MAS $7.4 Billion Net Loss – Why, How This Affects Us, And What We Can Do

The Monetary Authority of Singapore (MAS) has reported a net loss of $7.4 billion in the financial year ended 31 March 2022. Additionally, Singapore’s official foreign reserves also recorded a net loss of $4.7 billion.

What could have caused the substantial loss and performance of Singapore’s central bank? Should we be worried about this? We examine the contributing factors, as well as impacts this could have on Singaporeans.

Table of Contents:

- Factors Leading To This Fiscal Performance

- Impact On The Singapore Economy

- Impact On Individual Singaporeans

- Most Of Us Will Be Able To Tide Over The Uncertain Outlook

- How Do I Cope With The Impacts Of Inflation?

- Conclusion

Factors Leading To This Fiscal Performance

Let us take a closer look at the reasons behind MAS’s fiscal performance this year. Some of the major contributing factors include inflation, unsteady global economic growth and MAS’s monetary policies.

1. Large Negative Foreign Exchange Translation Effect

A major portion of MAS’s huge loss is its net loss in Singapore’s official foreign reserves (OFR), amounting to $4.7 billion.

According to the MAS, the loss largely comes about due to a huge negative currency translation effect.

The MAS OFR is held in foreign currencies; according to the Central Bank, three-quarter of the OFR is held in USD, euro, yen and pound, majority of which is held in USD.

A CNA report back in July reported that the Singapore dollar is performing well against the euro and pound, and is at an all-time high against the yen.

As MAS report its profit in Singdollars, the appreciation of Singdollars mean that you'll get lesser SGD when translating your foreign currency into the local currency. This is the main reason why the OFR saw a net loss of S$4.7 billion despite making a profit of S$4 billion in foreign investments.

2. Total Expenditure Increased to $2.8 Billion Due To Higher Interest Expense

MAS also spent a bigger sum this year as compared to previous years, mostly due to the higher interest rates causing higher expenses on Singapore’s domestic money market operations.

One of the core reasons behind all these measures is the rising core inflation in Singapore.

Core inflation has hit a new high of 4.4% year-on-year in June. The prices of food, utilities, transport and more have surged and many of us have surely seen and felt the impact. The increase in inflation this time round is sharp, which makes it all the more necessary for MAS to employ these fiscal and monetary measures to curb this persistent and drastic inflation.

With the tightening of our monetary policy, price stability at least in the medium term would be ensured, to allow for sustainable economic growth for all. A stronger Singdollar helps to reduce imported inflation and limit export demand as well. This will help ease labour pressures here.

Impact On The Singapore Economy

The lingering question in all our minds, I believe, is whether MAS’s net loss would affect us badly. Well, no.

