Best Home Mortgage Loan Refinancing 2024

Refinancing your home loan can save you thousands of dollars over its tenure. To help, our researchers analysed hundreds of live interest rates to allow you to find the best mortgage rates currently available. Besides identifying low interest rates, it is important to consider interest rate structure, the total cost of borrowing as well as the flexibility to refinance again.

With the hike in interest rates for property loans in Singapore, some homeowners might want to consider refinancing their mortgage loans to fight against the increase. You can check out PropertyGuru's SmartRefi tool today to find out how much you can save from refinancing your mortgage loan:

Find the Cheapest Home Loans in Singapore

Best Home Loan Refinancing for HDB Flats

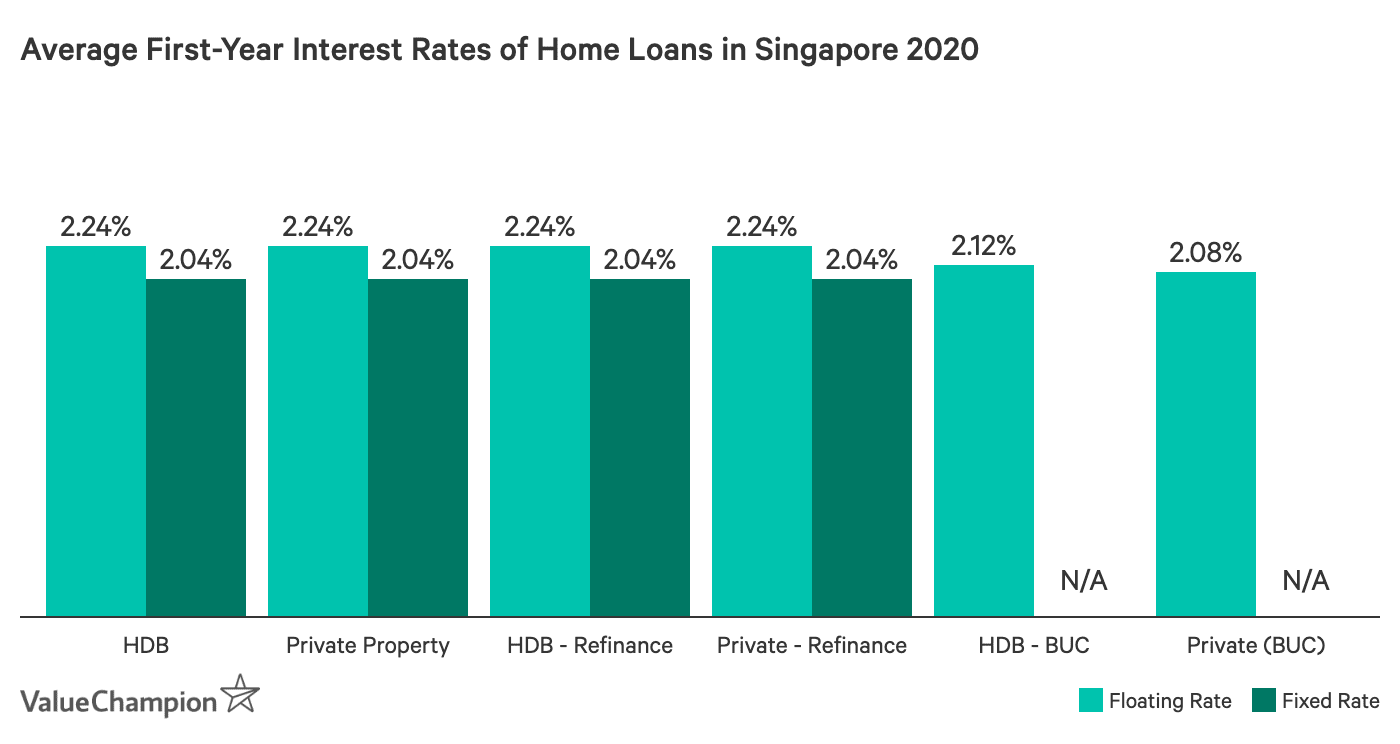

Approximately 4 out of 5 Singaporeans live in HDB flats, making these homes the most popular by far. Furthermore, refinancing is very common among individuals with mortgages on their HDB homes. In Singapore, borrowers typically refinance every few years, which makes it important to keep up to date with the best home loan refinance rates and obtain an affordable lender.

