5 Things Your Friends Say About Personal Loans That Are Wrong

Personal loans are incredibly popular in Singapore. Given that they neither require a collateral nor limits how you can use the money, it's not surprising that even Google sees the highest level of consumer interest in this product than other financial instruments. However, there are also many misconceptions about this product that can cost you if you believe them.

Misconception 1: Personal loan is the best way to pay off credit cards

Personal loans used to be one of the best ways to pay off one's credit card debt. However, this is no longer the case. Earlier this year, MAS introduced a new instrument called debt consolidation plan, which is effectively a spinoff of personal loan that is specifically designed for paying of other liabilities. While personal loans can be used for any purpose, debt consolidation plans have a more specific use of paying off your loans and therefore charge a slightly lower interest rate. For instance, HSBC offers one of the lowest interest rates for both personal loans and for debt consolidation plans in Singapore. However, its debt consolidation plan is 0.1% to 0.8% cheaper than its personal loan offering for tenures between 1 and 7 years. For a loan of S$20,000, this could mean difference in cost of S$60 to S$420.

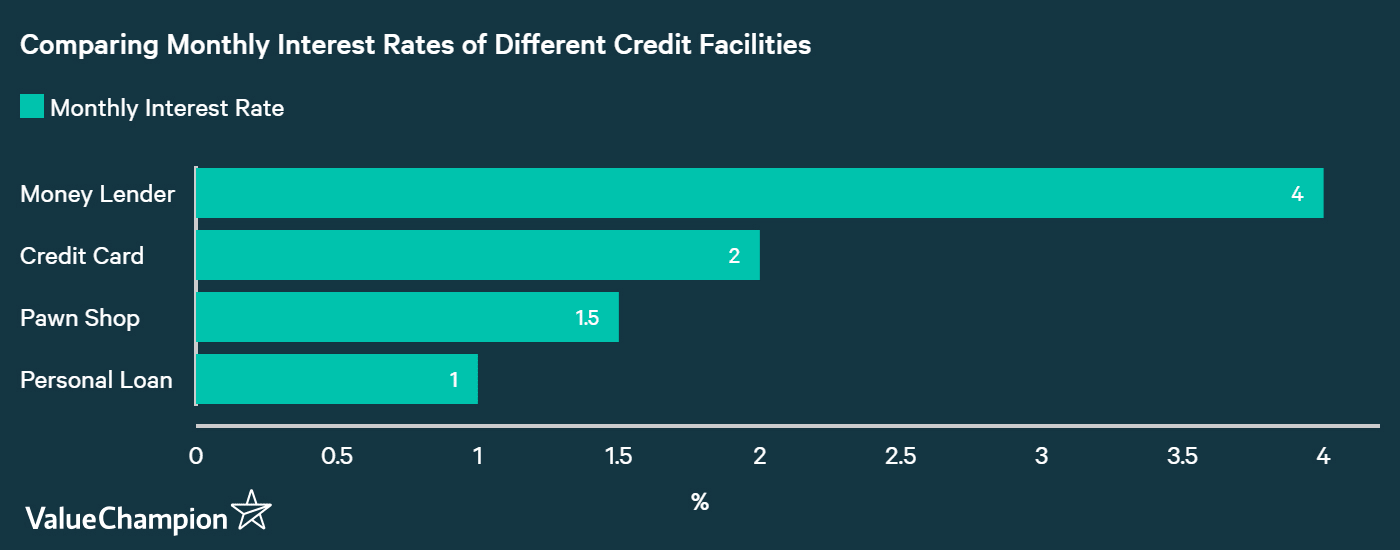

Misconception 2: Personal loan is the priciest loan type

While the average interest rate of personal loans may be higher than that of secured loans like home loans or car loans, it's still significantly lower than that of other unsecured loans that don't require any collateral. For instance, a payday loan from a money lender or cash advance from your credit card can easily be 2-4x higher than that of a personal loan. Therefore, just because you may have heard bad things about personal loans, it doesn't mean that you should avoid it at all costs. When you are in a desperate need for cash, it can actually be one of the best channels for securing what you need compared to other methods that can be just as easy.

For instance, building an unpaid balance S$10,000 on your credit card to make a big purchase can cost you S$1,300 in interest and S$1,025 in monthly payment even if you were pay down this balance over the course of a year. In contrast, getting a personal loan to make the S$10,000 payment should only cost you about S$500 in interest and fees. A credit card APR of 25% and a personal loan effective interest rate of 9% can make a world of a difference.

Misconception 3: Get personal loans buy your new TV (or do anything else you want)

Just because you can use something for anything does not mean that you should. This is a trap common to personal loan borrowers. Because a personal loan can be used for anything, they think they can just apply for one to buy an expensive TV they can't afford right now. Sure it's still cheaper than credit card debt, but it's still a pretty expensive source of capital that should be used selectively.

Some good use cases of personal loans include emergencies or big life time events, like surgery, emergency room bill, wedding or honeymoon. As long as you have a stable source of income to help you make the scheduled monthly repayment of a loan, it's not such a bad idea to get some financing so that you can do what you have to do. But, adding a few hundreds if not thousands of dollars of extra monthly obligations that you must pay off for a few years isn't really worth just for a random, spontaneous purchase you didn't need to make.

Misconception 4: Lenders all charge the same

With all the comparison websites and other information available online, one would expect that most banks charge similar price on personal loans. However, this cannot be farther from the truth. In fact, most banks differ on both interest rates and fees. For instance, our own comparison of all the personal loan offerings in Singapore have found that the effective interest rate, which accounts for both the processing fee and the interest rate, can vary from 9% per year to 26% per year even amongst the biggest banks in Singapore.

Therefore, it's highly advisable to compare the EIR of each offering instead of just going by the interest rate when looking for a personal loan. Not only that, different lenders can have varying degrees of penalty fees for late or early repayments, so at-risk borrowers should be conscious of these terms before applying for a loan.

Misconception 5: Need high credit score to qualify

Not having a great credit score doesn't preclude you from getting a personal loan. In fact, most banks use your annual income as an eligibility requirement instead of your credit score. As long as your credit score isn't dismal, you should be able to secure some amount of personal loan from a bank at the advertised rate. Most loans are available for people with an annual income of at least S$30,000, though there are definitely offerings for people with less income. For instance, Standard Chartered currently provides some of the lowest rates on personal loan for people who make an annual income between S$20,000 and S$30,000.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.