Best Term Life Insurance in Singapore 2024

Our life insurance experts researched dozens of term life insurance policies in Singapore and analysed their pricing and benefits. Because life insurance policies are complex products, you can use our guide below to compare different types of term life plans based on product type and coverage provided.

- Traditional Term Life Insurance: Aviva, Income & More. Traditional term life products to suit a variety of needs

- Direct Purchase Term Life Insurance: FWD, eTiQa & more. Competitive DPI Term Life plans that you can purchase instantly online

- Other Online Term Life Insurance: FWD, eTiQa & more. Term Life Insurance plans you can buy online that aren't DPI products

- Direct Purchase Whole Life Insurance: eTiQa, Income & more. Competitive DPI Whole Life products you can buy instantly online

- Traditional Whole Life Insurance: Aviva, AIA & More. Traditional whole life insurance products ranging from investment linked policies to simple whole life coverage

- Savings/Endowment Insurance: Income, Manulife & Aviva. Endowment plans are savings plans with a life insurance component attached. Annual rates are typically higher than regular savings accounts

Traditional Term Life Insurance

| Insurer | |||

|---|---|---|---|

| Plan Name | MyProtector-Term Plan II | AIA Secure Flexi Term | TM Term Assure II |

| Annual Premium^ | S$521 | S$448 | S$412 |

| Coverage | Death, TPD & Terminal Illness | Death, Terminal Illness, Terminal Cancer | Death, TPD & Terminal Illness |

| Term |

|

|

|

| Features |

|

|

|

Term life insurance is a type of life insurance that will pay out a specific sum if you die during the time you are insured. In general, it is most beneficial for young couples who want to ensure their young children will have financial support in the event of the parent's untimely death.

One of the most important things you have to look at when deciding which term life policy best suits you is to look at the term periods. Term life insurance comes in renewable and non-renewable terms. You can purchase a traditional term life policy with between 5 year (renewable) and 30 year maturities or up to ages between 55-99 (non-renewable).

You'll have to look at features next. Unlike whole life insurance, you'll only get a payout if you die or are diagnosed with a terminal illness. However, some insurers offer additional benefits and riders. These benefits can include guaranteed renewal, inflation protection, a convertibility option (converting to a whole life policy) or increased coverage for certain life milestones. Riders can include permanent disability coverage and premium waivers. Looking at your lifestyle and concerns and matching them with the benefits and riders offered can help you further narrow down your options.

Though term life insurance is fairly straightforward, it still requires a considerable amount of research to find the best plan for your needs. This is why we strongly recommend reaching out to our advisors at PolicyPal, to help you get the best coverage for you.

| Term Life Policy |

|---|

|

|

|

Term life insurance is a type of life insurance that will pay out a specific sum if you die during the time you are insured. In general, it is most beneficial for young couples who want to ensure their young children will have financial support in the event of the parent's untimely death.

One of the most important things you have to look at when deciding which term life policy best suits you is to look at the term periods. Term life insurance comes in renewable and non-renewable terms. You can purchase a traditional term life policy with between 5 year (renewable) and 30 year maturities or up to ages between 55-99 (non-renewable). As you get older and renew your term life plans, you should expect your premiums to rise, due to the increase in your age, potential health degeneration and other lifestyle factors.

You'll have to look at features next. Unlike whole life insurance, you'll only get a payout if you die or are diagnosed with a terminal illness. However, some insurers offer additional benefits and riders. These benefits can include guaranteed renewal, inflation protection, a convertibility option (converting to a whole life policy) or increased coverage for certain life milestones. Riders can include permanent disability coverage and premium waivers. Looking at your lifestyle and concerns and matching them with the benefits and riders offered can help you further narrow down your options.

Though term life insurance is fairly straightforward, it still requires a considerable amount of research to find the best plan for your needs. This is why we strongly recommend reaching out to our advisors at PolicyPal, to help you get the best coverage for you.

