Best Reward Credit Cards in Singapore 2024

Selecting the best credit card for you depends greatly on your priorities. For those looking for credit card rewards, such as signup bonuses, we analysed Singapore's most competitive credit cards and identified the best rewards credit cards in Singapore!

- UOB One: Highest flat rebate on the market, earn up to $300/qtr

- Maybank Family & Friends: 8% cashback with S$800 min. spend requirement

- Citi Cash Back: Up to 8% rebate on groceries & petrol, 6% on dining

- POSB Everyday: Rebates up to 10% in Singapore

- DBS Altitude: Earn 5 miles per S$1 spend on online flight & hotel transactions (capped at S$5,000 per month) and overseas spend (at point-of-sale), earn S$1 = 2 miles on overseas spend (online transactions), earn S$1 = 1.2 miles on local spend. All miles earned through this card is via DBS Points and thus will never expire.

- Citi PMV: 45,000 Welcome Citi Miles with S$9,000 spend in 3 mo

- KrisFlyer UOB: 3mi/S$1 on dining, transport, shopping & travel

- Amex SIA KrisFlyer: Directly earn KrisFlyer miles, S$150 SIA credit

- UOB PRVI Amex: Fee-Waiver + 20k bonus miles, 2.4 miles per $1 overseas

- OCBC 365: 6% rebate on dining, 3% rebate on groceries, utilities and travel, Visa Concierge Services

- MB Horizon Visa: Market-leading 3.2 miles per S$1 select local spend

- Unlimited Cards: Up to 1.6% unlimited cashback on daily spend

- HSBC Advance: Up to 3.5% cashback capped at S$300/month

- Citi Prestige: Unlimited lounge access, bonus hotel nights & more

- SC Visa Infinite X: Bonus S$6,000 w/ S$200k fund placement

- OCBC Voyage: Flexible miles redemption, boosted rewards for overseas spend

- OCBC Frank: Up to 6% rebate for FX, online and mobile purchases, low S$600 min. spend requirement

- Citi SMRT: 5% everyday rebates w/S$500 min spend

- MB Platinum Visa: Up to 3.33% rebate on local and foreign currency spend

- HSBC Revolution: 4 miles per S$1 spent online and on contactless payments

- DBS Live Fresh: Get up to 10% cashback w/ S$600 min. spend - 5% cashback on Online and Visa Contactless Spend, 5% green cashback at selected eco-eateries, retailers and transport services. Additional 0.3% cashback on all other spend

- UOB One: Highest flat rebate on the market, earn up to $300/qtr

- Maybank Family & Friends: 8% cashback with S$800 min. spend requirement

- Citi Cash Back: Up to 8% rebate on groceries & petrol, 6% on dining

- POSB Everyday: Rebates up to 10% in Singapore

- DBS Altitude: Earn 5 miles per S$1 spend on online flight & hotel transactions (capped at S$5,000 per month) and overseas spend (at point-of-sale), earn S$1 = 2 miles on overseas spend (online transactions), earn S$1 = 1.2 miles on local spend. All miles earned through this card is via DBS Points and thus will never expire.

- Citi PMV: 45,000 Welcome Citi Miles with S$9,000 spend in 3 mo

- KrisFlyer UOB: 3mi/S$1 on dining, transport, shopping & travel

- Amex SIA KrisFlyer: Directly earn KrisFlyer miles, S$150 SIA credit

- UOB PRVI Amex: Fee-Waiver + 20k bonus miles, 2.4 miles per $1 overseas

- OCBC 365: 6% rebate on dining, 3% rebate on groceries, utilities and travel, Visa Concierge Services

- MB Horizon Visa: Market-leading 3.2 miles per S$1 select local spend

- Unlimited Cards: Up to 1.6% unlimited cashback on daily spend

- HSBC Advance: Up to 3.5% cashback capped at S$300/month

- Citi Prestige: Unlimited lounge access, bonus hotel nights & more

- SC Visa Infinite X: Bonus S$6,000 w/ S$200k fund placement

- OCBC Voyage: Flexible miles redemption, boosted rewards for overseas spend

- OCBC Frank: Up to 6% rebate for FX, online and mobile purchases, low S$600 min. spend requirement

- Citi SMRT: 5% everyday rebates w/S$500 min spend

- MB Platinum Visa: Up to 3.33% rebate on local and foreign currency spend

- HSBC Revolution: 4 miles per S$1 spent online and on contactless payments

- DBS Live Fresh: Get up to 10% cashback w/ S$600 min. spend - 5% cashback on Online and Visa Contactless Spend, 5% green cashback at selected eco-eateries, retailers and transport services. Additional 0.3% cashback on all other spend

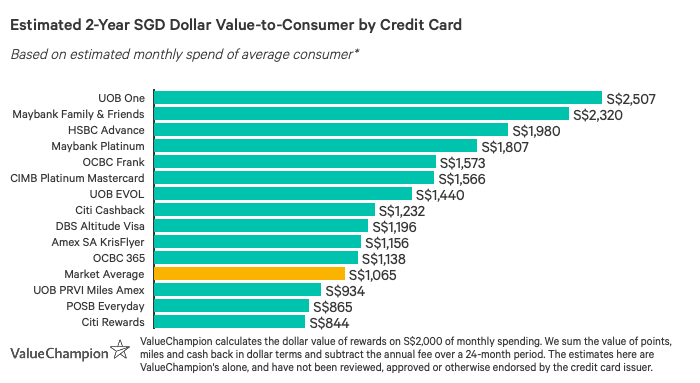

Compare Best Rewards Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best credit cards on the market in Singapore to estimate returned value-to-consumer after 2 years. We accounted for credit card rewards such as rebates and net-out annual fees. As a note, the dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Best Rewards Credit Cards for Cashback

These great cashback cards allow you to earn easy rebates that offset your monthly card statement. If you would like to take a deeper dive and compare these cards and the credit card rewards you can earn on spending, check out our credit card comparison tool.

