Best Credit Card Promotions 2024

Credit card issuers are constantly updating their sign-up promotions. Our credit card experts have carefully reviewed the market to aggregate all promotions in 2022 for the top credit cards in Singapore. Our analysis covers bonuses as well as inherent card values, ensuring the option you select will reward spending far beyond the welcome offer.

- SC Unlimited Cashback: 1.5% unlimited rebate + transport perks

- SC Visa Infinite X: Bonus S$6,000 w/ S$200k fund placement

- SC SingPost Spree: 3% rebate online overseas & vPost transactions

- SC Rewards+: 2.9 miles per S$1 overseas, 1.45 for dining

- SC Visa Infinite: 3 miles per S$1 overseas, rewards for tax-pay

- Citi PremierMiles Visa: 45,000 Welcome Citi Miles with S$9,000 spend in 3 mo

- Citi Cash Back: Up to 8% rebate on groceries & petrol, 6% on dining

- Citi Cash Back+: Unlimited 1.6% cashback on all spend

- Citi Prestige: Unlimited lounge access, bonus hotel nights & more

- Citi Rewards: Up to 4 miles per S$1 for fashion & online spend

- Citi Clear: 0.4 miles per S$1 for students, foodie privileges

- OCBC Titanium: 4 miles per S$1 on fashion & select retail

- Amex True Cash Back: Unlimited 1.5% rebate + Amex benefits

- Amex SIA KrisFlyer: Directly earn KrisFlyer miles, S$150 SIA credit

- Amex SIA KrisFlyer Ascend: Elite perks inc. hotel & flight upgrades

- Amex Platinum: Elite dining & lifestyle perks in SG

- Maybank Horizon Visa: Market-leading 3.2 miles per S$1 select local spend

- Maybank Family & Friends: 8% cashback with S$800 min. spend requirement

- Maybank FC Barcelona: Highest unlimited local rebate–1.6% on all spend

- Maybank Platinum Visa: Up to 3.33% rebate on local and foreign currency spend

- Maybank World: Free green fees at 100 fairways across 19 countries

- Maybank World: Highest rebate for students–1% on all spend

- SC Unlimited Cashback: 1.5% unlimited rebate + transport perks

- SC Visa Infinite X: Bonus S$6,000 w/ S$200k fund placement

- SC SingPost Spree: 3% rebate online overseas & vPost transactions

- SC Rewards+: 2.9 miles per S$1 overseas, 1.45 for dining

- SC Visa Infinite: 3 miles per S$1 overseas, rewards for tax-pay

- Citi PremierMiles Visa: 45,000 Welcome Citi Miles with S$9,000 spend in 3 mo

- Citi Cash Back: Up to 8% rebate on groceries & petrol, 6% on dining

- Citi Cash Back+: Unlimited 1.6% cashback on all spend

- Citi Prestige: Unlimited lounge access, bonus hotel nights & more

- Citi SMRT: 5% everyday rebates w/S$500 min spend

- Citi Rewards: Up to 4 miles per S$1 for fashion & online spend

- Citi Lazada: Up to 4 miles per S$1 spend on Lazada

- OCBC 365: 6% rebate on dining, 3% rebate on groceries, utilities and travel, Visa Concierge Services

- OCBC Frank: Up to 6% rebate for FX, online and mobile purchases, low S$600 min. spend requirement

