Compare Cashback Credit Cards

Great Maximum Cashback for Stable Budgets

UOB One Credit Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$40,000 |

|---|---|

| Overall Rewards Rate | 5.22% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

If you spend at least S$2,000 per month and want cashback on daily spend and bills, UOB One Card might just be the right fit for you. You can earn up to 5% rebate on general spend, 10% on Grab and 6% on utilities, adding up to S$300/quarter. This card also gets you petrol discounts at Shell and SPC stations.

- Annual fee: S$192.60 (first year- waived)

- 5% rebate on general spend, up to S$200/quarter (S$2,000 min spend) with min 5 transactions/mo

- Up to 10% on Grab, Shopee, Dairy Farm Singapore & select UOB travel, 1% on utilities bills

- 3.33% rebate, up to S$100/quarter (S$1,000 min spend)

- 3.33% rebate, up to S$50/quarter (S$500 min spend)

- 0.03% rebate on all spend if no rebate earned for calendar year

- Up to 21.15% savings at Shell and 22.66% at SPC

If you spend at least S$2,000 per month and want cashback on daily spend and bills, UOB One Card might just be the right fit for you. You can earn up to 5% rebate on general spend, 10% on Grab and 6% on utilities, adding up to S$300/quarter. This card also gets you petrol discounts at Shell and SPC stations.

- Annual fee: S$192.60 (first year- waived)

- 5% rebate on general spend, up to S$200/quarter (S$2,000 min spend) with min 5 transactions/mo

- Up to 10% on Grab, Shopee, Dairy Farm Singapore & select UOB travel, 1% on utilities bills

- 3.33% rebate, up to S$100/quarter (S$1,000 min spend)

- 3.33% rebate, up to S$50/quarter (S$500 min spend)

- 0.03% rebate on all spend if no rebate earned for calendar year

- Up to 21.15% savings at Shell and 22.66% at SPC

| Annual Income Needed | Citizen: S$30,000 Foreign: S$40,000 |

|---|---|

| Overall Rewards Rate | 5.22% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

Maybank Family & Friends Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 4.83% |

| Annual Fee | S$180.00 |

| Annual Fee Waiver Amount | S$12,000 |

Maybank Family & Friends MasterCard is a good option for earning cash back on essential spending with a moderate budget. Earn 5% on groceries, food delivery, transport and more if you spend S$500/month. If you spend over S$800/month, the cashback rate increases to 8% with a cap of S$80.

- Annual fee: S$180 (3 years fee waiver)

- Up to 8% rebate on 5 preferred categories (dining & food delivery, groceries, retail, petrol discounts & online TV streaming)

- Up to S$125 cashback per month with S$800 min spend

- 0.3% rebate all other spend

Maybank Family & Friends MasterCard is a good option for earning cash back on essential spending with a moderate budget. Earn 5% on groceries, food delivery, transport and more if you spend S$500/month. If you spend over S$800/month, the cashback rate increases to 8% with a cap of S$80.

- Annual fee: S$180 (3 years fee waiver)

- Up to 8% rebate on 5 preferred categories (dining & food delivery, groceries, retail, petrol discounts & online TV streaming)

- Up to S$125 cashback per month with S$800 min spend

- 0.3% rebate all other spend

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 4.83% |

| Annual Fee | S$180.00 |

| Annual Fee Waiver Amount | S$12,000 |

Great High Flat-Rate Cashback for Low Spenders

Maybank Platinum Visa Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 3.76% |

| Annual Fee | S$80.00 |

| Annual Fee Waiver Amount | none |

If you are a young adult with a monthly budget of S$300-S$500/month looking for a starter card, then you should consider Maybank Platinum Visa. At 3.33% cashback on S300 spend, it offers the highest cashback on low spend on the market. With monthly spend of S$1,000 you can earn up to S$100/quarter.

- Annual fee: S$80 (3 years fee waiver)

- Subsequently quarterly service fee is waived w/ card use at least 1x/quarter

- Up to 3.33% on all local and foreign currency spend

- $30 quarterly rebate with at least S$300 monthly spend

- S$100 quarterly rebate with at least S$1,000 monthly spend

- Free travel insurance

If you are a young adult with a monthly budget of S$300-S$500/month looking for a starter card, then you should consider Maybank Platinum Visa. At 3.33% cashback on S300 spend, it offers the highest cashback on low spend on the market. With monthly spend of S$1,000 you can earn up to S$100/quarter.

