3 Ways to Save on Living Costs for Disabilities

If you or your loved one has a disability, whether temporary, partial, or permanent, the cost of living is higher than if you don't have a disability. In fact, a serious disability that requires help with Activities of Daily Living (ADL) can result in a cost of S$15,458-S$17,212 during the first year after an accident. Even hiring an independent caregiver, whose cost ranges from S$15-S$125 per hour, can be financially draining. In all cases, finding ways to save on these costs can help ease your mind by reducing financial stress.

1. Make Sure You Know Which Benefits You're Entitled To

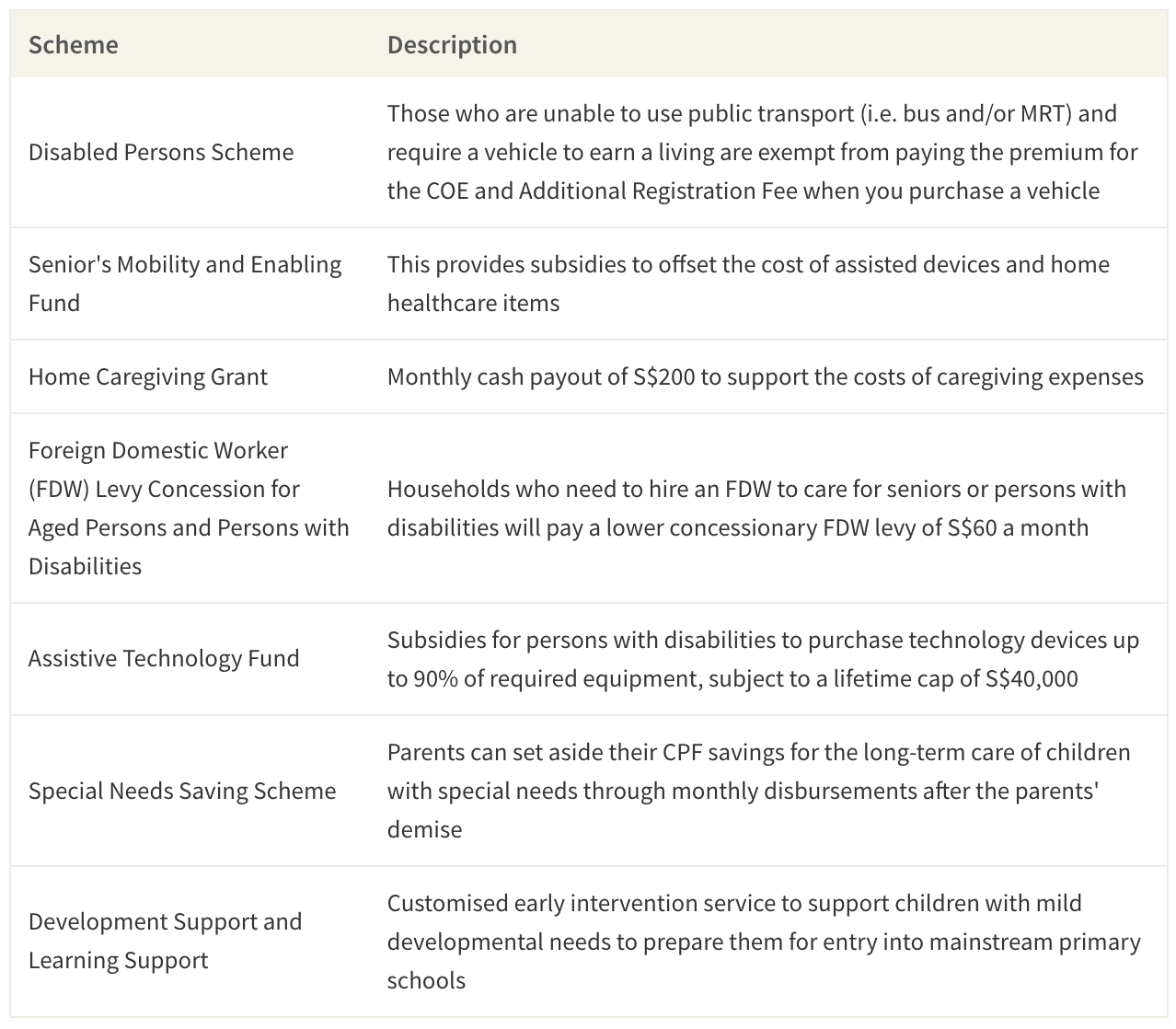

If you're a Singaporean citizen or permanent resident with a disability, you could be entitled to cash vouchers, grants, and special programs. One example scheme is the Disabled Persons Scheme, which exempts you from paying for the Certificate of Entitlement (COE) and Additional Registration Fee (ARF) when you buy a car. This can save you around S$41,996 for the COE and thousands more for the ARF.

Disability Benefits From the Singaporean Government

Another program is the Home Caregiving Grant, which can help you pay for a caregiver by giving you up to S$200 in monthly cash payments. There are several other schemes available that could help you support you or someone you love who has a disability during this time.