- OCBC Titanium: 4 miles per S$1 on fashion & select retail

- OCBC 90°N: Unlimited miles and cashback

- OCBC Voyage: Flexible miles redemption, boosted rewards for overseas spend

- OCBC Cashflo: Rewards for split payments, no processing fee

- Amex True Cash Back: Unlimited 1.5% rebate + Amex benefits

- Amex SIA KrisFlyer: Directly earn KrisFlyer miles, S$150 SIA credit

- Amex SIA KrisFlyer Ascend: Elite perks inc. hotel & flight upgrades

- Amex Platinum: Elite dining & lifestyle perks in SG

- Maybank Horizon Visa: Market-leading 3.2 miles per S$1 select local spend

- Maybank Family & Friends: 8% cashback with S$800 min. spend requirement

- Maybank FC Barcelona: Highest unlimited local rebate–1.6% on all spend

- Maybank Platinum Visa: Up to 3.33% rebate on local and foreign currency spend

- Maybank World: Free green fees at 100 fairways across 19 countries

- HSBC Advance: Up to 3.5% cashback capped at S$300/month

- HSBC Revolution: 4 miles per S$1 spent online and on contactless payments

- HSBC Visa Platinum: 5% rebate on groceries, dining & petrol, miles for general

- CIMB Platinum MC: 10% rebate on wine and dine, transport, petrol, health and travel, capped at S$100/month

- CIMB Visa Infinite: Unlimited 2% cashback on travel, overseas and online spend in foreign currencies

- CIMB World MC: Unlimited 2% cashback on wine and dine, food delivery, entertainment, taxi & automobile, luxury goods and 50% off green fees

- CIMB Visa Signature: 10% cashback on online shopping, groceries, beauty and wellness, pet shops and cruises

