Average Cost of Car Loans 2024

Find the Cheapest Car Loans in Singapore

Cars are almost impossible to purchase without a loan in Singapore. This is because import duty and cost of COE add up to a significant amount mover S$100,000 even for a mass-market car. If you are planning to buy a car with a car loan, it’s important to know what a car loan costs on average, and what factors can impact this cost. In this guide, we analyze the average cost of car loans in Singapore and various factors that can influence this cost.

Table of Contents

- Average Cost of Car Loans in Singapore

- Rest Rate vs Flat Rate

- Factors That Influence Cost of Car Loans

- Who Can Get Car Loans In Singapore

Average Cost of Car Loans In Singapore

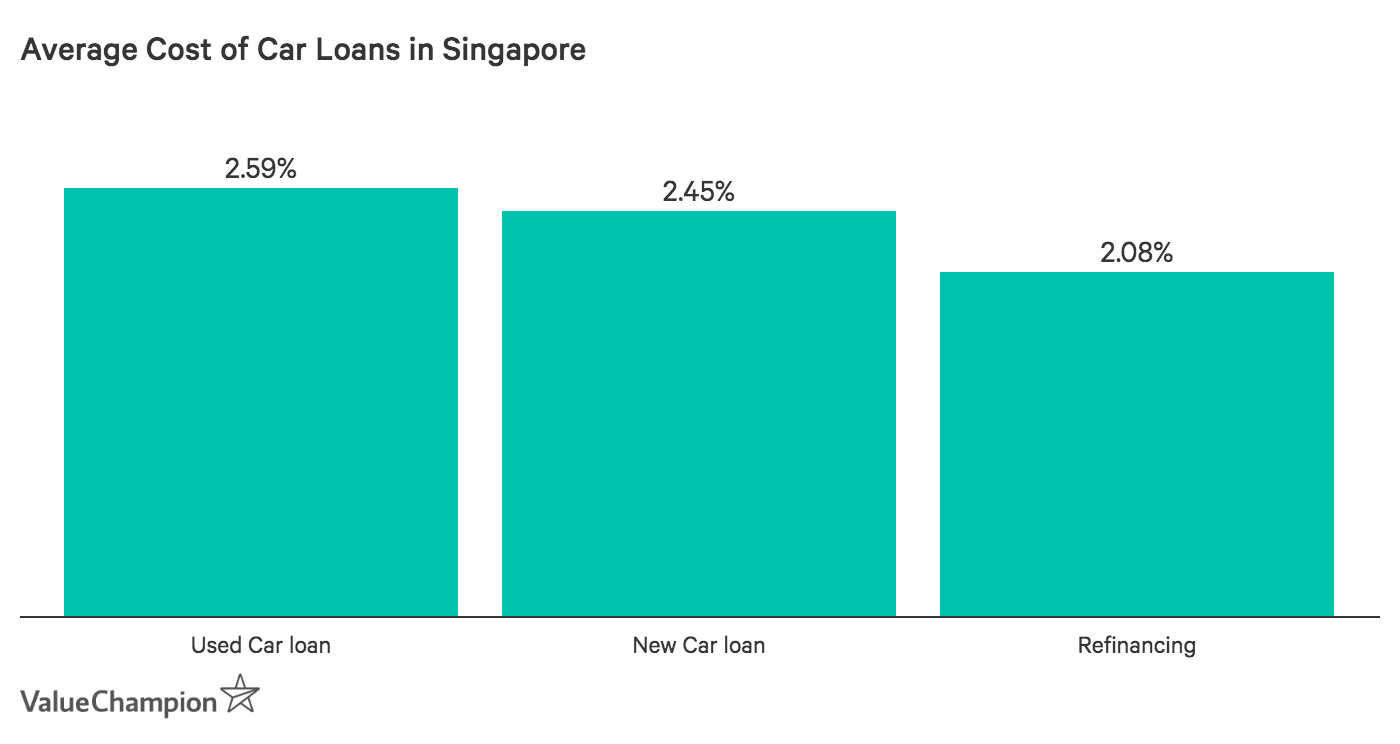

Car loans in Singapore are typically categorized into three categories: 1) car loans for new cars, 2) car loans for used cars and 3) car loans for refinancing. Also, there are a number of different providers for this type of loan: banks and financial leasing companies. We’ve collected as much data as we could find on the cost of these loans from different providers to arrive at the average cost below. On average, new car loans cost about 2.49% of interest per year, while used car loans cost about 2.59% of interest per year. Used cars cost more because lenders perceive these borrowers to be riskier than new car buyers due to the difference in their perceived income. These rates also compare to 2.78% and 3% from the best new car and used car loans in Singapore.