- Annual fee: S$80 (3 years fee waiver)

- Subsequently quarterly service fee is waived w/ card use at least 1x/quarter

- Up to 3.33% on all local and foreign currency spend

- $30 quarterly rebate with at least S$300 monthly spend

- S$100 quarterly rebate with at least S$1,000 monthly spend

- Free travel insurance

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 3.76% |

| Annual Fee | S$80.00 |

| Annual Fee Waiver Amount | none |

Great Unlimited Cashback for High Spenders

Standard Chartered Simply Cash Credit Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 2.67% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

Standard Chartered Unlimited Cashback Card offers just that, unlimited 1.5% cashback on all purchases with no minimum spend. Best option for affluent spenders with a monthly budget of S$7,000, with this card you can also enjoy 21% fuel savings at Caltex.

- Annual fee waived for two years

- Unlimited 1.5% cashback on all spend

- Caltex petrol discounts up to 21%

Standard Chartered Unlimited Cashback Card offers just that, unlimited 1.5% cashback on all purchases with no minimum spend. Best option for affluent spenders with a monthly budget of S$7,000, with this card you can also enjoy 21% fuel savings at Caltex.

- Annual fee waived for two years

- Unlimited 1.5% cashback on all spend

- Caltex petrol discounts up to 21%

| Annual Income Needed | Citizen: S$30,000 Foreign: S$60,000 |

|---|---|

| Overall Rewards Rate | 2.67% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

CIMB Visa Signature

| Annual Income Needed | Citizen: S$30,000 Foreign: N/A |

|---|---|

| Overall Rewards Rate | 2.63% |

| Annual Fee | S$0.00 |

| Annual Fee Waiver Amount | none |

With CIMB Visa Signature Card, you can earn 10% cashback on online retail, beauty, pet shops, groceries, and cruise line transactions. In addition to the no annual fee, you can enjoy complimentary travel insurance and concierge service.

- Annual fee: free for life

- 10% cashback on groceries, online shopping, beauty, petcare & cruises

- Unlimited 0.2% cashback on all other retail purchases

- Free travel insurance & global concierge

- CIMB 0% Interest i.Pay Instalment Plan

With CIMB Visa Signature Card, you can earn 10% cashback on online retail, beauty, pet shops, groceries, and cruise line transactions. In addition to the no annual fee, you can enjoy complimentary travel insurance and concierge service.

- Annual fee: free for life

- 10% cashback on groceries, online shopping, beauty, petcare & cruises

- Unlimited 0.2% cashback on all other retail purchases

- Free travel insurance & global concierge

- CIMB 0% Interest i.Pay Instalment Plan

| Annual Income Needed | Citizen: S$30,000 Foreign: N/A |

|---|---|

| Overall Rewards Rate | 2.63% |

| Annual Fee | S$0.00 |

| Annual Fee Waiver Amount | none |

UOB EVOL Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$40,000 |

|---|---|

| Overall Rewards Rate | 2.6% |

| Annual Fee | S$192.60 |

| Annual Fee Waiver Amount | none |

UOB EVOL is a great and easy-to-use card for young adults who primarily shop online. With a minimum spend of S$600 per month, you can earn 8% rebate on all online and mobile transactions.

- Annual fee: S$192.60 (first year- waived)

- 8% cashback on online and mobile contactless spend

- 0.3% cashback on all other spend

- S$600 min spend, S$60 cashback cap

- Southeast Asia’s first bio-sourced card

UOB EVOL is a great and easy-to-use card for young adults who primarily shop online. With a minimum spend of S$600 per month, you can earn 8% rebate on all online and mobile transactions.

- Annual fee: S$192.60 (first year- waived)

- 8% cashback on online and mobile contactless spend

- 0.3% cashback on all other spend

- S$600 min spend, S$60 cashback cap

- Southeast Asia’s first bio-sourced card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$40,000 |

|---|---|

| Overall Rewards Rate | 2.6% |

| Annual Fee | S$192.60 |

| Annual Fee Waiver Amount | none |

Best for Getting Cashback on Everyday Purchases

Citi Cash Back Card

| Annual Income Needed | Citizen: S$30,000 Foreign: S$42,000 |

|---|---|

| Overall Rewards Rate | 2.56% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

The Citi Cash Back Card is a good choice for everyday spend, with a generous 8% cash back on groceries, 6% cash back on dining, and discounted petrol at Esso and Shell. Be prepared for the S$800 monthly spend requirement and the annual fee.

- Annual fee: S$194.40 (first year- waived)

- 8% cashback on groceries

- 6% cashback on dining

- Up to 20.88% fuel savings at Esso & Shell and 8% cashback at other petrol stations

- 0.25% cashback on all other purchases

- Min. monthly spend of S$800 required to earn bonus cashback

- Cashback capped at S$80/month

The Citi Cash Back Card is a good choice for everyday spend, with a generous 8% cash back on groceries, 6% cash back on dining, and discounted petrol at Esso and Shell. Be prepared for the S$800 monthly spend requirement and the annual fee.