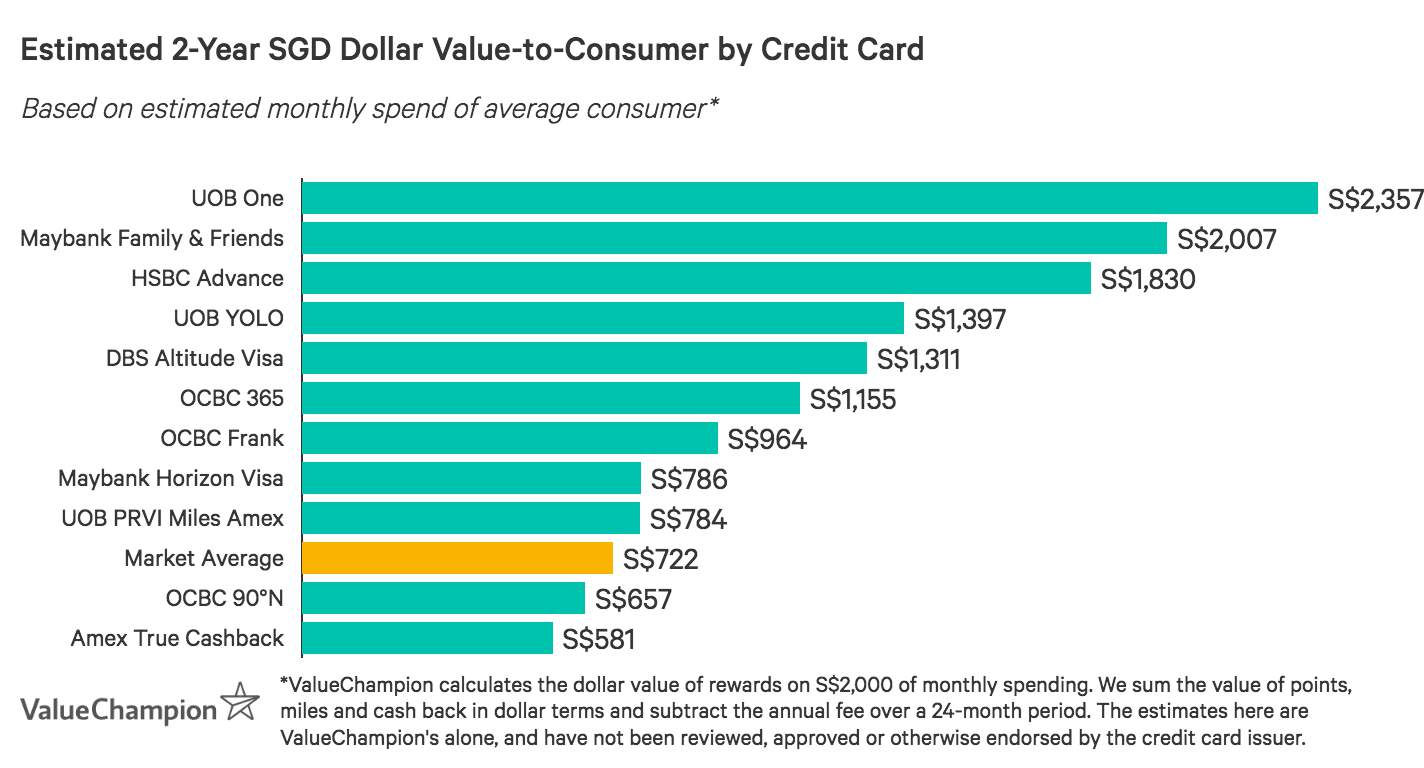

Compare the Best Credit Cards in Singapore by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best credit cards on the market in Singapore to estimate how much value they return to the consumers after 2 years, accounting for rebates, welcome bonus promotions, and annual fees. We've organised the best credit card promotions in 2022 by the provider to help you assess which card will be the best fit for your needs.

Best Standard Chartered Credit Card Promotions

Learn more about the best credit cards from Standard Chartered as well as their credit card promotions in 2022.

Standard Chartered Unlimited Cashback Card: Uncapped Rebates + Transport Perks

| |

If you spend S$7,000+/month, you’re likely going to feel restricted by cashback credit cards with earnings caps–this is why Standard Chartered Unlimited Cashback Card may very well be the best option for you. Cardholders earn 1.5% flat cashback with no rewards caps, which offers high spenders unlimited earning potential.

| |

|

|

If you spend S$7,000+/month, you’re likely going to feel restricted by cashback credit cards with earnings caps–this is why Standard Chartered Unlimited Cashback Card may very well be the best option for you. Cardholders earn 1.5% flat cashback with no rewards caps, which offers high spenders unlimited earning potential.

|

Standard Chartered SingPost Spree: Cashback on Online Overseas

|

|

If you have a low budget of about S$300 to S$500/month, it can be very difficult to meet the minimum spend requirements for most cashback credit cards, leaving you to earn a base rate of just 0.3% in most cases. With Standard Chartered SingPost Spree Card, however, you can completely avoid minimum spend requirements and earn a comparably high 3% cashback on foreign online and vPost transactions, 2% on local online and contactless transactions, and 1% on general spend.

| |

|

|

|---|

|

|

If you have a low budget of about S$300 to S$500/month, it can be very difficult to meet the minimum spend requirements for most cashback credit cards, leaving you to earn a base rate of just 0.3% in most cases. With Standard Chartered SingPost Spree Card, however, you can completely avoid minimum spend requirements and earn a comparably high 3% cashback on foreign online and vPost transactions, 2% on local online and contactless transactions, and 1% on general spend.

|

Standard Chartered Rewards+: Small Dining Budgets

| |

If you currently have a specialised credit card, such as a shopping card, chances are you might be earning just 0.3% on dining, which often isn’t rewarded at an elevated rate. With Standard Chartered Rewards+ Card, you can make more of your S$250 to S$350/month dining budget without worrying about minimum spend requirements.

| |

|

|

If you currently have a specialised credit card, such as a shopping card, chances are you might be earning just 0.3% on dining, which often isn’t rewarded at an elevated rate. With Standard Chartered Rewards+ Card, you can make more of your S$250 to S$350/month dining budget without worrying about minimum spend requirements.

|

Best Citibank Credit Card Promotions

Learn more about the best credit cards from Citibank as well as their credit card promotions in 2022.

