To this extent, we wanted to explore how other types of insurance stacks up in terms of pricing factors. Below, we explore the different types of insurance schemes that charge different premiums for males and females, as well as why these differences could exist.

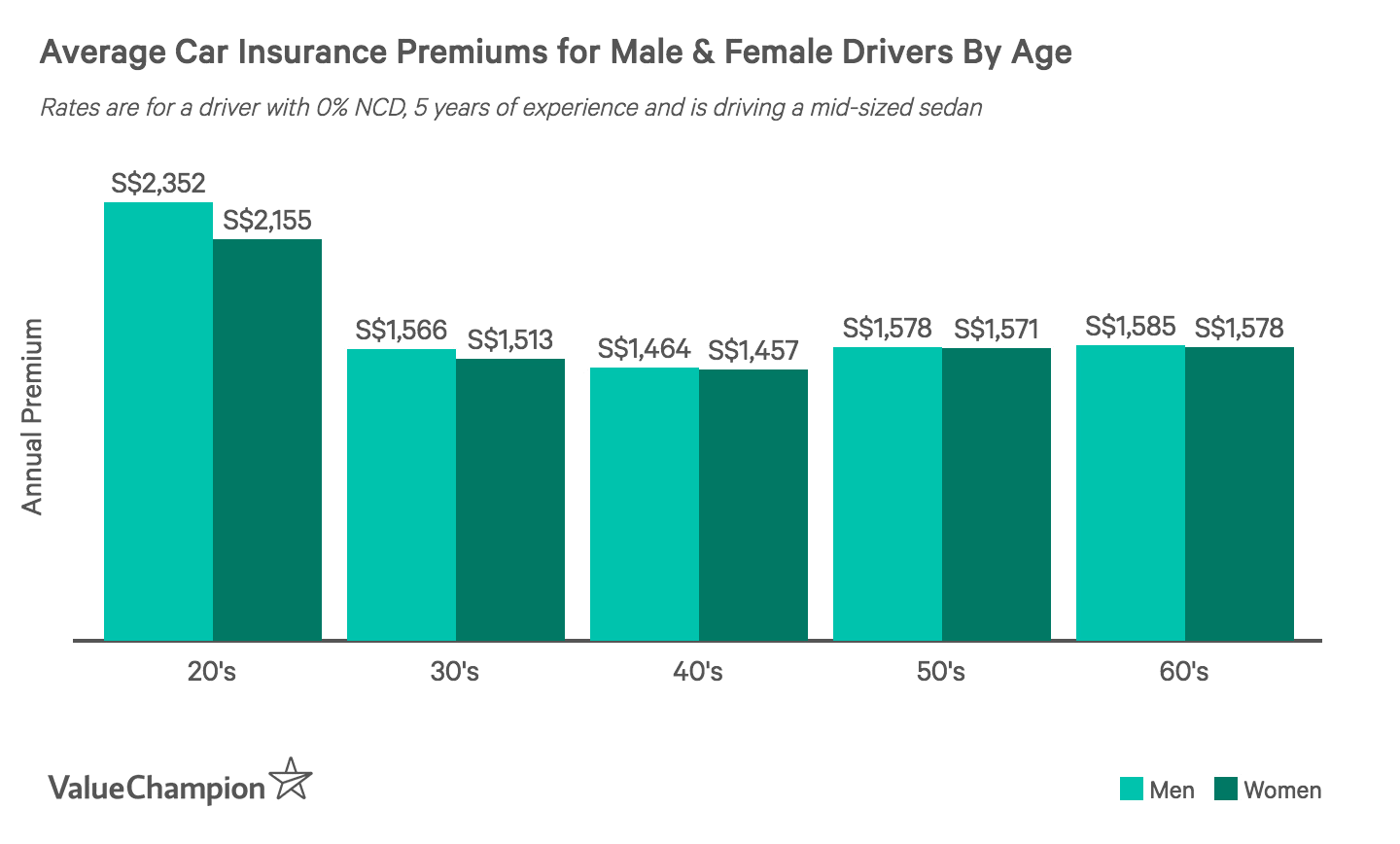

Car Insurance Premiums Depend Not Only On Gender But Age

When people think of gender differentiating premiums, they most likely think of car insurance. It is a well known fact that males pay more than females due to their higher accident incidence— especially during their younger years. Evidence compiled by the World Health Organisation (WHO) suggests that young men make up 73% of all road traffic deaths and they are 3x as likely as females to be killed in a traffic crash. Not only that but, research conducted by Aviva showed that men in Singapore are also 1.4x as likely to get into a car accident as their female counterparts, showing that men are riskier not only on a global level, but on a domestic level as well. In fact, based on our research of car insurance premiums, we found that younger men pay on average 10% higher premiums than younger women.

However, car insurers ask for more than just your gender: they also take into consideration your age, the type of car you drive, your driving history and your marriage status. In fact, the difference in car insurance premiums between genders slowly decreases with age, and women between the ages of 55-65 may end up paying around the same as men. As the WHO statistics have shown, age matters significantly for insurers because younger drivers tend to be riskier drivers than their more mature counterparts.