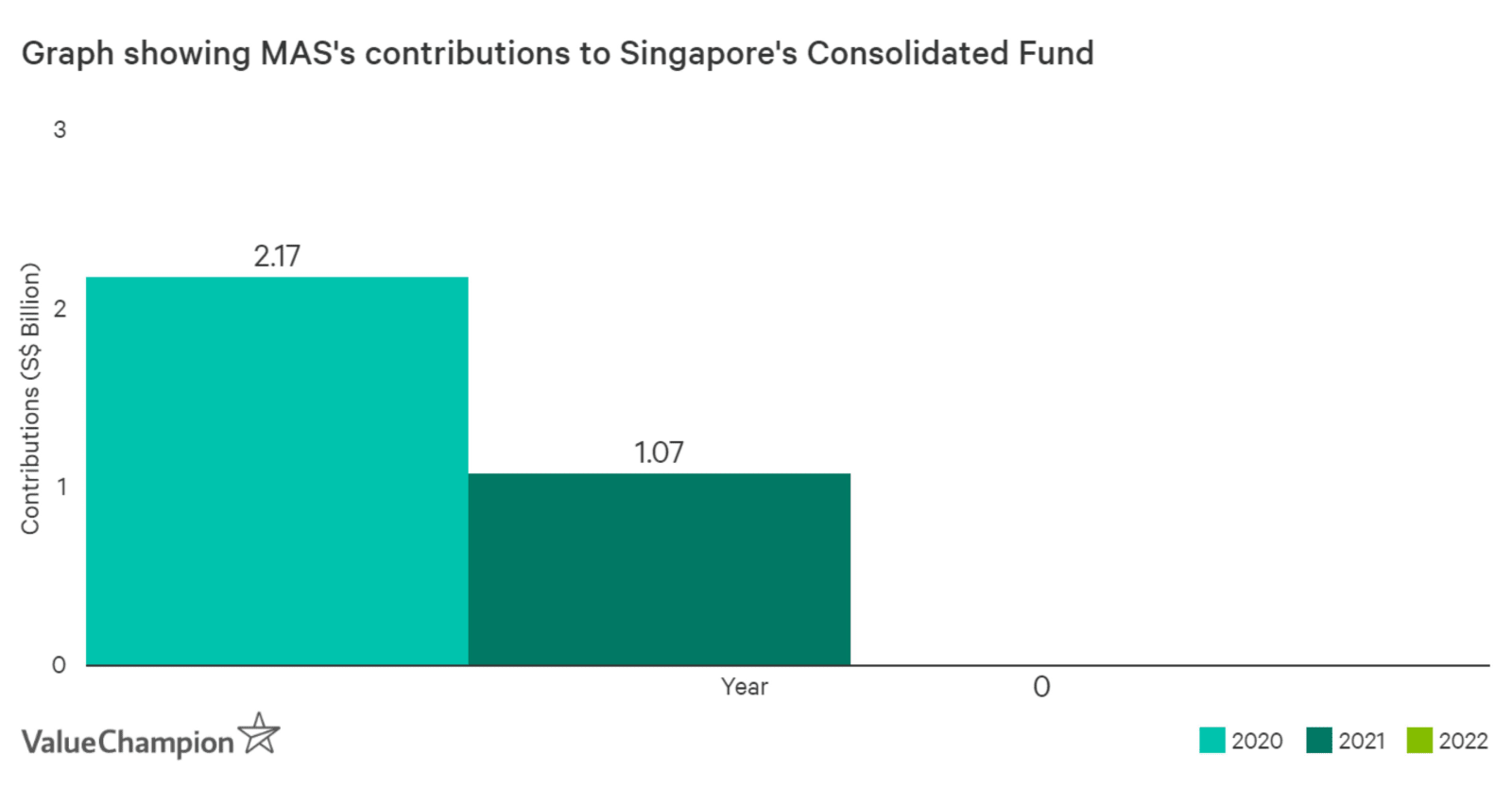

MAS would not be contributing to Singapore’s Consolidated Fund this year. However, it is considered as a short-term loss. This is the first time it has not contributed in 2 years, as MAS had contributed $2.17 billion in FY 2019/20 and $1.07 billion in FY 2020/21.

What is the Consolidated Fund? It is just like a bank account held by the Singapore Government, of which revenues are channelled towards and out of which Government expenditures are spent. In years of net profits, the contribution for each financial year will be paid over a period of three years; this helps to ensure the stability of the government budget.

Even though MAS will not be contributing to the Conslidated Fund, the Government will still receive S$1.1 billion due to the previous years' profits.

Impact On Individual Singaporeans

Despite the monetary measures taken by MAS, high inflation is a current global phenomenon and cannot be avoided fully. Sectors like food and energy are expected to see the highest increase in prices, with tight food and energy supplies arising from various factors such as the Russia-Ukraine conflict.

Since inflation cannot be avoided completely, prices will surely increase and hence, real incomes may fall as purchasing power falls. The economic growth in Singapore may be slowed and dampened in the short to medium term.

Most Of Us Will Be Able To Tide Over The Uncertain Outlook

Although Singapore’s economy is forecasted to experience slowing growth, Singapore banks have maintained healthy investments and asset quality, allowing them to survive price and asset shocks.

For the average Singaporean, MAS has expressed that most should be able to tide over amidst the uncertain outlook and lowering of real incomes due to rising interest rates.

However, rising interest rates is still a worrying phenomenon, and some households may be priced out of the market.

How Do I Cope With The Impacts Of Inflation?