2. Get Additional Insurance To Cover Long-Term Costs

If you're a Singaporean citizen, you must pay into the CareShield Life insurance scheme when you reach 30 years old. The primary benefit of this scheme is that, upon a successful claim, you will receive S$600 (or more) in monthly payouts for as long as you remain severely disabled. While the government is trying to promote this scheme by giving cash incentives of up to S$4,000 to those born before 1979, getting additional coverage can help with long-term costs by providing additional monthly support.

There are also two types of insurance plans that could provide additional help to offset the cost of future charges. The first is a supplemental insurance plan to CareShield Life, which can increase your monthly payouts to up to S$5,000 per month, give you a lump sum payments of 3 times your first monthly benefit, and give you death benefits of up to 300% of your disability benefit in the event of an accident or progressive illness. The second type is a private health insurance plan that will fully cover hospitalisation and certain treatments, as well as equipment for mobility. While you may be hesitant to purchase additional insurance, there are health plans that can fit a myriad of budgets and the monthly payouts could prove vital in the long-run.

3. Implement Smart Shopping Strategies

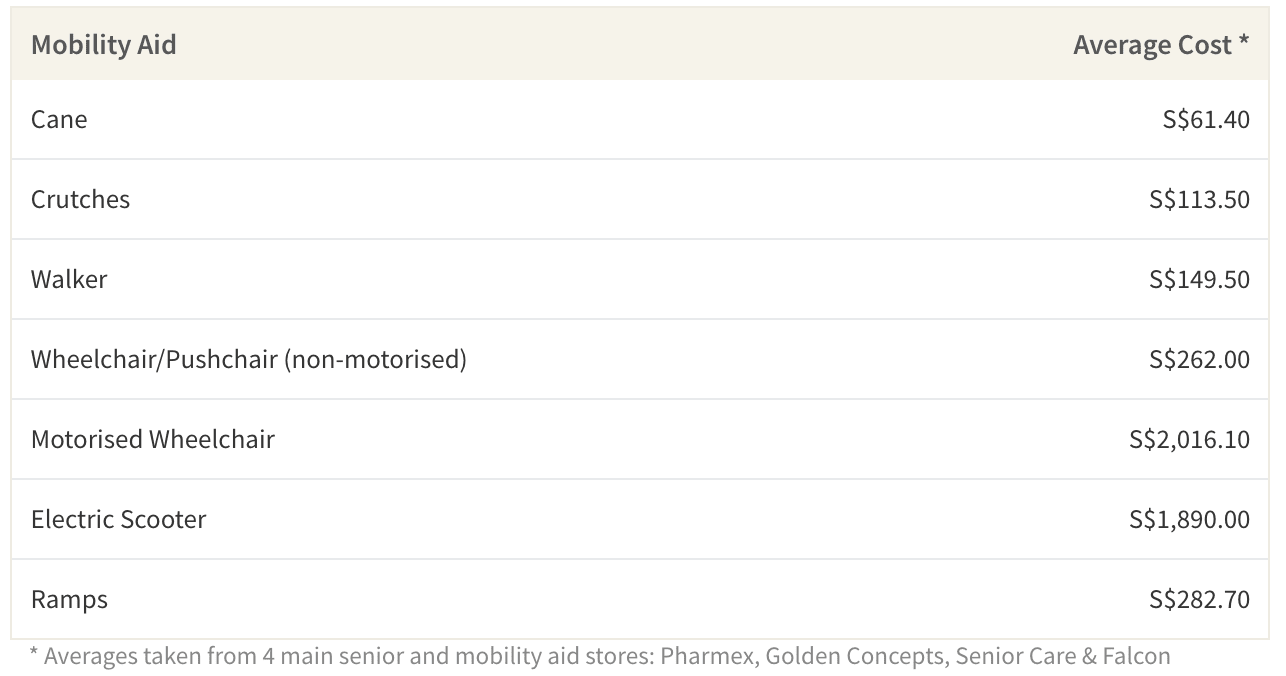

A good rule of thumb to save on living costs for disability equipment is to always check online for promotions and to compare prices before you buy something. For example, the same 3-in-1 shower chair (sold by two different vendors on iPrice) costs S$153.70 and S$199.00. In this scenario, comparing the prices would lead to S$45.30 in savings should you buy the more affordable option.

Average Cost of Mobility Aids in Singapore

Where possible, moreover, use a cashback credit card with a high rebate on general purchases. This could save you hundreds, if not thousands, each year on disability aids. For instance, UOB's One credit card offers a 5% rebate on general spending with a limit of S$300 each quarter. That means each year you could save up to S$1,200. By implementing smart shopper strategies, you could make small savings that will add up overtime.

When You Save on Costs, You Can Focus on Care

If you or a loved one has a disability, you may be wondering how you will afford both the short-term, like mobility aids, and long-term, like hospitalisation, costs. By knowing what benefits you're entitled to, finding a good insurance plan that can cover additional costs and lost wages, and putting into practice clever shopping strategies, you can save hundreds, if not thousands, each year on the living costs for disabilities. Additionally, when your financial stress dissipates you can find yourself with more time to focus on rehabilitation and care.

Anya is a Research Analyst for ValueChampion who focuses on loans and investments in Singapore. Previously, she assisted global consultancies, hedge funds and private equities with primary research at a high-growth fin-tech based in London. A graduate of the University of Oxford and King's College London, Anya is currently interested in applying quantitative research to help consumers make better financial decisions.