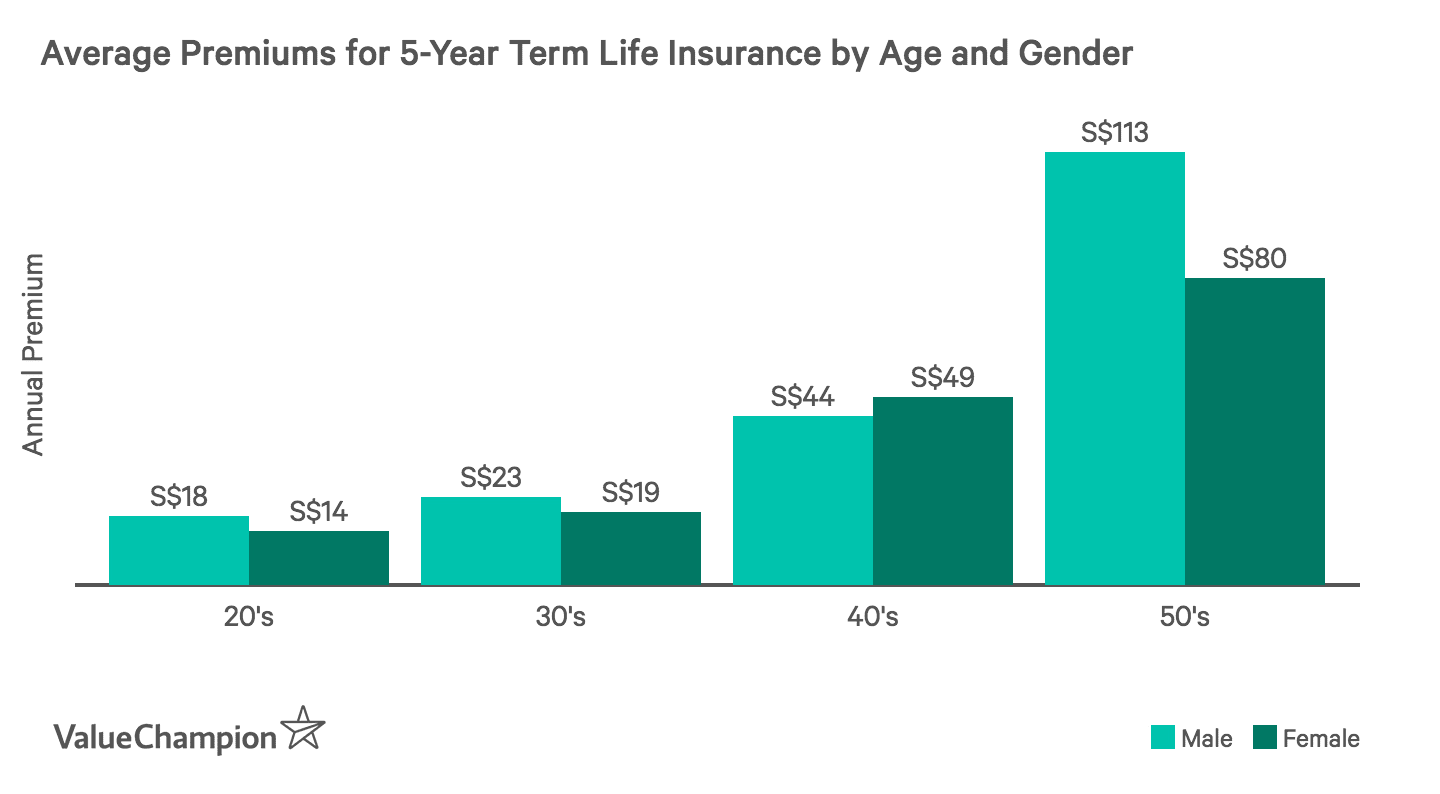

Men Pay Higher Rates than Women for Life Insurance

In terms of life insurance, we found that men pay 26.8% more than women for term life insurance in Singapore. The case for this, as mentioned by insurer Aviva, is that Singaporean men have a shorter life expectancy than women, thus increasing the likelihood of a payout, which is a direct cost for the insurance companies. Additionally, not only do the shorter lifespans increase the chance of a payout, but Singaporean men also have a 73% higher incidence rate of stroke, 143% higher incidence rate of heart attacks, tend to work in riskier occupations and exhibit overall higher death rate than female Singaporeans. Naturally, insurers may see men as riskier to insure and therefore charge a higher premium for them.

Older Men and Younger Women Pay More for Critical Illness Insurance

According to AXA's premium data, critical illness insurance seems to be 7% more expensive for younger women than younger men, but changes to be 7% less expensive for older women than older men. Women may see higher critical illness premiums due to their higher risk of developing cancer. For example, out of the more than 64,000 cases of cancer studied by the National Registry of Diseases Office, 51% of those diagnosed were women. Because cancer treatment is costly, the higher rate of cancer among women and cancer's expensive treatment could mean insurers feel that women will file claims more often. However, men may most likely pay more as they get older because their chances of getting a stroke or heart attack becomes much higher than for females. Not only do strokes and heart attack treatments cost over S$10,000 on average to treat, strokes also have the longest long-term physical disability treatment, meaning insurers may believe they'll pay out higher claims with older males.

Interestingly, we found that female smokers pay less across the board for a critical illness plan than their male smoking counterparts. Additionally, critical illness premiums increase with age, due to the higher risk of developing serious illnesses down the line.

Gender Doesn't Always Matter