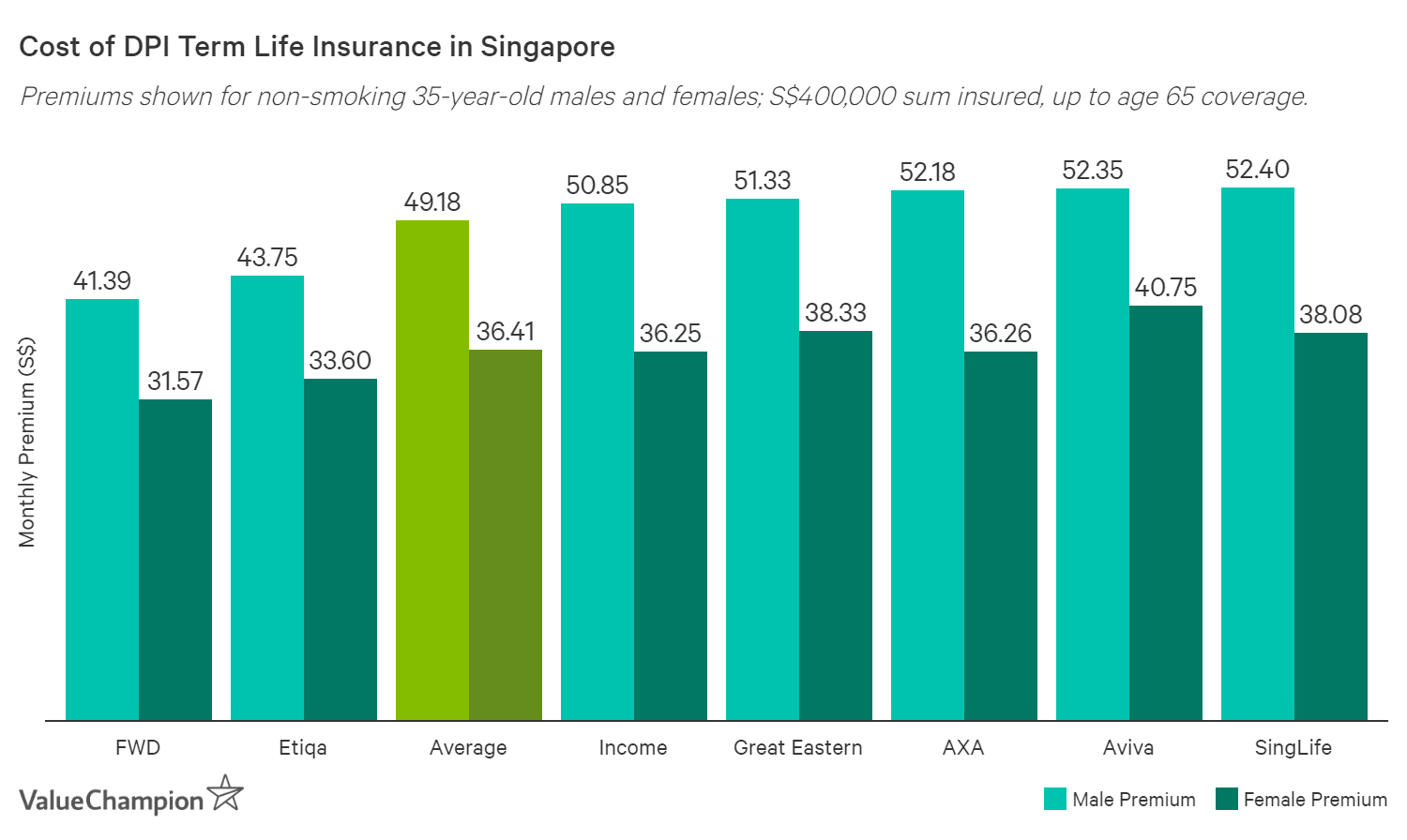

Cheapest Direct Purchase Term Life Insurance

Term insurance offers protection for a fixed amount of time and will only pay out the sum assured if death, terminal illness or total and permanent disability occurs within the period insured. Term Life Direct Purchase Insurance (DPI) is a life insurance scheme that lets consumers purchase a term life insurance plan directly through the insurer without going through an intermediary such as a financial advisor.

Similar to a traditional term life policy, Direct Purchase term life insurance will offer no cash value when the policy ends or if it is ended prematurely. Its benefits are fairly standard, including up to S$400,000 of death, terminal illness (until age 85) and total permanent disability (until age 65) coverage. You can also get a critical illness rider. Below we discuss some DPI plans from a few leading insurers in Singapore.

| Amount Insured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | 5-Years | S$3.48 | S$4.31 | S$7.34 |

| 20-Years | S$3.85 | S$5.79 | S$12.60 | |

| Age 65 | S$5.64 | S$8.08 | S$12.18 | |

| S$200,000 | 5-Years | S$9.21 | S$11.89 | S$21.78 |

| 20-Years | S$9.90 | S$16.46 | S$39.50 | |

| Age 65 | S$16.72 | S$24.28 | S$38.40 | |

| S$400,000 | 5-Years | S$17.56 | S$23.09 | S$43.50 |

| 20-Years | S$19.01 | S$32.61 | S$75.22 | |

| Age 65 | S$33.33 | S$48.89 | S$78.04 |

FWD Direct Purchase Term Life Insurance

| Sum Assured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | 5-Years | S$2.76 | S$3.77 | S$7.24 |

| 20-Years | S$4.17 | S$6.05 | S$12.23 | |

| Age 65 | S$6.45 | S$8.02 | S$11.53 | |

| S$200,000 | 5-Years | S$7.72 | S$10.70 | S$20.52 |

| 20-Years | S$8.95 | S$16.31 | S$39.99 | |

| Age 65 | S$18.42 | S$25.61 | S$39.82 | |

| S$400,000 | 5-Years | S$12.63 | S$17.19 | S$32.98 |

| 20-Years | S$14.38 | S$26.31 | S$64.55 | |

| Age 65 | S$29.82 | S$41.39 | S$64.20 |

FWD's DIRECT-Term Life insurance offers death and total & permanent disability coverage (TPD) of up to S$400,000 and offers the opportunity to buy a critical illness rider. You can get the plan for 5 years, 20 years or until you are 65. FWD offers competitive prices for its S$300,000 and S$400,000 plans, with its premiums 10-25% cheaper than the market average for 5 and 20-year plans regardless of your gender. You will also receive S$5,000 for funeral expenses paid by the next business day after they receive the death certificate. However, FWD is not the cheapest option for 25-year olds or those who are looking for plans with coverage of up to age 65. FWD's umbrella company, FWD Group Financial Services, currently has a credit rating of BBB-.

| Sum Assured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | 5-Years | S$2.76 | S$3.77 | S$7.24 |

| 20-Years | S$4.17 | S$6.05 | S$12.23 | |

| Age 65 | S$6.45 | S$8.02 | S$11.53 | |

| S$200,000 | 5-Years | S$7.72 | S$10.70 | S$20.52 |

| 20-Years | S$8.95 | S$16.31 | S$39.99 | |

| Age 65 | S$18.42 | S$25.61 | S$39.82 | |

| S$400,000 | 5-Years | S$12.63 | S$17.19 | S$32.98 |

| 20-Years | S$14.38 | S$26.31 | S$64.55 | |

| Age 65 | S$29.82 | S$41.39 | S$64.20 |

FWD's DIRECT-Term Life insurance offers death and total & permanent disability coverage (TPD) of up to S$400,000 and offers the opportunity to buy a critical illness rider. You can get the plan for 5 years, 20 years or until you are 65. FWD offers competitive prices for its S$300,000 and S$400,000 plans, with its premiums 10-25% cheaper than the market average for 5 and 20-year plans regardless of your gender. You will also receive S$5,000 for funeral expenses paid by the next business day after they receive the death certificate. However, FWD is not the cheapest option for 25-year olds or those who are looking for plans with coverage of up to age 65. FWD's umbrella company, FWD Group Financial Services, currently has a credit rating of BBB-.

Etiqa Direct Purchase Term Life Insurance

| Sum Assured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | 5-Years | S$2.19 | S$3.13 | S$5.97 |

| 20-Years | S$2.54 | S$4.14 | S$8.09 | |

| Age 65 | S$5.14 | S$7.38 | S$11.40 | |

| S$200,000 | 5-Years | S$6.80 | S$9.74 | S$18.56 |

| 20-Years | S$7.90 | S$15.44 | S$36.93 | |

| Age 65 | S$15.99 | S$22.97 | S$35.46 | |

| S$400,000 | 5-Years | S$12.95 | S$18.55 | S$35.35 |

| 20-Years | S$15.05 | S$29.4 | S$70.35 | |

| Age 65 | S$30.45 | S$43.75 | S$67.55 |

Direct-Etiqa Term Life provides 5-year, 20-year and until age 65 plans with death and total & permanent disability (TPD) coverage between S$50,000 and S$400,000. It is one of the cheapest options on the market for young non-smoking consumers in their 20-30's, as its premiums range between 10-47% below average for this age group. It is especially affordable for females, as their 5-year plans with S$50,000 of coverage cost less than S$1.50 per month. Those looking for up to age 65 plans, S$400,000 plans and older consumers may see premiums hover around average to 20% below average. You can save a further 5% by paying annually instead of monthly. Etiqa's credit rating according to Fitch is A-.