UOB One Card: Best Flat Rebate Rate

- Pros

- Good fit for budgets of at least S$2,000 per month

- Easy cashback on daily spend

- Gives rebates for paying bills

- Cons

- Doesn't fit inconsistent budgets

- Annual fee

If you consistently spend S$2,000/month, UOB One Card is the best card for maximising cashback on all spend. UOB One Card offers 5% general cashback, boosted to 6% on electric bills and 10% on Grab and select UOB Travel spend. Given the card's very high base rate, cardholders don’t need to track purchases by category (ie, dining) or merchant in order to rapidly earn rewards. Cardholders who spend at least S$2,000/month for 3 months earn an impressive S$300 for that quarter (equal to S$100/month); lower or inconsistent spenders, however, earn between S$50 to S$100/quarter.

| |

- Pros

- Good fit for budgets of at least S$2,000 per month

- Easy cashback on daily spend

- Gives rebates for paying bills

- Cons

- Doesn't fit inconsistent budgets

- Annual fee

|

If you consistently spend S$2,000/month, UOB One Card is the best card for maximising cashback on all spend. UOB One Card offers 5% general cashback, boosted to 6% on electric bills and 10% on Grab and select UOB Travel spend. Given the card's very high base rate, cardholders don’t need to track purchases by category (ie, dining) or merchant in order to rapidly earn rewards. Cardholders who spend at least S$2,000/month for 3 months earn an impressive S$300 for that quarter (equal to S$100/month); lower or inconsistent spenders, however, earn between S$50 to S$100/quarter.

|

Maybank Family & Friends MasterCard: Top Rebates in SG & MY

- Pros

- Good for budgets of S$800/month

- Awards 8% cashback on 5 categories of your choice

- 3 year annual fee waiver

- Great to use in Singapore, Malaysia, Indonesia and the Philippines

- Cons

- Merchant restrictions

- Lacks miles & travel perks

People spending S$500 to S$1,000/month in Singapore and Malaysia can potentially earn more with Maybank Family & Friends Card than any other card on the market. After just $500 minimum spend, cardholders earn 5% rebate on fast food & food delivery, groceries, transport, petrol, and data communications/online TV streaming in Singapore and Malaysia. A S$800 minimum spend earns an 8% rebate. Most cashback cards only offer base rates (around 0.3%) at this spend level. In fact, even Maybank F&F Card’s closest competitor offers just 3.33%. Even better, there are no merchant restrictions, rebates are capped at a competitive S$80/month, and cardholders enjoy a fee-waiver with just S$12,000 annual spend. While overseas purchases aren't eligible for such rewards, cardholders who spend regionally can truly benefit from Maybank F&F Card.

| |

- Pros

- Good for budgets of S$800/month

- Awards 8% cashback on 5 categories of your choice

- 3 year annual fee waiver

- Great to use in Singapore, Malaysia, Indonesia and the Philippines

- Cons

- Merchant restrictions

- Lacks miles & travel perks

|

People spending S$500 to S$1,000/month in Singapore and Malaysia can potentially earn more with Maybank Family & Friends Card than any other card on the market. After just $500 minimum spend, cardholders earn 5% rebate on fast food & food delivery, groceries, transport, petrol, and data communications/online TV streaming in Singapore and Malaysia. A S$800 minimum spend earns an 8% rebate. Most cashback cards only offer base rates (around 0.3%) at this spend level. In fact, even Maybank F&F Card’s closest competitor offers just 3.33%. Even better, there are no merchant restrictions, rebates are capped at a competitive S$80/month, and cardholders enjoy a fee-waiver with just S$12,000 annual spend. While overseas purchases aren't eligible for such rewards, cardholders who spend regionally can truly benefit from Maybank F&F Card.

|

Citi Cash Back Card: Cashback for Global Food & Transport

- Pros

- Great dining and groceries rewards

- High petrol discounts

- Cons

- Lacks shopping and entertainment rewards

- Not suitable for lower budgets

Citi Cash Back Card is one of the best cashback cards on the market because it rewards average consumers with top rates in key categories–food and transport. Cardholders earn up to 8% cashback on dining, groceries and petrol (any station), in addition to saving up to 20.88% on fuel at Esso & Shell. Even more, consumers earn up to S$75/month, which is quite high by market standards, adding up to a potential S$900/year.

| |

- Pros

- Great dining and groceries rewards

- High petrol discounts

- Cons

- Lacks shopping and entertainment rewards

- Not suitable for lower budgets

|

Citi Cash Back Card is one of the best cashback cards on the market because it rewards average consumers with top rates in key categories–food and transport. Cardholders earn up to 8% cashback on dining, groceries and petrol (any station), in addition to saving up to 20.88% on fuel at Esso & Shell. Even more, consumers earn up to S$80/month, which is quite high by market standards, adding up to a potential S$960/year.

|

POSB Everyday Card: Rebates on Essentials

- Pros

- Benefits highly diversified spend with large food budgets

- Great fit for commuters seeking a convenient, an all-in-one card

- Cons

- Not suitable for consistent spend of S$2k+/mo

- Lacks travel rewards

- Has an annual fee

POSB Everyday Card is a great rebate card for spend on daily essentials. Cardholders typically earn cashback rates of up to 10% cashback on online food delivery, dining, groceries, transport, personal care and recurring bills. Earning these rates requires cardholders to meet a minimum spend of S$800 per month.

| |

- Pros

- Benefits highly diversified spend with large food budgets

- Great fit for commuters seeking a convenient, an all-in-one card

- Cons

- Not suitable for consistent spend of S$2k+/mo

- Lacks travel rewards

- Has an annual fee

|

POSB Everyday Card is a great rebate card for spend on daily essentials. Cardholders typically earn cashback rates of up to 10% cashback on online food delivery, dining, groceries, transport, personal care and recurring bills. Earning these rates requires cardholders to meet a minimum spend of S$800 per month.

|

Best Rewards Credit Cards for Air Miles

A suitable choice when looking for travel rewards for credit cards, frequent travellers can enjoy top rates, credit card rewards as well as attractive perks with the following cards.

DBS Altitude Visa: Affordable Luxury Perks

- Pros

- Great for online travel bookings

- Cons

- Those willing to pay an annual fee for more bonus miles

- Affluent travellers who are willing to pay a high fee for luxury travel perks

Frequent travellers seeking luxury perks–without having to pay a monumental annual fee–can enjoy top rewards rates plus a fee-waiver with DBS Altitude Visa Card. Cardholders earn 1.2 miles per S$1 local spend, 2 miles overseas, and 3 miles for online travel bookings. Even better, miles earned never expire.

| |

- Pros

- Great for online travel bookings

- Cons

- Those willing to pay an annual fee for more bonus miles

- Affluent travellers who are willing to pay a high fee for luxury travel perks

|

Frequent travellers seeking luxury perks–without having to pay a monumental annual fee–can enjoy top rewards rates plus a fee-waiver with DBS Altitude Visa Card. Cardholders earn 1.2 miles per S$1 local spend, 2 miles overseas, and 3 miles for online travel bookings. Even better, miles earned never expire.

|

Citi PremierMiles Visa Card: Annual Bonus Miles + Lounge Access

- Pros

- Frequent traveler perks

- Low fees

- Flexible miles redemption

- Cons

- Lacks luxury perks

- Not suitable for occasional travel

Average consumers looking for great perks without a high fee should consider Citi PremierMiles Visa Card. Cardholders earn 1.2 miles per S$1 spend locally and 2 miles overseas, which aligns with market standards. However, Citi PMV Card goes above and beyond by offering 2 free airport lounge visits per year and free travel insurance. Consumers receive up to 45,000 bonus miles miles on sign-up and 10,000 annual renewal miles. Many travel cards come with lounge access and bonus renewal miles have non-waivable fees of S$400+.