Best Fixed Rates for Home Loan Refinancing as of January 25, 2024

| Bank | Monthly Instalment | 1st Yr Interest | Lock-in Period | |

|---|---|---|---|---|

| No offerings at this time |

| Bank | 1st Yr Interest | Lock-in Period | |

|---|---|---|---|

| No offerings at this time |

We have found that the best fixed rate refinance rates offered by banks in Singapore tend to be about 10% to 15% cheaper than the average fixed rate refinance loan. Therefore, by choosing one of the cheapest refinance rates from our list can save you up to S$30,000 compared to the average fixed rate home loan refinancing. Find the best refinancing offer by connecting with our mortgage broker partner using the links in the table above.

In addition to choosing a loan with a low rate, it is also essential to consider how much the loan you each month in terms of monthly instalments. Similarly, it is important to consider whether you'd like the flexibility to refinance your loan sooner rather than later. To compare these options, you should keep an eye out for "lock-in" periods, which dictate the length of the period in which you are unable to renegotiate the terms of your loan. For example, some banks will let you refinance after just one year, while other banks will have lock-in periods of up to 3 years.

Best Floating Rates for Home Loan Refinancing as of January 25, 2024

| Bank | Monthly Instalment | 1st Yr Interest | Lock-in Period | |

|---|---|---|---|---|

| No offerings at this time |

| Bank | 1st Yr Interest | Lock-in Period | |

|---|---|---|---|

| No offerings at this time |

While fixed rate refinancing gives borrowers the ability to secure a given interest rate for a set period of time, borrowers can also choose to refinance their home loan with a floating rate loan, which charges interest rates based on reference rates that continuously change over time. In Singapore, we follow the Singapore Overnight Rate Average Interest Rate Benchmark, also known as SORA.

The best floating rate home loan refinancing products, which are listed above, tend to be about 10% to 15% lower than the average of floating rate home loans according to our research. Therefore, choosing one of the cheapest options from our table below can save up to S$30,000 compared to some of the average offerings available in Singapore. Find option for you by connecting with our mortgage broker partner by using the links above.

Best Home Loan Refinancing for Private Properties

While private residences are less common than HDB flats in Singapore, these condos and landed properties can easily cost several millions of dollars, requiring many private homeowners to resort to home loans. Below, we explain various private home loan refinancing options available in Singapore, and highlight the most affordable refinancing loans.

Best Fixed Rates for Home Loan Refinancing as of January 25, 2024

| Bank | Monthly Instalment | 1st Yr Interest | Lock-in Period | |

|---|---|---|---|---|

| No offerings at this time |

| Bank | 1st Yr Interest | Lock-in Period | |

|---|---|---|---|

| No offerings at this time |

When choosing fixed rate loan refinancing, it is important to minimise your total interest cost while also being able to ensure that you can afford to pay your monthly installment every month. It is also helpful to consider the flexibility of each loan, as some loans offer shorter lock-in periods that can allow you to refinance your loan again more quickly, which can sometimes reduce your total interest cost or monthly instalments. Typically, fixed rate home loans include a fixed interest rate for 2 to 3 years, after which interest rates change based on SORA. This means you'll have the opportunity to refinance again after the lock-in period ends.

Our review of the best fixed rate home loan refinancing for private homes indicates that the cheapest rates, offered by the banks in the table below, are typically 5% to 10% lower than the market average. By choosing one of the cheapest home loan refinancing options can save you up to S$30,000 in total interest cost compared to the average refinancing option. Use the table above to get the best refinancing rate through our home mortgage broker partner.

Best Floating Rates for Home Loan Refinancing as of January 25, 2024

| Bank | Monthly Instalment | 1st Yr Interest | Lock-in Period | |

|---|---|---|---|---|

| No offerings at this time |

| Bank | 1st Yr Interest | Lock-in Period | |

|---|---|---|---|

| No offerings at this time |

While fixed rate refinancing allows borrowers to choose a refinancing option with a set interest rate, floating rate refinancing features interest rates that continuously change of time. Banks typically charge floating interest rates based on SORA and these rates continuously move over time, hence the name "floating." When comparing various interest rate types, it helps to consider what your expectations for interest rate movement. For example, in general, it makes sense to go with a long-term rate in a rising rate environment; in a declining to flat environment, go with a short-term rate.