| Sum Assured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | 5-Years | S$2.19 | S$3.13 | S$5.97 |

| 20-Years | S$2.54 | S$4.14 | S$8.09 | |

| Age 65 | S$5.14 | S$7.38 | S$11.40 | |

| S$200,000 | 5-Years | S$6.80 | S$9.74 | S$18.56 |

| 20-Years | S$7.90 | S$15.44 | S$36.93 | |

| Age 65 | S$15.99 | S$22.97 | S$35.46 | |

| S$400,000 | 5-Years | S$12.95 | S$18.55 | S$35.35 |

| 20-Years | S$15.05 | S$29.4 | S$70.35 | |

| Age 65 | S$30.45 | S$43.75 | S$67.55 |

Direct-Etiqa Term Life provides 5-year, 20-year and until age 65 plans with death and total & permanent disability (TPD) coverage between S$50,000 and S$400,000. It is one of the cheapest options on the market for young non-smoking consumers in their 20-30's, as its premiums range between 10-47% below average for this age group. It is especially affordable for females, as their 5-year plans with S$50,000 of coverage cost less than S$1.50 per month. Those looking for up to age 65 plans, S$400,000 plans and older consumers may see premiums hover around average to 20% below average. You can save a further 5% by paying annually instead of monthly. Etiqa's credit rating according to Fitch is A-.

Great Eastern Direct Purchase Term Life Insurance

| Sum Assured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | 5-Years | S$3.96 | S$4.83 | S$7.67 |

| 20-Years | S$4.38 | S$6.08 | S$12.08 | |

| Age 65 | S$6.33 | S$8.08 | S$11.71 | |

| S$200,000 | 5-Years | S$9.17 | S$12.67 | S$24.00 |

| 20-Years | S$10.83 | S$17.67 | S$41.67 | |

| Age 65 | S$18.67 | S$25.67 | S$40.17 | |

| S$400,000 | 5-Years | S$18.33 | S$25.33 | S$48.00 |

| 20-Years | S$21.68 | S$35.33 | S$83.33 | |

| Age 65 | S$37.33 | S$51.33 | S$80.33 |

Great Eastern's Direct-Great Term Life insurance is one of the cheapest options for older Singaporeans looking for up-to-age-65 plans, regardless of the amount you want to be insured for. For instance, a 55-year old consumer looking for an up to 65-year old plan will see premiums that are around 30% below the market average. On the other hand, Great Eastern is less competitively priced for 5 and 20-year plans and for younger consumers. Furthermore, age is defined as age at next birthday, as opposed to other plans that define your age as the age of your previous birthday, decreasing your total coverage by one year. Great Eastern's latest credit rating from S&P is AA-. If you'd like to apply for this plan or learn more, speak with one of our advisors at PolicyPal.

| Sum Assured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | 5-Years | S$3.96 | S$4.83 | S$7.67 |

| 20-Years | S$4.38 | S$6.08 | S$12.08 | |

| Age 65 | S$6.33 | S$8.08 | S$11.71 | |

| S$200,000 | 5-Years | S$9.17 | S$12.67 | S$24.00 |

| 20-Years | S$10.83 | S$17.67 | S$41.67 | |

| Age 65 | S$18.67 | S$25.67 | S$40.17 | |

| S$400,000 | 5-Years | S$18.33 | S$25.33 | S$48.00 |

| 20-Years | S$21.68 | S$35.33 | S$83.33 | |

| Age 65 | S$37.33 | S$51.33 | S$80.33 |

Great Eastern's Direct-Great Term Life insurance is one of the cheapest options for older Singaporeans looking for up-to-age-65 plans, regardless of the amount you want to be insured for. For instance, a 55-year old consumer looking for an up to 65-year old plan will see premiums that are around 30% below the market average. On the other hand, Great Eastern is less competitively priced for 5 and 20-year plans and for younger consumers. Furthermore, age is defined as age at next birthday, as opposed to other plans that define your age as the age of your previous birthday, decreasing your total coverage by one year. Great Eastern's latest credit rating from S&P is AA-. If you'd like to apply for this plan or learn more, speak with one of our advisors at PolicyPal.

SingLife Direct Purchase Term Life Insurance

| Sum Assured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | 5-Years | S$3.02 | S$3.52 | S$6.07 |

| 20-Years | S$2.88 | S$4.63 | S$10.46 | |

| Age 65 | S$4.95 | S$7.21 | S$11.42 | |

| S$200,000 | 5-Years | S$10.33 | S$12.33 | S$22.51 |

| 20-Years | S$9.77 | S$16.78 | S$40.09 | |

| Age 65 | S$18.07 | S$27.07 | S$43.93 | |

| S$400,000 | 5-Years | S$18.91 | S$22.90 | S$43.28 |

| 20-Years | S$17.78 | S$31.80 | S$78.42 | |

| Age 65 | S$34.40 | S$52.40 | S$86.12 |

SingLife's Direct-Term Life insurance offers quite competitively priced plans for older consumers looking for low to mid-level coverage. Its Direct Purchase option offers death and total & permanent disability (TPD) coverage up to S$400,000 and also offers a critical illness rider. Its credit rating is currently BBB. If you'd like to apply for this plan or learn more, speak with one of our advisors at PolicyPal.

| Sum Assured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | 5-Years | S$3.02 | S$3.52 | S$6.07 |

| 20-Years | S$2.88 | S$4.63 | S$10.46 | |

| Age 65 | S$4.95 | S$7.21 | S$11.42 | |

| S$200,000 | 5-Years | S$10.33 | S$12.33 | S$22.51 |

| 20-Years | S$9.77 | S$16.78 | S$40.09 | |

| Age 65 | S$18.07 | S$27.07 | S$43.93 | |

| S$400,000 | 5-Years | S$18.91 | S$22.90 | S$43.28 |

| 20-Years | S$17.78 | S$31.80 | S$78.42 | |

| Age 65 | S$34.40 | S$52.40 | S$86.12 |

SingLife's Direct-Term Life insurance offers quite competitively priced plans for older consumers looking for low to mid-level coverage. Its Direct Purchase option offers death and total & permanent disability (TPD) coverage up to S$400,000 and also offers a critical illness rider. Its credit rating is currently BBB. If you'd like to apply for this plan or learn more, speak with one of our advisors at PolicyPal.

Term Life Insurance Options You Can Buy Online

FWD, Etiqa and SingLife also let you purchase traditional term life insurance policies online with death and terminal illness coverage that goes beyond the S$400,000 DPI limit. You may have the option of purchasing either a total & permanent disability or critical illness rider as well.