Citi PremierMiles Visa: Affordable Miles + Lounge

| |

If you’re an average spender looking for travel perks without high annual fees, Citi PremierMiles Visa Card is one of your best options. Cardholders earn a respectable rewards rate of 1.2 miles per S$1 local spend and 2 miles overseas, and receive free travel insurance and 2 free lounge visits per year.

| |

|

|

If you’re an average spender looking for travel perks without high annual fees, Citi PremierMiles Visa Card is one of your best options. Cardholders earn a respectable rewards rate of 1.2 miles per S$1 local spend and 2 miles overseas, and receive free travel insurance and 2 free lounge visits per year.

|

Citi Cash Back Card: Top Rebates on Food & Petrol

| |

Citi Cash Back Card is the best credit card on the market for average spenders because it rewards key categories–food and transport–with remarkably high rewards rates. Cardholders earn 8% cashback on dining, groceries, and petrol after S$800 minimum spend, with earning potential capped at S$80/month. This is quite a respectable earning potential, allowing consumers to earn up to S$900/year. While there’s a S$192.6 fee, it’s waived the 1st year and can easily be offset by these extra savings.

| |

|

|

Citi Cash Back Card is the best credit card on the market for average spenders because it rewards key categories–food and transport–with remarkably high rewards rates. Cardholders earn 8% cashback on dining, groceries, and petrol after S$800 minimum spend, with earning potential capped at S$80/month. This is quite a respectable earning potential, allowing consumers to earn up to S$900/year. While there’s a S$192.6 fee, it’s waived the 1st year and can easily be offset by these extra savings.

|

Citi Cash Back+ Card: Highest Unlimited Cashback Rate

| |

Citi Cash Back+ Card is ideal for high spenders looking to avoid caps on their earnings. Cardholders earn 1.6% rebate on all spend, with no limits, which is higher than the 1.5% offered by comparable cards. This allows consumers with budgets of about S$7k+ to earn more than they could with any alternatives, including capped cards with higher rates. The S$192.6 fee is waived the 1st year, allowing consumers to begin earning immediately with Citi Cash Back+ Card, ultimately maximising rewards to their full potential.

| |

|

|

Citi Cash Back+ Card is ideal for high spenders looking to avoid caps on their earnings. Cardholders earn 1.6% rebate on all spend, with no limits, which is higher than the 1.5% offered by comparable cards. This allows consumers with budgets of about S$7k+ to earn more than they could with any alternatives, including capped cards with higher rates. The S$192.6 fee is waived the 1st year, allowing consumers to begin earning immediately with Citi Cash Back+ Card, ultimately maximising rewards to their full potential.

|

Citi Prestige MasterCard: Perks for Affluent Travellers

|

|

Affluent travellers who prioritise perks should definitely check out Citi Prestige MasterCard. Cardholders earn high rewards rates of 1.3 miles per S$1 local spend and 2 miles overseas. In addition, they receive more benefits than what’s offered by most other travel cards on the market, including unlimited lounge access, bonus hotel nights, golfing & dining privileges and much, much more. Even though there’s a S$535 fee, it's offset by 25,000 annual renewal miles (worth S$250) plus an annual bonus of up to 30% based on tenure of relationship with Citibank. Overall, Citi Prestige is the best match available for affluent consumers looking for luxury travel benefits.

| |

|

|

|---|

|

|

Affluent travellers who prioritise perks should definitely check out Citi Prestige MasterCard. Cardholders earn high rewards rates of 1.3 miles per S$1 local spend and 2 miles overseas. In addition, they receive more benefits than what’s offered by most other travel cards on the market, including unlimited lounge access, bonus hotel nights, golfing & dining privileges and much, much more. Even though there’s a S$535 fee, it's offset by 25,000 annual renewal miles (worth S$250) plus an annual bonus of up to 30% based on tenure of relationship with Citibank. Overall, Citi Prestige is the best match available for affluent consumers looking for luxury travel benefits.

