Paktor Owner M17 Entertainment's IPO Trouble: 3 Questions That Must Be Addressed

M17 Entertainment, the company that owns Paktor and live-streaming service 17 Media, has postponed its IPO that was originally scheduled for 7th of June. The delay came after its IPO pricing of US$8 came in far below the original range of US$10-12 that the company was hoping for. But what concerns could investors have had around the company and its future prospects? We discuss some of the biggest risk factors that investors must answer before purchasing M17 Entertainment's stock, if it lists at all.

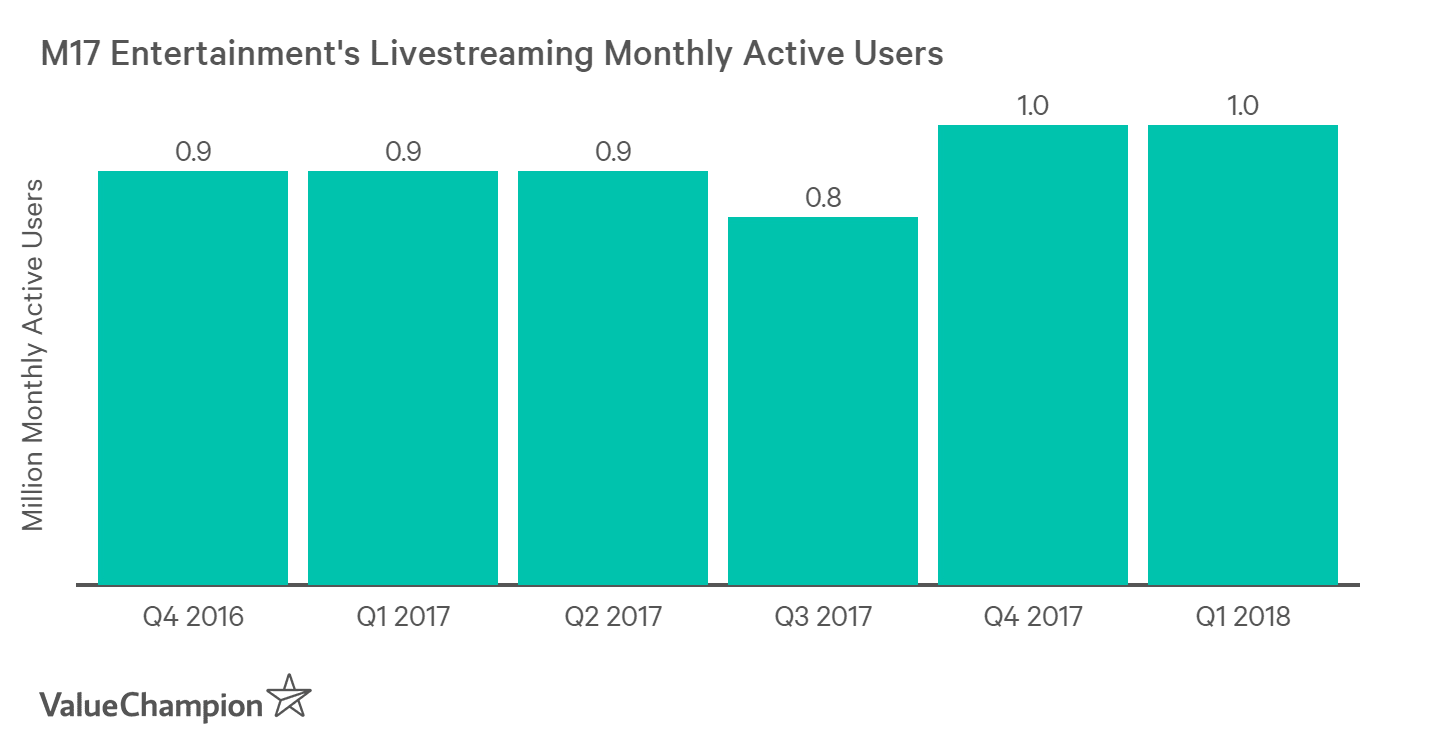

How Will 17 Media Grow Its User Base?

17 Media, the leading live-streaming service in Taiwan, HK and Japan, is the biggest part of the company that accounts for 90% of its revenue. However, the growth rate of its user base has been rather stagnant, reaching about 1 million monthly active users in Q1 of 2018 from 0.9 million in 2016. Given the fact that it has been steadily dominant in Taiwan and Hong Kong for quite some time, it may have a difficult time attracting more users in its core markets.

Still, one hope for the company in terms of user growth could be Japan. After becoming the 2nd biggest live streaming platform in the country in Q1 2018, it now seems to have taken the #1 spot according to its Apple App Store download rankings. However, its competition in Japan remains both well-funded and fierce, and just how impactful this market could be for 17 Media is still unclear.

