How Do Singapore's Housing Market Cooling Measures Affect First-Time Home Buyers?

Individuals preparing to purchase their first home typically pay close attention to interest rate changes and other news that will affect what is likely to be the biggest purchase in their lives. For this reason, these consumers should be aware of recent housing market cooling measures introduced by the government earlier this month. We dove into the details in order to make sense of these new rules and explain the implications for prospective homeowners.

What Type of Adjustments Were Introduced and Why?

Singapore's government implemented cooling measures to the housing market in the form of higher Additional Buyer's Stamp Duty (ABSD) rates and tightened loan-to-value (LTV) rules for borrowers getting home loans from financial institutions (i.e. not the Housing Development Board). These policies were implemented following a significant rise in private housing prices (9.1% in the past year) and a significant increase of en bloc sales transactions (S$8.8 billion in the first 6 months of 2018). The measures are intended to keep residential property prices "in line with economic fundamentals", which really means to rein in the growth of private property prices.

What Changes Will First-Time Homeowners Face?

Luckily for most first-time home buyers, the ABSD increases are not applicable to them. For example, most ABSD increases are levied to individuals purchasing multiple residences. The ABSD for Singapore Permanent Residents purchasing their first home remains at 5% of the property's purchase price or market value, whichever higher. Additionally, there is still no ABSD levied for Singapore Citizens purchasing their first residential property. On the other hand, since foreigners tend to represent a big portion of private property buyers, they will now be required to pay a 20% ABSD (up from 15%), whether or not it is their first home purchase.

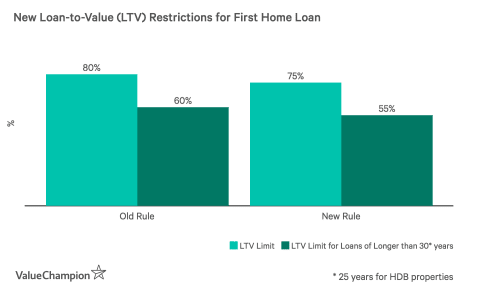

While most first-time home buyers will not be affected by changes to ABSD, they will still be impacted by LTV tightening. The new LTV requirement for first-time home buyers has been lowered to 75% from 80%, which means these home buyers must now make a down payment of 25% of their new home's purchase price, instead of 20%. The LTV limit for loans of more than 25 (HDB) or 30 years (private) was lowered from 60% to 55%.

Implications for First-Time Home Buyers: Significantly Larger Down Payments

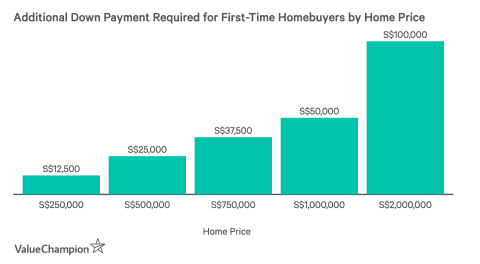

While these may appear to be small changes, they actually require home buyers to make significantly larger down payments. In fact, under these new rules, first-time home buyers will have to make down payments that are 25% bigger than under the previous rule (12.5% larger for 25/30 year loans). This measure effectively reduces the affordability of homes, and therefore the demand for residential properties, which has major implications for prospective home buyers that are currently saving up to purchase their first home. For example, prospective homeowners may have to save for a longer period or even consider purchasing home in a cheaper neighborhood.

Still, the good news for these home buyers is that the resulting decline in demand could potentially result in lower prices for both HDB and private flats, making them more affordable over time. Another silver lining to the LTV tightening for home buyers is that borrowers will pay less in interest over the duration of their home loan by being required to pay more upfront. However, the new rule definitely could have negative impact for current owners of resale HDB flats and private properties.

Parting Thoughts: Short-Term Pain, Long-Term Benefits

The cooling measures introduced on the residential housing market appear to be primarily directed at real estate investors who purchase multiple properties, not first-time home buyers. However, first-time home buyers will still be impacted by facing stiffer LTV requirements. In the short-term, this may delay some prospective homeowners from purchasing their dream home because they will be required to make larger down payments.

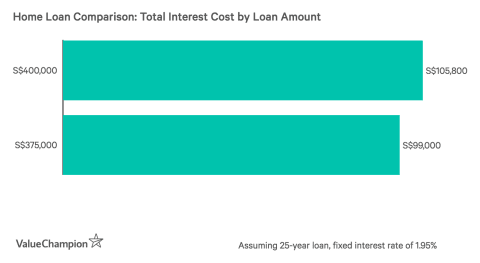

With that said, this requirement may also save these individuals money in the long run. For instance, the upfront down payment isn't necessarily a cost since it is going towards your own ownership value of the property. Additionally, making a larger down payment can reduce the total cost of your loan in terms of interest payments. For example, under the new rules, a S$500,000 home requires a down payment of at least S$125,000, while it previously required a S$100,000 down payment. Assuming that the home buyer makes the minimum down payment, he could save almost S$7,000 or more in interest over the course of the loan.