|

Citi Rewards: Miles for Online & Fashion Spend

| |

Citi Rewards Card is one of the best miles-earning shopping cards on the market. Cardholders earn 10 points–equivalent to 4 miles–per S$1 spend online and on fashion retail. What makes Citi Rewards Card so great is its flexibility. Consumers earn miles for fashion spend online, offline, locally and overseas. In other words, you can earn just about anywhere you shop for clothing, bags, shoes, and other fashion items. Citi Rewards Card even rewards spend at department stores, which are sometimes excluded. In addition, nearly all online transactions earn rewards (travel bookings and mobile wallet pay are excluded, however). Other spend earns just 1 point (0.4 miles) per S$1, so this is best used as an online & shopping card, and while there’s a S$192.6 fee, it’s waived the first year. Ultimately, Citi Rewards Card is a great match for shoppers looking for flexible miles earning.

| |

|

|

Citi Rewards Card is one of the best miles-earning shopping cards on the market. Cardholders earn 10 points–equivalent to 4 miles–per S$1 spend online and on fashion retail. What makes Citi Rewards Card so great is its flexibility. Consumers earn miles for fashion spend online, offline, locally and overseas. In other words, you can earn just about anywhere you shop for clothing, bags, shoes, and other fashion items. Citi Rewards Card even rewards spend at department stores, which are sometimes excluded. In addition, nearly all online transactions earn rewards (travel bookings and mobile wallet pay are excluded, however). Other spend earns just 1 point (0.4 miles) per S$1, so this is best used as an online & shopping card, and while there’s a S$192.6 fee, it’s waived the first year. Ultimately, Citi Rewards Card is a great match for shoppers looking for flexible miles earning.

|

Citi Clear Card: Best Miles Card for Students

|

|

Citi Clear Card is one of the only options on the market that allows students to earn points/miles instead of cashback. Cardholders earn 1 point (0.4 miles) per S$1 spend, which is roughly equal to a 0.4% rebate. This is a higher rate than offered by several competitor cards. In addition, cardholders have access to dining programmes like Citi Gourmet Pleasures, which offers discounts on everything from online food delivery to sit-down meals at high-end restaurants. There are no minimum spend requirements and the S$29.96 fee is waived 1 year. For students who prefer miles to cashback, Citi Clear Card is worth considering.

| |

|

|

|---|

|

|

Citi Clear Card is one of the only options on the market that allows students to earn points/miles instead of cashback. Cardholders earn 1 point (0.4 miles) per S$1 spend, which is roughly equal to a 0.4% rebate. This is a higher rate than offered by several competitor cards. In addition, cardholders have access to dining programmes like Citi Gourmet Pleasures, which offers discounts on everything from online food delivery to sit-down meals at high-end restaurants. There are no minimum spend requirements and the S$29.96 fee is waived 1 year. For students who prefer miles to cashback, Citi Clear Card is worth considering.

|

Best OCBC Credit Card Promotions

Learn more about the best credit cards from OCBC Bank as well as their credit card promotions in 2022.

OCBC Titanium Card: Miles for Fashion & Retail

| |

If you’re a frequent retail shopper, OCBC Titanium Rewards Card offers one of the best ways to maximise rewards for your spend without paying a fee. Cardholders earn 10 points (4 miles) per S$1 spend on fashion retail, department stores, and electronics online, offline, locally and overseas. This same rate is offered by competitors, but OCBC Titanium Card also offers 4 miles per S$1 spend with select merchants like Amazon, Alibaba, Lazada, Qoo10 & many more–essentially, cardholders can earn on just about every kind of retail purchase, from appliances to beauty products and beyond. This makes it quite easy to max out the 4,000 miles/month rewards cap.

| |

|

|

If you’re a frequent retail shopper, OCBC Titanium Rewards Card offers one of the best ways to maximise rewards for your spend without paying a fee. Cardholders earn 10 points (4 miles) per S$1 spend on fashion retail, department stores, and electronics online, offline, locally and overseas. This same rate is offered by competitors, but OCBC Titanium Card also offers 4 miles per S$1 spend with select merchants like Amazon, Alibaba, Lazada, Qoo10 & many more–essentially, cardholders can earn on just about every kind of retail purchase, from appliances to beauty products and beyond. This makes it quite easy to max out the 4,000 miles/month rewards cap.

|

Best American Express Credit Card Promotions

Learn more about the best credit cards from American Express Singapore as well as their credit card promotions in 2022.