Clearly, gender is an important factor that influences many insurance product's pricing. However, it's neither the only nor the most important factor. In fact, there are other insurance products that don't even consider the policyholder's gender. For example, travel insurance policies prioritise length of trip, trip location and the number of people travelling with you. This is likely because longer trips, certain destinations and more people travelling together can increase the probability of a claim. Gender could matter since it may well be possible that a certain gender exhibits riskier behaviors while travelling, but no insurers in Singapore even ask for this information.

In terms of home insurance and maid insurance, genders don't seem to matter either, since policyholders tend to be a family comprised of both men and women. Instead, insurers prioritize other factors like the value of contents in your home, the amount of renovation work that has been done and the type of property for home insurance and nationality of foreign domestic worker for maid insurance.

What This Means For You

While the concept of insurance is to protect you from costly risks, insurers still want to make a profit and ensure that they will be able to pay out on all their claims. Because of that, certain insurance schemes will cost more for some groups of people compared to others due to the higher perceived risk. While there are some ways of finding out why insurers charge certain premiums to some groups—such as looking at historical data or worldwide trends—other ways such as looking at claims history may not be available. This can make it seem like a lack of transparency, leading to a general feeling of distrust in insurers.

However, just because the average rate is higher for one gender over the other does not mean that you will necessarily fall prey to that statistic. Your insurance premiums will depend on your history, your individual perceived risk and your past insurance experience. For instance, a safe male driver may end up paying much lower premiums than a female with a couple of accidents under her belt. Likewise, a young female looking to get critical illness insurance may end up paying less in premiums with a clean bill of health, compared to her male counterpart who has had critical illness claims in the past.

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.