Rising Interest Rates: Singaporean Consumers Are Rushing to Borrow

Since the US Fed announced its plans to raise interest rates in December of 2016, interest rates in Singapore have also begun to rise, albeit slowly. For instance, 3-Month Singapore Interbank Offered Rate (SIBOR) has already reached 0.94% in March 2017 after bottoming out around 0.87% in September of 2016. While that may seem small to some people, that's a relatively meaningful increase of 8%. SIBOR affects almost every interest rate in Singapore, and therefore an increase in SIBOR means greater interest burdens for borrowers.

Given that Singapore's monetary policy is almost solely focused on currency exchange rate stabilisation, further interest hikes expected to come from the US usually means higher rates for Singaporeans too. In anticipation of such at rend, it seems that Singaporean consumers are rushing to finance their big purchases before rates rise further. Below are some of the key trends we observed.

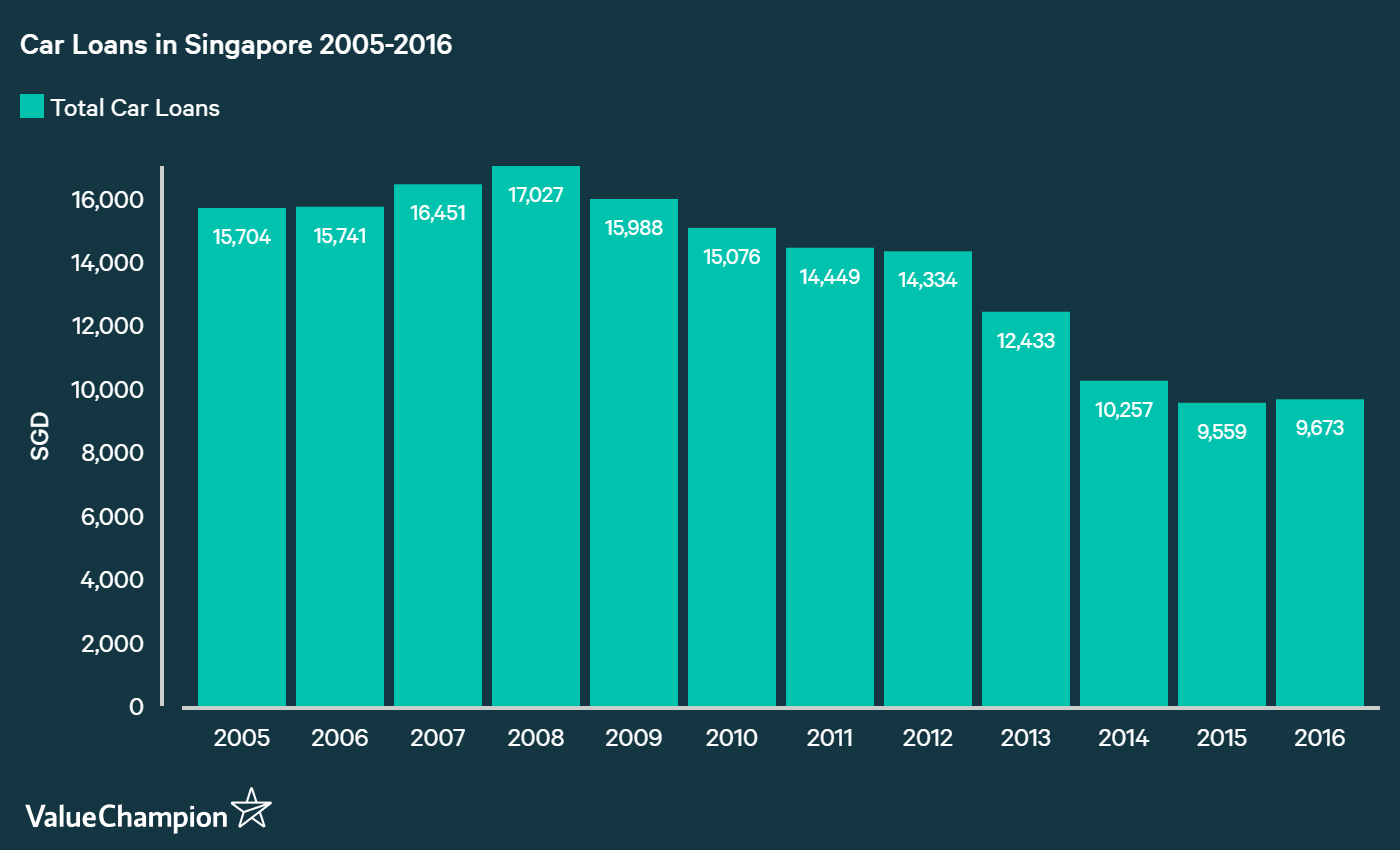

Car Loans Are Increasing for the First Time in 8 Years

According to our study of household balance sheet in Singapore, car loans have been declining consistently since 2008. After reaching S$17bn in 2008, it nosedived to almost half of its peak to S$9.6bn in 2015. Towards the end of 2016, however, car loans began to grow again for the first time in 8 years.

While the number of cars in Singapore still declined in 2016, a closer look suggests there's more to this story. For one, we saw a noticeable pick up number of new car registrations in 2016. In 2014, only 28,932 new cars were registered; however, this number grew to 58,000 in 2015 and 89,000 in 2016! MAS's easing restrictions on getting car loans last year may have helped to increase car purchases as well as car loan applications, but we also know that car loans didn't start growing until December of 2016. Given this, a logical deduction of facts suggests that a significant number of consumers may be rushing to buy cars with cheap car loans while historically low interest rates are still available.

Home Loan Growth is Accelerating

Our intuition about a rush towards borrowing was further evidenced in home loan trends. For instance, the growth rate of total home loans outstanding accelerated for 3 months in a row from October to December of 2016, which has never happened since 2011. For example, home loans grew at an average of 3.66% on an annual basis for the first 9 months of 2016; for the last 3 months of 2016, however, home loans grew at an average rate of 3.78% compared to the same period in 2015.