Our analysis indicates that the banks with the best floating rates for home loan refinancing for private residences charge interest rates that are approximately 10% to 15% cheaper than the market average. Therefore, by choosing one of the cheaper options from our list, you can you save as much as S$30,000 compared to refinancing with some of the other lenders in the country. To obtain one of these rates, connect with our home loan broker partner using the links in the table above.

Best Refinancing for Jumbo-Size Home Loans

Jumbo-sized home loans, which are very large mortgages, help individuals purchase very expensive homes. Many banks in Singapore actually offer special rates for jumbo loans, typically these lenders offer better interest rates for loans of at least S$1,000,000 to S$2,000,000. The table below lists the best refinancing options for jumbo-size home loans. Find the best option for you by connecting with our mortgage broker partner using the links below.

Best Refinancing Rates for Jumbo Home Loans as of January 25, 2024

| Bank | Monthly Instalment | 1st Yr Interest | Lock-in Period | |

|---|---|---|---|---|

| No offerings at this time |

| Bank | 1st Yr Interest | Lock-in Period | |

|---|---|---|---|

| No offerings at this time |

According to our analysis, the banks with the lowest refinancing rates for large mortgage loans had rates that are 10% to 15% lower than the market average. Given this difference in rates, and the sheer size of these loans, the best refinancing options can offer very significant savings, of as much as S$50,000 to S$100,000, over the course of the loan tenure compared to offerings from other lenders.

How to Choose the Best Home Loan Refinancing

Home loans can be a daunting financial products for consumers. While they appear to be straightforward, these loans are actually quite complex. Not only do home loan interest rates change frequently, the cheapest loan type can also change depending on trends in the lending market. Additionally, home loans typically require 10 to 20 documents as part of the application, which further complicates the process. Due to these complexities, we recommend that you consult a mortgage broker when shopping for a home loan. With that said, we encourage you to do your own research in order to find the most affordable home loan refinancing possible.

Why Should You Consider Refinancing Your Home Loan?

According to our research, most homeowners in Singapore refinance their home loans very frequently; about once every 2 to 4 years. While this trend may be influenced by a decline in interest rates in recent years, home loan refinancing can be a great tool for any homeowner.

Here are the top two reasons to refinance your current home loan:

- Lower interest rates

- Lower monthly payments

When applying to refinance your home loan, lenders will often enquire about your current loan's interest rate, and try to quote you a lower interest rate in order to win or maintain your business. This can work out well for homeowners who can refinance their current home loan and reduce their monthly installment and total cost of borrowing. Please keep in mind that most banks require a remaining loan balance of at least S$100,000 and at least 5 years. There are always exceptions, so make sure to check with our mortgage broker (using any of the buttons on this page), before ruling out refinancing!

With lower interest rates, you will enjoy lower monthly payments. If you choose to forego refinancing your existing mortgage loan, your interest rate will almost always increase leading to higher monthly instalments and total interest costs.

When Should You Refinance Your Current Home Loan?

It is important to choose the right time to refinance your current mortgage loan. Banks require a 3-month notice before refinancing and switching banks. So it is important you know when your lock-in period ends, in order to refinance your housing loan at the right time. Although you can refinance during your lock-in period, you will incur penalty fees. Plan ahead and give yourself at least 4 months to begin the refinancing process.

Find the Cheapest Home Loans in Singapore

Home Loan Costs: Interest Expense & Refinancing Fees

Prospective homeowners are typically most concerned with interest rates when comparing home loans and home loan refinancing. This is logical because interest rates dictate the majority of a home loan's cost. Additionally, because the credit criteria that banks use to approve a home loan application are nearly identical, your credit score is not a significant factor that influences borrowers' decisions to choosing one bank over another, which allows borrowers to focus on interest rates.

Aside from interest rates, borrowers should be aware of each loan's flexibility in terms of renegotiating terms and refinancing. This is important to Singaporeans, as most homeowners in Singapore refinance their home loans every 2 to 4 years. For this reason, it is important to keep an eye out for restrictions and fees such lock-in periods, legal fees, valuation fees and fire insurance premiums, which can reduce your savings from refinancing.