| |

- Pros

- Frequent traveler perks

- Low fees

- Flexible miles redemption

- Cons

- Lacks luxury perks

- Not suitable for occasional travel

|

Average consumers looking for great perks without a high fee should consider Citi PremierMiles Visa Card. Cardholders earn 1.2 miles per S$1 spend locally and 2 miles overseas, which aligns with market standards. However, Citi PMV Card goes above and beyond by offering 2 free airport lounge visits per year and free travel insurance. Consumers receive up to 45,000 bonus miles on sign-up and 10,000 annual renewal miles. Many travel cards come with lounge access and bonus renewal miles have non-waivable fees of S$400+.

|

KrisFlyer UOB Credit Card: Top Miles for Young SIA Loyalists

- Pros

- 3 mi per S$1 on SIA, SilkAir, Scoot & KrisShop

- Up to 3 mi on dining, transport, online shopping & travel

- Expedited KF Elite Silver status, Scoot privileges

- 10,000 annual bonus renewal miles

- Cons

- Just 1.2 mi on non-category overseas spend

- No lounge access perks

- No spend-based fee-waiver

KrisFlyer UOB Card is one of the best options on the market for loyal SIA flyers, especially young adults who travel on a budget. Cardholders earn 3 miles per S$1 spend on SIA brands like SIA, Scoot, SilkAir and KrisShop. All general spend, both locally and overseas, earns just 1.2 miles per S$1. Fortunately, consumers who spend S$500+ with SIA in a year access boosted rates of 3 miles per S$1 on global dining, transport, online fashion shopping and even travel bookings. These rates are not only amongst the highest on the market, they're also uncapped. The categories themselves are a great fit to a young adult's lifestyle, and unlocking the boost is fairly easy for people who travel a few times a year.

| |

- Pros

- 3 mi per S$1 on SIA, SilkAir, Scoot & KrisShop

- Up to 3 mi on dining, transport, online shopping & travel

- Expedited KF Elite Silver status, Scoot privileges

- 10,000 annual bonus renewal miles

- Cons

- Just 1.2 mi on non-category overseas spend

- No lounge access perks

- No spend-based fee-waiver

|

KrisFlyer UOB Card is one of the best options on the market for loyal SIA flyers, especially young adults who travel on a budget. Cardholders earn 3 miles per S$1 spend on SIA brands like SIA, Scoot, SilkAir and KrisShop. All general spend, both locally and overseas, earns just 1.2 miles per S$1. Fortunately, consumers who spend S$500+ with SIA in a year access boosted rates of 3 miles per S$1 on global dining, transport, online fashion shopping and even travel bookings. These rates are not only amongst the highest on the market, they're also uncapped. The categories themselves are a great fit to a young adult's lifestyle, and unlocking the boost is fairly easy for people who travel a few times a year.

|

American Express Singapore Airlines KrisFlyer Card: Option for Frequent SIA Flyers

- Pros

- Easy-to-use miles card

- No conversions & transfer fees

- Great rewards with Singapore Airlines

- Cons

- Not easy to maximise miles

- Lacks airline/travel rewards aside from SIA

American Express Singapore Airlines KrisFlyer Card is a noteworthy option for miles card beginners. Spend directly earns KrisFlyer Miles, which are credited to the cardholder’s frequent flyer account–there are no conversions or transfer fees. In addition, while consumers earn 1.1 miles per S$1 spend (2 miles for overseas in June & December) they can earn 2 miles for spend on SingaporeAir, SilkAir, and KrisShop. These straightforward rates are complemented by perks like free travel insurance, Hertz rental car privileges and Amex Selects discounts and deals. While there’s a S$176.55 fee, it's waived 1-year. Ultimately, Amex SIA KF Card is a worthwhile option for Singapore Airlines flyers looking for a convenient miles.

| |

- Pros

- Easy-to-use miles card

- No conversions & transfer fees

- Great rewards with Singapore Airlines

- Cons

- Not easy to maximise miles

- Lacks airline/travel rewards aside from SIA

|

American Express Singapore Airlines KrisFlyer Card is a noteworthy option for miles card beginners. Spend directly earns KrisFlyer Miles, which are credited to the cardholder’s frequent flyer account–there are no conversions or transfer fees. In addition, while consumers earn 1.1 miles per S$1 spend (2 miles for overseas in June & December) they can earn 2 miles for spend on SingaporeAir, SilkAir, and KrisShop. These straightforward rates are complemented by perks like free travel insurance, Hertz rental car privileges and Amex Selects discounts and deals. While there’s a S$176.55 fee, it's waived 1-year. Ultimately, Amex SIA KF Card is a worthwhile option for Singapore Airlines flyers looking for a convenient miles.

|

UOB PRVI Miles American Express Card: Rapid Miles Accumulation

- Pros

- Great for rapid miles accrual

- Awards high spend on airlines & hotels

- Annual fee waiver with Amex card

- Cons

- Doesn't fit infrequent travellers with mostly local budgets

- Lacks luxury perks & privileges

UOB PRVI Miles American Express Card is the best way for above-average spenders to rapidly accrue miles and even enjoying a fee waiver. Consumers with S$50,000 annual spend are exempt from the S$256.8 fee and receive 20,000 bonus miles (worth S$200). No other high-end travel card offers a fee-waiver. In addition, UOB PRVI Miles Card offers perks like free airport transfers and travel insurance.

| |

- Pros

- Great for rapid miles accrual

- Awards high spend on airlines & hotels

- Annual fee waiver with Amex card

- Cons

- Doesn't fit infrequent travellers with mostly local budgets

- Lacks luxury perks & privileges

|

UOB PRVI Miles American Express Card is the best way for above-average spenders to rapidly accrue miles and even enjoying a fee waiver. Consumers with S$50,000 annual spend are exempt from the S$256.8 fee and receive 20,000 bonus miles (worth S$200). No other high-end travel card offers a fee-waiver. In addition, UOB PRVI Miles Card offers perks like free airport transfers and travel insurance.

|

Best No-Fee Rewards Credit Cards

Tired of paying annual fees for your credit card? The following reward credit cards in Singapore have no annual fee or come with an easy fee waiver.