American Express True Cashback Card: Unltd Earnings + Amex Benefits

|

|

American Express True Cashback Card is the best cashback option for high-spending Amex loyalists because it offers unlimited 1.5% cashback with no minimum spend requirements–basically, offering affluent consumers uncapped earning potential.

| |

|

|

|---|

|

|

American Express True Cashback Card is the best cashback option for high-spending Amex loyalists because it offers unlimited 1.5% cashback with no minimum spend requirements–basically, offering affluent consumers uncapped earning potential.

|

American Express Singapore Airlines Krisflyer Card: Miles for Beginners

|

|

American Express Singapore Airlines KrisFlyer Card is a straightforward option for people looking for a "starter" miles card. In terms of rates, general spend earns 1.1 miles per S$1 (2 miles overseas in June & December) and spend with SingaporeAir, SilkAir and KrisShop earns 2 miles. Spend on Grab rides earn 3.1 miles per S$1, up to 620 miles/month. Rewards are earned directly in KrisFlyer miles, so there's no need to worry about transfers, conversions or any associated fees. Most travel cards actually earn in points–so Amex SIA KF Card is a bit more straightforward. Finally, Amex SIA KF is reasonably affordable with a S$176.55 fee that's waived 1 year. As a result, it's a worth considering for those who are looking for an easy-to-manage miles-earning credit card.

| |

|

|

|---|

|

|

American Express Singapore Airlines KrisFlyer Card is a straightforward option for people looking for a "starter" miles card. In terms of rates, general spend earns 1.1 miles per S$1 (2 miles overseas in June & December) and spend with SingaporeAir, SilkAir and KrisShop earns 2 miles. Spend on Grab rides earn 3.1 miles per S$1, up to 620 miles/month. Rewards are earned directly in KrisFlyer miles, so there's no need to worry about transfers, conversions or any associated fees. Most travel cards actually earn in points–so Amex SIA KF Card is a bit more straightforward. Finally, Amex SIA KF is reasonably affordable with a S$176.55 fee that's waived 1 year. As a result, it's a worth considering for those who are looking for an easy-to-manage miles-earning credit card.

|

American Express Singapore Airlines Krisflyer Ascend Card: Exclusive Travel Memberships

|

|

American Express Singapore Airlines KrisFlyer Ascend Card offers an extraordinary balance between competitive rates and luxury perks, all at a lower cost than offered by most high-end travel cards. Consumers earn 1.2 miles/S$1 on general spend, 2 miles on SIA brands and overseas in June & December, and 3.2 miles with Grab (up to 640 mi/mo). Another perk is that while Amex SIA KF Ascend's annual fee is a moderate S$337.05, it provides benefits that are typically associated with the most expensive miles cards. Consumers enjoy 4 free lounge visits/year, 1 free hotel night annually, free travel insurance, and potential upgrades to Hilton Honors Silver, KrisFlyer Elite Gold, and Hertz Gold Plus Rewards membership statuses. Overall, Amex SIA KF Ascend Card is a great match for people who often fly SIA, especially those who prioritise travel perks and specialty memberships.