How Will 17 Media Make More Money from Its Users?

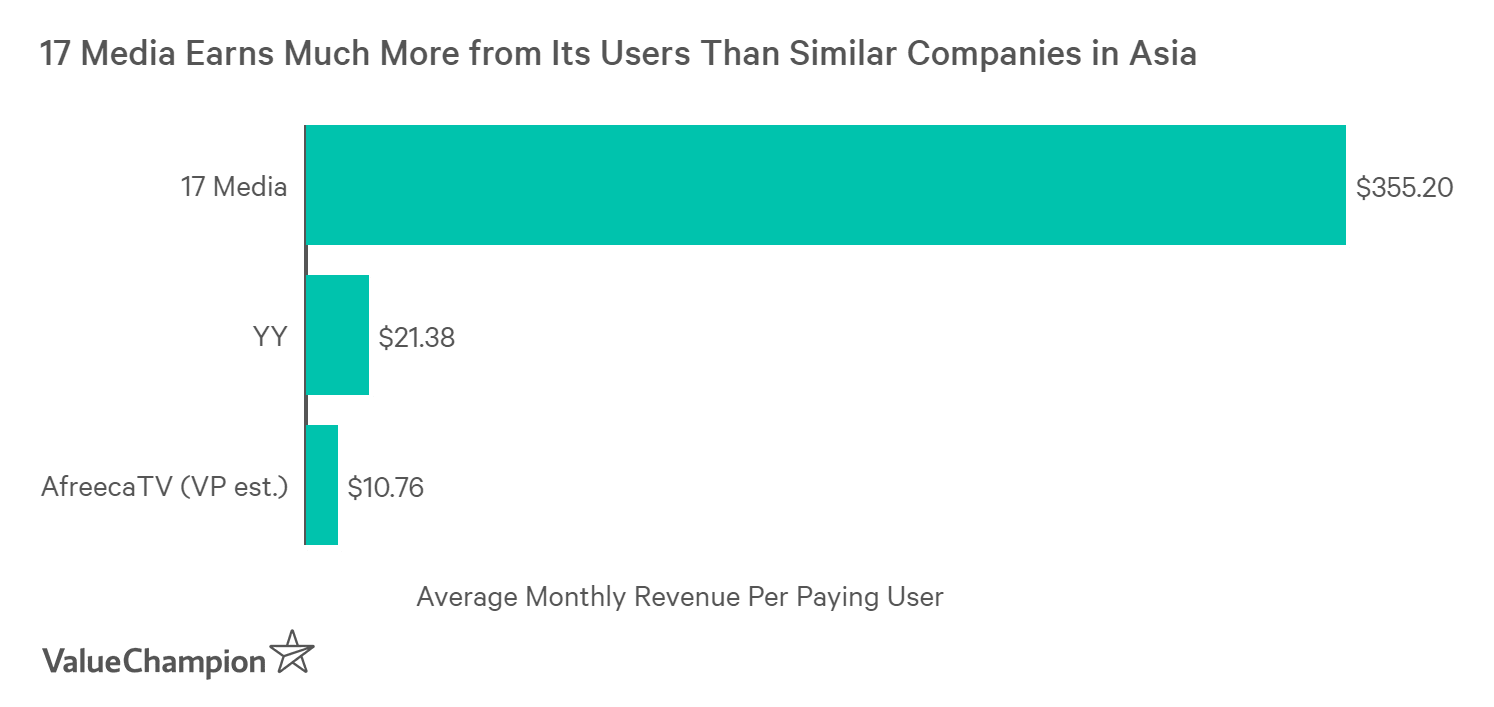

One shockingly "positive" finding about 17 Media was its monetization capability: it earns 20-30x more from each user than similar live streaming platforms in the region. For example, YY in China earns about $20 per paying user per month, while AfreecaTV earns about $10 per paying user per month. In contrast, 17 Media earns a staggering $355 per paying user per month.

However, this disparity also raises some questions. Given that all three of these live-streaming apps make money by allowing users to purchase gifts for their favorite streamers, how is one platform able to outperform all others to this extent? And what does this imply about 17 Media's ability to earn more from its users over time? It's possible that this company has figured out some "secret sauce" in live streaming that induces its users to spend more. In fact, the company provides evidence that it makes twice as much on its Taiwanese users as it does on its users in other countries. Still, there are two other plausible scenarios. First, it may be that 17 Media is over-monetizing its user base and doesn't have that much more room for improvement. Or secondly, it is also possible that it has already attracted most of the valuable users, and new users will bring the average revenue per paying user down over time (which implies slower revenue growth than one may otherwise expect).

Can Paktor Survive in Face of Competition from Tinder?

