5 Uncomfortable Financial Conversations You Must Have with Your Loved Ones

It can be awkward or even painful to have tough financial discussions with your loved ones. However, avoiding these conversations can be disastrous for your relationships and financial future. In this article we aim to outline these important conversations to help you conceptualise them and to eventually broach these conversations.

Get on The Same Page Financially Before Getting Married

Getting married requires you to be direct and honest as well as make compromises. When it comes to personal finances, different couples have different approaches, but there are a few things that you should definitely consider together before you end up tying the knot.

Be Honest About Your Personal Debt

If you or your partner have accumulated a significant amount of personal debt, you will want to discuss this before getting married or before combining your financial assets. This is an important conversation for couples, as debt can be a significant source of stress. It also may restrict your budget at times, so you'll want to be open and honest in order to avoid any more difficult conversations.

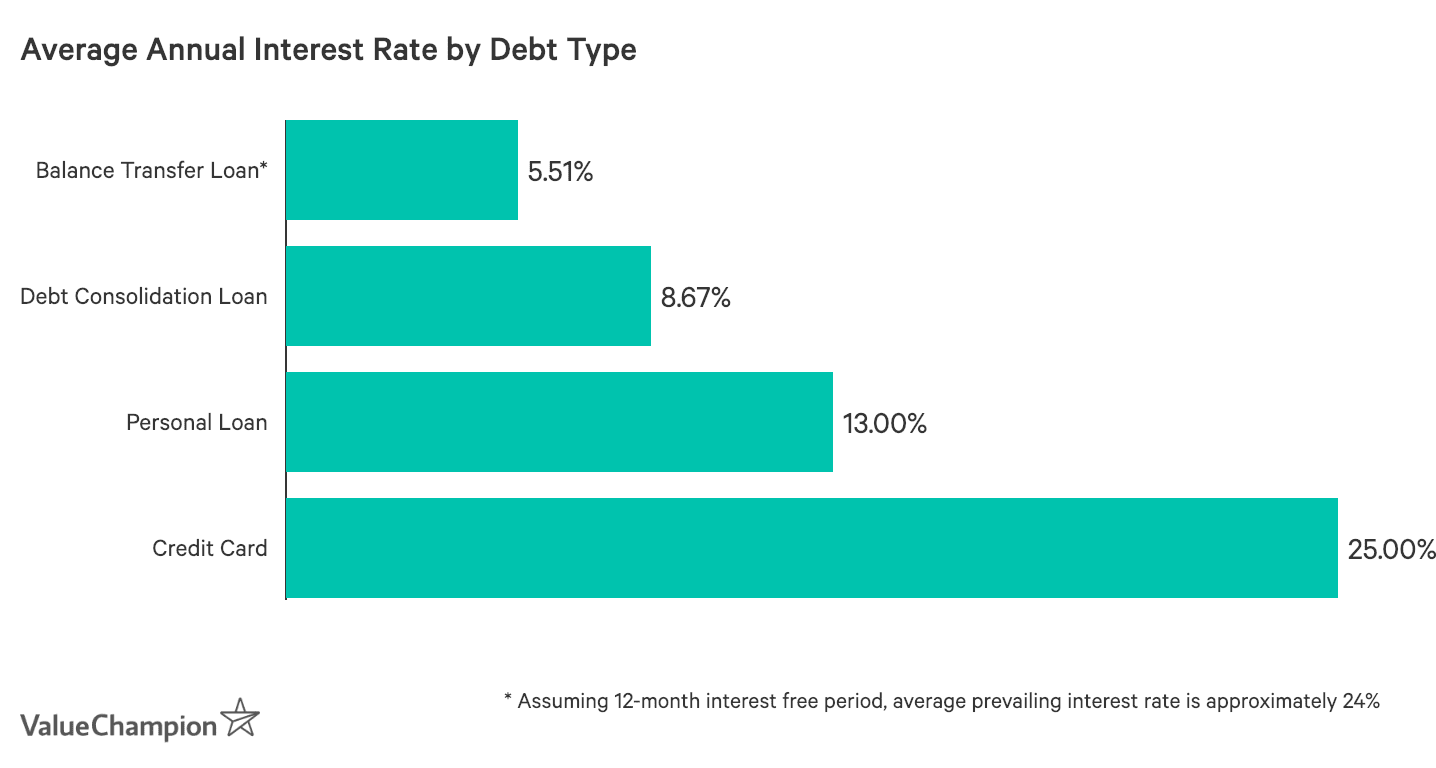

If you have a lot of credit card or other personal debt, you may want to consider a debt consolidation plan or balance transfer loan to help you pay down your obligations. Balance transfer loans allow borrowers to transfer their current personal debt to a loan that typically comes with a 3 to 12-month interest free period in which you can make repay a big chunk of your debt without incurring more interest. Debt consolidation loans are another great option, which tend to charge significantly lower rates than other types of debt, making them a good way to repay debt over a longer period of time. For example, the average personal loan rate is about 13%, while those debt consolidation loans tend to be about 9%.

Will You Apply for a BTO Flat Before Marriage?