- Annual fee: S$194.40 (first year- waived)

- 8% cashback on groceries

- 6% cashback on dining

- Up to 20.88% fuel savings at Esso & Shell and 8% cashback at other petrol stations

- 0.25% cashback on all other purchases

- Min. monthly spend of S$800 required to earn bonus cashback

- Cashback capped at S$80/month

| Annual Income Needed | Citizen: S$30,000 Foreign: S$42,000 |

|---|---|

| Overall Rewards Rate | 2.56% |

| Annual Fee | S$194.40 |

| Annual Fee Waiver Amount | none |

Load More

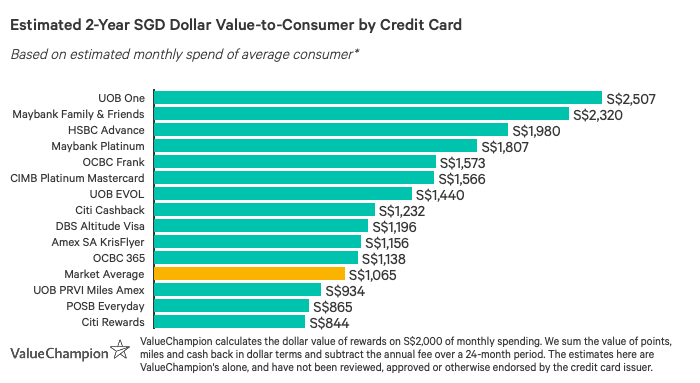

Best Cashback Credit Cards in Singapore

| Credit Card | Best For | Rate |

|---|---|---|

| Maybank Family & Friends | Everyday household spend | 8% |

| OCBC Frank | Online, mobile and foreign currency spend | 6% |

| Citi Cash Back | Dining, groceries and petrol | 6%-8% |

| POSB Everyday | Deliveroo and foodpanda deals | 10% |

| UOB One | Shopee, Dairy Farm and Grab deals | 10% |

| UOB EVOL | Online, mobile spend & sustainable deals | 8% |

| UOB Absolute Cashback | Unlimited cashback on often excluded categories | 1.7% |

If you're interested in a more detailed analysis of Singapore's strongest cashback card options, check out our curated list of picks for different types of consumers.

- UOB One: Highest flat rebate on the market, earn up to $300/qtr

- Maybank Family & Friends: 8% cashback with S$800 min. spend requirement

- Citi Cash Back: Up to 8% rebate on groceries & petrol, 6% on dining

- POSB Everyday: Rebates up to 10% in Singapore

- BOC Visa Infinite: Unlimited 1% earnings on all local purchases, no caps

- OCBC 365: 6% rebate on dining, 3% rebate on groceries, utilities and travel, Visa Concierge Services

- HSBC Visa Platinum: 5% rebate on groceries, dining & petrol, miles for general

- CIMB Platinum MasterCard: 10% rebate on wine and dine, transport, petrol, health and travel, capped at S$100/month

- Citi Cash Back+: Unlimited 1.6% cashback on all spend

- HSBC Advance: Up to 3.5% cashback capped at S$300/month

- OCBC Frank: Up to 6% rebate for FX, online and mobile purchases, low S$600 min. spend requirement

- Citi SMRT: 5% everyday rebates w/S$500 min spend

- Maybank Platinum Visa: Up to 3.33% rebate on local and foreign currency spend

- DBS Live Fresh: Get up to 10% cashback w/ S$600 min. spend - 5% cashback on Online and Visa Contactless Spend, 5% green cashback at selected eco-eateries, retailers and transport services. Additional 0.3% cashback on all other spend

- SC SingPost Spree: 3% rebate online overseas & vPost transactions

- CIMB Visa Signature: 10% cashback on online shopping, groceries, beauty and wellness, pet shops and cruises

- UOB EVOL: Rebates on online and contactless spend with easy fee-waiver

- CIMB World MasterCard: Unlimited 2% cashback on wine and dine, food delivery, entertainment, taxi & automobile, luxury goods and 50% off green fees

How to Choose the Best Cashback Credit Card

Compared to other rewards credit cards, cashback cards are simple to understand: you get back a percentage of the amount you spend using the card, which is credited to your monthly statement. For instance, buying S$100 of groceries using a cashback credit card that gives you 5% cash back on groceries would lead to a credit of S$5 on your statement, or a total cost of S$95 to you on that purchase.

To find the best cashback credit card for your particular needs, fill out the spending categories in our tool as accurately as you can. If you can provide a good estimate of how much money you spend per month in different areas, our rewards calculator will automatically show you a list of cards that would give you the highest value after considering monthly caps and differences in category cashback rates.