FWD COVID-19 Insurance

| Benefits | Limits |

|---|---|

| Policy Term | 100 days |

| COVID-19 Death Benefit | S$50,000 |

| COVID-19 Death Benefit (Frontliners) | S$100,000 |

| ICU Daily Cash Allowance (14 days) | S$100/day |

| Post-Hospitalisation Benefit | S$800 |

FWD's COVID-19 insurance is a short term life insurance policy that provides S$50,000 of death coverage. For people looking for short-term protection strictly for the duration of this pandemic, the coverage, non-committal policy term and flat fee of S$28 can make FWD's COVID-19 insurance an attractive choice. The death benefit for frontline workers is also doubled to S$100,000. Beyond the death benefit, there are also a couple of peace of mind benefits, such as an ICU daily cash allowance and a post-hospitalisation benefit to help you pay for outpatient treatment not covered by the government.

Please note that you will not be eligible to purchase this policy if you previously tested positive for COVID-19, have experienced COVID-19 symptoms, have been self-isolated or traveled in the past 30 days. There is also 14-day waiting period before the policy benefits kick in.

| Benefits | Limits |

|---|---|

| Policy Term | 100 Days |

| COVID-19 Death Benefit | S$50,000 |

| COVID-19 Death Benefit (Frontliners) | S$100,000 |

| ICU Daily Cash Allowance (14 days) | S$100/day |

| Post-Hospitalisation Benefit | S$800 |

FWD's COVID-19 insurance is a short term life insurance policy that provides S$50,000 of death coverage. For people looking for short-term protection strictly for the duration of this pandemic, the coverage, non-committal policy term and flat fee of S$28 can make FWD's COVID-19 insurance an attractive choice. The death benefit for frontline workers is also doubled to S$100,000. Beyond the death benefit, there are also a couple of peace of mind benefits, such as an ICU daily cash allowance and a post-hospitalisation benefit to help you pay for outpatient treatment not covered by the government.

Please note that you will not be eligible to purchase this policy if you previously tested positive for COVID-19, have experienced COVID-19 symptoms, have been self-isolated or traveled in the past 30 days. There is also 14-day waiting period before the policy benefits kick in.

FWD Term Life Plus Insurance

| Death & TPD Coverage (Fixed Term) | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$500,000 | 5-Years | S$16.93 | S$23.06 | S$47.10 |

| 20-Years | S$21.40 | S$32.49 | S$81.82 | |

| S$1,000,000 | 5-Years | S$34.47 | S$41.48 | S$101.03 |

| 20-Years | S$36.22 | S$55.16 | S$139.36 | |

| S$1,500,000 | 5-Years | S$51.70 | S$62.22 | S$151.55 |

| 20-Years | S$54.33 | S$82.75 | S$209.03 |

FWD offers a traditional term life plan, Term Life Plus, that let you purchase up to S$1,500,000 in death and terminal illness coverage online. You can either get this as a renewable option, where you can renew your policy each year, or a fixed term policy where you pay the same premiums throughout the selected period. Furthermore, in the event of your death, your spouse (provided they're younger than 55) will be eligible for term life cover of up to S$250,000 for 1 year.

Furthermore, FWD offers a unique Care Recovery feature, in which you will be connected with a nurse after you file a successful claim, who will answer your questions and provide dietary, physiotherapy, nutritional and other services. With a flexible design, this policy makes both the total & permanent disability benefit and critical illness benefit available as a rider.

| Death & TPD Coverage (Fixed Term) | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$500,000 | 5-Years | S$16.93 | S$23.06 | S$47.10 |

| 20-Years | S$21.40 | S$32.49 | S$81.82 | |

| S$1,000,000 | 5-Years | S$34.47 | S$41.48 | S$101.03 |

| 20-Years | S$36.22 | S$55.16 | S$139.36 | |

| S$1,500,000 | 5-Years | S$51.70 | S$62.22 | S$151.55 |

| 20-Years | S$54.33 | S$82.75 | S$209.03 |

Furthermore, FWD offers a unique Care Recovery feature, in which you will be connected with a nurse after you file a successful claim, who will answer your questions and provide dietary, physiotherapy, nutritional and other services. With a flexible design, this policy makes both the total & permanent disability benefit and critical illness benefit available as a rider.

Etiqa eProtect Term Life Insurance

| Death & TPD Coverage | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$500,000 | 5-Years | S$16.19 | S$23.19 | S$44.19 |

| 20-Years | S$18.81 | S$37.19 | S$93.19 | |

| Age 65 | S$38.06 | S$54.69 | S$88.81 | |

| S$1,000,000 | 5-Years | S$29.14 | S$41.74 | S$79.54 |

| 20-Years | S$33.86 | S$66.94 | S$167.74 | |

| Age 65 | S$68.51 | S$98.44 | S$159.86 | |

| S$2,000,000 | 5-Years | S$51.80 | S$74.20 | S$141.40 |

| 20-Years | S$60.20 | S$199.00 | S$298.20 | |

| Age 65 | S$121.80 | S$175.00 | S$284.20 |

Etiqa's eProtect term life plans provides between S$401,000 and S$2 million of death, terminal illness and total & permanent disability coverage. eProtect term life policy terms are either 5-years (as a guaranteed renewable), 20 years or up to age 65. We found its premiums to be especially competitive among S$1,000,000 coverage plans for young non-smoking consumers and S$2,000,000 coverage plans for middle-aged consumers. However, there is no option to add a critical illness rider to this plan.

| Death & TPD Coverage | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$500,000 | 5-Years | S$16.19 | S$23.19 | S$44.19 |

| 20-Years | S$18.81 | S$37.19 | S$93.19 | |

| Age 65 | S$38.06 | S$54.69 | S$88.81 | |

| S$1,000,000 | 5-Years | S$29.14 | S$41.74 | S$79.54 |

| 20-Years | S$33.86 | S$66.94 | S$167.74 | |

| Age 65 | S$68.51 | S$98.44 | S$159.86 | |

| S$2,000,000 | 5-Years | S$51.80 | S$74.20 | S$141.40 |

| 20-Years | S$60.20 | S$199.00 | S$298.20 | |

| Age 65 | S$121.80 | S$175.00 | S$284.20 |

Etiqa's eProtect term life plans provides between S$401,000 and S$2 million of death, terminal illness and total & permanent disability coverage. eProtect term life policy terms are either 5-years (as a guaranteed renewable), 20 years or up to age 65. We found its premiums to be especially competitive among S$1,000,000 coverage plans for young non-smoking consumers and S$2,000,000 coverage plans for middle-aged consumers. However, there is no option to add a critical illness rider to this plan.