Lastly, M17 Entertainment's dating arm seems to be struggling to grow, especially in face of competition from Tinder. For instance, its dating monthly active users has remained relatively stable around 0.6 million to 0.7 million since 2017, while Paktor's app store download rankings have lagged behind Tinder in all of its major markets. While 17 Media may have some advantages to stave off the competitive pressure from larger, global competitors like Twitch, it seems like Paktor may not be as lucky.

Ultimately a Proven Business Model, but Unproven Growth Opportunity

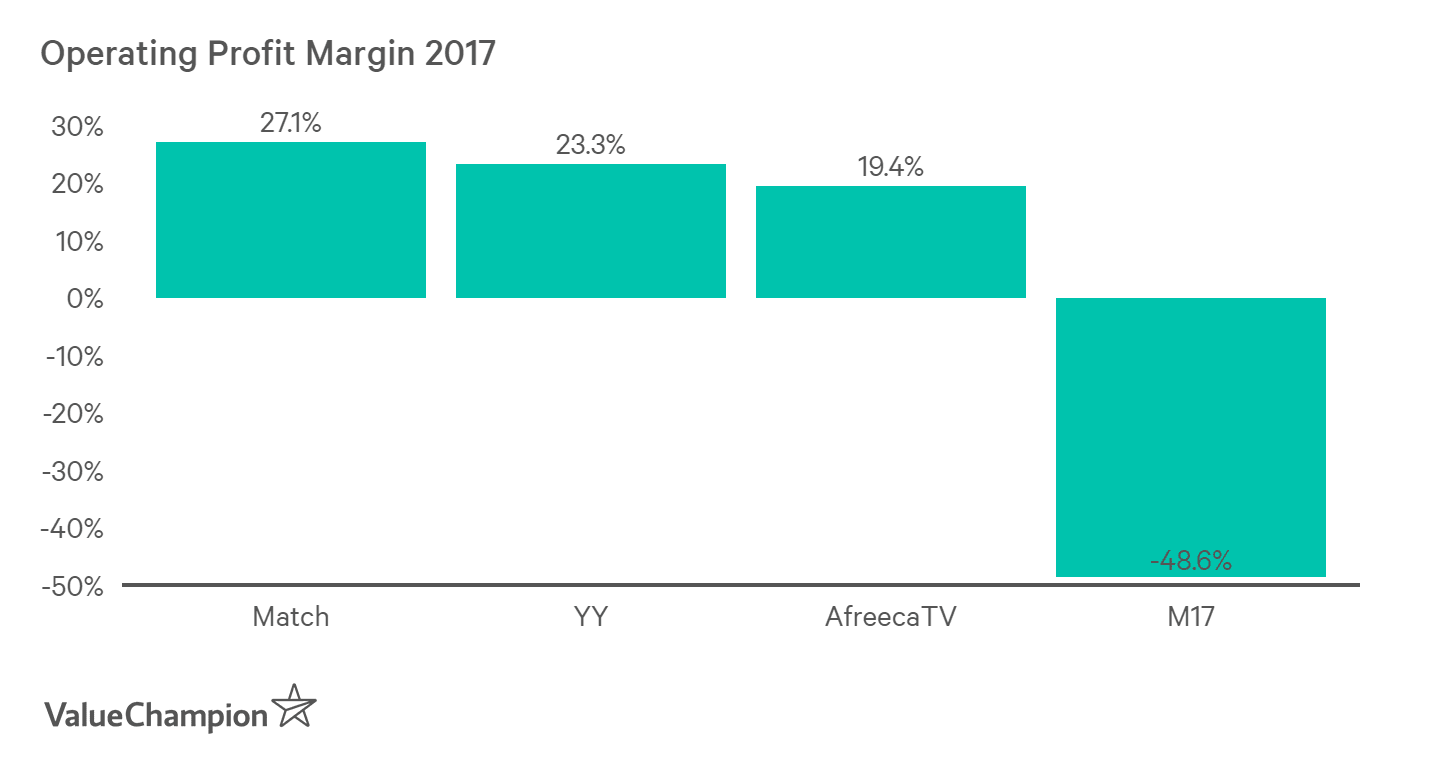

Ultimately, M17 Entertainment's business models definitely have been proven to be successful and profitable. In live streaming, YY and AfreecaTV both make +20% operating profit margin, while Match (the leading online dating company) earns an even higher margin of 27.1% across their dating apps as well. Therefore, although M17 Entertainment is bleeding money today (-126% operating margin in Q1 2018), it's possible that it could turn profitable as it grows. However, it would also have to grow exponentially to reach that stage. Given the delay of its IPO, it seems that investors may still be uncomfortable with some of the questions around this company's growth opportunities.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.