OCBC 365 Card: No-Fee Rebates on Essentials

- Pros

- 6% rebate on dining, 3% on groceries, transport, utilities, online travel

- Fee waiver with S$10,000 annual spend

- Up to 22.1% fuel savings at Caltex, 20.2% at Esso

- Cons

- 0.3% rebate on general spend

- High S$800 minimum spend requirement

If having a single card to reward nearly all of your everyday spend at high rates sounds appealing to you, you should definitely consider OCBC 365 Card. Unlike its competitors, OCBC 365 Card does not limit rebates to select merchants in any category. Cardholders enjoy 6% rebates on dining & online food delivery, plus 3% on online & offline grocery purchases, land transport (including Grab, Go-Jek, ComfortDelGro and more) and online travel bookings. Another stand-out feature is 3% rebate on recurring electricity and telco bills with no category-specific cap. Alternatives offer only 1% rebate, capped as low as S$1/month.

| |

- Pros

- 6% rebate on dining, 3% on groceries, transport, utilities, online travel

- Fee waiver with S$10,000 annual spend

- Up to 22.1% fuel savings at Caltex, 20.2% at Esso

- Cons

- 0.3% rebate on general spend

- High S$800 minimum spend requirement

|

If having a single card to reward nearly all of your everyday spend at high rates sounds appealing to you, you should definitely consider OCBC 365 Card. Unlike its competitors, OCBC 365 Card does not limit rebates to select merchants in any category. Cardholders enjoy 6% rebates on dining & online food delivery, plus 3% on online & offline grocery purchases, land transport (including Grab, Go-Jek, ComfortDelGro and more) and online travel bookings. Another stand-out feature is 3% rebate on recurring electricity and telco bills with no category-specific cap. Alternatives offer only 1% rebate, capped as low as S$1/month.

|

Maybank Horizon Visa Signature: Best Miles for Local Spend

- Pros

- High spend on local dining & transport

- Great for local spend and miles rewards on travel

- 3 years fee waiver

- Cons

- Doesn't reward overseas spend

- Few travel perks & privileges

- Lacks in rewards for essentials (ie groceries)

While most travel cards are expensive and mostly reward overseas spend, Maybank Horizon Visa Signature Card stands out as balanced, offering high miles for local and travel spend. Cardholders earn 3.2 miles per S$1 local spend on dining, petrol, taxis and Grab, and hotel bookings with Agoda. Most miles cards offer just 1.2 to 1.4 miles per S$1 local spend. Maybank Horizon Visa Card also offers 2 miles per S$1 spend on air tickets, travel packages and overseas transactions–a rate which aligns with most alternatives. Consumers can earn more at home on food and transport, while still earning respectable rates overseas.

| |

- Pros

- High spend on local dining & transport

- Great for local spend and miles rewards on travel

- 3 years fee waiver

- Cons

- Doesn't reward overseas spend

- Few travel perks & privileges

- Lacks in rewards for essentials (ie groceries)

|

While most travel cards are expensive and mostly reward overseas spend, Maybank Horizon Visa Signature Card stands out as balanced, offering high miles for local and travel spend. Cardholders earn 3.2 miles per S$1 local spend on dining, petrol, taxis and Grab, and hotel bookings with Agoda. Most miles cards offer just 1.2 to 1.4 miles per S$1 local spend. Maybank Horizon Visa Card also offers 2 miles per S$1 spend on air tickets, travel packages and overseas transactions–a rate which aligns with most alternatives. Consumers can earn more at home on food and transport, while still earning respectable rates overseas.

|

Best Rewards Credit Cards for High Spenders

For the very affluent consumers looking to enjoy credit card rewards, the following reward cards allow you to enjoy uncapped cashback and luxury travel perks.

Citi Cash Back+ Card: Top Limitless Rebate Rate

- Pros

- Affluent consumers spending S$7k+/mo

- People interested in an easy-to-use flat rate card

- Those looking to avoid spend requirements or rewards caps

- Cons

- Average or lower spenders looking to maximise rewards

- Those with specialised spend (i.e. dining, shopping)

- Consumer looking to avoid an annual fee

Citi Cash Back+ Card is the best card on the market for high-spenders who want to earn straightforward rewards without having to worry about earnings caps. Cardholders earn an unlimited 1.6% rebate on all spend, both locally and overseas, which is higher than the 1.5% offered by competitors. In addition, there's no minimum spend requirement, and the moderate S$192.6 fee is waived the 1st year. Ultimately, high-spending consumers can immediately begin earning cashback and truly maximise their rewards potential with Citi Cash Back+ Card.

| |

- Pros

- Affluent consumers spending S$7k+/mo

- People interested in an easy-to-use flat rate card

- Those looking to avoid spend requirements or rewards caps

- Cons

- Average or lower spenders looking to maximise rewards

- Those with specialised spend (i.e. dining, shopping)

- Consumer looking to avoid an annual fee

|

Citi Cash Back+ Card is the best card on the market for high-spenders who want to earn straightforward rewards without having to worry about earnings caps. Cardholders earn an unlimited 1.6% rebate on all spend, both locally and overseas, which is higher than the 1.5% offered by competitors. In addition, there's no minimum spend requirement, and the moderate S$192.6 fee is waived the 1st year. Ultimately, high-spending consumers can immediately begin earning cashback and truly maximise their rewards potential with Citi Cash Back+ Card.

|

Standard Chartered Simply Cash Credit Card: Unlimited Rebates + Transport Perks

- Pros

- Unlimited 1.5% flat cashback

- No minimum spend requirement

- Up to 21% fuel savings with Caltex

- Cons

- No boosted rates in specific categories

- No travel perks

High spenders with budgets of approximately S$7,000+/month will typically run into earnings restrictions with most capped cashback cards. With Standard Chartered Simply Cash Credit Card, however, cardholders can earn an unlimited 1.5% rebate on all spend without having to worry about such caps–in other words, earning to their full potential. Consumers can also benefit from up to 21% fuel savings at Caltex and SimplyGo compatibility, which makes transport a bit easier and more cost-effective. Overall, affluent individuals who want to fully maximise their cashback may want to consider SC Unlimited Cashback Card.

| |

- Pros

- Unlimited 1.5% flat cashback

- No minimum spend requirement

- Up to 21% fuel savings with Caltex

- Cons

- No boosted rates in specific categories

- No travel perks

|

High spenders with budgets of approximately S$7,000+/month will typically run into earnings restrictions with most capped cashback cards. With Standard Chartered Simply Cash Credit Card, however, cardholders can earn an unlimited 1.5% rebate on all spend without having to worry about such caps–in other words, earning to their full potential. Consumers can also benefit from up to 21% fuel savings at Caltex and SimplyGo compatibility, which makes transport a bit easier and more cost-effective. Overall, affluent individuals who want to fully maximise their cashback may want to consider SC Unlimited Cashback Card.

|

American Express True Cashback: Unlimited Cashback + Wedding Perks

- Pros

- Great Amex perks

- Straightforward, easy-to-use card

- Cons

- Not suitable for lower budgets

- Rewards general spend only

High-spenders, especially those with a budget of S$7k+/month, can easily maximise their earnings with American Express True Cashback Card. Cardholders earn a flat 1.5% cashback on all spend, without earnings caps–which is great for wealthy consumers who feel constrained by limits of S$100/month or lower (as per market standard).