For instance, consider a home loan of S$500,000. By refinancing from 2.0% annually to 1.5% per year, you can save S$2,500 per year. However, legal fees in Singapore can cost about S$2,500, while valuation fees can range from S$500 to S$1,000. Additionally, some lenders charge an additional fee to borrowers that refinance during their loan's lock-in period. Below is a list of fees associated with home loan refinancing.

Various Fees Involved in Home Loan Refinancing

| Miscellaneous Fees In Refinancing | Cost |

|---|---|

| Legal Fee | S$1,600-S$2,200 |

| Valuation fee | S$250-S$1,000 |

| Fire Insurance | S$120/annum |

| Partial/Full Redemption Fees | 1.5% |

| Cancellation Fees | 0.75%-1.5% |

| Pricing Reset Date Penalty | 0.5%-1.5% of amount prepaid |

How to Choose Between Fixed & Floating Home Loan Refinancing Rates

One of the most difficult questions to answer when trying to refinance your home loan is whether to choose a fixed or floating rate loan. Both loans are valuable depending on the context of your loan and interest rates in the country. When trying to decide whether you should refinance with a fixed or floating rate, it is important to understand how rates will behave during the next 2 to 4 years (the years of a lock-in period) and how that impacts your total cost of borrowing. It is not necessary to consider a much longer time horizon because you can always refinance your loan after your lock-in period concludes. Below, we discuss a few possible scenarios that you must consider, and whether fixed or floating rate is more preferable depending on the context of each situation.

When Rates are Flat or Declining: Floating Rate

If interest rates are relatively stable or declining, it is generally prudent to refinance your home loan with a floating interest rate. Floating rates tend to be lower than fixed rates because banks are willing to offer a lower rate in the short-term, in order to obtain your business and charge you higher rates once market interest rates increase. On the other hand, fixed rates tend to be slightly higher as banks charge a premium for loans with set rates.

When Interest Rates are Rising: Fixed Rates

When overall interest rates are rising, it is generally advisable to refinance with a fixed rate than a floating rate. Although fixed rates are typically a bit higher than floating rates, they provide borrowers an opportunity to save if market rates rise significantly. For example, imagine that you are able to refinance at a fixed rate of 1.5% for the next three years or the option of refinancing at a floating rate beginning at 1%. If market interest rates rise soon after you refinance the floating rate could end up being 2% to 3%, while the fixed rate would remain at 1.5%. While these may not seem very significant, the difference could actually result a difference of S$5,000 in annual interest.

Methodology

We conducted our review based on data available online and from our home loan broker partner. We reviewed home loan products from the lenders below. We examined loan data that would be most relevant to potential borrowers, including interest rates, lock-in periods, fees, and subsidies.

Home Mortgage Loan Refinancing Frequently Asked Questions

Have a question about mortgage loan refinancing? We have the answer.

The lock-in period refers to the minimum number of years required to stay with the current bank issuing the mortgage loan. During this period, if you choose to refinance, partially repay or fully repay the loan, you will likely be hit with penalty fees.

Home mortgage loan rates change daily and the best home loan might not be the same since you've last checked. It is important to check regularly leading up to when you would like to take out a home loan or refinance your current mortgage loan. We make it easy and compare the best up to date home loans for you.

Repricing is when you change your interest rate package under the same bank. There are repricing fees that usually range between S$800 and S$1,000. Since banks will usually offer lower rates to attract new customers, the repricing package offered by the current bank tends to be worse than shopping for another bank. If you can find an attractive offer from another bank, refinancing your home loan can save you a lot of money.

There is no limit to the number of times you can refinance your loan. As long as you can save on your interest rate, you should consider refinancing your home loan every few years.

Read More:

Stephen Lee is a Senior Research Analyst at ValueChampion, specializing in insurance. He holds a Bachelor of Arts degree in International Studies from the University of Washington, and his prior work experience include risk management and underwriting for professional liability and specialty insurance at Victor Insurance. Additionally, Stephen is a former US Peace Corps Volunteer in Myanmar (serving between 2018-2020), where he continues to provide business development consulting services to HR companies in Asia Pacific.