The Cost of Wedding Banquets Is Soaring in Singapore

If you are planning to get married soon, there's an uncomfortable fact that you need to be aware of: the cost of wedding in Singapore is rising extremely quickly. What's even more interesting is that this is occurring amidst trouble in the overall food and beverage sector in the country and the economy is expected to be "sluggish" in the months ahead. Below, we discuss our findings of collecting and analyzing prices of 47 most well-known wedding banquet venues in Singapore.

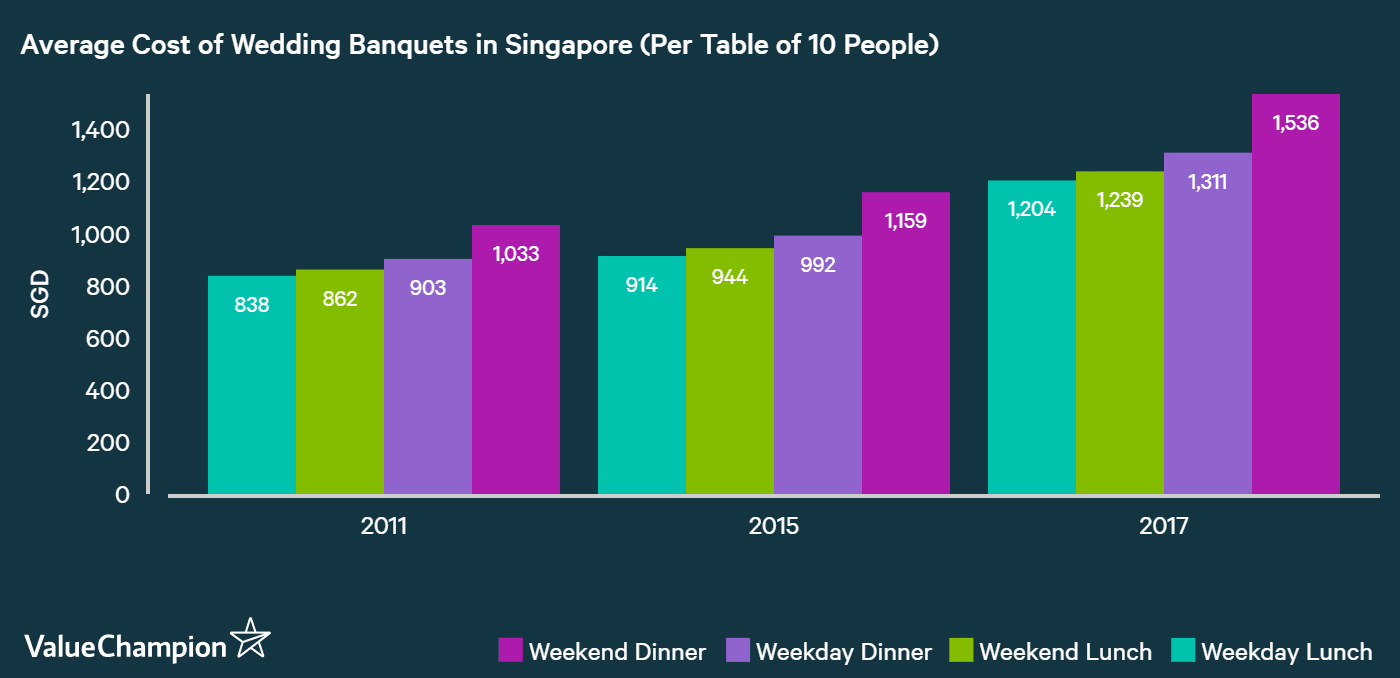

The Cost of Wedding Banquets Has Risen by Almost 50% Since 2011

By comparing the average price of 47 different banquet venues in 2011, 2015 and 2017, our team at ValueChampion found that the average price of these 47 locations has risen by 49% from S$1,033 (for a weekend dinner) in 2011 to S$1,536 in 2017. This growth was more than 2x higher than the 22% increase in median income excluding CPF contribution, and almost 6x higher than rate of inflation of 8.6% since 2011. To put that in perspective, that represents around S$46,100 of cost for a banquet with 300 people. Given that the median income excluding CPF contribution was around S$3,600 in 2016, this means that an average person has to save 13-month's worth of salary in order to afford a wedding even before considering other costs like wedding gown, honeymoon, wedding ring, etc.

What's also interesting is that the increase in banquet price has accelerated meaningfully since 2015. For instance, the average cost of a banquet on a weekend grew only by 13% from 2011 to 2015. Since 2015, however, it jumped a whopping 34%. Furthermore, this change in pricing was tended to be more dramatic for high-end venues. For example, Ritz Carlton & Sofitel Sentosa Resort's prices increased by 74-79% from S$1,200-S$1,300 in 2011 to S$2,100-S$2,200 in 2017.

As a side note, ValueChampion's study of 107 banquet venues found that the average cost of wedding banquet in 2017 was around S$1,274 per table (or S$127 per person) for a dinner event on a weekend. This figure is different from what we mentioned above solely because of the sample size. We could only find prices for 47 matching locations in 2011, 2015 and 2017, which lifts up the overall average. However, the overall trend was the same for each locations that we could find data for all three time periods.