Rest Rate vs Flat Rate

It’s important to understand that car loans in Singapore are priced with “flat” interest rates, as opposed to “rest” interest rates. In contrast, home loans tend to be priced with rest rates. The difference between the two rates is that flat rates tend to be more expensive than rest rates because of the way they are calculated. Let’s examine this difference in detail. Let’s consider a car loan of S$50,000 over 5 years with a flat interest rate of 2.5%. Because this car loan comes with a “flat rate,” your interest is a “flat,” constant payment of S$50,000 x 2.5%, which translates to S$1,250 of interest expense each year. Your monthly instalment will be a constant amount consisting of S$104.17 (S$1,250 divided by 12 months) plus a principal payment of S$833 (S$50,000 divided by 60 months). After 5 years, you will have repaid your debt in full after having paid S$6,250 in interest. The key principle to understand here is that interest payment is kept “flat” no matter how much money you repay.

| Flat Rate | |

|---|---|

| Principal | S$50,000 |

| Interest Rate | 2.50% |

| Tenure | 5 Years |

| Monthly Instalments | S$938 |

| Total Interest | S$6,250 |

Now, let’s consider a home loan of S$50,000 over 5 years with an interest rate of 2.5%. Because a home loan in Singapore is priced with a “rest” interest rate, your interest expenditure is calculated based on the remaining balance of your loan after each month. This means that your monthly payment will be about S$887.37, which consists of an increasing amount of principal and decreasing amount of interest payment over time. Because the interest rate is applied only to the remaining balance (as opposed to the beginning balance for flat rates), you end up paying only S$3,242.08 in interest over 5 years, almost half of the cost a corresponding car loan.

| Flat Rate | |

|---|---|

| Principal | S$50,000 |

| Interest Rate | 2.50% |

| Tenure | 5 Years |

| Monthly Instalments | S$887 |

| Total Interest | S$3,242 |

Factors That Influence Cost of Car Loans

Different factors can change the cost of your car loan. Below is a brief discussion of each of the main variables so you have a better idea of what to expect in the future when you are shopping for a car and a car loan.

Market Interest Rates

Many car loans are priced around the prime lending rate in Singapore. A prime lending rate is the lowest lending rate which a bank is prepared to lend in Singapore Dollars to its best customers on an overdraft or demand basis. This changes all the time, and you can check out what it is at the beginning of each month on ABS’s website. If prime lending rates increase, car loan rates could increase along with it.

Tenure vs Principal

When considering the cost of a car loan, you must think about the balance between total interest cost and monthly instalments. Ideally, you want to borrow as much as you need at the lowest rate possible. This means that you want to minimize total interest cost while making sure you can comfortably manage your monthly payment. Shop for the best rate, but make sure you only borrow an amount that you can manage. Most car loans in Singapore will allow you to borrow up to 70% of your car’s open market value (purchase price for new and used cars).

Credit Score

Car loans can be priced higher if your credit score is low. This means that it’s very important to pay your credit card and other financing bills on time every month. Not only that, if you already have a home loan, a lender may deem you to be too indebted & thus charge a higher interest rate to compensate. Therefore, it’s often wise to purchase your home first before buying your car.

Who Can Get Car Loans In Singapore

Anyone at least 21 years of age with a good enough credit score and income can get a car loan in Singapore, though foreigners need an employment pass and a local guarantor. While most banks require an annual income of S$24,000 to qualify for a car loan, some lenders will require an annual income of up to S$30,000. If you are shopping for a car loan now, you can check our hand-picked selection of the best car loans in Singapore

Read More:

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.