| |

- Pros

- Great Amex perks

- Straightforward, easy-to-use card

- Cons

- Not suitable for lower budgets

- Rewards general spend only

|

High-spenders, especially those with a budget of S$7k+/month, can easily maximise their earnings with American Express True Cashback Card. Cardholders earn a flat 1.5% cashback on all spend, without earnings caps–which is great for wealthy consumers who feel constrained by limits of S$100/month or lower (as per market standard).

|

Maybank FC Barcelona Visa Signature: Unlimited Local Cashback

- Pros

- Affluent consumers spending S$6,500+/month

- High spenders with mostly local budgets

- Football fans–especially of FC Barcelona

- Cons

- Frequent travellers with high overseas spend

- People spending less than S$5,000/month

- Consumers who prioritise travel perks & privileges

Maybank FC Barcelona Visa Signature Card is an excellent card for wealthy consumers who aren't frequent travellers. Cardholders earn an elevated 1.6% unlimited cashback on all local spend, compared to competitors' standard 1.5% rate. Maybank FC Barcelona Card is also great because the lack of earnings caps make it easy for very high spenders to earn without constraint. Other perks include discounts at FC Barcelona stores, the chance to win free game tickets, and free travel insurance.

| |

- Pros

- Affluent consumers spending S$6,500+/month

- High spenders with mostly local budgets

- Football fans–especially of FC Barcelona

- Cons

- Frequent travellers with high overseas spend

- People spending less than S$5,000/month

- Consumers who prioritise travel perks & privileges

|

Maybank FC Barcelona Visa Signature Card is an excellent card for wealthy consumers who aren't frequent travellers. Cardholders earn an elevated 1.6% unlimited cashback on all local spend, compared to competitors' standard 1.5% rate. Maybank FC Barcelona Card is also great because the lack of earnings caps make it easy for very high spenders to earn without constraint. Other perks include discounts at FC Barcelona stores, the chance to win free game tickets, and free travel insurance.

|

HSBC Advance: Best for Affluent Advance Customers

- Pros

- Great fit for budgets between S$2,000 and S$8,000/month

- Easy, low-maintenance cashback

- Cons

- Lacks travel perks

- Doesn't fit highly specialised spend behaviors

Current HSBC Advance customers–and those willing to consider opening an account–can earn up to S$3,600 cashback per year with HSBC Advance Card. Cardholders enjoy up to 3.5% flat cashback after S$2,000 spend (or 2.5% cashback if spend is lower) and up to S$300/month for simply depositing a minimum of S$2,000 per month in fresh funds and charging at least five transactions to their account.

| |

- Pros

- Great fit for budgets between S$2,000 and S$8,000/month

- Easy, low-maintenance cashback

- Cons

- Lacks travel perks

- Doesn't fit highly specialised spend behaviors

|

Current HSBC Advance customers–and those willing to consider opening an account–can earn up to S$3,600 cashback per year with HSBC Advance Card. Cardholders enjoy up to 3.5% flat cashback after S$2,000 spend (or 2.5% cashback if spend is lower) and up to S$300/month for simply depositing a minimum of S$2,000 per month in fresh funds and charging at least five transactions to their account.

|

Citi Prestige MasterCard: Luxury Travel Perks

- Pros

- Great luxury benefits

- Ideal for higher budgets

- Great golfing and travel perks

- Cons

- Very high annual fees

- Unsuitable for moderate budgets

Affluent travellers who prioritise luxury perks should consider Citi Prestige MasterCard. Cardholders earn 1.3 miles per S$1 locally, 2 miles overseas, which are amongst the highest rates on the market. In addition, consumers can earn up to 30% annual bonuses based on the length of their relationship with Citibank. Simply using your card over time multiplies your earnings–few alternative cards offer such a bonus structure.

| |

- Pros

- Great luxury benefits

- Ideal for higher budgets

- Great golfing and travel perks

- Cons

- Very high annual fees

- Unsuitable for moderate budgets

|

Affluent travellers who prioritise luxury perks should consider Citi Prestige MasterCard. Cardholders earn 1.3 miles per S$1 locally, 2 miles overseas, which are amongst the highest rates on the market. In addition, consumers can earn up to 30% annual bonuses based on the length of their relationship with Citibank. Simply using your card over time multiplies your earnings–few alternative cards offer such a bonus structure.

|

Standard Chartered Visa Infinite X: Best Sign-on Bonus for Affluent Travellers

- Pros

- Earn up to 300,000 bonus welcome miles

- Earn 2 miles/S$1 spend overseas

- Special privileges with elite hotels

- Cons

- Bonus miles limited to affluent consumers

- Very high & unwaivable S$702 annual fee

- Lower rewards rates than other lux. cards

Affluent travellers open to banking with Standard Chartered should definitely consider Standard Chartered Visa Infinite X Card, which has one of the best sign-on bonuses on the market. Wealthy consumers who can place at least S$300k in fresh funds in a SC Priority Banking account receive an incredible 100,000 KrisFlyer miles, which is worth about S$10k when redeemed for business class tickets. Those who can place S$800k receive 150,000 miles (worth S$15k) and Priority Private Banking customers who place S$1.5m receive a total of 300,000 miles (worth S$30k). This bonus offers very high-income individuals an extraordinary opportunity to accrue a massive amount of miles almost immediately, without almost any added effort.

| |

- Pros

- Earn up to 300,000 bonus welcome miles

- Earn 2 miles/S$1 spend overseas

- Special privileges with elite hotels

- Cons

- Bonus miles limited to affluent consumers

- Very high & unwaivable S$702 annual fee

- Lower rewards rates than other lux. cards

|

Affluent travellers open to banking with Standard Chartered should definitely consider Standard Chartered Visa Infinite X Card, which has one of the best sign-on bonuses on the market. Wealthy consumers who can place at least S$300k in fresh funds in a SC Priority Banking account receive an incredible 100,000 KrisFlyer miles, which is worth about S$10k when redeemed for business class tickets. Those who can place S$800k receive 150,000 miles (worth S$15k) and Priority Private Banking customers who place S$1.5m receive a total of 300,000 miles (worth S$30k). This bonus offers very high-income individuals an extraordinary opportunity to accrue a massive amount of miles almost immediately, without almost any added effort.

|

OCBC Voyage: Flexible Earning & Luxury Perks

- Pros

- 2.2 miles per S$1 overseas retail and dining spend

- 1.3 miles per S$1 local retail spend

- 15,000 annual bonus renewal miles (worth S$150)

- Unlimited lounge access, limo transfers & more

- Up to 19% fuel savings with Caltex

- Cons

- High S$488 annual fee (no waiver)