Income iTerm Term Life Insurance

| Death & TPD Coverage (Fixed Term) | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$150,000 | 5-Years | S$10.90 | S$13.05 | S$24.25 |

| 20-Years | S$11.90 | S$19.45 | S$49.85 | |

| Age 64 | S$21.45 | S$32.85 | S$46.35 | |

| S$250,000 | 5-Years | S$16.50 | S$19.75 | S$36.75 |

| 20-Years | S$18.00 | S$29.50 | S$75.50 | |

| Age 64 | S$32.50 | S$49.75 | S$70.25 | |

| S$450,000 | 5-Years | S$51.80 | S$74.20 | S$62.20 |

| 20-Years | S$60.20 | S$33.40 | S$127.75 | |

| Age 64 | S$55.00 | S$84.20 | S$118.85 |

Income's iTerm term life insurance plan offers up to S$499,999 of death, terminal illness and total and permanent disability coverage. You can buy this plan online without going through a financial advisor. You can choose coverage terms between 5-35 years (in increments of 5) or choose to be covered up to the ages of 54, 64, or 74, with the ability to renew until age 84. There are also 4 riders you can get with iTerm, including a dread disease rider that will enhance your coverage to include cover for 32 dread diseases (for instance, major cancers, terminal illness, blindness or coma).

| Death & TPD Coverage (Fixed Term) | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$150,000 | 5-Years | S$10.90 | S$13.05 | S$24.25 |

| 20-Years | S$11.90 | S$19.45 | S$49.85 | |

| Age 64 | S$21.45 | S$32.85 | S$46.35 | |

| S$250,000 | 5-Years | S$16.50 | S$19.75 | S$36.75 |

| 20-Years | S$18.00 | S$29.50 | S$75.50 | |

| Age 64 | S$32.50 | S$49.75 | S$70.25 | |

| S$450,000 | 5-Years | S$51.80 | S$74.20 | S$62.20 |

| 20-Years | S$60.20 | S$33.40 | S$127.75 | |

| Age 64 | S$55.00 | S$84.20 | S$118.85 |

Income's iTerm term life insurance plan offers up to S$499,999 of death, terminal illness and total and permanent disability coverage. You can buy this plan online without going through a financial advisor. You can choose coverage terms between 5-35 years (in increments of 5) or choose to be covered up to the ages of 54, 64, or 74, with the ability to renew until age 84. There are also 4 riders you can get with iTerm, including a dread disease rider that will enhance your coverage to include cover for 32 dread diseases (for instance, major cancers, terminal illness, blindness or coma).

SingLife Term Life Insurance

| Death & TPD Coverage | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$500,000 | 5-Years | S$24.12 | S$26.71 | S$46.95 |

| 20-Years | S$28.74 | S$45.56 | S$105.27 | |

| S$1,000,000 | 5-Years | S$39.22 | S$45.26 | S$78.03 |

| 20-Years | S$41.98 | S$68.70 | S$S$153.05 | |

| S$2,000,000 | 5-Years | S$74.70 | S$86.20 | S$148.56 |

| 20-Years | S$79.87 | S$130.55 | S$290.66 |

SingLife's term life insurance policy allows consumers to purchase up to S$10,000,000 of death and terminal illness coverage online with the option to purchase total & permanent disability or critical illness riders. The premiums for SingLife's higher coverage plans are pricier for younger consumers compared to other insurers offering similar online plans, but the amount of coverage that you can purchase can be a benefit that may be worth the higher price. Speak to one of our advisors at PolicyPal if you'd like to apply for this product.

| Death & TPD Coverage | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$500,000 | 5-Years | S$24.12 | S$26.71 | S$46.95 |

| 20-Years | S$28.74 | S$45.56 | S$105.27 | |

| S$1,000,000 | 5-Years | S$39.22 | S$45.26 | S$78.03 |

| 20-Years | S$41.98 | S$68.70 | S$S$153.05 | |

| S$2,000,000 | 5-Years | S$74.70 | S$86.20 | S$148.56 |

| 20-Years | S$79.87 | S$130.55 | S$290.66 |

SingLife's term life insurance policy allows consumers to purchase up to S$10,000,000 of death and terminal illness coverage online with the option to purchase total & permanent disability or critical illness riders. The premiums for SingLife's higher coverage plans are pricier for younger consumers compared to other insurers offering similar online plans, but the amount of coverage that you can purchase can be a benefit that may be worth the higher price. Speak to one of our advisors at PolicyPal if you'd like to apply for this product.

Traditional Whole Life Insurance

| Insurer: | |||

|---|---|---|---|

| Plan Name | MyWholeLife Plan III | Star Assure | Life Treasure |

| Annual Premium^ | S$5,138 | S$4,777 | S$5,260 |

| Coverage | Death, TPD, Terminal Illness | Death, TPD, Terminal Illness | Death, TPD, Terminal Illness |

| Pay Premiums | Single, Between 5-25 years | 5-30 years up to age 64 | 10, 15, 20, 25 or 30 years |

| Features |

|

|

|

Whole life insurance products are quite complex and will require you to consider a number of factors, ranging from your lifestyle and financial needs to your ability to make premium payments. The first thing you'll do is narrow down the type of whole life insurance plan you want. Traditional whole life insurance is divided up into three portions: participating (par), non-participating (non-par) and investment-linked policies (ILP).

Participating whole life policies provide guaranteed and non-guaranteed benefits. The guaranteed benefits are the sum assured (the payout you get upon an insured event happening). Non-guaranteed benefits are bonuses you may receive in addition to the sum assured, which depend on the performance of the insurer's fund. On the other hand, non-participating policies only provide guaranteed benefits (i.e. the sum assured). Investment-linked policies are a combination of life insurance coverage and an investment component. Unlike par and non-par plans, you choose the investment funds rather than the insurer so you bear all the investment risk. Investment-linked policies are generally riskiest life insurance products.

While term life insurance will be the better (and cheaper) option for most people, there may be cases where you'll want greater protection. This includes people who want financial protection for their dependants, want supplemental retirement income or want to leave a financial legacy for future generations. For instance, if you want a savings feature (such as a cash value) with your policy so you can get more than just your sum assured at the end of the term, you can look into a participating whole life policy. On the other hand, if you want the flexibility to invest in the funds you want and have a long investment window (i.e. you are young, working and are experienced with investing), you may look into ILPs.

For all types of whole life insurance plans, we recommend getting coverage that is at least 10-15x your annual income. You should also take into consideration your debt obligations, financial obligations for your children, and lump sum benefits for your beneficiaries. Due to the complex nature of whole life insurance products, we recommend speaking with a financial advisor. Speak to our advisors at PolicyPal to get the best whole life insurance policy for you.

| Whole Life Policy |

|---|

|

|

|

Whole life insurance products are quite complex and will require you to consider a number of factors, ranging from your lifestyle and financial needs to your ability to make premium payments. The first thing you'll do is narrow down the type of whole life insurance plan you want. Traditional whole life insurance is divided up into three portions: participating (par), non-participating (non-par) and investment-linked policies (ILP).

