Why Do Start-Ups Need More Support From Banks Following The Pandemic?

Singapore is one of the leading start-up capitals of the world. With its favourable tax laws and ease of setting up a business, many entrepreneurs have set up shop here. As of 2022, Singapore is home to 20 unicorn start-ups that have reached S$1 billion in valuation, with most of them operating within the Southeast Asian region.

Yet, start-ups were some of the hardest hit by the COVID-19 pandemic. Their smaller balance sheets made them particularly vulnerable when weathering multiple lockdowns as compared to larger conglomerate firms. What obstacles do start-ups face that the pandemic has exacerbated, and continue to persist even now?

Read Also: Best SME and Business Loans in Singapore for Start-Ups

Challenges Faced By Start-Ups

1. Underserved by Traditional Banks

Start-ups have found themselves underserved at traditional banks partly due to the difference in types of companies. On the one hand, there are micro start-ups that are more similar in organisational structure to one-man entrepreneurship. On the other hand, there are larger start-ups which mirror the structure and needs of large corporations.

The vast difference in the organisational structure of start-ups means that there could be start-ups that may fall between the cracks of what traditional banks typically serve. Start-ups might find themselves lost between retail and corporate banking segments, unable to obtain the relevant support that they require.

This is particularly true when it comes to financing. From a bank’s perspective, micro start-ups are smaller business clients with higher perceived risks as financing requirements (such as credit ratings, consistent cash flow, and a strong business plan) are based on the construct of established companies, which small businesses are less likely to be able to meet. Start-ups often own fewer assets as collateral, which reduces the type of loans they can apply for.

As a result, start-ups often find themselves getting the short end of the stick. They are not only faced with difficulties in obtaining loans and other financial services through traditional banks, but are also often unable to obtain the level of customer service that they would like as banks are not as well-versed in their wants and needs.

2. Inflationary Macro Environment

One of the lingering impacts of the COVID-19 pandemic is the inflationary pressures that we are currently facing. The supply chain issues experienced as a result of labour shifts, multiple lockdowns in China, and the Russia-Ukraine conflict have resulted in commodity prices around the world being affected.

These two major factors combined have resulted in some of the highest rates of inflation experienced in decades. Singapore’s inflation rate year-on-year as of September 2022 was 7.483%.

Start-ups have not been spared by inflation either. Despite growing consumer spending post-lockdown, higher costs of production as a result of inflation have eaten into company profits.

A more competitive labour market has also caused upward pressure on wages. As labour is one of the main costs for most companies, this has also had a great impact on start-ups’ expenses.

3. Cyber Security

The pandemic had drastically altered working arrangements. Start-ups have had to adopt more remote working arrangements to support their employees during lockdowns. As more employees are accessing company cloud services from their personal devices at home, this opens up more points of vulnerability for many enterprises to be hacked.

An estimated 43% of cyberattacks in 2020 were targeted towards SMEs. SMEs are smaller in size and often do not have as robust protocols and training in place to prevent employees from falling victim to cyberattacks, as compared to much larger companies.

Similarly, a breach in cyber-security can result in significant financial and reputational losses for a start-up. 60% of SMEs are forced to shut their doors six months after experiencing a cyber-attack. Therefore, cyber-security is paramount, especially to smaller, more vulnerable start-ups.

How Can Banks Better Serve Start-ups?

To solve the above concerns, start-ups have increasingly turned to digital banking. Digital banks help to fill in that market gap as they are more suited to the scale of start-up operations. In a previous study by Visa, it was found that 88% of smaller enterprises would be amenable to switching to a digital bank to meet their banking needs.

A digital bank account is particularly attractive to start-ups that value a convenient and straightforward banking experience. Digital banks streamline banking services through automation, with effective user-oriented pricing algorithms that create a more tailored banking experience as compared to traditional banks.

This could translate to lower costs for start-ups as unnecessary frills are reduced. Digital banks do away with a bank’s physical presence to reduce costs and focus on the core financial services that businesses need.

Many start-ups have cited that they were willing to access unsecured funding at a higher interest rate as long as it is obtained through reliable convenient channels. Digital banks offer such channels and address start-ups’ need for simple products and services with quick turnaround time.

Even while doing so, digital banks do not compromise on their cybersecurity. They allow customers to transact through different channels while bearing the burden of data security and risk mitigation.

Read Also: Best SME Loans for Small Businesses in Singapore 2022

ANEXT Bank — A Digital Bank For The SME Community

ANEXT Bank offers accessible and effortless digital banking solutions aimed at addressing the needs of start-ups to enable them to adapt and thrive in an increasingly challenging and competitive market.

No-Frills, Affordable Banking For Start-Ups

Banking with ANEXT Bank is also cost-effective, which is compatible with bootstrapping start-ups.

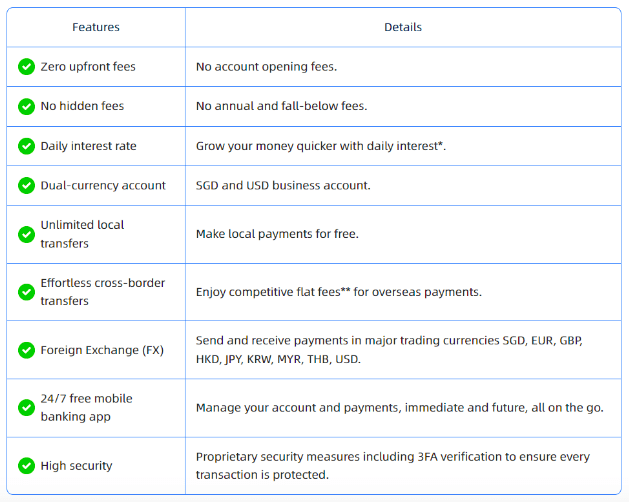

Their competitive advantage lies in their digital ANEXT Business Account, which allows for high-security cross-border transactions at lower costs than regular banks.

The dual-currency account allows businesses to send and receive payments using major trading currencies such as SGD, EUR, GBP, HKD, JPY, KRW, MYR, THB, and USD.

This enables seamless B2B transactions across the world.

To top that off, they offer no account opening fees, annual or fall-below fees, and even no inward telegraphic transfer fees. Outward telegraphic transfers can also be done at a flat rate, so there are no hidden costs to business account holders.

A Digital Bank in Singapore For Start-Ups

The ANEXT Business Account offers more value for business owners with daily interest, enabling businesses to grow their balances at no additional or hidden fees.

This can help alleviate some of the inflation-induced operational costs that have now become a major cause of concern for start-ups.

Furthermore, ANEXT Bank tackles the security concerns of start-ups with its 3-factor authentication feature. Multi-factor authentication greatly improves security and makes start-ups less vulnerable to attacks as it acts as multiple barriers for hackers. After all, it would be much harder for a hacker to fake or steal information through three different layers of authentication.

Setting up a business bank account in Singapore is swift and easy with ANEXT Bank — business owners can apply for an account here using MyInfo Business.

For more information on opening a digital business bank account with ANEXT, you can check out our previous article on digital banking.

Like what you just read? Follow us on Telegram to get up to date on fresh content!

Read Also:

Cover image source: Pexels

Enya is a budding Research Analyst at ValueChampion. She has a BA in Economics from the University of Melbourne and has previously worked in the banking sector. Enya combines her experience and passion for personal finance to bring digestible and enriching financial content to readers.