- Recurring bills ineligible for rewards

- Access to limo transfers requires S$5,000 minimum spend

If you're seeking flexible miles rewards both at home and abroad–paired with great travel perks–you're likely to benefit from OCBC Voyage Card. Cardholders enjoy high rates of 2.2 miles per S$1 overseas, 1.3 miles locally. As a result, it's fairly easy to continue earning even when you're not abroad (compared to other luxury cards, which heavily favour overseas spend).

| |

- Pros

- 2.2 miles per S$1 overseas retail and dining spend

- 1.3 miles per S$1 local retail spend

- 15,000 annual bonus renewal miles (worth S$150)

- Unlimited lounge access, limo transfers & more

- Up to 19% fuel savings with Caltex

- Cons

- High S$488 annual fee (no waiver)

- Recurring bills ineligible for rewards

- Access to limo transfers requires S$5,000 minimum spend

|

If you're seeking flexible miles rewards both at home and abroad–paired with great travel perks–you're likely to benefit from OCBC Voyage Card. Cardholders enjoy high rates of 2.2 miles per S$1 overseas, 1.3 miles locally. As a result, it's fairly easy to continue earning even when you're not abroad (compared to other luxury cards, which heavily favour overseas spend).

Of the cards that do reward local spend with high miles rates, OCBC Voyage is one of the few that also offers luxury travel perks. Cardholders receive unlimited airport lounge access, 2 free limo transfers per month, and even 50% off green fees at fairways throughout SE Asia. This card does come at a cost–a S$488 annual fee, to be exact–but its high rates and luxury perks make OCBC Voyage worth considering for the wealthy consumer. |

Best Rewards Credit Cards for Low Spenders

Standing out for their affordability as well as the accessibility of high rewards rates, find the best rewards credit cards in Singapore suitable for low spenders.

OCBC Frank: No-Fee & Low Min. Spend Requirement

- Pros

- 6% rebate on online, mobile contactless, and FX spend

- Fee waiver with S$10,000 annual spend

- Cons

- 0.3% rebate on general purchases

- Annual fee after 2 years

- Capped cashback at S$75

If you’re looking for an accessible cashback card that rewards social and online spending with high rates, OCBC Frank Card is one of the best options available. First of all, OCBC Frank Card rewards consumers who are comfortable with technology–specifically, cardholders earn 6% cashback on online, FX, and mobile contactless purchases. These boosted rates are accompanied by a 0.3% on all other purchases, which has no minimum spend requirement. Rewards are capped at S$75/month (separate S$25 limits for online, FX & mobile contactless, and general spend).

What makes OCBC Frank Card special is that young adults can access these rates after just S$600 spend. Competitor cards with similar rewards rates have minimums above S$600. Finally, the already low S$80.0 fee is waived 2 years, and then with S$10,000 annual spend. Most competitors don’t offer a fee waiver. Overall, OCBC Frank Card is the easiest and most accessible way for young consumers to earn on online & mobile spend. | |

- Pros

- 6% rebate on online, mobile contactless, and FX spend

- Fee waiver with S$10,000 annual spend

- Cons

- 0.3% rebate on general purchases

- Annual fee after 2 years

- Capped cashback at S$75

|

If you’re looking for an accessible cashback card that rewards social and online spending with high rates, OCBC Frank Card is one of the best options available. First of all, OCBC Frank Card rewards consumers who are comfortable with technology–specifically, cardholders earn 6% cashback on online, FX, and mobile contactless purchases. These boosted rates are accompanied by a 0.3% on all other purchases, which has no minimum spend requirement. Rewards are capped at S$75/month (separate S$25 limits for online, FX & mobile contactless, and general spend).

What makes OCBC Frank Card special is that young adults can access these rates after just S$600 spend. Competitor cards with similar rewards rates have minimums above S$600. Finally, the already low S$80.0 fee is waived 2 years, and then with S$10,000 annual spend. Most competitors don’t offer a fee waiver. Overall, OCBC Frank Card is the easiest and most accessible way for young consumers to earn on online & mobile spend. |

Citi SMRT Card: Top Rebates for Young Professionals

- Pros

- Good rewards rates for modest budgets

- SMRT$ rewards on EZ-Reload transactions

- Cons

- Not suitable for higher budgets

- Lacks travel and overseas rewards

Citi SMRT Card is the best card on the market for young professionals because of its accessibility and balance between rewarding essential and leisure spend. Cardholders earn 5% rebate on groceries, online purchases, EZ–Link Auto top-up and taxi rides, all after S$500 minimum spend. In fact, there isn’t a cashback card out there with a lower minimum spend, making Citi SMRT Card excellent for a modest budget. Citi SMRT Card also has EZ-Link functionality and rewards Auto Top-Ups with 5% rebate–a perfect way to earn from your daily commute.

| |

- Pros

- Good rewards rates for modest budgets

- SMRT$ rewards on EZ-Reload transactions

- Cons

- Not suitable for higher budgets

- Lacks travel and overseas rewards

|

Citi SMRT Card is the best card on the market for young professionals because of its accessibility and balance between rewarding essential and leisure spend. Cardholders earn 5% rebate on groceries, online purchases, EZ–Link Auto top-up and taxi rides, all after S$500 minimum spend. In fact, there isn’t a cashback card out there with a lower minimum spend, making Citi SMRT Card excellent for a modest budget. Citi SMRT Card also has EZ-Link functionality and rewards Auto Top-Ups with 5% rebate–a perfect way to earn from your daily commute.

|

Maybank Platinum Visa: Flat Rebate for Small Budgets

- Pros

- Great starter card for young adults

- Good fit for budgets between S$300 and S$500/month

- S$80 annual fee

- Cons

- Few extra perks

- Doesn't award specialised spend (ie dining, shopping)

If you spend between S$300 to S$500/month, Maybank Platinum Visa Card is an excellent way to maximise cashback on daily spend while also avoiding an annual fee. While most cashback cards require at least S$500 minimum spend, Maybank Platinum Visa Card offers S$30/quarter with just S$300 monthly spend–allowing cardholders to earn S$120/year with just S$1,200 annual spend. With typical cashback cards, this spend level would earn at just 0.3%–spending S$1,200 would earn just S$3.6.

| |

- Pros

- Great starter card for young adults

- Good fit for budgets between S$300 and S$500/month

- S$80 annual fee

- Cons

- Few extra perks

- Doesn't award specialised spend (ie dining, shopping)

|

If you spend between S$300 to S$500/month, Maybank Platinum Visa Card is an excellent way to maximise cashback on daily spend while also avoiding an annual fee. While most cashback cards require at least S$500 minimum spend, Maybank Platinum Visa Card offers S$30/quarter with just S$300 monthly spend–allowing cardholders to earn S$120/year with just S$1,200 annual spend. With typical cashback cards, this spend level would earn at just 0.3%–spending S$1,200 would earn just S$3.6.

|

Best Rewards Credit Cards for Online & Mobile Pay

Modern online shoppers and those who prefer contactless pay can maximise earnings with these rewards credit cards.