Participating whole life policies provide guaranteed and non-guaranteed benefits. The guaranteed benefits are the sum assured (the payout you get upon an insured event happening). Non-guaranteed benefits are bonuses you may receive in addition to the sum assured, which depend on the performance of the insurer's fund. On the other hand, non-participating policies only provide guaranteed benefits (i.e. the sum assured). Investment-linked policies are a combination of life insurance coverage and an investment component. Unlike par and non-par plans, you choose the investment funds rather than the insurer so you bear all the investment risk. Investment-linked policies are generally riskiest life insurance products.

While term life insurance will be the better (and cheaper) option for most people, there may be cases where you'll want greater protection. This includes people who want financial protection for their dependants, want supplemental retirement income or want to leave a financial legacy for future generations. For instance, if you want a savings feature (such as a cash value) with your policy so you can get more than just your sum assured at the end of the term, you can look into a participating whole life policy. On the other hand, if you want the flexibility to invest in the funds you want and have a long investment window (i.e. you are young, working and are experienced with investing), you may look into ILPs.

For all types of whole life insurance plans, we recommend getting coverage that is at least 10-15x your annual income. You should also take into consideration your debt obligations, financial obligations for your children, and lump sum benefits for your beneficiaries. Due to the complex nature of whole life insurance products, we recommend speaking with a financial advisor. Speak to our advisors at PolicyPal to get the best whole life insurance policy for you.

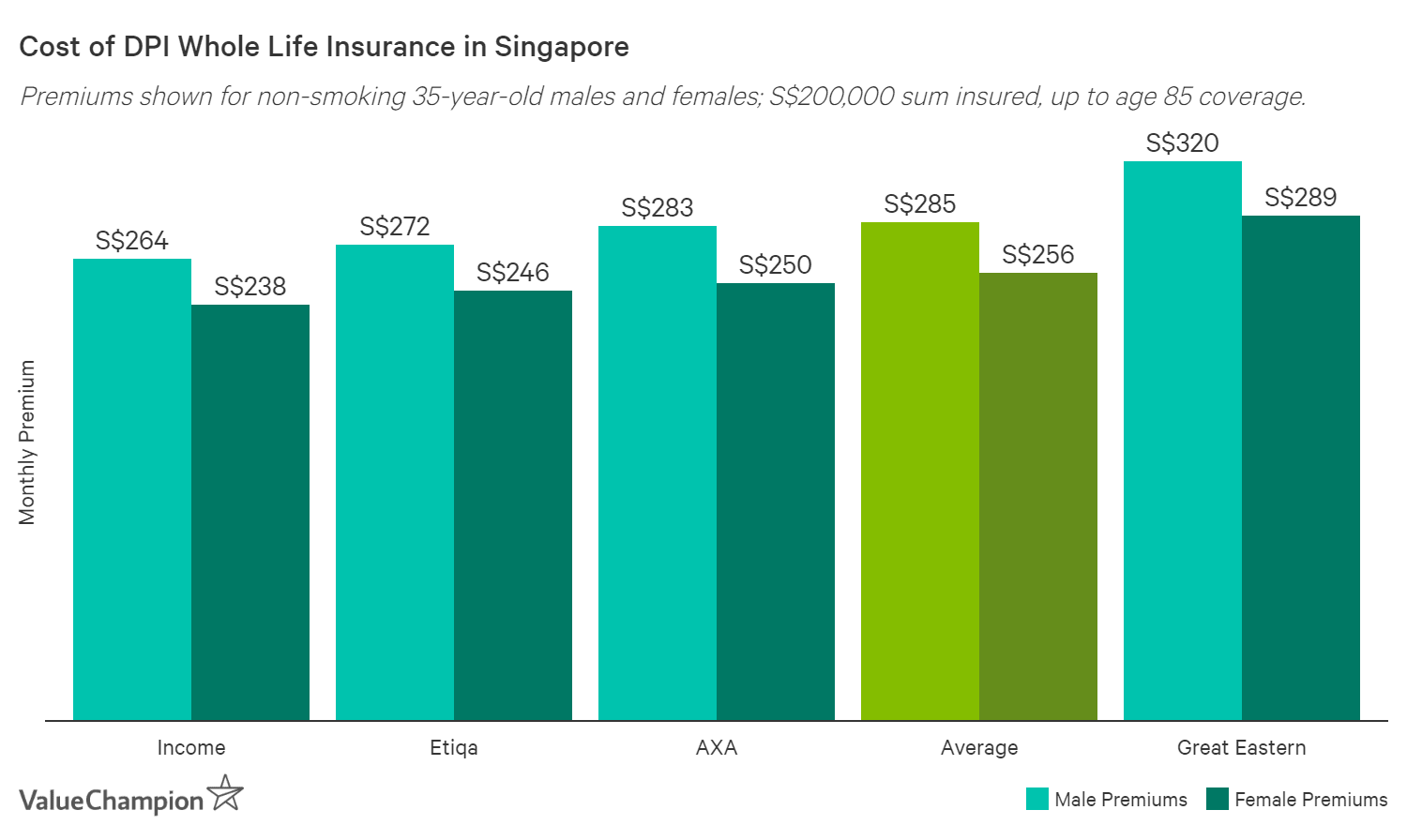

Cheapest Direct Purchase Whole Life Insurance

A whole life insurance policy provides lifetime financial protection, sometimes offers a non-guaranteed bonus and can build up cash value over time. Upon death or terminal illness, your policy will pay out a lump sum plus any of the bonuses accumulated. If you want a whole life policy that you can purchase online without going through an intermediary, you can consider a Direct Purchase Whole Life insurance plan. Since DPIs are standardised, you can purchase up to S$200,000 in death and coverage.

