3 Maid Insurance Conditions You Must Know to Save on Your FDW's Medical Costs

Your domestic worker plays an important role in supporting your household. That's why when she falls ill, it can be a scramble to get her prompt medical attention, pay for her treatment and find a temporary replacement while she recovers.

Luckily, this is when your FDW insurance comes in and helps you deal with costly medical bills. However, there are limitations and coverage gaps in maid insurance that can result in surprise out-of-pocket costs for unsuspecting employers. To help FDW employers manage their domestic worker's healthcare costs, we discuss 3 conditions surrounding your domestic worker's healthcare coverage and provide a few ways to reduce unexpected healthcare spending.

1. Hospitalisation Coverage is Limited to Ward & Hospital Type

If your domestic worker needs to be hospitalised, the ward she gets admitted to will play an important role in determining your out-of-pocket costs. Maid insurance policies fully cover hospitalisation expenses if your FDW stays in B2 or C wards at public hospitals.

However, you will be responsible for the remainder of the bill if your domestic worker stays in a B1 ward or higher. If that happens, your out-of-pocket responsibility can range from 30% to 50% of the bill. Also, families who use private hospitals and want their domestic worker to use the same medical team should be careful when choosing their maid insurance plans. While some insurers will partially cover hospitalisation at private hospitals, many insurers exclude them from coverage.

| Medical Benefits | Industry Average Limits |

|---|---|

| Outpatient Expenses | S$2,446 |

| Hospitalisation | S$18,420 |

| Personal Accident | S$2,808 |

| Recuperation (Total) | S$682 |

2. Overseas Hospitalisation Is Only Covered If FDW Travels With Employers

We know that maid insurance offers medical coverage while your worker is in Singapore, but what happens if she travels with you or she goes home on personal leave? In these cases, coverage will depend on your insurer. Typically, insurers provide partial coverage if she is travelling with you.

When your FDW goes home on personal leave, however, her medical coverage becomes quite limited. While a few insurers like NTUC provide some coverage for accidents, others don't provide any coverage during your FDW's personal leave.

Regardless of your insurer's coverage, it can be tricky to figure out your out-of-pocket responsibility for your FDW's medical care when she travels alone. Because of this, you should consult the Ministry of Manpower (MOM) regarding when you need to provide medical coverage.

3. Dental & Pre-Existing Illnesses Not Among Covered Conditions

Unfortunately, your FDW's medical insurance won't cover every type of condition. For instance, pre-existing conditions are not covered unless your domestic worker was already insured in Singapore when the condition arose. Because pre-existing conditions can be expensive to treat, you should enquire about your domestic worker's medical history before making the hire.

Common Medical Exclusions

- Nursing care

- Dental treatment for tooth, gum or oral disease

- Routine physical examinations

- Pre-existing conditions (unless previously covered)

- Non-emergency treatment outside of hospitalisation

- Alcohol or drug addiction

- Elective plastic or cosmetic surgery

- Braces, prosthetic devices and medical-related equipment

- Contraception

- Travel to receive overseas medical treatment

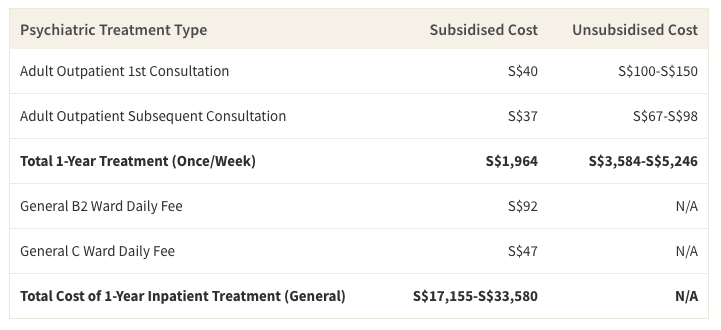

- Psychiatric illnesses

Other common exclusions include routine dental care, outpatient care, immunizations, STD treatment and psychiatric care. While some exclusions, like pregnancy, will result in a cancelled work permit and no financial responsibilities on your end, others may require prompt medical care. For instance, anxiety and depression can occur among domestic workers, but their treatment isn't covered by insurance. Since you will be responsible for 100% of the medical bill in these cases, it could be helpful to create an emergency healthcare fund to avoid potentially going into debt over your FDW's healthcare expenses.

Read Also: MSIG MaidPlus Insurance: What Makes It Unique

How to Save on Your FDW's Healthcare Expenses

Regardless of the severity of your FDW's illness, it is your responsibility as an employer to pay for her medical care. But since medical care is expensive even with insurance coverage, paying for an extra person's healthcare can become burdensome for families. Luckily, there are a few ways to reduce your domestic worker's health care bills.

First, employers can look for outpatient clinics that offer discounts for FDWs. Alternatively, if you don't have time to compare different medical providers, you can consider signing up for HealthPal, which offers subsidised medical care at dozens of clinics for your FDW for as low as S$24 per year. This includes S$13 GP consultations, S$80 specialist consultations and S$70 dental polishing and scaling, saving employers 48% on their FDW's medical bills.

Employers facing financial hardship can consider making appointments for their FDWs at the Humanitarian Organisation for Migration Economics (HOME), which offers free dental care. However, because the waitlist is typically a couple of months, HOME appointments are recommended for procedures that don't require urgent care (for instance, non-emergency fillings).

Another way to save money on your worker's domestic expenses is to prioritise prevention. Prevention services like immunisations are typically cheaper than paying for treatment. You should also make sure your FDW is eating healthy meals and engaging in physical activity to reduce the risk of heart disease and diabetes—two fairly common critical illnesses in Singapore that are both costly and require long-term treatment.

Read Also:

Fiona is a full-stack marketer working in the digital sphere for more than six years.

A self-proclaimed foodie and bargain hunter, she wants to bring the best deals and value to the community around the world. When not working on her pet projects, Fiona can be found sipping a coffee while reading a paperbacks or watching mystery thrillers on Netflix and Disney+.