HSBC Revolution: No-Fee Miles for Social & Online Spend

- Pros

- Great rewards on local dining and entertainment

- Online shopping perks

- No-fee card

- Cons

- Lacks rewards for frequent travellers who spend large amounts overseas

- Not suitable for low budgets

If you’re a social spender, HSBC Revolution Card is one of the few cards that offers high local rates without minimums or earnings caps. While most miles cards skew towards rewarding overseas spend, HSBC Revolution offers high rates for local spend. Cardholders earn 4 miles per S$1 on online and contactless spend, or 2.5% cashback, which is up to twice the rate offered by traditional miles cards.

| |

- Pros

- Great rewards on local dining and entertainment

- Online shopping perks

- No-fee card

- Cons

- Lacks rewards for frequent travellers who spend large amounts overseas

- Not suitable for low budgets

|

If you’re a social spender, HSBC Revolution Card is one of the few cards that offers high local rates without minimums or earnings caps. While most miles cards skew towards rewarding overseas spend, HSBC Revolution offers high rates for local spend. Cardholders earn 4 miles per S$1 on online and contactless spend, or 2.5% cashback, which is up to twice the rate offered by traditional miles cards.

|

DBS Live Fresh: Easy Rebates for Modern Spenders

- Pros

- Great rewards on contactless payment methods (Visa payWave)

- Green cashback on eco-eateries and retailers

- Various entertainment discounts and promotions

- Cons

- Lacks travel and overseas spend rewards

- Not suitable for low budgets

If you're a modern spender who frequently shops online and feels comfortable using digital wallets, look no further than DBS Live Fresh Card. Cardholders earn an impressive 5% cashback for spend in both categories, and an additional 5% on sustainable spend, with a total monthly cashback cap at S$75/month. There is a S$600 minimum spend requirement to access these rates, but it's slightly lower than the S$800 required by most competitors. Paired with its SimplyGo functionality, DBS Live Fresh Card's rewards structure is great for people looking to streamline their wallets and maximise rebates from tech-forward spend methods.

| |

- Pros

- Great rewards on contactless payment methods (Visa payWave)

- Green cashback on eco-eateries and retailers

- Various entertainment discounts and promotions

- Cons

- Lacks travel and overseas spend rewards

- Not suitable for low budgets

|

If you're a modern spender who frequently shops online and feels comfortable using digital wallets, look no further than DBS Live Fresh Card. Cardholders earn an impressive 5% cashback for spend in both categories, and an additional 5% on sustainable spend, with a total monthly cashback cap at S$75/month. There is a S$600 minimum spend requirement to access these rates, but it's slightly lower than the S$800 required by most competitors. Paired with its SimplyGo functionality, DBS Live Fresh Card's rewards structure is great for people looking to streamline their wallets and maximise rebates from tech-forward spend methods.

|

Learn More About Selecting the Best Rewards Card for You

While most consumers shopping for a rewards credit card just want to find out "What is the best rewards card?", the answer unfortunately depends on many different factors. Which rewards card will be the best for you will depend entirely on your personal spending, travel and credit habits. Taking a moment to consider your personal preferences before searching for a card will go a long way in helping you find the best deal.

In exchange for giving you bonuses and rewards, rewards credit cards always charge an extremely high interest rates around 25%. If you're unable to pay off your monthly charges in entirety, additional interest will easily exceed what you earn in rewards. Therefore, rewards cards are only beneficial for consumers who pay off their credit card bills on time on a monthly basis. If you are having difficulty in doing this, you should consider getting a low interest credit card or sticking to using cash. You're much better off reducing your interest payments than trying to get a few percentage points in rewards.

For you to benefit from rewards cards, you actually have to use them. People tend to rack up miles and points that are never used. Even worse, many miles and reward points expire within a certain time frame. For those consumers these rewards might as well be worth nothing. Since some rewards expire, you might want to consider whether you like save up towards one big redemption or want to be redeem rewards as frequently as possible.

Also, consider what kind of rewards you actually will be likely to use. Do you travel frequently, and would like to get free air tickets? Or would you rather receive cashback for daily purchases?

Lastly, you should consider how much you value flexibility. While cashback rewards are often immediately awarded, redeeming miles often take weeks of preparation because of processing time, and it may be more difficult to earn a free trip than you would like.

Cards with the highest rewards rates often come with a high annual fee and minimum spend requirements. With many no-fee rewards credit card options available, the decision to pay an annual fee will depend on the amount you will spend on the card. As a rule of thumb, you should plan to spend at least S$500 a month per card for a fee-based rewards card to be viable.

What credit card you should choose should depend first on how much money you spend. For example, my friend Robert makes S$50,000 a year, and spends about S$2,000 on his UOB One Card on a monthly basis. UOB One Card is a great cashback card that provides up to 5% cash rebate for all of your expenditures, plus some other benefits like discounts on petrol. Based on Rob's spending level, this translates to about S$1,200 of cash rebate annually, which nets out to S$2,207.4 in rebate over 2 years after subtracting S$192.6 of annual fee (which is waived for 1 year). While this may seem great, one should wonder: what if Robert spends less money?

Because UOB One Card requires at least S$2,000 of monthly spend to qualify for the 5% rebate, anything less would only earn maximum 3.33% of flat rate cashback. This means that my other friend Henry, who only spends S$1,000 on his card every month, can only earn S$607.4 in net cash rebate over 2 years if he uses the UOB One Card. In this case, Henry may have been better off by using a card like OCBC 365 Card, which earns cash rebate and waives the annual fee for anyone who spends S$10,000 per year on the card. To be specific, OCBC 365 earns 24% on petrol, 3% on online shopping, up to 6% on dining and 3% on groceries, among other things.

Let's now assume that my third friend Tom is a foodie who loves to eat well. However, he doesn't care that much about traveling, shopping or entertainment (i.e. bars, karaokes, etc.). Therefore, he spends about 60% of his monthly budget on dining and groceries, while Henry only spends 35% of his spending on these two categories. In this case, Tom should prefer to use Citi Cash Back Card over using OCBC 365 Card, since Citi Cash Back card earns 8% cash rebate on all of his dining and grocery bills.

There are many other factors besides your spending patterns that you must consider before choosing the right credit card. For instance, you may want to go for an air miles credit card instead of a cash back card if you tend to travel frequently. This is especially so for people who like to redeem their miles for business class or first class seats. Our study has shown that 1 mile can be worth up to S$0.08 for longer and more expensive flights, compared to S$0.01 conversion rate for economy flights.