FAQs

A cashback credit card is a credit card that gives you a percentage of your spend back in cash, credited to your card. Some cashback cards will credit your account with cashback for your monthly purchases allowing you to choose which purchases to use that credit on, while others will credit your account automatically.

If your cashback credit card offers 5% cashback on all spend, then spending S$200 will earn you a S$10 credit on your card. However, it is important to keep in mind that most cards have a cap on how much cashback you can earn per month, quarter or year, as well as a minimum required spend per month to qualify for cashback. That is why selecting the right credit card for your spending profile is so crucial.

A cashback credit card is worth it if you are able to pay off your monthly credit card balance. Otherwise the cashback you will earn on your purchases will be outweighed by the interest you will have to pay on your balance. Read our guide to find the best cashback credit card for you.

The biggest difference between cashback, points, and miles is the flexibility they provide to consumers. While similar, they each have distinct characteristics.

Cashback rewards are perhaps the most flexible. When you make purchases on a cashback card, a designated percent of that spend value is returned to your account, often to offset your monthly bill. For example, 5% cashback on a S$100 eligible purchase means S$5 are credited back to your account.

Points rewards are also fairly flexible, because they can usually be redeemed for merchandise vouchers, air miles, or even cash credits. Every card issuer’s rewards system is a little different, so it’s worth checking out the terms and conditions for details. A benefit of points systems is that they are often paired with coupons and discounts with popular merchants. A drawback, however, is that converting points to miles often incurs a S$25 administrative fee.

Miles rewards are the least flexible, but can be more valuable to frequent travellers than points or cashback. Often, miles earned by spend on the card are directly transferred to the cardholder’s frequent flyer airline account. This means cardholders don’t need to worry about conversion fees or the hassle of manual transfers. In terms of value, 1 mile often equals between S$0.01 to S$0.08 in value-to-consumer.

The value of credit card rewards depends on how much effort you are willing to put in to redeem them, and how likely you will be to apply them. For example, while frequent travellers may be interested in points or miles rewards cards, those who don’t want to deal with the hassle of conversions or who are less likely to travel may prefer cashback. In fact, cash rebates are usually automatically applied to the next monthly statement, with no action required by the cardholder. Cashback is low-maintenance and worry-free, so if you’re looking for rewards that are easy and straightforward, cashback may be the best option for you.

To determine which type of credit card is best for you, it’s important to understand how much value they’ll ultimately provide–how much money do you get back for the amount you spend? While comparing cashback to cashback or miles to miles is fairly easy, it can be difficult when you want to compare cashback rewards to miles rewards.

To figure out a credit card’s rewards rate, you first need to determine the worth of its miles or points. How many points (or miles) are needed to redeem a certain prize? Divide the dollar value of that prize by the number of points needed for redemption. This tells you the dollar value per point. Next, multiply this value by the number of points earned for every S$100 spent to determine the rewards rate. We have collected data to calculate value of miles, which generally range from 1 cent to 8 cents per mile. Value of points will differ depending on the issuing bank's policies.

Finally, each card offers differently structured reward programs. For example, some cards will rebate 10% on dining, but will only yield 0.2% on other expenses. By understanding how your own monthly expenses are generally distributed across different categories, you can better calculate how much money you can save by using a card.

This analysis can help you accurately evaluate which card will result in the highest benefits for your budget.

- Overall Best Credit Cards

- Best Rewards Credit Cards

- Best Credit Card Promotions

- Best Cashback Credit Cards

- Best Air Miles Credit Cards

- Best Agoda Credit Card Promotions

- Best Expedia Credit Card Promotions

- Best Booking.com Credit Card Promotions

- Best Credit Cards with Klook Promo Codes

- Best No Annual Fee Credit Cards

- Best Miles Cards with No Annual Fee

- Best Cashback Cards with No Annual Fee

- Best Petrol Credit Cards

- Best Cards for SPC Discounts

- Best Cards for Esso Promotions

- Best Cards for Shell Discounts

- Best Shopping Credit Cards

- Best Student Credit Cards

- Best Credit Cards for Seniors

- Best Expat Credit Cards

- Best Unlimited Cashback Credit Cards

- Best Cards for High Income

- Best Dining Credit Cards

- Best Cards for Food Delivery

- Best Credit Card 1 for 1 Buffet Promotions

- Best Grocery Credit Cards

- Best Entertainment Credit Cards

- Best Credit Cards for TransitLink SimplyGo

- Best EZ-Link Credit Cards

- Best Cards for Insurance

- Medical Credit Cards

- Wedding Credit Cards

- Best Debit Cards

- Best Cards for Seniors