1. Hunt For Discounts

With inflation pushing up the prices of many of our daily necessities, it is sadly getting more and more expensive to maintain our standard of living.

In order to cope with this, we can try to make our money's worth by hunting for discounts. A great way to continue buying what you love, at better prices, would be to hunt for – you name it: offers, promotions, discounts, cashbacks and rewards.

We have some nifty tips and promotions up our sleeves this month, especially if you are a NSman who will be receiving your NS55 credit vouchers, or a Singaporean who will soon receive your GST vouchers. For the foodies, 1 for 1 buffets are one of the best phrases you would love to hear, getting to enjoy sumptuous food at half the price!

2. Use Credit Cards The Smart Way

As typical Singaporeans, we all love to get more bang for our buck. One way to make our spending less painful would be to fully utilise your credit cards, so as to maximise its rewards and make every dollar you spend worthwhile. There are so many different types of credit cards which can help you gain rewards in your everyday spending. Some types of credit cards include miles, cashback, rebates and rewards cards. You can feel free to pick and choose the most suitable type of card for your spending.

Recommended Card: UOB One Card The UOB One Credit Card offers the highest flat rebate rate for spenders with budgets of at least $2,000 a month. You can earn easy cashback on your daily spend and even get rewarded for paying your bills.

With this credit card, you will be able to maximise your savings and cashback. Enjoy a 5% flat rebate on all expenses, and an impressive 10% on Dairy Farm, Grab, Shopee and others. The UOB One card is surely one of the best cards that provides top rates for spenders.

- Pros

- Good fit for budgets of at least S$2,000 per month

- Easy cashback on daily spend

- Gives rebates for paying bills

- Cons

- Doesn't fit inconsistent budgets

- Annual fee

3. Invest

With inflation being a persistent problem that is set to ease only next year (though the outlook remains very volatile and uncertain, how should the normal Singaporean combat it?

Keeping your money in savings accounts with a low interest rate would mean that you’re ‘losing’ money, when we adjust for inflation.

In order to battle inflation, one of the best ways to cushion the impact of inflation on us would be to make smart investments. Invest in products that are safe and provide good inflation-adjusted returns so that you can beat inflation. Disclaimer though, all investments have an element of risk to them, so anyone should always research carefully before committing their money to the various investments available.

1. Saxo Markets

The easiest way to get started on investing would be to do it via an online brokerage trading platform, such as Saxo Markets, which provide low fees and excellent market access.

With Saxo Markets, you will be able to trade on many investment products such as stocks, options, forex, ETFs and more, all of which may offer higher returns that help you to combat inflation. Access to a variety of international markets is also granted so that you can diversify your portfolio, at low commissions.

2. Endowus https://www.valuechampion.sg/endowus-robo-advisor-review

Robo Advisors are AI-assisted investment platforms which may be very suitable for the busy Singaporean worker. Endowus is one of the best robo-advisors in Singapore, with its very competitive fees and has an independent status.

Endowus boasts some of the best yields for investors, and at low user fees, this makes Endowus a very attractive option for investors.

- Minimum Investment

- S$1,000

- MAS Licence

- Financial Advisor License

4. Gain Additional Income

The other way to stay afloat of inflation on top of savings and investment would also be to diversify your income streams and gain additional income from various sources, be it part-time jobs, side hustles and more.

You could also try to be more active in earning more and to clinch salary increments at your workplace. Employing the FIRE movement would not only help you to tide over this period of inflation and high prices, but help you in earning and saving enough to retire early and enjoy your golden years in peace and happiness.

Conclusion

We now know that MAS’s net loss is largely due to their policies to help curb rising inflation in Singapore.

The main enemy is inflation due to the highly volatile economic conditions worldwide, and we may never know when it would finally ease.

For the time being, the only thing that we as Singaporeans can do is to amp up our financial knowledge and try our best to employ strategies such as investing, to cushion the impacts that inflation may have on us.

Additional Resources:

Boon Hun spent over five years in the content marketing space as the managing editor of Goody Feed creating interesting and relevant content for the social media generation. In 2022, he moved to the FinTech space while remaining true to his roots, intending to bring financial literacy to more people in Singapore. When not doing his work, he can be found watching people build homes on YouTube.