Thinking of Buying Your First Home? Don't Forget About These 5 Expenses When Creating Your Budget

When you're putting together a budget to estimate location, size and type of home you plan to purchase, it's tempting to structure your search based on list prices. While this represents the most significant cost of becoming a homeowner, it is just one of many that you'll have to consider when purchasing your first home. Therefore, some prospective home buyers may need to adjust their expectations and budget in order to account for these various expenses.

Home Loan Payments

First-time homebuyers are only required to put as little as 5% cash down for their purchase, assuming they have a 25-year bank loan. However, this figure belies the total cost homeownership due to interest costs. Homeowners will have to consider the ongoing costs associated with housing loans in the form of required monthly payments.

There are a few ways to keep your monthly payments affordable. First, by choosing a less expensive home, you will be saddled with less debt and therefore face smaller monthly debt obligations. If you are not willing to purchase a less expensive home, you can still save a lot of money by finding the cheapest home loan rates. Additionally, by choosing a longer loan tenure you can spread the cost of your loan out and pay smaller monthly payments, though you will likely end up paying more in total interest given the longer tenure. Finally, it is common to refinance one's home loan every few years in order to capitalise on low introductory rates offered by banks seeking to attract new customers.

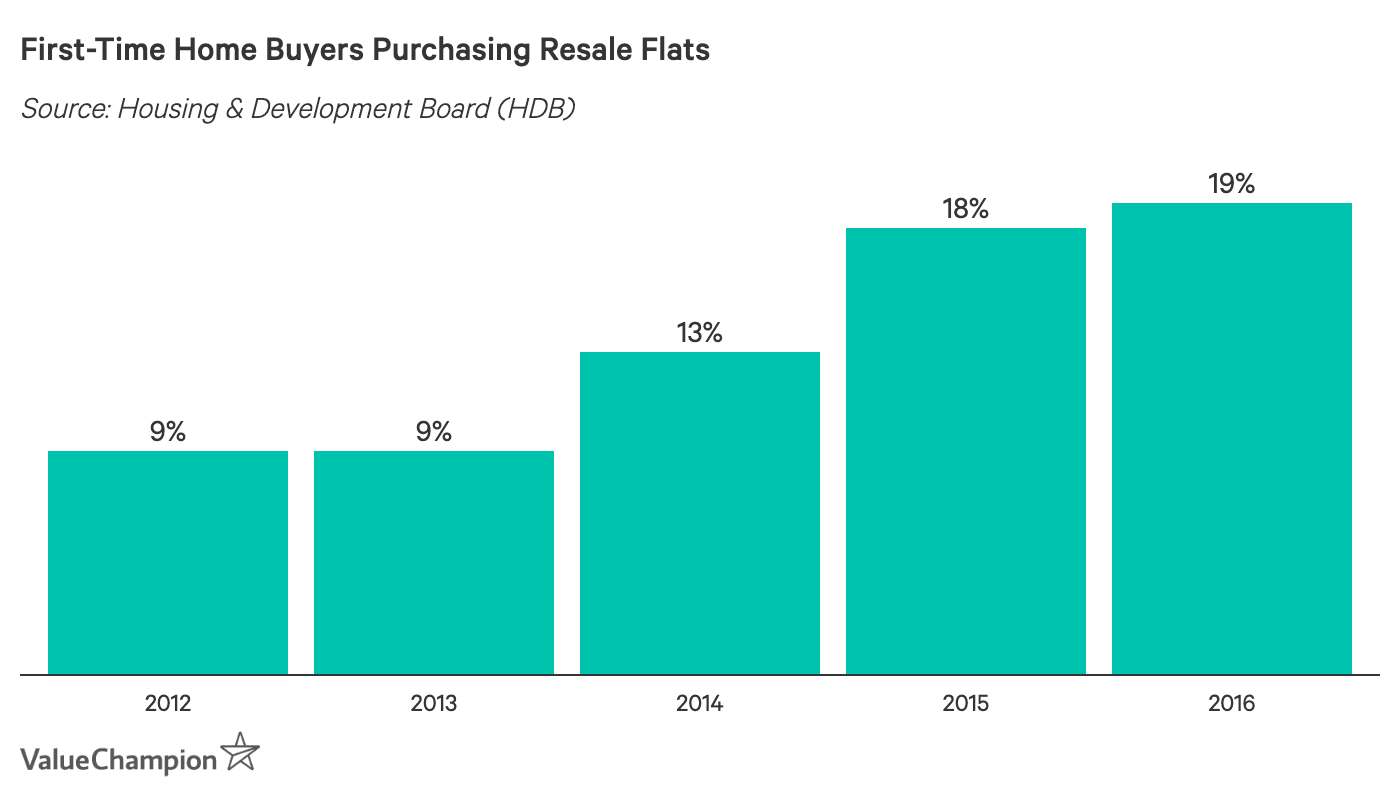

Renovation & Maintenance Costs

In recent years, first-time home buyers have increasingly elected to purchase HDB resale flats, rather than BTO units. These individuals may find it preferable or necessary to make renovations to their new flat, given that it is not a brand new unit. For this reason, it is crucial for many individuals to consider the cost of renovations when purchasing their first home.

We estimate that the average cost of renovating a 4-room HDB flat costs about S$55,000. However, this figure can vary dramatically depending on the number of rooms being renovated, style of renovation, and materials used. For example, a simple upgrade of one or two rooms will cost significantly less than a more extensive remodel with high-end finishes.

While there are financing options available to those hoping to renovate their new flat, it is important to consider the financial burden of making multiple loan payments each month if you are also on the hook for a home loan. Additionally, before making significant renovations to a HDB flat, it is important to make sure that they are permitted by the Housing & Development Board.

Even if you do not plan to make renovations to your new home, you will have to have room in your budget for on-going maintenance costs. HDB estates tend to charge from about S$20 to about S$100 per month depending on your citizenship and flat size. On the other hand, condo maintenance fees typically cost about S$300 monthly, but can cost as much as S$1,000 per month.