| Amount Insured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | Age 70 | S$58 | S$80 | S$123 |

| Age 85 | S$55 | S$74 | S$106 | |

| S$100,000 | Age 70 | S$110 | S$155 | S$241 |

| Age 85 | S$105 | S$144 | S$207 | |

| S$150,000 | Age 70 | S$165 | S$233 | S$362 |

| Age 85 | S$158 | S$215 | S$311 | |

| S$200,00 | Age 70 | S$217 | S$308 | S$480 |

| Age 85 | S$208 | S$285 | S$412 |

Etiqa's DIRECT – Etiqa whole life Insurance

| Sum Insured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | Age 70 | S$54.12 | S$74.42 | S$114.17 |

| Age 85 | S$51.39 | S$68.07 | S$96.56 | |

| S$100,000 | Age 70 | S$108.25 | S$148.85 | S$228.35 |

| Age 85 | S$102.79 | S$136.14 | S$193.12 | |

| S$150,000 | Age 70 | S$162.37 | S$223.27 | S$342.52 |

| Age 85 | S$154.18 | S$204.21 | S$289.68 | |

| S$200,000 | Age 70 | S$216.49 | S$297.70 | S$456.70 |

| Age 85 | S$205.57 | S$272.28 | S$386.24 |

Etiqa's Direct-Whole Life premiums are slightly below average. It offers up to age 75 and up to age 85 plans and will cover you up to S$200,000 until your death or a specified maturity date. There is also a cash value and reversionary bonus accumulation attached to the plan and you can add a critical illness rider. If you choose to pay your premiums annually, you will save around 2.3%. Etiqa's current credit rating is A-.

| Sum Insured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | Age 70 | S$54.12 | S$74.42 | S$114.17 |

| Age 85 | S$51.39 | S$68.07 | S$96.56 | |

| S$100,000 | Age 70 | S$108.25 | S$148.85 | S$228.35 |

| Age 85 | S$102.79 | S$136.14 | S$193.12 | |

| S$150,000 | Age 70 | S$162.37 | S$223.27 | S$342.52 |

| Age 85 | S$154.18 | S$204.21 | S$289.68 | |

| S$200,000 | Age 70 | S$216.49 | S$297.70 | S$456.70 |

| Age 85 | S$205.57 | S$272.28 | S$386.24 |

Etiqa's Direct-Whole Life premiums are slightly below average. It offers up to age 75 and up to age 85 plans and will cover you up to S$200,000 until your death or a specified maturity date. There is also a cash value and reversionary bonus accumulation attached to the plan and you can add a critical illness rider. If you choose to pay your premiums annually, you will save around 2.3%. Etiqa's current credit rating is A-.

Income DIRECT Star Classic Life Insurance

| Sum Insured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | Age 70 | S$51.00 | S$73.00 | S$112.50 |

| Age 85 | S$49.00 | S$66.00 | S$93.50 | |

| S$100,000 | Age 70 | S$102.00 | S$146.00 | S$225.00 |

| Age 85 | S$98.00 | S$132.00 | S$187.00 | |

| S$150,000 | Age 70 | S$153.00 | S$219.00 | S$337.50 |

| Age 85 | S$147.00 | S$198.00 | S$280.50 | |

| S$200,000 | Age 70 | S$204.00 | S$292.00 | S$450.00 |

| Age 85 | S$196.00 | S$264.00 | S$374.00 |

Income's DIRECT Star Classic Life insurance plan is competitively priced for older consumers compared to other DIRECT Whole Life plans. You will be protected against death and terminal illness until age 99 and total and permanent disability before you turn 65. Upon any of the claimable events, you will receive the sum assured and any accumulated bonuses. You can get a plan either up to age 70 or age 85, but you should note that plans that provide coverage until you turn 85 are slightly cheaper. Income's current credit rating is AA-.

| Sum Insured | Plan Tenure | Age 25 | Age 35 | Age 45 |

|---|---|---|---|---|

| S$50,000 | Age 70 | S$51.00 | S$73.00 | S$112.50 |

| Age 85 | S$49.00 | S$66.00 | S$93.50 | |

| S$100,000 | Age 70 | S$102.00 | S$146.00 | S$225.00 |

| Age 85 | S$98.00 | S$132.00 | S$187.00 | |

| S$150,000 | Age 70 | S$153.00 | S$219.00 | S$337.50 |

| Age 85 | S$147.00 | S$198.00 | S$280.50 | |

| S$200,000 | Age 70 | S$204.00 | S$292.00 | S$450.00 |

| Age 85 | S$196.00 | S$264.00 | S$374.00 |

Income's DIRECT Star Classic Life insurance plan is competitively priced for older consumers compared to other DIRECT Whole Life plans. You will be protected against death and terminal illness until age 99 and total and permanent disability before you turn 65. Upon any of the claimable events, you will receive the sum assured and any accumulated bonuses. You can get a plan either up to age 70 or age 85, but you should note that plans that provide coverage until you turn 85 are slightly cheaper. Income's current credit rating is AA-.

Best Savings Endowment Plans

An endowment plan is a savings plan with a life insurance component attached. If you are looking to save for the future,while also receiving supplemental coverage for death, and endowment plan could be a suitable option. Below, we provide two short-term savings plan and one long-term savings plan that will provide at least 100% capital guarantee at the end of your term with solid returns. If you would like to purchase one of these plans, or simply learn more, click on get a quote to be connected with one of our advisors at PolicyPal.

| Plan: |

Smart Secure

|

Goal 4

| MySavingsPlan

|

|---|---|---|---|

| Best For | Short-term savings | Short-term savings | Long-term Savings |

| Capital Guaranteed | 100% | 100% | 100% |

| Policy Term | 4 years | 4 years | 10-25 years |

| Premium Term | Single Premium | Single Premium | 10-25 years |

| Life Coverage | Death, TPD | Death | Death, Accidental Death, Terminal Illness |

| Yearly Cash Benefit | 25% of Sum Assured | 1.80% of Premium | None |

| Credit Rating | AA- | AA- | A- |

| Learn More | Full Review | Full Review | Full Review |

Income's Smart Secure is an endowment plan that only requires one single premium payment and has a short term of just 4 years. It is a general savings plan, which means you can use the funds to pay for anything you want once the term is over. There is a guaranteed cash benefit of 25% of your sum assured that will be disbursed yearly from the end of the first policy year. There is also a 100% capital guarantee, which means that your return will be at least 100% of the premiums you paid (in the form of guaranteed cash and maturity benefits), so you don't have to worry about losing money. However, please note this is as long as you made no policy alternatives or claims over the course of the policy term. The life insurance component provides coverage for death and total and permanent disability.

Manulife's Goal 4 endowment plan is another single premium, short-term savings plan that matures in 4 years. It provides guaranteed yearly income payouts with the option to reinvest them and receive a lump sum when your policy expires. The minimum premium is S$10,000 but you can pay this either in cash or with your Supplementary Retirement Scheme funds. Manulife's Goal 4 endowment plan offers an annual payout of 1.8% of your premium at the end of years 1 to 3, which is smaller than Income's but still a relatively generous amount. Upon policy maturity, you will receive at least 100% of your premiums and you may be eligible for a maturity bonus as high as 1.8% of your premium.

