Why the Korean Stock Market is Interesting: Samsung Electronics & Corporate Governance

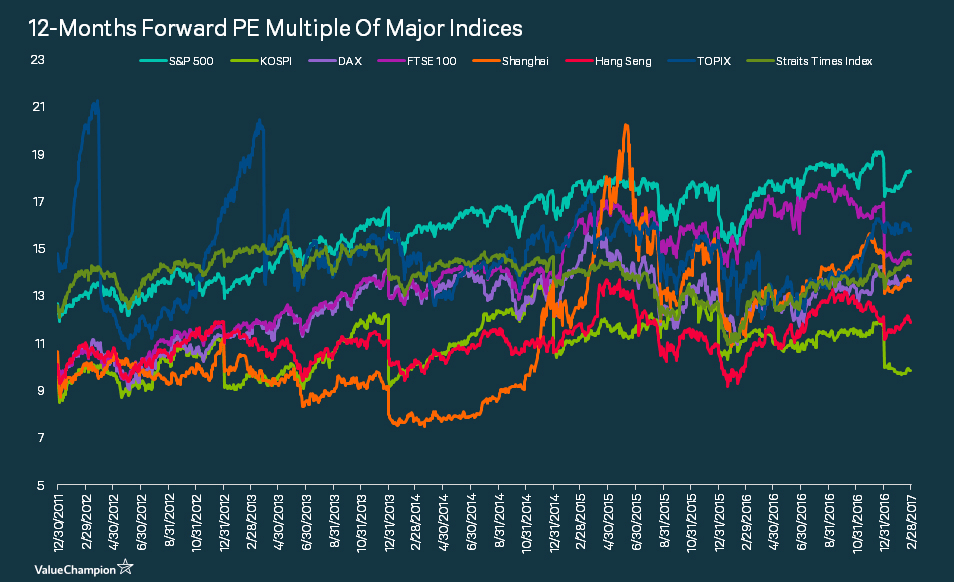

Korea has one of the biggest stock markets in the world, with $1.2 trillion of market capitalization and over 2,000 companies listed on the exchange. It also has been one of the cheapest markets historically, and even Warren Buffett, the legendary investor, chose it as the first foreign market to invest outside of the US. Today, it still remains one of the cheapest markets in the world on P/E ratio, trading just around 10x 2017 PE compared to 13x-19x of most other major markets in the world.

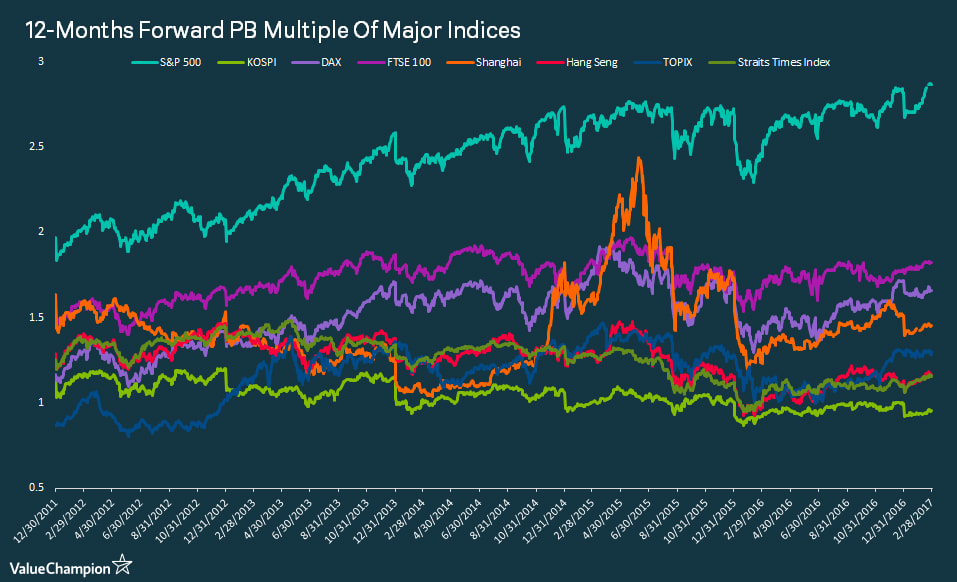

As you can see in the chart above, however, the Korean stock market has always been one of the cheapest markets in the world. The reason is that most companies are controlled by "Chaebol" families, who generally only care about their self-interests and ignore for the wellbeing of their shareholders. Global investors have shunned away from such disregard for corporate governance to avoid being negatively affected by Chaebol's influences. Thus, the demand for Korean stocks have traditionally been low, resulting is low valuation for these companies. This phenomenon is generally refereed to as a "Korea discount." The valuation discount is apparent even on other valuation metrics like P/B Ratio.

