Debt Consolidation Loan vs Balance Transfer: How to Escape Your Credit Card Debt

In Singapore, household debt is on the rise, and consumers are finding themselves under increasing financial burden of their debt. In particular, personal loans and credit card debt have been two of the main culprits contributing to the bloated consumer balance sheet in the recent years. In face of rising unemployment rate and lagging income growth, consumers have had to resort to borrowing in order to continue their consumption spree. However, with interest rates set to rise in the US and therefore possibly also in Singapore, it's about time for people to start actively planning to pay down their debt. Here, we discuss the two 2 main types of personal loans that help you do just this: balance transfers and debt consolidation plans. Read our guide below to find out how you can choose between the two options.

Balance Transfers vs Debt Consolidation Plans: How They Differ

While these two loan facilities have similar functions, they have important distinctions that make them useful for different kinds of people and usages. A balance transfer provides you with a "interest free period" ranging from 3 months to 1 year, during which time you can pay down your credit card debt without incurring the usual interest of 25% or higher. For this privilege, banks tend to charge a one-time processing fee ranging from 1.5% to 5.5%. In contrast, a debt consolidation plan is an instalment loan that lends you a lump sum, which you can use to pay off your existing debt right away. Then, you would have to repay the new loan over 1 to 10 year period.

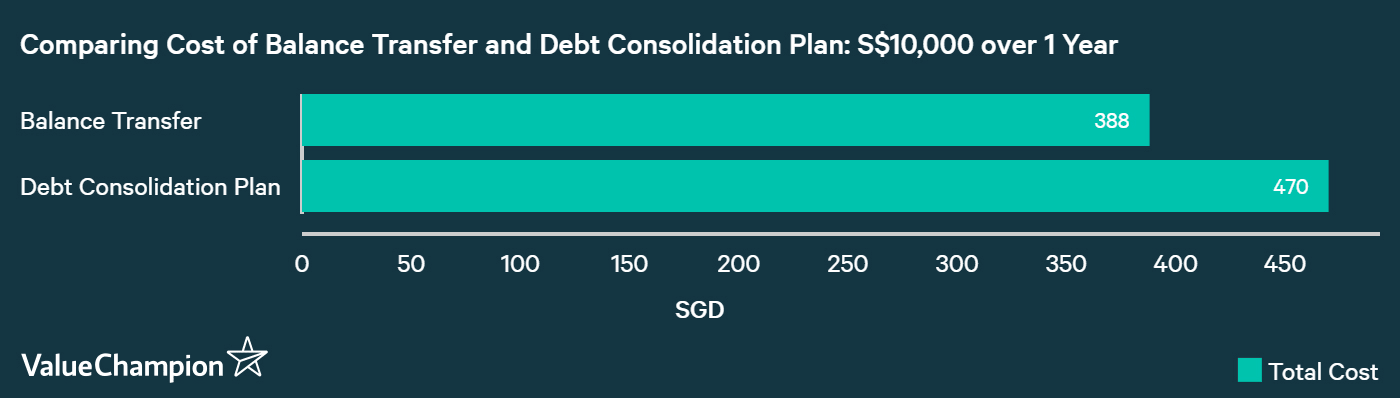

To demonstrate their differences, let's go through a real life example. Let's assume that you have an unpaid credit card balance of S$10,000 that you need to pay off. If you use a 12-month balance transfer, it'll cost you 3.88% in processing fee (or S$388) as long as you pay the loan back in entirety by the 12th month. On the other hand, a 1-year tenure of debt consolidation plan will cost you 4.7% of interest, translating to about S$470 of total cost. Not only that, a balance transfer requires you to make only a "minimum monthly repayment" until you make a lumpsum payment at the end to payoff the whole thing, though you can definitely repay as much as you like at any time. On the other hand, a debt consolidation plan requires you to adhere to a fixed, consistent monthly repayment schedule.

Which Is Right For You?

When deciding between getting a balance transfer loan and getting a debt consolidation plan, the most important factor that should sway your decision is how much time you need to repay your loan, not how big your unpaid card bill is. The rule of the thumb is this: If you make enough money to repay your balance within 12 months, you should go for a balance transfer. If you need more than 1 year to payoff your loan in full, you should go for a debt consolidation plan.

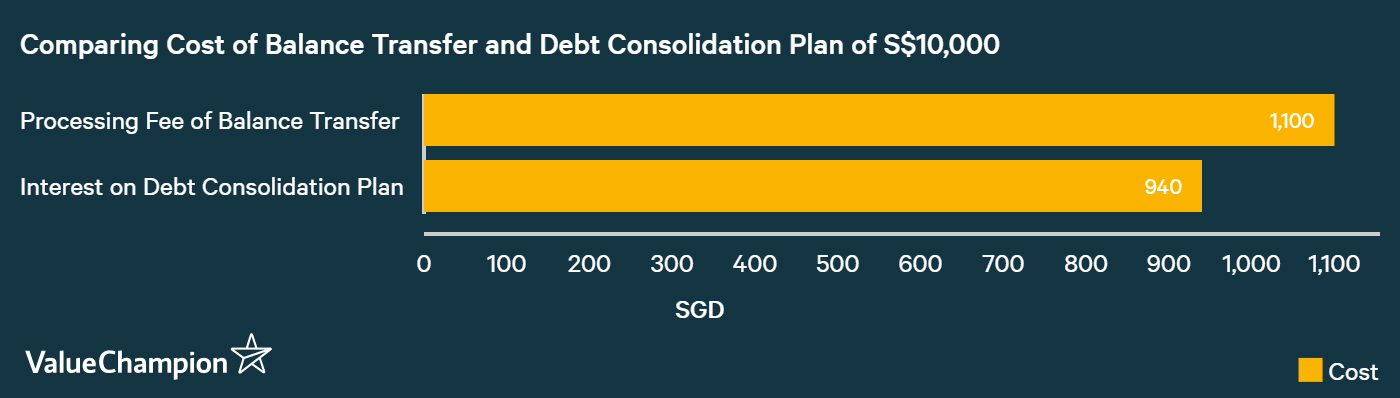

Our example in the previous section is a good example demonstrating this rule's effect. Because the loan is for 1 year, a balance transfer was 17% cheaper than the alternative. However, it can cost you a lot less to go with a debt consolidation plan if you have enough balance that you need to spend 2 years or longer to pay it down. By spreading out your loan repayment for longer than 1 year (2-10 years), it can lighten the burden of debt repayment on your daily lifestyle. In contrast, balance transfers charge you an astronomical rate of 26% or higher after your 12-months of grace period. Below, we compare the cost of a debt consolidation loan and balance transfer loan of S$10,000 over 2 years. For balance transfer loan, we assuem that you only pay off 50% of your balance in 12 months, and gradually pay down your debt throughout your 2nd year. Doing so should cost you almost S$1,100 of interest and fees, 17% higher than S$940 of interest you would've paid on your debt consolidation loan.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.