| |

|

|

|---|

|

|

American Express Singapore Airlines KrisFlyer Ascend Card offers an extraordinary balance between competitive rates and luxury perks, all at a lower cost than offered by most high-end travel cards. Consumers earn 1.2 miles/S$1 on general spend, 2 miles on SIA brands and overseas in June & December, and 3.2 miles with Grab (up to 640 mi/mo). Another perk is that while Amex SIA KF Ascend's annual fee is a moderate S$337.05, it provides benefits that are typically associated with the most expensive miles cards. Consumers enjoy 4 free lounge visits/year, 1 free hotel night annually, free travel insurance, and potential upgrades to Hilton Honors Silver, KrisFlyer Elite Gold, and Hertz Gold Plus Rewards membership statuses. Overall, Amex SIA KF Ascend Card is a great match for people who often fly SIA, especially those who prioritise travel perks and specialty memberships.

|

American Express Platinum Card: Local Luxury for Singapore's Elite

|

|

If you're an affluent Singaporean that rarely travels, you can enjoy luxury locally with American Express Platinum Card. Cardholders have access to a myriad of privileges within the city state–Platinum Wellness discounts of up to 40% off elite spas, waived green fees at regional fairways and up to 50% off high-end dining & free drinks at trendy bars through the Love Dining & Chillax programmes. Amex Platinum is even the official card partner of the Michelin Guide Singapore, giving cardholders access to exclusive guest chef dinners.

| |

|

|

|---|

|

|

If you're an affluent Singaporean that rarely travels, you can enjoy luxury locally with American Express Platinum Card. Cardholders have access to a myriad of privileges within the city state–Platinum Wellness discounts of up to 40% off elite spas, waived green fees at regional fairways and up to 50% off high-end dining & free drinks at trendy bars through the Love Dining & Chillax programmes. Amex Platinum is even the official card partner of the Michelin Guide Singapore, giving cardholders access to exclusive guest chef dinners.

|

Best Maybank Credit Card Promotions

Learn more about the best credit cards from Maybank as well as their credit card promotions in 2022.

Maybank Horizon Visa Signature: Best for Local Miles

| |

Maybank Horizon Visa Signature Card is the best travel credit card for people with mostly local budgets, but who want to earn miles when they plan and go on vacations. Cardholders earn more for local spend than any other miles card on the market–3.2 miles per S$1 spend on dining, petrol, taxis and Grab, and hotel bookings with Agoda. However, consumers also earn at respectable rates on travel spend and overseas, at 2 miles per $1 spend on air tickets, travel packages and foreign currency transactions. While not a traditional travel card, Maybank Horizon Card even offers a few perks, like free travel insurance and airport lounge access.

| |

|

|

Maybank Horizon Visa Signature Card is the best travel credit card for people with mostly local budgets, but who want to earn miles when they plan and go on vacations. Cardholders earn more for local spend than any other miles card on the market–3.2 miles per S$1 spend on dining, petrol, taxis and Grab, and hotel bookings with Agoda. However, consumers also earn at respectable rates on travel spend and overseas, at 2 miles per $1 spend on air tickets, travel packages and foreign currency transactions. While not a traditional travel card, Maybank Horizon Card even offers a few perks, like free travel insurance and airport lounge access.

|

Maybank Family & Friends MasterCard: Top Rebates in SG & MY

| |

The absolute best credit card for people who spend time in both Malaysia and Singapore is Maybank Family & Friends Card. Spending S$500/month earns 5% rebate on fast food & food delivery, groceries, transport, petrol, data communications/online TV streaming & more; S$800/month spend earns 8% rebate. Most other cards offer a maximum of 3.33% cashback at this spend level.

| |

|

|

The absolute best credit card for people who spend time in both Malaysia and Singapore is Maybank Family & Friends Card. Spending S$500/month earns 5% rebate on fast food & food delivery, groceries, transport, petrol, data communications/online TV streaming & more; S$800/month spend earns 8% rebate. Most other cards offer a maximum of 3.33% cashback at this spend level.