Aviva MySavings Plan can be a good option for people who are looking for long-term savings. It guarantees a 100% return on your premiums upon policy maturity and provides death, accidental death and terminal illness coverage. It can be suitable for long-term savers who want to commit between 10-25 years to a savings plan.

If you're interested in these plans and would like to learn more, please speak to one of our financial advisors at PolicyPal by clicking the "Get a Quote" button.

| Policy |

|---|

|

Smart Secure

|

|

Manulife Educate

|

|

Income's Smart Secure is an endowment plan that only requires one single premium payment and has a short term of just 4 years. It is a general savings plan, which means you can use the funds to pay for anything you want once the term is over. There is a guaranteed cash benefit of 25% of your sum assured that will be disbursed yearly from the end of the first policy year. There is also a 100% capital guarantee, which means that your return will be at least 100% of the premiums you paid (in the form of guaranteed cash and maturity benefits), so you don't have to worry about losing money. However, please note this is as long as you made no policy alternatives or claims over the course of the policy term. The life insurance component provides coverage for death and total and permanent disability.

Manulife's Goal 4 endowment plan is another single premium, short-term savings plan that matures in 4 years. It provides guaranteed yearly income payouts with the option to reinvest them and receive a lump sum when your policy expires. The minimum premium is S$10,000 but you can pay this either in cash or with your Supplementary Retirement Scheme funds. Manulife's Goal 4 endowment plan offers an annual payout of 1.8% of your premium at the end of years 1 to 3, which is smaller than Income's but still a relatively generous amount. Upon policy maturity, you will receive at least 100% of your premiums and you may be eligible for a maturity bonus as high as 1.8% of your premium.

Aviva MySavings Plan can be a good option for people who are looking for long-term savings. It guarantees a 100% return on your premiums upon policy maturity and provides death, accidental death and terminal illness coverage. It can be suitable for long-term savers who want to commit between 10-25 years to a savings plan.

If you're interested in these plans and would like to learn more, please speak to one of our financial advisors at PolicyPal by clicking the "Get a Quote" button.

Why Do I Need Life Insurance?

When you buy into a life insurance policy, your insurance company will provide a lump-sum payout to your family in the event that you become totally and permanently disabled, suffer a terminal illness or pass away. Life insurance is not necessary for everyone, but there are many scenarios in which you could benefit from a life insurance plan.

- If you are the sole breadwinner of your family, a life insurance plan can help relieve your spouse, children, and parents of any financial debt after you pass or are otherwise unable to work.

- People with hazardous jobs or hobbies have a bigger chance of dying. While they will likely need to pay higher premiums for this reason, a good life insurance policy can financially assist dependents in the case of an untimely death or disability.

- New parents and those with special needs children should consider life insurance while their kids are young and not yet self-reliant. If your children are older and able, then you don't necessarily need to invest in a long policy term because your kids are closer to an age of financial independence.

- If you are older and without savings, a life insurance policy can help your family or friends cover your funeral or any other lasting expenses.

- Adults with large amounts of debt can rely on a life insurance policy to help relieve any cosigners of the burden of payment. For instance, if your parents cosigned your private school loan, then they would not be expected to pay off your loans if your life insurance payout covered the costs.

Read More: 10 Important Life Insurance Terms You Should Know

When Do I Get Life Insurance?

The younger you are, the cheaper your life insurance premium will be. For instance, whole life insurance for children will be much cheaper than a working adult, as a child likely has less health risks. Similarly, working adults will find the lowest premiums in their 20s, when they are healthy and less likely to get sick.

Some young people may think that they do not have enough assets or debt to justify a life insurance plan. However, anyone with dependents will greatly benefit from buying a life insurance plan early on, so that they pay the least to provide the most financial protection to their loved ones in the case of an unforeseen accident.

Rad More: Average Cost & Benefits of Direct Purchase Life Insurance

Types of Life Insurance

The purpose of life insurance is to provide a lump-sum payout to your family in the event that you are permanently incapacitated by a disability, illness or death. However, there are 3 main types of life insurance to choose from: whole life, term life, and universal life insurance.

Whole Life Insurance

Whole life insurance provides lifelong protection with possible cash returns, depending on if you invest in a participating, non-participating, or investment-linked policy. A whole life insurance policy is usually more expensive than a term life insurance policy, as it's meant to build up cash value through the investment of part of your premium. With this in mind, older individuals who want to leave a legacy for their dependents can make great use of a whole life insurance plan.

Term Life Insurance

Term life insurance will provide financial protection for a fixed period of time, and generally not past the age of 75. For instance, if you invest in a term life policy of 10 years, then you and your family can only receive a lump sum payout if a claimable event occurs within those 10 years. If a claimable event doesn't happen in that time span, the policy will end and you will not get any payouts. Additionally, you do not have the opportunity of cash returns with a term life plan. For these reasons, term life insurance is cheaper than whole life insurance.

Universal Life Insurance

Universal life insurance consists of whole life benefits, but gives the insured the opportunity to change premiums and sum assured amounts. This type of insurance is generally offered to high net-worth individuals interested in legacy planning. In Singapore, they're not as common as whole or term life insurance plans and are typically denominated in USD.

How Do I Find the Best Life Insurance Plan?

We researched all the term and whole life insurance plans available in Singapore to help you discover which policies are available, their features and whether they may be a fit for you. As a rule of thumb, term life is best for younger couples and individuals as it is cheaper than whole life insurance. On the other hand, those looking to leave a legacy for their children and grandchildren and need high levels of coverage pay find whole life insurance more suitable. As with all long-term commitments, you should be sure to discuss your preferred life insurance product with your financial advisor before purchasing.

Methodology

To accurately represent the life insurance products featured on this page, we gathered quotes for non-smoking males and females of a variety of ages. We then compared how each insurer's premiums compared to their peers in order to see which plan offered more competitive rates for different demographics. For continuity's sake, premiums for non-DPI term life plans that you can purchase online included total & permanent disability riders since these plans are similar to DPI plans which already include total & permanent disability in their base coverage. For plans where pricing wasn't available, we separated plans based on the category of life insurance they fell under as well as the different features offered.

| Insurance Companies Sampled | ||

|---|---|---|

| FWD | Etiqa | Income |

| ManuLife | SingLife | AIA |

| AXA | Aviva | Great Eastern |

| Prudential | Tokio Marine | Raffles Medical |

Disclaimer

Regardless of the policy you are thinking of getting, analysing all of your life insurance options and speaking to a licensed financial advisor is key to making sure you are getting the right plan. We do not claim to endorse, promote or recommend any product on this page. All products listed here are examples of different types of life insurance and their benefits and is meant to be for educational purposes only.

Read More:

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.