Home & Fire Insurance

Insuring your home is not the most expensive aspect of homeownership; however, it can be a crucial one. There are two types of common insurance for one's home: fire and home insurance. Fire insurance is required by most lenders for HDB flats, though it is quite inexpensive for most individuals due to the HDB Fire Insurance Scheme.

Home insurance, also known as home contents insurance, provides a more comprehensive coverage. For instance, home insurance typically protects homeowners from damage costs caused by fires, leaks, burglary and natural disasters. It also provides insurance coverage for expenses related to injuries that occur in your home. Home insurance policies vary in cost due to the type of home and desired coverage amounts. For example, the average cost of home insurance for a 4-room HDB flat costs about S$150 per month. On the other end of the spectrum, insurance for landed homes typically costs about S$270 on average. To determine how you should pay for your desired coverage, it can be helpful to consult free, online guides, such as ValueChampion's.

Property Tax

Another perpetual cost of owning a home is the expense of property tax. Property taxes are levied based on your property's annual value (AV), which is an estimate of the total annual rental value of the property. In Singapore, property taxes are charged on a progressive scale, from 0-16%. For example, an owner occupied home with an annual value of S$60,000 would be subjected to 0% for it's first S$8,000, 4% of its next S$47,000 of value (S$1,880) and 6% on the remaining S$5,000 (S$300) for a total tax bill of S$2,180.

The IRAS has a handy property tax calculator to help you estimate your annual tax burden. It is also possible to check the Annual Value of any property using the IRAS website for just S$2.50 per property.

Other Purchasing Fees

In order to purchase a home in Singapore, there are a number of fees that you must pay. For example, those purchasing an HDB flat must pay an option fee of S$500 to S$2,000 for a BTO unit or S$5,000 for a resale flat. Those purchasing executive condominium (EC) or private properties must pay a 5% option fee. Other expenses include a buyer's stamp duty (1-4% of property value) as well as fees for a professional appraiser and a legal fee for working on a mortgage with a lawyer. In total, these fees can amount to several thousand dollars, which can eat into your overall housing budget. It is also worth mentioning that first-time homebuyers considering resale flats should also look into housing grants, as they could receive up to S$120,000 depending on their income and desired flat type.

Proper Planning for Financial Freedom

Finding your first home is an exciting process. As you begin to develop your price range for homes you can afford, make sure to account for the range of costs associated with purchasing and owning a home, rather than just the purchase price. This will help you enjoy your new home without unexpected financial pressures.