Characteristics of Korean Companies

The consequence of Chaebol's corporate governance culture manifests itself on a few fronts. First, Korean companies tend to have low margins because they tend to prolong investments in loss-making side businesses for a long time. Often, these families over-commit themselves to "long-term" projects that are supposed to create a better future for those companies. However, the problem is that these investment areas are often completely unrelated to their core businesses, and therefore do not benefit from any synergies with the parent companies. Often fueled by personal egos of the families, these investment areas usually end up in spectacular failures.

Secondly, Korean companies tend to hoard a lot of cash on their balance sheets because Chaebols don't have much incentives to distribute the cash to their shareholders. This is because Chaebols don't like to sell their shares. What they care about is retaining control over their companies while enjoying a steady access to cash via dividends and company's finances. Why give out cash to increase your stock price when you can use them on your own already however you see fit? This also often results in bad acquisitions because Chaebols care more about making a big deal to either fulfill their egos or secure their control. This also means that Korean companies refrain from borrowing debt to optimize their balance sheets, in fear of potentially losing control of their companies in case of emergencies like the Asian crisis in 1998.

The result of low net margin and under-levered balance sheets is low Return-On-Equity (ROE). This means that for every dollar of investor's money, Korean companies only make $X, while US companies or Singaporean companies make $Y.

What Samsung's Change Means For the Country

Samsung Electronics, one of the largest chips and consumer electronics manufacturers in the world, is both the most well-known and most representative of Korean companies. It is controlled by the Lee family through an infamously complex cross-holding structure via different Samsung entities. It holds a lot of cash, and earns lower ROE than compared to its peers. Its stock trades at a discount to peers, and the famous investment firm Elliot management even published a lengthy report detailing why it should be valued at a significantly higher price.

| Forward PE Ratio | Forward PB Ratio | Forward ROE | Cash as % of Assets | |

|---|---|---|---|---|

| SAMSUNG ELECTRONICS | 9.8 | 1.46 | 12.8 | 30% |

| LG ELECTRONICS | 12.57 | 0.78 | 7.08 | 7% |

| LG DISPLAY | 7.82 | 0.93 | 13.58 | 11% |

| SK HYNIX | 8.82 | 1.55 | 15.3 | 16% |

| MICRON TECHNOLOGY | 8.01 | 1.85 | 20.07 | 16% |

| TSMC | 12.96 | 3.1 | 25.26 | 35% |

| QUALCOMM | 14.09 | 3.06 | 20.88 | 36% |

| APPLE | 13.27 | 4.66 | 49.43 | 21% |

What's interesting right now is that Samsung's corporate governance culture seems to be at a turning point. First, the firm's leader Lee Kun-Hee is effectively dead, and is being kept alive on life-support in order to secure a peaceful transition of control to his son, Lee Jae-yong. Secondly, Samsung Electronics has been dragged into the spotlight with Korean President's "strange" corruption scandal recently. The investigation has been shedding light on how Samsung might have been involved in, if not benefiting from, some illegitimate practices.

Whether or not the allegations are true, Samsung Electronics has been responding to the pressure by promising better corporate governance. Under pressure from investors, public, media and the legal authorities, Samsung has been promising higher dividends for investors and even possibly reorganizing the company structure to be more favorable for investors. The subsequent results have been quite great. Samsung Electronics's stock recently hit all time high of KRW1,873,000, which is up about 60% from beginning of 2016.

While it remains to be seen if Samsung's stock has much more room to go up, what's even more interesting to consider is the ramification of this change on the general Korean stock market. Other Chaebols at SK, LG or Hyundai must be closely monitoring this series of event. One way or another, they must be either aware that they are also vulnerable to the same level of "attention" or envious of the enormous share gain that Samsung has been achieving thus far. If Samsung's transition is successful and beneficial to all stakeholders (including the Lee family, as Elliot Management claims), we could be looking at a potential seismic shift in corporate governance culture in Korea. Many of these major Chaebol companies are trading at discounts to their global peers, and Samsung's transformation could signal a potential change in the rest of these Chaebol companies.

| Forward PE Ratio | Forward PB Ratio | Forward ROE | Cash as % of Assets | |

|---|---|---|---|---|

| SK TELECOM | 12.74 | 1.13 | 9.57 | 5% |

| AT&T | 13.96 | 2.03 | 7.05 | 1% |

| VERIZON COMMUNICATION | 13.18 | 9.54 | 63.6 | 2% |

| HYUNDAI MOTOR | 5.85 | 0.63 | 9.15 | 15% |

| TOYOTA MOTOR | 10.84 | 1.22 | 9.86 | 12% |

| FORD MOTOR | 7.7 | 1.71 | 17.8 | 16% |

| GENERAL MOTORS | 6.56 | 1.25 | 21.49 | 12% |

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.