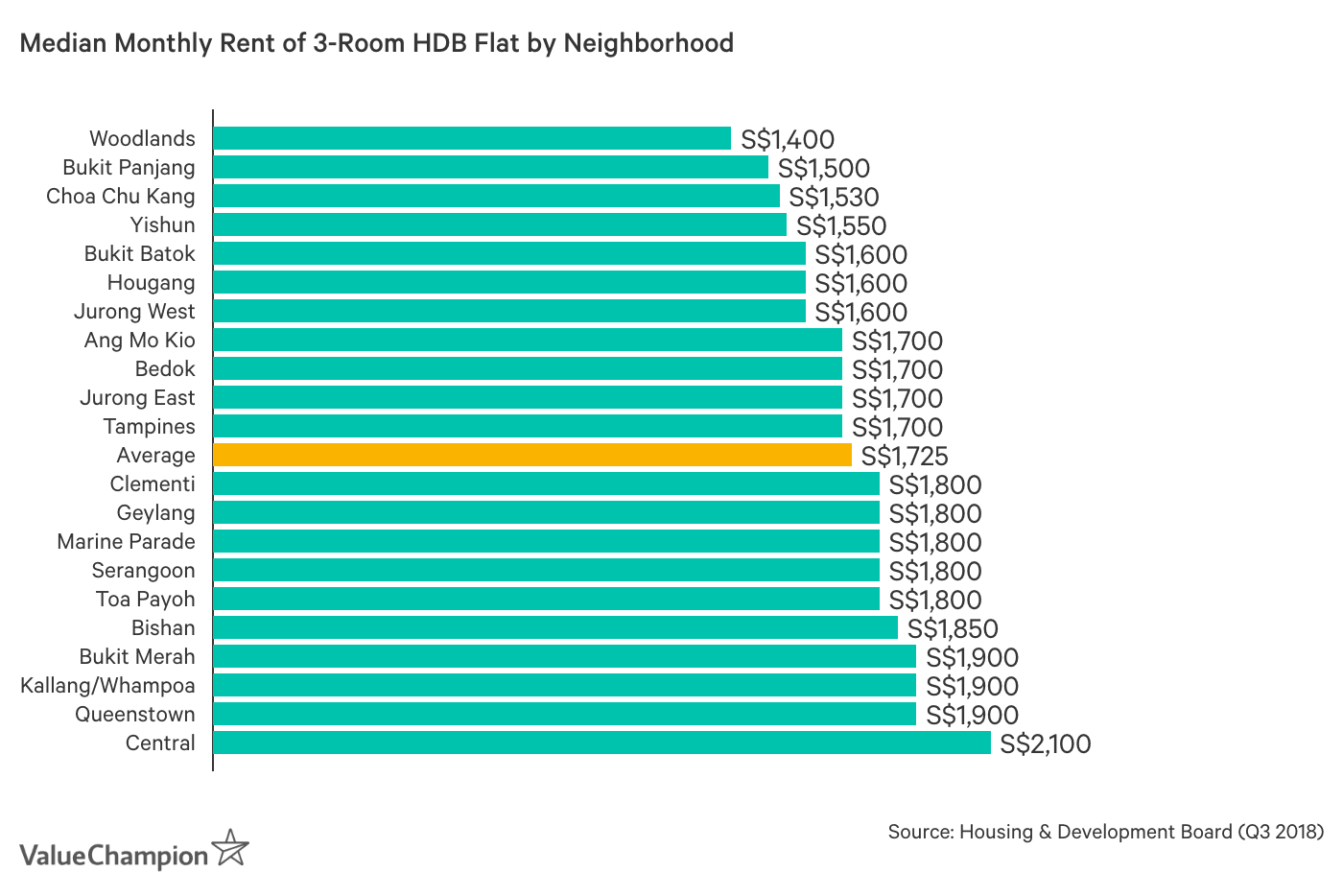

Those that are on good financial footing may be excited to buy a home and start their lives together. Due to long wait periods, many couples in Singapore apply for BTO units before they are officially married. While there are clearly benefits to this approach, you should also be aware of the potential downside. If you cancel your booking for a BTO unit, you may end up forfeiting thousands of dollars. For this reason, you may not want to rush your first home purchase. Instead, you may choose to rent as a couple before you purchase an HDB flat.