Singaporeans Are Getting Married Later in Life

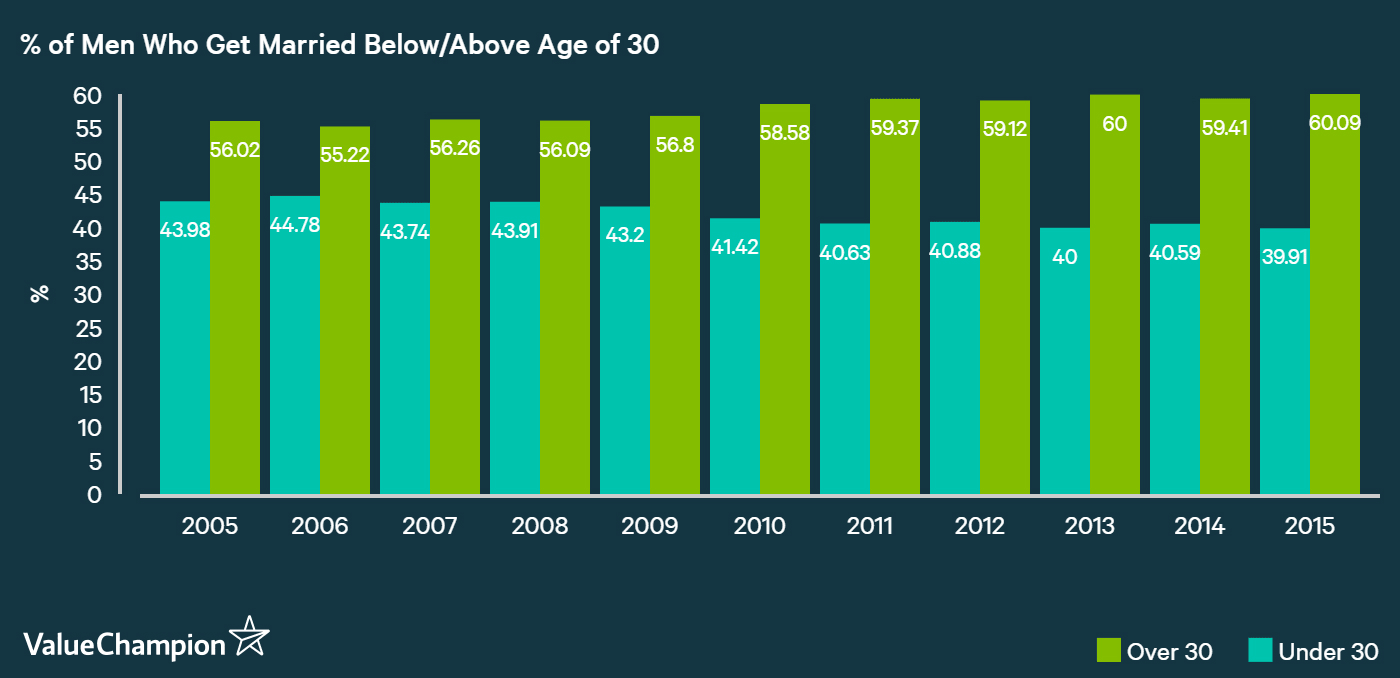

While we don't have enough data to prove any causative relationship, we also found that both men and women in Singapore are choosing to marry later in their life while the cost of wedding has been rising.

For example, back in 2005, about 44% of men married before the age of 30. This declined to about 40.6% of men getting married before the age of 30 by 2011, and has fallen further to 39.9% by 2015.

This change was even more apparent for women. In 2005, about 68% of women married before reaching the age of 30. By 2011, it fell by 6% to 62%. Since then, it fell another 3% to 59% in 2015.

Of course, there are multiple other factors that might be more important in people's decision to get married later in life. While we can't argue that the rise in banquet cost is responsible for this trend of getting married later in life, we think there might be a relationship between the two findings. It could be possible that the higher cost of marriage may contribute to this trend as people might feel the need to save more money than they did 10 years ago in order to comfortably afford the wedding of their dreams.

Related to Rise of Personal Debt?

There are other parallel trends that may be related to our findings. As the increase in cost of expensive but necessary life events like marriage continue to outpace in wage growth, it seems that consumers have resorted to borrowing more to fund their consumption. Even cost of college education has risen by 40% since 2007, compared to just 24% increase in CPI. In response, Singaporean households have been getting an increasing amount of personal debt (comprising of credit card debt, personal loans, study loans, etc.), which now comprises 21% of household's total liabilities, up from just 16% in 2005.

This is a worrying trend, especially as interest rate is set to rise over the next few years. Using debt to fund consumption is viable strategy only when interest rates are extremely low; higher rates can quickly erode borrower's discretionary spending power as more of their income needs to be funneled to finance their debt. Preparing the perfect wedding is great, but we strongly advise our readers to refrain from using too much debt to do so.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.