Let's consider our example of Robert again from the scenario above, who spends about S$2,000 per month on his card. If he used a Citi PremierMiles Visa Card, he could be earning about 110,920 of miles over 2 years, plus additional savings on petrol, according to our calculations. This is because Citi PMV card awards 1.2 miles for every S$1 you spend locally and 2 miles for S$1 you spend overseas. If you were to convert the 111,000 miles you earn at a S$0.03 to 1 mile rate (i.e. short-haul business class seat), that's worth significantly more than the cashback Robert would earn on UOB One Card even after subtracting the annual fees. On the other hand, if Rob used his miles at a S$0.01 per mile rate, or never redeemed his miles at all, then UOB One Card would be the better deal.

In examining the different rewards credit cards, we looked at different factors that should influence your decision. Understanding all these different aspects can help you figure out just how good a card really is.

How Do the Rewards Work?: While most cards use the same set of terms (points, miles, cash back), the ways these rewards work will vary significantly. Some rewards can be applied as statement credits, as cashback, as reward points or as miles. Some cards will even allow for conversion between rewards points and miles. While cashback and statement credits are two best options for most people, miles can be highly valuable for those who redeem them for long-haul flights on business class or better. Some cards also allow you to transfer your rewards to other loyalty programs giving you another way to use what you've earned.

Rewards Rate: If your rewards card is going to be your primary card then the rewards rate for general spending is very important. For everyday spending you can expect to earn up to 5% of what you spend as rewards. As a rule of thumb, the more flexible the type of reward you get, the lower the rewards rate you can expect. Otherwise, you could pick a few cards that collectively offer high award rates on most of your expenditures.

Welcome & Renewal Bonuses Matter: The promotions offered to new card holders and renewal bonuses are major contributors of the value you can get from rewards cards. Most of these bonuses require you to either make a purchase on the card or spend a certain amount within a set time limit. Because the value of welcome bonuses and renewal bonuses can range from S$50 - S$500, you should make sure to fulfill the qualifications.

FAQs

Credit cards allow you to spend credit provided by the bank which you then have to repay. When you receive a credit card, your credit card limit is the maximum amount you have been approved for at the time of your application. This is highly dependent on your annual income. The great benefit of having a credit card is that, depending on the card itself, you can receive cashback on various purchases, discounts and perks on travel, dining, sports and other activities.

Depending on whether you are a student, an employed citizen or foreigner, the requirements you must meet to apply for a credit card vary. Typically, you are required to have a minimum annual salary of S$30,000, and to provide your payslips, most recent Tax Assessment and a copy of your NRIC. Read our guide to see specific details about these requirements.

With more than 100 credit cards available in Singapore, there is a credit card for every spending profile, income level and spending preference. Read our guide to find out which credit card is best for you.

- Cashback: Cashback credit cards, also known as rebate cards, are named as such because they reward spend with cash credit equal to a given percentage of the transaction amount. For example, a credit card may offer 5% cashback on dining. Using that credit card to pay a S$100 restaurant bill will then earn S$5 in cash credit rewards. Cashback credits usually cannot be redeemed as actual cash. Instead, rebates are usually automatically applied to the next monthly card statement to offset the bill. Because of this automation, cashback cards are quite simple to use. This makes them a great choice for credit card beginners or those seeking an easy-to-use card for daily essentials.

- Miles: Travel cards offer cardholders air miles for their purchases. Unlike cashback cards, rewards are usually differentiated by local vs. overseas spend, rather than by individual spend category (ie dining, transport, etc). Miles cards also typically offer higher rewards rates for purchases made in foreign currency. They also often offer luxury perks ranging from airport lounge access to free travel insurance, golfing privileges & more. For these reasons, travel cards are understandably popular with frequent travellers who can take advantage of miles rewards while enjoying luxury perks. Miles cards also rarely have minimum spend requirements or rewards earning caps, but they tend to have higher (and often non-waivable) annual fees.

- Points: The most typical kind of points credit cards is shopper cards. In this case, a certain number of points are earned per S$1 spend. However, points are often represented in miles form instead. For example, if S$1 spend earns 10 points, but cardholders can redeem 10 points for 4 miles on the rewards platform, it's safe to say that spending S$1 earns 4 miles. Points can also be redeemed for other rewards such as cash vouchers, merchandise, or credit with select vendors. However, the value gained from redeeming points for such items is typically lower that the redemption rate for miles.

Selecting the right credit card depends both on spending behaviour & a few key factors.

To begin with, nearly all credit cards have annual fees that can limit accessibility or diminish earnings. Travel credit cards tend to have higher annual fees, but some–alongside several rebate cards–offer condition-based fee-waivers. In these cases, a consumer can avoid paying the annual fee if they achieve a minimum spend by the end of the year (ie, waiver granted with S$12k annual spend). Many cards also waive the annual fee for the first 1-3 years after approval, making it easy to get started with the card upfront. Nonetheless, even if the annual fee seems achievable, it's possible to end up with a nett loss by the end of the year. In other words, if earnings from the credit card do not exceed the fee, you'll actually end up losing money. This is one reason it's important to pick a card that rewards your lifestyle.

In addition to annual fees, minimum spend requirements are important to consider. Minimum spend requirements reflect how much a cardholder must spend in order to unlock higher rewards rates as advertised. For example, a card might require S$800 minimum spend for the month in order to earn a 8% rebate that month. Spending even S$1 less than the minimum may result in the cardholder earning at a base rate of just 0.2%–0.3%, which translates to a massive loss in earnings potential. It's incredibly important to review a card's minimum spend requirement before applying. If you can't reliably achieve the given amount, you won't be able to access meaningful rewards rates.

Finally, make sure to review the overall rewards system structure. Choose a card that rewards categories you're most likely to spend on. Many cards cater to specific profiles (retail shoppers, travellers, everyday spenders & more) which can make selection a bit easier. It's essential to keep in mind that while high rewards rates can be very tempting, they won't prove beneficial unless you're likely to spend in the rewarded category.

Considering these factors together can help you to find a credit card that will truly maximise earnings for your spend.

That largely depends on your spending habits. There are credit cards best suited for high or low spenders, for frequent travelers and those looking for no fee credit cards. For example, DBS Altitude Visacredit card is a great option for frequent travelers looking for affordable luxury perks, while OCBC 365 Card card may be a better option for those looking for those with broad spending habits seeking daily rebates.

Rewards credit cards can be worth it if you can find one that fits your needs and your spending profile. The best option is to find a card which rewards your spending behavior without requiring you to change your habits. Read our guide to figure out which one is the best fit for you.

Rewards credit cards generally reward certain spending habits and spending amounts, based on the terms of the given credit card. Cashback credit cards do just that: they give you cashback on certain everyday purchases. While cashback cards provide a nearly immediate reward, that is cash on your credit card, rewards credit cards work differently. Some in addition to providing cashback and rebates, reward you with accumulating points on certain purchases which in turn, provide other travel and entertainment perks over time. Rewards credit cards can often be part of a rewards program, which come with their own benefits.

Read More:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.