It seems that this "debt rush" may have had some impact on property prices as well. While property prices declined for the 13th consecutive quarters in Q4, it actually fell by only -0.5% Q/Q in Q4, a substantial recovery from -1.5% in Q3. Not only that, prices for landed properties actually increased by 0.8% Q/Q, compared to -2.7% decline it faced in Q3.

Concerns About Consumer Health

While increased demand for cars and properties is certainly a welcome sign for the economy, the fact that these "positive" trends are largely funded by debt is certainly a concerning phenomenon. Consumption growth that is being driven by people borrowing money is not as sustainable as one that is driven by income growth. For instance, credit card debt has grown by 5% in 2016, compared to a -1.6% decline in 2015, and is still the fastest growing category of consumer debt in January 2017.

This is a very worrying sign that implies people are spending more on credit cards without necessarily paying down their balance. Sure, credit card rewards can be quite generous in Singapore, but they are in no way significant enough to offset the 25% of interest that credit cards charge on average on these unpaid balances. Higher level of debt funded consumption necessarily means that discretionary spending will be negatively impacted if and when rates rise.

Other loans, which includes personal loans and share financing loans, was the only category of loans that showed decline in 2016.

Opportunity to Refinance Your Existing Debt

While we cannot wholeheartedly welcome this trend of rising debt & debt fueled purchases of cars, homes and other goods, we do think historically low interest rates and upcoming rate hikes do present a great opportunity for consumers to refinance their debt. Refinancing is a great tool to lower your interest burden, especially if you got your car or home loan few years ago when rates were meaningfully higher than they are today.

Not only that, if you have been racking up a credit card balance that is snowballing into an unmanageable proportion, you should consider refinancing your card debt with a personal loan or a balance transfer. These are great tools for you to consolidate your high-interest debt into a lower cost loan with a fixed repayment schedule that you can adhere to on a regular basis.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.