Before Your Child Attends University, Explain the Financial Cost and Benefits

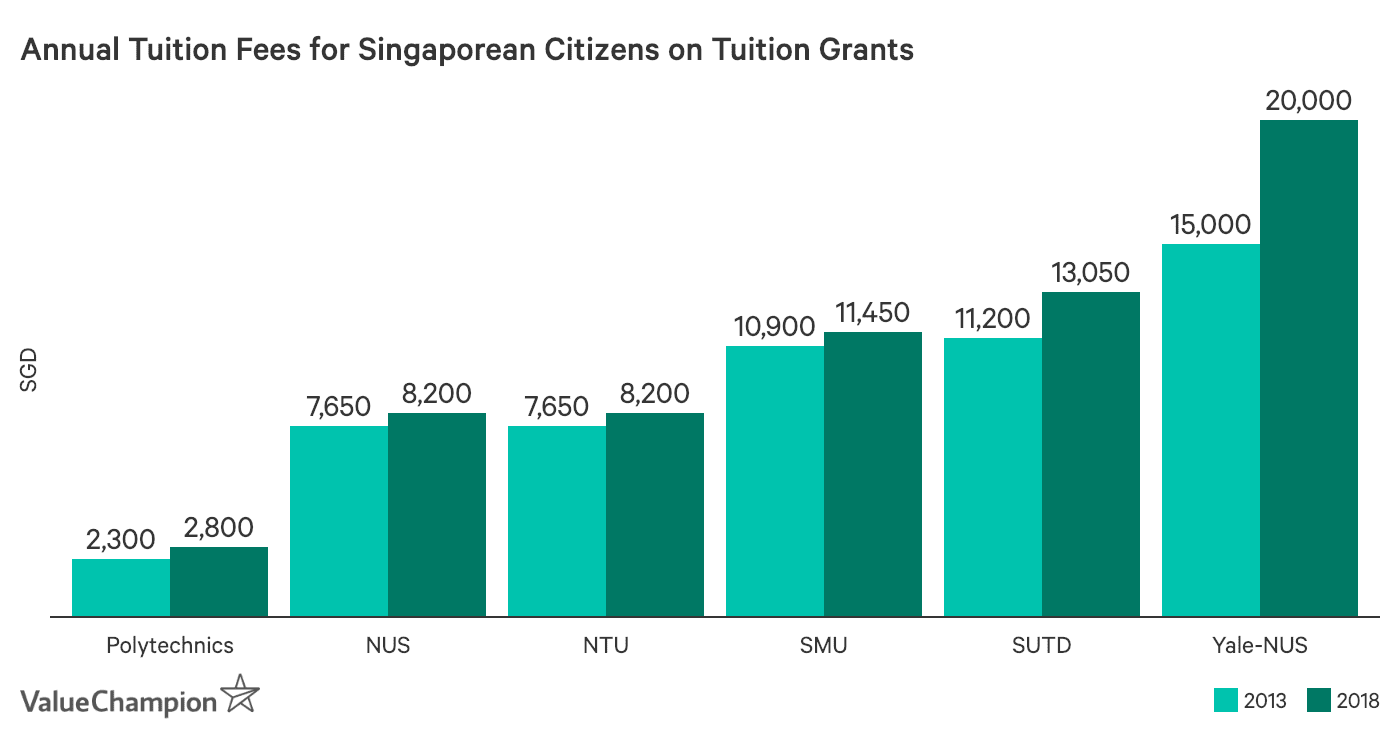

For those that are already married, many big financial decisions may revolve around your children. If your child would like to attend university someday, it is important to help support them academically so they will be prepared for this challenge. It is also important to help them understand this investment by explaining the difference in cost between various programs. For example, studying overseas or for a four-year degree is typically more expensive than studying locally or for a 2-year programme.

Of course, the sticker price of each school is not the entire story. If your child knows what kind of programme they are interested in pursuing, you can help them explore career opportunities and understand the approximate returns of each major. Furthermore, it is important to help explain the burden of student loans as well as the benefit of these financing tools if your family does not have enough money to pay for their tuition in full. For some students, part-time work will also be appealing, so you will want to chat about balancing this work with their coursework.

Discussions with Parents

Some of the most difficult discussions can be the ones you should have with your parents. It can be hard for older people to accept advice from their children and it can be tough to bring up these conversations to the people who raised you. Still, it is important to understand your parent's needs, so these discussions are important.

Does Downsizing Make Sense?

For some elderly people, living in a larger home is unnecessary or even burdensome. For example, parents may have picked out their current flat or house when they were raising children. After these children leave the home to start their own lives, the space can be a chore to clean and maintain.

Furthermore, elderly retirees may be eligible for as much as S$20,000 if they choose to downsize to a smaller HDB flat through the Silver Housing Bonus. This programme provides a cash bonus to individuals that top-up their CPF Account after selling their current flat. Therefore, it is important to know if your parent(s) would benefit or be interested in downsizing from their current home.

Silver Housing Bonus Requirements

- Owner is Singapore Citizen, 55 years or older

- Gross monthly household income does not exceed $12,000

- Selling HDB flat or private property with Annual Value of S$13,000 or less

- Purchasing HDB flat (3-room or smaller)

- Purchase price does not exceed sale price

- No concurrent ownership of second property

What Happens When Loved Ones Pass On

Having a conversation to understand your parent's post-life wishes may be even more upsetting, but is equally important. For example, you will want to make funeral arrangements that your parent would appreciate. In Singapore, this can cost several thousands of dollars, so proper planning is essential. Additionally, you will want to understand their financial positions, such as any life insurance plans, investments or personal debts. If they do not already have a will, you may want to discuss this together as a family.

Major Takeaways: Be Honest & Plan Ahead

One crucial theme throughout this list is to have these important conversations before you are immediately confronted with financial decisions. If you take an open and honest approach with your loved ones and give yourselves time to make these big decisions, you are all more likely to end up better off.