|

Maybank FC Barcelona Visa Signature: Unlimited Local Cashback

| |

If you’re an especially affluent local spender, Maybank FC Barcelona Visa Signature Card is the best unlimited cashback option for you. This card offers 1.6% flat cashback on local spend, which is higher than competitors, who offer just 1.5%. This may seem like a small difference, but it quickly adds up with higher spend–another reason why high spenders are most likely to benefit from this card, beyond its uncapped earning potential.

| |

|

|

If you’re an especially affluent local spender, Maybank FC Barcelona Visa Signature Card is the best unlimited cashback option for you. This card offers 1.6% flat cashback on local spend, which is higher than competitors, who offer just 1.5%. This may seem like a small difference, but it quickly adds up with higher spend–another reason why high spenders are most likely to benefit from this card, beyond its uncapped earning potential.

|

Maybank Platinum Visa: Easy Rebates for Smaller Budgets

| |

Lower spenders often have trouble earning cashback because of the high minimum requirements associated with most cards. Maybank Platinum Visa Card, however, is the best credit card for people with smaller budgets because it offers respectable rebates after just S$300 minimum monthly spend. At this spend level, cardholders earn S$30/quarter, which adds up to S$120 in annual earnings with just S$1,200 annual spend. With alternative cards, consumers would likely earn 0.3% base rebate, totalling to S$3.6/year. Higher spend can earn higher rebates (S$1,000/month earns $100/quarter), but this rate is less competitive than alternatives on the market.

| |

|

|

Lower spenders often have trouble earning cashback because of the high minimum requirements associated with most cards. Maybank Platinum Visa Card, however, is the best credit card for people with smaller budgets because it offers respectable rebates after just S$300 minimum monthly spend. At this spend level, cardholders earn S$30/quarter, which adds up to S$120 in annual earnings with just S$1,200 annual spend. With alternative cards, consumers would likely earn 0.3% base rebate, totalling to S$3.6/year. Higher spend can earn higher rebates (S$1,000/month earns $100/quarter), but this rate is less competitive than alternatives on the market.

|

Maybank World MasterCard: Miles + Golfing Privileges

| |

If you’re an affluent golfer–and especially if you often spend on luxury retail–Maybank World MasterCard is the best card on the market for you. Cardholders receive the most comprehensive set of golfing privileges available with 2 complimentary green fees per month at an incredible 120 fairways across 25 countries.

| |

|

|

If you’re an affluent golfer–and especially if you often spend on luxury retail–Maybank World MasterCard is the best card on the market for you. Cardholders receive the most comprehensive set of golfing privileges available with 2 complimentary green fees per month at an incredible 120 fairways across 25 countries.

|

Maybank eVibes: Best Rebate Card for Students

| |

Maybank eVibes Cardis the best rebate card on the market for students, offering a market-leading 1% cashback on all spend. In fact, this rate is 4x higher than most competitor cards’ and there are no merchant restrictions, unlike the closest alternative. Cardholders do not need to worry about minimum spend requirements and the S$5.0 quarterly service fee is waived simply with card use. This makes Maybank eVibes Card extremely easy to use and maintenance-free–perfect for students just starting out with their first credit card.

| |

|

|

Maybank eVibes Cardis the best rebate card on the market for students, offering a market-leading 1% cashback on all spend. In fact, this rate is 4x higher than most competitor cards’ and there are no merchant restrictions, unlike the closest alternative. Cardholders do not need to worry about minimum spend requirements and the S$5.0 quarterly service fee is waived simply with card use. This makes Maybank eVibes Card extremely easy to use and maintenance-free–perfect for students just starting out with their first credit card.

|

Learn More About How to Find the Best Credit Card for You

- How to Apply for a Credit Card

- How to Use a Credit Card

- How to Find the Best Rewards Credit Card

- Should You Wait for the Next Big Promotion to Apply for a Credit Card?

- Visa v. MasterCard Credit Cards–Which are Better?

- Everything You Need to Know About Credit Card Cash Advances

- Understanding Credit Card APRs & Interest Rates

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.